The Asset-Based Lending market is a financial sector that provides businesses with access to capital by using their assets as collateral. Asset-based lending allows companies to borrow funds based on the value of their assets, such as accounts receivable, inventory, equipment, and real estate. This form of lending offers flexibility and liquidity to businesses that may not qualify for traditional bank loans. Asset-based loans are typically structured as revolving lines of credit, providing businesses with ongoing access to funds as they need them. This market has gained popularity among small and medium-sized enterprises (SMEs) seeking working capital to support their growth and operations.

Meaning

Asset-Based Lending refers to a financing method in which businesses use their assets as collateral to secure a loan. The lender evaluates the value of the assets, such as accounts receivable, inventory, and equipment, and extends credit based on a percentage of their appraised worth. If the borrower defaults on the loan, the lender can seize and sell the assets to recover the outstanding debt. This type of lending is commonly used by businesses to fund working capital needs, manage cash flow, finance expansion plans, and address short-term financial challenges.

Executive Summary

The Asset-Based Lending market has witnessed significant growth in recent years, driven by the increasing demand for flexible financing options among businesses. SMEs, in particular, have embraced asset-based lending as an alternative to traditional bank loans, as it offers greater accessibility and less stringent qualification requirements. The market is characterized by a diverse range of lenders, including commercial banks, non-bank financial institutions, and private equity firms. The competitive landscape is highly fragmented, with players offering varying terms, interest rates, and asset valuation methodologies.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Growing Demand for Working Capital: Businesses across industries require working capital to fund day-to-day operations, manage inventory, and cover operating expenses. Asset-based lending provides a valuable solution for businesses to access the necessary funds quickly and efficiently.

Flexibility and Liquidity: Asset-based loans offer flexibility in terms of borrowing capacity, repayment schedules, and collateral options. This flexibility allows businesses to adjust their borrowing based on their evolving needs and provides them with immediate liquidity.

Alternative to Traditional Bank Loans: Asset-based lending serves as an alternative financing option for businesses that may not qualify for traditional bank loans due to limited credit history, high-risk profile, or lack of collateral. It provides an avenue for these businesses to secure the necessary funds and support their growth aspirations.

Industry-Specific Expertise: Asset-based lenders often specialize in specific industries, such as manufacturing, retail, or healthcare. This industry-specific expertise allows lenders to better understand the unique challenges and opportunities within each sector and provide tailored lending solutions.

Market Drivers

Increasing Demand for Working Capital: Businesses require adequate working capital to fund their day-to-day operations, manage inventory, and meet short-term financial obligations. Asset-based lending provides a flexible and accessible source of working capital, enabling businesses to meet their liquidity needs.

Limited Access to Traditional Financing: Many businesses, particularly SMEs, face challenges in accessing traditional bank loans due to stringent qualification requirements, lack of collateral, or limited credit history. Asset-based lending offers an alternative financing option, leveraging the value of their assets to secure the necessary funds.

Growth of Non-Bank Lenders: The rise of non-bank financial institutions, such as asset-based lending firms and private equity funds, has expanded the availability of asset-based lending options. These lenders offer more flexible terms and a streamlined approval process compared to traditional banks.

Global Economic Conditions: Economic conditions, such as market volatility, fluctuations in interest rates, and changes in trade policies, can impact businesses’ financing options. Asset-based lending provides a stable financing alternative, as it relies on the value of tangible assets rather than market conditions.

Market Restraints

Risk of Asset Value Fluctuation: The value of assets used as collateral in asset-based lending can fluctuate over time. Economic factors, market conditions, and industry-specific challenges can impact the value of assets, which may affect the borrower’s ability to secure the desired loan amount.

Higher Interest Rates: Asset-based loans often come with higher interest rates compared to traditional bank loans. This is due to the perceived higher risk associated with asset-based lending, as the collateral value determines the loan amount rather than the borrower’s creditworthiness.

Collateral Evaluation and Monitoring: Asset-based lending requires a rigorous evaluation and monitoring process to assess the value and condition of the assets used as collateral. Lenders must invest resources in appraisals, audits, and ongoing monitoring to ensure the assets maintain their value and remain adequate collateral.

Potential Ownership Loss: If a borrower defaults on an asset-based loan, the lender has the right to seize and liquidate the collateral. In some cases, this may result in the borrower losing ownership of their assets, which can have significant consequences for the business.

Market Opportunities

Technological Advancements: The integration of technology, such as automation, data analytics, and artificial intelligence, presents opportunities to streamline the asset-based lending process. Digitizing workflows, enhancing risk assessment models, and leveraging data insights can improve efficiency, reduce operational costs, and enhance the borrower experience.

Expansion into Emerging Markets: Asset-based lending has significant growth potential in emerging markets, where access to traditional financing options may be limited. As these markets continue to develop and businesses seek working capital solutions, asset-based lending can provide a valuable avenue for growth.

Collaboration with Fintech Innovators: Collaboration between asset-based lenders and fintech companies can drive innovation and improve the lending experience. Fintech solutions, such as online platforms, digital underwriting, and alternative credit scoring models, can enhance efficiency and accessibility in the asset-based lending process.

Industry-Specific Lending Solutions: Asset-based lenders can capitalize on industry-specific lending solutions by developing expertise in niche sectors. Understanding the unique financing needs and risk profiles of specific industries allows lenders to tailor their offerings and provide customized solutions.

Market Dynamics

Asset-Based Lending market dynamics are influenced by various factors, including economic conditions, regulatory changes, technological advancements, and market competition. Key dynamics include:

Economic Conditions: Economic factors such as GDP growth, interest rates, inflation, and industry performance can impact the demand for asset-based lending. During periods of economic expansion, businesses may require additional working capital to support growth initiatives, while economic downturns may lead to increased demand for short-term financing.

Regulatory Environment: Regulatory changes, including lending regulations, accounting standards, and consumer protection laws, can impact the asset-based lending landscape. Lenders must stay informed and compliant with regulatory requirements to ensure transparency, fairness, and risk mitigation.

Technological Advancements: The adoption of technology, such as digital platforms, automation, and data analytics, can streamline the asset-based lending process. Technology-driven solutions enhance efficiency, reduce manual errors, and provide faster access to funds for borrowers.

Market Competition: The asset-based lending market is highly competitive, with various financial institutions and alternative lenders vying for market share. Lenders differentiate themselves based on factors such as interest rates, loan terms, customer service, industry specialization, and value-added services.

Industry Consolidation: The asset-based lending market is subject to consolidation as larger financial institutions acquire smaller players or form strategic partnerships. Consolidation can lead to increased market concentration, enhanced capabilities, and expanded product offerings.

Regional Analysis

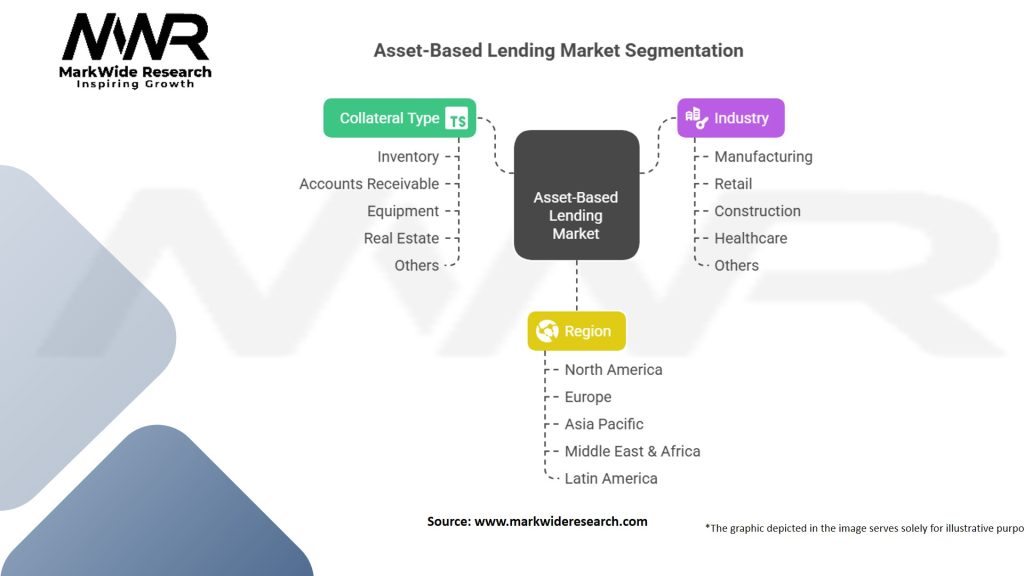

The asset-based lending market exhibits regional variations influenced by economic factors, industry dynamics, and regulatory frameworks. Key regions in the market include:

North America: The North American market is characterized by a robust financial sector and a strong presence of traditional banks, non-bank lenders, and private equity firms. The United States, in particular, represents a significant portion of the asset-based lending market, driven by the country’s economic strength and diverse business landscape.

Europe: European countries have a well-established asset-based lending market, with the United Kingdom, Germany, and France being key players. The market in Europe is influenced by regulatory frameworks, economic conditions, and cross-border lending activities.

Asia Pacific: The Asia Pacific region, including countries like China, India, Japan, and Australia, presents significant growth opportunities for asset-based lending. The region’s expanding SME sector, increasing demand for working capital, and evolving regulatory environment contribute to market growth.

Latin America: Latin American countries, such as Brazil, Mexico, and Argentina, have seen increased adoption of asset-based lending as businesses seek alternative financing options. Economic growth, trade activities, and industry-specific developments impact the market dynamics in the region.

Middle East and Africa: The asset-based lending market in the Middle East and Africa region is influenced by economic diversification efforts, infrastructure development projects, and the presence of multinational corporations. The market dynamics vary across countries due to different economic and regulatory factors.

Competitive Landscape

Leading Companies in the Asset-Based Lending Market:

Wells Fargo & Company

JPMorgan Chase & Co.

Bank of America Corporation

Citigroup Inc.

PNC Financial Services Group, Inc.

HSBC Holdings plc

Goldman Sachs Group, Inc.

Morgan Stanley

U.S. Bancorp

SunTrust Banks, Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

The asset-based lending market can be segmented based on various factors:

By Industry: Asset-based lenders may specialize in specific industries, such as manufacturing, retail, healthcare, or transportation. Each industry has unique financing needs, risk profiles, and asset classes, which influence the lending terms and conditions.

By Type of Assets: Asset-based lending can be categorized based on the type of assets used as collateral. This may include accounts receivable financing, inventory financing, equipment financing, real estate financing, or a combination of multiple asset classes.

By Business Size: Asset-based lending solutions cater to businesses of different sizes, ranging from small and medium-sized enterprises (SMEs) to large corporations. The lending terms, borrowing capacity, and requirements may vary based on the business size.

By Geography: The asset-based lending market exhibits regional variations, influenced by economic factors, industry dynamics, and regulatory frameworks. Regional segmentation allows for a deeper analysis of market trends and opportunities.

Category-wise Insights

Accounts Receivable Financing: Accounts receivable financing, also known as invoice factoring, involves borrowing funds against outstanding customer invoices. This category of asset-based lending provides immediate cash flow to businesses, allowing them to meet their working capital needs while waiting for customers to settle their invoices.

Inventory Financing: Inventory financing allows businesses to borrow funds based on the value of their inventory. It helps businesses optimize their cash flow by converting inventory into working capital. This category is particularly relevant for industries with significant inventory holdings, such as retail and manufacturing.

Equipment Financing: Equipment financing involves using equipment as collateral to secure a loan. Businesses can borrow funds to purchase or lease equipment, enabling them to expand operations, upgrade machinery, or replace outdated equipment. This category is relevant for industries dependent on specialized equipment, such as construction, healthcare, or transportation.

Real Estate Financing: Real estate financing involves using commercial or residential properties as collateral to secure a loan. Businesses can leverage the value of their properties to access funds for expansion, renovations, or real estate investments. This category is particularly relevant for industries such as real estate development, hospitality, or construction.

Mixed Collateral Financing: Mixed collateral financing involves using a combination of assets, such as accounts receivable, inventory, and equipment, as collateral for a loan. This category provides businesses with flexibility in utilizing multiple asset classes to secure the necessary funds.

Key Benefits for Industry Participants and Stakeholders

Access to Working Capital: Asset-based lending provides businesses with access to working capital, enabling them to manage cash flow, meet short-term obligations, and seize growth opportunities.

Flexible Financing Options: Asset-based lending offers flexibility in terms of borrowing capacity, repayment schedules, and collateral options. This flexibility allows businesses to adjust their borrowing based on their evolving needs and operational requirements.

Speed and Efficiency: Asset-based lending provides a streamlined and efficient lending process compared to traditional bank loans. The evaluation of assets as collateral allows for faster approvals, reducing the time required to access funds.

Improved Cash Flow Management: Asset-based lending helps businesses improve cash flow management by converting assets into immediate liquidity. It allows businesses to unlock the value of their assets and utilize the funds for operational needs or investment opportunities.

Growth and Expansion Support: Asset-based lending can support business growth and expansion plans by providing the necessary funds for acquisitions, market expansion, product development, or infrastructure investments.

Mitigation of Risk: Asset-based lending reduces the risk for lenders by using tangible assets as collateral. This mitigates the lender’s exposure to default and provides a level of security for the loan.

SWOT Analysis

Strengths:

Flexible borrowing capacity based on asset value

Faster access to funds compared to traditional loans

Industry-specific expertise and tailored solutions

Ability to support businesses with limited credit history or collateral

Weaknesses:

Higher interest rates compared to traditional bank loans

Potential loss of assets if the borrower defaults on the loan

Vulnerability to fluctuations in asset values

Requires thorough evaluation and monitoring of collateral assets

Opportunities:

Integration of technology to streamline lending processes

Expansion into emerging markets with limited financing options

Collaboration with fintech companies for innovative solutions

Customization of lending offerings for specific industries

Threats:

Competitive landscape with various lenders vying for market share

Regulatory changes impacting lending practices and requirements

Economic downturns affecting borrower ability to repay loans

Risk of asset depreciation or devaluation impacting loan value

Market Key Trends

Technology Integration: The asset-based lending market is witnessing the integration of technology, including online platforms, automation, data analytics, and artificial intelligence. These technologies streamline the lending process, enhance risk assessment models, and improve customer experience.

Industry-Specific Lending Solutions: Lenders are increasingly focusing on industry-specific lending solutions, leveraging their expertise and understanding of unique industry challenges. This allows for customized lending offerings tailored to the specific needs of businesses in various sectors.

Rise of Non-Bank Lenders: Non-bank financial institutions, such as asset-based lending firms and private equity funds, are gaining prominence in the market. These lenders offer alternative financing options and more flexible terms compared to traditional banks.

Demand for Sustainable Financing: There is a growing demand for sustainable financing options in the asset-based lending market. Businesses are seeking lenders that incorporate environmental, social, and governance (ESG) factors into their lending practices.

Emphasis on Risk Management: Lenders are placing greater emphasis on risk management strategies to mitigate default risk and ensure the quality of collateral assets. This includes thorough due diligence, collateral valuation methodologies, and ongoing monitoring of borrower activities.

Covid-19 Impact

The Covid-19 pandemic had a significant impact on the asset-based lending market, with both challenges and opportunities emerging:

Economic Uncertainty: The pandemic led to economic uncertainty, impacting businesses across sectors. Many businesses faced liquidity challenges and sought asset-based lending as a source of working capital to navigate the crisis.

Demand for Emergency Funding: Asset-based lending played a crucial role in providing emergency funding to businesses affected by the pandemic. It helped businesses maintain operations, manage cash flow, and address short-term financial obligations.

Risk Assessment and Asset Valuation: The pandemic highlighted the importance of accurate risk assessment and asset valuation in asset-based lending. Lenders had to evaluate the impact of the pandemic on collateral assets and adjust loan terms accordingly.

Digital Transformation: The pandemic accelerated the digital transformation in the asset-based lending market. Lenders implemented digital platforms, online document submission, and remote appraisal methods to facilitate lending processes amidst social distancing measures.

Industry-Specific Impacts: The pandemic had varying impacts on different industries, with some sectors experiencing significant disruptions while others thrived. Asset-based lenders had to adapt their lending practices and risk assessment models to address these industry-specific challenges.

Key Industry Developments

Technological Advancements: The asset-based lending industry is witnessing advancements in technology, such as the use of blockchain for secure asset verification, digital platforms for streamlined processes, and artificial intelligence for automated risk assessments.

Regulatory Changes: Regulatory frameworks governing asset-based lending are evolving, with new guidelines and requirements being introduced. These changes aim to enhance transparency, consumer protection, and risk management in the industry.

Partnerships and Collaborations: Asset-based lenders are forming partnerships and collaborations with fintech companies, credit rating agencies, and industry-specific organizations to leverage expertise, enhance services, and drive innovation in the market.

Market Consolidation: The asset-based lending market is experiencing consolidation, with larger financial institutions acquiring smaller players or merging with competitors. This consolidation aims to expand market reach, increase capabilities, and improve operational efficiency.

Analyst Suggestions

Embrace Technology: Asset-based lenders should invest in technology and leverage digital solutions to streamline processes, enhance risk assessment models, and improve the customer experience. This includes adopting online platforms, automation, data analytics, and artificial intelligence.

Enhance Risk Management: Lenders should prioritize robust risk management practices, including thorough due diligence, collateral valuation methodologies, and ongoing monitoring of borrower activities. Effective risk management reduces the likelihood of default and strengthens the lender’s position.

Industry Specialization: Lenders can differentiate themselves by developing industry-specific expertise and tailored lending solutions. Understanding the unique needs, risks, and opportunities within specific sectors allows lenders to provide customized financing options.

Collaboration and Partnerships: Collaboration with fintech companies, credit rating agencies, and industry associations can drive innovation and enhance the lending process. Partnerships can provide access to advanced technologies, market insights, and additional resources.

Sustainable Financing: There is a growing demand for sustainable financing options. Lenders should incorporate environmental, social, and governance (ESG) factors into their lending practices to meet the evolving needs of businesses and align with responsible lending principles.

Future Outlook

The asset-based lending market is expected to witness continued growth and evolution in the coming years. Key trends and factors shaping the future outlook include:

Continued Technological Advancements: Technology will play an increasingly significant role in the asset-based lending market. Digital platforms, automation, data analytics, and artificial intelligence will drive efficiency, speed, and risk management.

Focus on Industry Expertise: Lenders will continue to develop industry-specific expertise and tailored lending solutions. This specialization allows lenders to understand the unique needs and risks of different sectors and provide customized financing options.

Expansion into Emerging Markets: Asset-based lending will continue to expand into emerging markets with growing SME sectors and limited access to traditional financing options. These markets present significant growth opportunities for asset-based lenders.

Enhanced Risk Management Practices: Lenders will continue to enhance their risk management practices to mitigate default risk and ensure the quality of collateral assets. Thorough due diligence, collateral valuation methodologies, and ongoing monitoring will be critical.

Sustainable Financing: The demand for sustainable financing options will continue to rise. Lenders will incorporate ESG factors into their lending practices to meet the evolving needs of businesses and align with responsible lending principles.

Conclusion

The asset-based lending market provides businesses with flexible access to working capital by leveraging their assets as collateral. It offers an alternative financing option for businesses that may not qualify for traditional bank loans or require immediate liquidity. The market is characterized by a competitive landscape with various lenders, including traditional banks, non-bank financial institutions, and private equity firms.

Asset-based lending offers several key benefits, including access to working capital, flexible financing options, speed and efficiency, improved cash flow management, and support for growth and expansion. However, there are challenges such as higher interest rates, potential asset loss, and the need for thorough collateral evaluation and monitoring.

What is Asset-Based Lending?

Asset-Based Lending refers to a type of financing where a borrower secures a loan using an asset as collateral. This can include inventory, accounts receivable, or other tangible assets, allowing businesses to access capital based on the value of their assets.

What are the key players in the Asset-Based Lending Market?

Key players in the Asset-Based Lending Market include Wells Fargo, Bank of America, and CIT Group, among others. These companies provide various asset-based financing solutions to businesses across different sectors.

What are the main drivers of growth in the Asset-Based Lending Market?

The main drivers of growth in the Asset-Based Lending Market include the increasing demand for flexible financing options, the rise of small and medium-sized enterprises seeking capital, and the growing need for businesses to leverage their assets for liquidity.

What challenges does the Asset-Based Lending Market face?

Challenges in the Asset-Based Lending Market include fluctuating asset values, regulatory compliance issues, and the potential for increased default risk during economic downturns. These factors can impact lenders’ willingness to provide financing.

What opportunities exist in the Asset-Based Lending Market?

Opportunities in the Asset-Based Lending Market include the expansion of digital lending platforms, the growing trend of alternative financing solutions, and the potential for increased partnerships between lenders and technology firms to enhance service delivery.

What trends are shaping the Asset-Based Lending Market?

Trends shaping the Asset-Based Lending Market include the integration of technology in underwriting processes, the rise of fintech companies offering innovative lending solutions, and a shift towards more personalized lending experiences for borrowers.

Leading Companies in the Asset-Based Lending Market:

Wells Fargo & Company

JPMorgan Chase & Co.

Bank of America Corporation

Citigroup Inc.

PNC Financial Services Group, Inc.

HSBC Holdings plc

Goldman Sachs Group, Inc.

Morgan Stanley

U.S. Bancorp

SunTrust Banks, Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.