444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Asia Pacific semiconductor memory market represents one of the most dynamic and rapidly evolving technology sectors in the global economy. This region has emerged as the epicenter of semiconductor manufacturing and innovation, driven by robust demand from consumer electronics, automotive, data centers, and emerging technologies. The market encompasses various memory technologies including DRAM, NAND flash, NOR flash, and emerging memory solutions that power everything from smartphones to artificial intelligence applications.

Market dynamics in the Asia Pacific region are characterized by intense competition, technological advancement, and significant capital investments from both established players and emerging companies. Countries like South Korea, Taiwan, China, and Japan have established themselves as manufacturing powerhouses, collectively accounting for a substantial portion of global semiconductor memory production. The region benefits from a comprehensive ecosystem that includes raw material suppliers, equipment manufacturers, and end-user industries.

Growth trajectories indicate that the Asia Pacific semiconductor memory market is experiencing robust expansion, with analysts projecting a compound annual growth rate (CAGR) of 8.2% through the forecast period. This growth is fueled by increasing digitalization, the proliferation of connected devices, and the rapid adoption of technologies such as 5G networks, Internet of Things (IoT), and artificial intelligence. The region’s strategic importance continues to grow as global technology companies establish manufacturing facilities and research centers to capitalize on local expertise and cost advantages.

The Asia Pacific semiconductor memory market refers to the comprehensive ecosystem of memory chip design, manufacturing, and distribution activities across the Asia Pacific region. This market encompasses the production and sale of various types of semiconductor memory devices that store data temporarily or permanently in electronic systems. Semiconductor memory serves as the critical component that enables data storage and retrieval in virtually all modern electronic devices, from consumer gadgets to industrial equipment.

Memory technologies within this market include volatile memory such as Dynamic Random Access Memory (DRAM) and Static Random Access Memory (SRAM), which lose data when power is removed, and non-volatile memory including NAND flash, NOR flash, and emerging technologies like 3D XPoint and Resistive RAM (ReRAM). These components are essential for system performance, enabling faster data access, improved multitasking capabilities, and enhanced user experiences across various applications.

Regional significance of the Asia Pacific semiconductor memory market extends beyond manufacturing to include research and development, supply chain management, and technology innovation. The market represents a critical link in the global technology supply chain, with regional companies and facilities serving customers worldwide while also meeting the growing domestic demand for advanced memory solutions.

Strategic positioning of the Asia Pacific semiconductor memory market reflects its dominant role in global technology manufacturing and innovation. The region has established itself as the world’s primary hub for semiconductor memory production, with leading companies investing heavily in advanced manufacturing facilities and cutting-edge technologies. This market leadership is supported by favorable government policies, skilled workforce availability, and established supply chain networks that create competitive advantages for regional players.

Market segmentation reveals diverse opportunities across multiple technology categories and application areas. DRAM technology continues to represent the largest segment, driven by increasing memory requirements in smartphones, servers, and personal computers. Meanwhile, NAND flash memory is experiencing rapid growth due to expanding solid-state drive adoption and increasing storage demands in data centers. Emerging memory technologies are gaining traction, particularly in specialized applications requiring high performance and reliability.

Competitive landscape features a mix of established multinational corporations and emerging regional players, each pursuing different strategies to capture market share. Innovation cycles are accelerating, with companies investing approximately 15-20% of revenue in research and development to maintain technological leadership. The market is characterized by continuous technological advancement, with new memory architectures and manufacturing processes being developed to meet evolving performance and efficiency requirements.

Future prospects indicate sustained growth driven by emerging applications in artificial intelligence, autonomous vehicles, and edge computing. The transition to 5G networks and the expansion of Internet of Things deployments are creating new demand patterns that favor advanced memory solutions with improved performance characteristics and energy efficiency.

Technology evolution in the Asia Pacific semiconductor memory market is accelerating at an unprecedented pace, with manufacturers transitioning to advanced process nodes and innovative memory architectures. The following key insights highlight the most significant developments shaping market dynamics:

Innovation trends demonstrate the market’s commitment to addressing evolving customer needs through technological advancement. Companies are developing memory solutions with improved performance, reduced power consumption, and enhanced reliability to support next-generation applications and use cases.

Digital transformation across industries serves as the primary catalyst driving semiconductor memory demand throughout the Asia Pacific region. The accelerating pace of digitalization in business operations, consumer behavior, and government services is creating unprecedented requirements for data storage and processing capabilities. This transformation is particularly pronounced in emerging economies where rapid modernization is driving technology adoption across multiple sectors simultaneously.

Consumer electronics proliferation continues to fuel substantial memory demand, with smartphone penetration reaching 85% in developed markets and growing rapidly in emerging economies. The evolution toward more sophisticated devices with enhanced capabilities requires increasingly advanced memory solutions. 5G smartphone adoption is particularly significant, as these devices require substantially more memory to support enhanced features and applications.

Data center expansion represents another critical growth driver, as cloud computing adoption accelerates across the region. Enterprises are migrating workloads to cloud platforms, while hyperscale data center operators are expanding capacity to meet growing demand. This trend is driving substantial requirements for high-performance memory solutions that can support intensive computing workloads and large-scale data processing applications.

Automotive electrification and the development of autonomous driving technologies are creating new memory market segments with specialized requirements. Modern vehicles incorporate numerous electronic systems that require reliable, high-performance memory solutions. The transition to electric vehicles and the integration of advanced driver assistance systems are significantly increasing memory content per vehicle.

Artificial intelligence and machine learning applications are driving demand for specialized memory architectures optimized for AI workloads. These applications require memory solutions with high bandwidth, low latency, and energy efficiency characteristics that differ from traditional computing requirements.

Cyclical market dynamics present ongoing challenges for the Asia Pacific semiconductor memory market, with periodic downturns affecting pricing, profitability, and investment decisions. The industry experiences regular cycles of oversupply and undersupply that can significantly impact financial performance and strategic planning. These cycles are often exacerbated by the long lead times required for capacity expansion and the substantial capital investments involved in semiconductor manufacturing.

Geopolitical tensions and trade policy uncertainties create additional complexity for market participants, particularly those with global operations and supply chains. Export restrictions, tariff policies, and technology transfer limitations can affect market access and competitive positioning. Companies must navigate evolving regulatory environments while maintaining operational efficiency and market competitiveness.

Capital intensity requirements for semiconductor memory manufacturing present barriers to entry and expansion for many companies. Advanced manufacturing facilities require investments that can exceed several billion dollars, with ongoing technology development costs adding to financial requirements. This capital intensity limits the number of companies that can compete effectively in leading-edge memory technologies.

Technical complexity associated with advanced memory technologies creates challenges in manufacturing yield, product reliability, and time-to-market. As memory devices become more sophisticated and manufacturing processes more complex, companies face increasing difficulties in achieving acceptable production yields and maintaining quality standards.

Supply chain vulnerabilities have become more apparent following recent global disruptions, highlighting dependencies on specific suppliers, materials, and manufacturing locations. Companies are working to address these vulnerabilities, but solutions often require significant time and investment to implement effectively.

Emerging memory technologies present significant opportunities for companies willing to invest in next-generation solutions. Technologies such as 3D XPoint, Resistive RAM, and Magnetoresistive RAM offer unique performance characteristics that can address specific application requirements. These technologies are particularly valuable for applications requiring high-speed data access, non-volatility, and endurance characteristics that exceed traditional memory capabilities.

Edge computing expansion is creating new market segments with specialized memory requirements. As processing capabilities move closer to data sources, there is growing demand for memory solutions optimized for edge environments. These applications often require memory with specific power, size, and reliability characteristics that differ from traditional data center or consumer applications.

Internet of Things proliferation across industrial, automotive, and consumer applications is driving demand for specialized memory solutions. IoT devices often require memory with ultra-low power consumption, small form factors, and cost-effective pricing. The diversity of IoT applications creates opportunities for customized memory solutions tailored to specific use cases and requirements.

Automotive technology evolution continues to create new opportunities as vehicles become more sophisticated and connected. The development of autonomous driving capabilities, advanced infotainment systems, and vehicle-to-everything communication requires memory solutions with automotive-grade reliability and performance characteristics.

Artificial intelligence acceleration is driving demand for memory architectures optimized for AI and machine learning workloads. These applications benefit from memory solutions with high bandwidth, parallel processing capabilities, and energy efficiency characteristics that can improve AI system performance and reduce operational costs.

Competitive intensity within the Asia Pacific semiconductor memory market continues to drive innovation and efficiency improvements across the industry. Companies are competing on multiple dimensions including technology leadership, manufacturing cost, product quality, and customer service. This competition is beneficial for end users but creates pressure on profit margins and requires continuous investment in research and development.

Technology roadmaps are evolving rapidly as companies pursue different approaches to address scaling challenges and performance requirements. The traditional approach of shrinking device dimensions is becoming more difficult and expensive, leading to exploration of alternative architectures and materials. 3D memory structures have emerged as a key technology for increasing storage density while managing manufacturing costs.

Customer requirements are becoming more sophisticated and diverse as applications evolve and new use cases emerge. End users are demanding memory solutions with specific performance, power, and reliability characteristics tailored to their applications. This trend is driving market segmentation and creating opportunities for specialized products and services.

Supply chain evolution is ongoing as companies work to improve resilience, reduce costs, and enhance flexibility. The semiconductor memory industry relies on complex global supply chains that include raw materials, manufacturing equipment, and specialized services. Recent disruptions have highlighted the importance of supply chain diversification and risk management.

Investment patterns reflect the industry’s commitment to maintaining technological leadership and expanding capacity. According to MarkWide Research analysis, regional companies are allocating approximately 18% of revenues to capital expenditures and research and development activities to support growth and innovation objectives.

Comprehensive analysis of the Asia Pacific semiconductor memory market employs multiple research methodologies to ensure accuracy and completeness of findings. Primary research activities include extensive interviews with industry executives, technology experts, and market participants across the value chain. These interviews provide insights into market trends, competitive dynamics, and future outlook that complement quantitative data analysis.

Secondary research encompasses analysis of company financial reports, industry publications, government statistics, and technology roadmaps. This research provides historical context and quantitative foundations for market analysis. Data sources include regulatory filings, industry associations, and specialized research organizations that track semiconductor market developments.

Market modeling techniques incorporate both bottom-up and top-down approaches to validate market size estimates and growth projections. Bottom-up analysis examines individual market segments, applications, and geographic regions to build comprehensive market understanding. Top-down analysis considers macroeconomic factors, industry trends, and technology adoption patterns that influence overall market development.

Expert validation processes ensure research findings accurately reflect market realities and industry perspectives. Independent experts review analysis methodologies, data sources, and conclusions to identify potential biases or gaps in coverage. This validation process enhances the reliability and credibility of research outcomes.

Continuous monitoring of market developments ensures research remains current and relevant as conditions evolve. Regular updates incorporate new data, emerging trends, and changing competitive dynamics that may affect market outlook and strategic implications.

South Korea maintains its position as a global leader in semiconductor memory manufacturing, with major companies operating advanced fabrication facilities and research centers. The country benefits from strong government support, skilled workforce, and established supply chain networks. South Korean companies control approximately 45% of global DRAM production and maintain significant market share in NAND flash memory. Continued investment in next-generation technologies and manufacturing capabilities supports the country’s competitive position.

Taiwan serves as another critical hub for semiconductor memory manufacturing and technology development. The island’s strategic location, advanced infrastructure, and technology expertise make it an attractive location for memory manufacturing operations. Taiwanese companies are particularly strong in specialty memory applications and contract manufacturing services, providing flexibility and cost advantages for global customers.

China represents the fastest-growing segment of the Asia Pacific semiconductor memory market, driven by substantial government investment and growing domestic demand. Chinese companies are investing heavily in memory manufacturing capabilities and technology development to reduce dependence on imports. The domestic market for memory products is expanding rapidly as Chinese technology companies grow and local demand increases.

Japan continues to play an important role in the semiconductor memory ecosystem, particularly in materials, equipment, and specialized memory applications. Japanese companies maintain leadership positions in memory materials and manufacturing equipment that are essential for advanced memory production. The country’s focus on high-value applications and technology innovation supports its continued relevance in the global market.

Southeast Asian countries including Malaysia, Thailand, and Singapore serve important roles in semiconductor assembly, testing, and packaging operations. These countries provide cost-effective manufacturing capabilities and strategic locations for serving regional markets. Growing investment in advanced packaging technologies is enhancing their value proposition in the memory supply chain.

Market leadership in the Asia Pacific semiconductor memory market is concentrated among several major companies that have established dominant positions through technology innovation, manufacturing scale, and customer relationships. These companies compete intensively across multiple dimensions including product performance, manufacturing cost, and technology roadmaps.

Strategic initiatives among leading companies include capacity expansion, technology development partnerships, and vertical integration efforts. Companies are investing in advanced manufacturing processes, new product development, and supply chain optimization to maintain competitive advantages and serve evolving customer requirements.

Innovation focus areas include development of next-generation memory architectures, improvement of manufacturing efficiency, and expansion into emerging application areas. Companies are also investing in artificial intelligence and machine learning capabilities to enhance product development and manufacturing operations.

By Technology:

By Application:

By End-User:

DRAM Technology Segment continues to represent the largest portion of the Asia Pacific semiconductor memory market, driven by increasing memory requirements in computing and mobile applications. DDR5 DRAM adoption is accelerating as system manufacturers transition to next-generation platforms requiring higher bandwidth and improved power efficiency. Server applications are driving demand for high-capacity DRAM modules, while mobile applications require memory solutions optimized for power consumption and form factor constraints.

NAND Flash Segment is experiencing robust growth driven by expanding storage requirements across multiple applications. 3D NAND technology has become the dominant architecture, enabling higher storage densities and improved cost-effectiveness. Solid-state drive adoption in both consumer and enterprise applications is driving substantial NAND flash demand, while mobile applications require memory solutions with specific performance and power characteristics.

Automotive Memory Segment is emerging as a high-growth category with specialized requirements for reliability, temperature tolerance, and functional safety. Advanced driver assistance systems and autonomous driving technologies require memory solutions that can operate reliably in automotive environments while providing the performance needed for real-time processing applications.

Emerging Memory Technologies are gaining traction in specialized applications where traditional memory technologies cannot meet specific performance requirements. Storage-class memory applications are driving interest in technologies that combine the speed of DRAM with the non-volatility of NAND flash, creating new product categories and market opportunities.

Industrial Applications require memory solutions with extended temperature ranges, enhanced reliability, and long product lifecycles. These applications often involve smaller volumes but higher margins, making them attractive for companies seeking to diversify their customer base and reduce exposure to consumer market volatility.

Technology Companies benefit from access to advanced memory solutions that enable product differentiation and improved performance. The availability of diverse memory technologies allows system designers to optimize their products for specific applications and use cases. Collaboration opportunities with memory manufacturers can accelerate product development and time-to-market while reducing development costs and risks.

Manufacturing Partners gain access to established supply chains, proven manufacturing processes, and technical expertise that can improve operational efficiency and product quality. The semiconductor memory industry’s focus on continuous improvement and cost reduction creates opportunities for suppliers to participate in technology advancement and market growth.

End Users benefit from improved system performance, enhanced functionality, and better user experiences enabled by advanced memory technologies. The industry’s commitment to innovation ensures that memory solutions continue to evolve to meet changing application requirements and performance expectations.

Investors can participate in a market with strong growth prospects driven by fundamental technology trends and expanding application areas. The industry’s capital-intensive nature creates barriers to entry that can protect established companies’ market positions and profitability over time.

Regional Economies benefit from high-value manufacturing activities, technology development capabilities, and skilled employment opportunities. The semiconductor memory industry’s presence supports broader technology ecosystems and contributes to economic development and competitiveness.

Research Institutions gain opportunities to collaborate with industry leaders on advanced technology development projects. These partnerships can accelerate research progress while providing practical applications for academic research and development activities.

Strengths:

Weaknesses:

Opportunities:

Threats:

Artificial Intelligence Integration is driving fundamental changes in memory architecture requirements and product development priorities. AI workloads require memory solutions with high bandwidth, parallel processing capabilities, and energy efficiency characteristics that differ significantly from traditional computing applications. This trend is creating opportunities for specialized memory products and driving innovation in memory-centric computing architectures.

Edge Computing Expansion is creating new market segments with unique memory requirements. As processing capabilities move closer to data sources, there is growing demand for memory solutions optimized for edge environments with specific power, size, and reliability constraints. This trend is driving development of specialized memory products tailored to edge computing applications.

Sustainability Initiatives are becoming increasingly important as companies and customers focus on environmental impact and energy efficiency. Memory manufacturers are developing products with reduced power consumption and implementing more sustainable manufacturing processes. This trend is driving innovation in low-power memory technologies and creating competitive advantages for companies that can demonstrate environmental leadership.

Memory-Centric Computing architectures are emerging as alternatives to traditional von Neumann computing models. These approaches integrate memory and processing capabilities to reduce data movement and improve system efficiency. Processing-in-memory and near-data computing concepts are gaining attention as potential solutions for data-intensive applications.

Automotive Technology Evolution continues to drive demand for specialized memory solutions with automotive-grade reliability and performance characteristics. The transition to electric vehicles and development of autonomous driving capabilities are significantly increasing memory content per vehicle and creating new market opportunities.

5G Network Deployment is creating new infrastructure requirements that drive demand for high-performance memory solutions. 5G base stations and network equipment require memory with specific performance and reliability characteristics to support enhanced network capabilities and services.

Technology Advancement initiatives across the Asia Pacific semiconductor memory market are accelerating as companies invest in next-generation manufacturing processes and memory architectures. Recent developments include advancement to smaller process nodes, implementation of 3D memory structures, and exploration of alternative materials and device concepts that can extend memory technology roadmaps.

Capacity Expansion projects are ongoing across the region as companies respond to growing demand and work to maintain competitive positioning. Major manufacturers are investing in new fabrication facilities and expanding existing operations to increase production capacity for both traditional and emerging memory technologies. These investments represent commitments of several billion dollars and demonstrate confidence in long-term market growth prospects.

Strategic Partnerships are becoming more common as companies seek to share development costs, access complementary technologies, and accelerate time-to-market for new products. Recent partnerships include collaborations between memory manufacturers and system companies, joint development agreements for emerging technologies, and supply chain partnerships that enhance operational efficiency.

Acquisition Activity continues to reshape the competitive landscape as companies seek to acquire technologies, manufacturing capabilities, or market access. Recent transactions have focused on emerging memory technologies, specialized applications, and regional market expansion opportunities.

Government Support programs across the region are providing funding and policy support for semiconductor memory development and manufacturing. These initiatives reflect recognition of the strategic importance of semiconductor capabilities and aim to enhance regional competitiveness in global markets.

Research Collaboration between industry and academic institutions is expanding as companies seek to access cutting-edge research and develop next-generation technologies. These partnerships are particularly important for exploring fundamental advances in memory materials, device physics, and system architectures.

Investment Prioritization should focus on technologies and applications with strong growth prospects and sustainable competitive advantages. MWR analysis suggests that companies prioritize investments in emerging memory technologies, automotive applications, and artificial intelligence-optimized solutions that can command premium pricing and provide differentiation in competitive markets.

Supply Chain Diversification is essential for managing risks and ensuring operational continuity in an increasingly complex global environment. Companies should develop multiple supplier relationships, invest in supply chain visibility tools, and consider regional supply chain strategies that can reduce dependency on single sources or geographic regions.

Technology Roadmap Development requires careful balance between advancing existing technologies and exploring alternative approaches. Companies should maintain strong positions in current technology generations while investing in research and development for next-generation solutions that can address emerging application requirements.

Market Segmentation Strategy should recognize the increasing diversity of memory requirements across different applications and use cases. Companies can benefit from developing specialized products for high-value segments while maintaining cost-competitive solutions for volume markets.

Partnership Strategy should leverage collaboration opportunities to share development costs, access complementary capabilities, and accelerate innovation. Strategic partnerships can be particularly valuable for emerging technologies where development costs and risks are high.

Sustainability Integration should become a core component of product development and manufacturing operations. Companies that can demonstrate environmental leadership while maintaining performance and cost competitiveness will be well-positioned for long-term success.

Long-term growth prospects for the Asia Pacific semiconductor memory market remain positive, supported by fundamental technology trends and expanding application areas. The continued digitalization of business and consumer activities will drive sustained demand for memory solutions across multiple market segments. Emerging technologies including artificial intelligence, autonomous systems, and edge computing are expected to create new market opportunities with specialized requirements.

Technology evolution will continue to drive market development as manufacturers advance to smaller process nodes and explore alternative memory architectures. The transition to 3D memory structures will continue, while emerging memory technologies may begin to gain significant market traction in specialized applications. Integration of memory with processing capabilities represents a potential paradigm shift that could create new product categories and market dynamics.

Regional dynamics are expected to evolve as countries implement policies to enhance domestic semiconductor capabilities and reduce import dependencies. This trend may lead to increased regional manufacturing capacity and technology development activities. MarkWide Research projects that regional production capacity could increase by 25-30% over the next five years as new facilities come online and existing operations expand.

Application diversification will continue as memory requirements expand beyond traditional computing and consumer electronics into automotive, industrial, and infrastructure applications. These new applications often have specialized requirements that can support premium pricing and provide opportunities for differentiation.

Competitive landscape evolution will likely include continued consolidation as companies seek scale advantages and technology access. Strategic partnerships and joint ventures may become more common as development costs increase and technology complexity grows. Companies that can successfully navigate these dynamics while maintaining innovation capabilities will be best positioned for long-term success.

The Asia Pacific semiconductor memory market represents a dynamic and rapidly evolving sector that plays a critical role in global technology advancement. The region’s established manufacturing capabilities, innovation focus, and comprehensive ecosystem provide strong foundations for continued growth and market leadership. Technological advancement continues to drive market development, with companies investing heavily in next-generation memory solutions and manufacturing processes.

Market opportunities are expanding as new applications emerge and existing use cases become more sophisticated. The growth of artificial intelligence, autonomous systems, edge computing, and 5G networks is creating demand for specialized memory solutions with unique performance characteristics. These trends support positive long-term growth prospects while also creating challenges related to technology development complexity and capital requirements.

Strategic success in this market will require companies to balance multiple priorities including technology innovation, manufacturing efficiency, supply chain resilience, and market diversification. The most successful companies will be those that can maintain leadership in existing technologies while successfully developing capabilities in emerging areas. Collaboration and partnership strategies will become increasingly important as development costs increase and technology complexity grows.

The Asia Pacific semiconductor memory market is well-positioned to continue its leadership role in global technology development, supported by strong regional capabilities, growing domestic demand, and expanding international market opportunities. Companies that can successfully navigate the challenges and capitalize on the opportunities in this dynamic market will be well-positioned for sustained growth and profitability in the years ahead.

What is Semiconductor Memory?

Semiconductor memory refers to a type of computer memory that is made using semiconductor technology, which includes various forms of volatile and non-volatile memory such as DRAM, SRAM, and flash memory. These components are essential for data storage and processing in electronic devices.

What are the key players in the Asia Pacific Semiconductor Memory Market?

Key players in the Asia Pacific Semiconductor Memory Market include Samsung Electronics, SK Hynix, Micron Technology, and Toshiba, among others. These companies are leading the development and production of advanced memory solutions for various applications.

What are the main drivers of the Asia Pacific Semiconductor Memory Market?

The main drivers of the Asia Pacific Semiconductor Memory Market include the increasing demand for high-performance computing, the growth of mobile devices, and the expansion of data centers. These factors are pushing the need for advanced memory technologies.

What challenges does the Asia Pacific Semiconductor Memory Market face?

The Asia Pacific Semiconductor Memory Market faces challenges such as supply chain disruptions, fluctuating raw material prices, and intense competition among manufacturers. These issues can impact production efficiency and pricing strategies.

What opportunities exist in the Asia Pacific Semiconductor Memory Market?

Opportunities in the Asia Pacific Semiconductor Memory Market include the rise of artificial intelligence and machine learning applications, which require advanced memory solutions, and the increasing adoption of Internet of Things (IoT) devices. These trends are expected to drive innovation and growth.

What trends are shaping the Asia Pacific Semiconductor Memory Market?

Trends shaping the Asia Pacific Semiconductor Memory Market include the shift towards higher capacity and faster memory solutions, the development of 3D NAND technology, and the growing focus on energy-efficient memory products. These innovations are crucial for meeting the demands of modern computing.

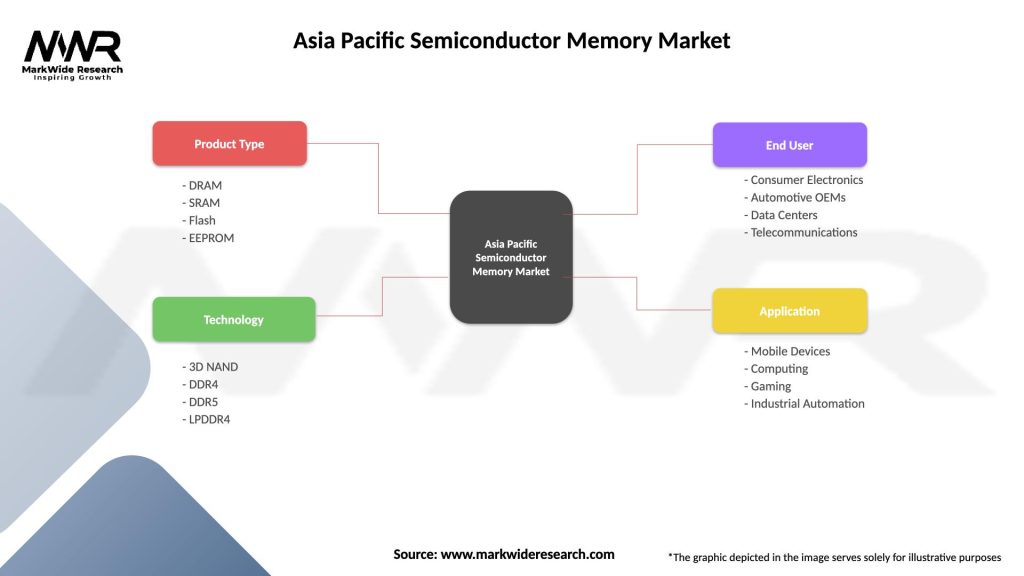

Asia Pacific Semiconductor Memory Market

| Segmentation Details | Description |

|---|---|

| Product Type | DRAM, SRAM, Flash, EEPROM |

| Technology | 3D NAND, DDR4, DDR5, LPDDR4 |

| End User | Consumer Electronics, Automotive OEMs, Data Centers, Telecommunications |

| Application | Mobile Devices, Computing, Gaming, Industrial Automation |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Asia Pacific Semiconductor Memory Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.