Market Overview: The Asia-Pacific Open Banking market stands at the forefront of financial innovation, reshaping traditional banking landscapes and fostering enhanced connectivity across the region. Open Banking, driven by technological advancements and regulatory initiatives, is transforming how financial services are delivered and consumed. This comprehensive article delves into the intricacies of the Asia-Pacific Open Banking market, exploring key trends, market drivers, challenges, and the vast opportunities it presents.

Meaning: Open Banking refers to a financial model that allows third-party financial service providers to access and utilize consumer banking data through Application Programming Interfaces (APIs). By enabling the secure exchange of data between banks and authorized third-party providers, Open Banking aims to enhance competition, drive innovation, and empower consumers with more personalized and efficient financial services.

Executive Summary: The Asia-Pacific Open Banking market has experienced remarkable growth, propelled by a confluence of factors including regulatory mandates, technological advancements, and shifting consumer expectations. As financial ecosystems embrace openness, the market offers a dynamic landscape of opportunities for banks, FinTechs, and other stakeholders. Understanding the key market insights is essential for navigating this evolving landscape successfully.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights:

Regulatory Catalysts: Regulatory bodies across Asia-Pacific, recognizing the transformative potential of Open Banking, have introduced frameworks to facilitate its implementation. Regulatory initiatives, such as the Revised Payment Services Directive (PSD2) in Europe, have inspired similar measures in the region to promote competition and innovation.

Technological Advancements: Rapid advancements in technology, including cloud computing, artificial intelligence, and blockchain, have played a pivotal role in the growth of Open Banking. These technologies underpin the development of secure, efficient, and scalable API-driven ecosystems.

Ecosystem Collaboration: Open Banking encourages collaboration between traditional financial institutions and FinTech innovators. Strategic partnerships and collaborations between banks and FinTechs are fostering the creation of diverse and customer-centric financial solutions.

Consumer-Centric Approach: Open Banking places greater control in the hands of consumers by allowing them to share their financial data securely with third-party providers. This shift toward a consumer-centric approach is driving the development of personalized and on-demand financial services.

Market Drivers:

Enhanced Customer Experience: Open Banking enables the creation of customer-centric financial products and services. By leveraging data from multiple sources, financial institutions can offer more personalized and tailored solutions, enhancing the overall customer experience.

Increased Competition: The opening up of banking data to third-party providers fosters increased competition within the financial services sector. New entrants, including FinTech startups, can leverage Open Banking APIs to offer innovative and competitive products.

Innovation and Product Development: Open Banking acts as a catalyst for innovation, prompting financial institutions to explore new business models and develop innovative products. The ability to tap into a broader ecosystem of services stimulates creativity and accelerates product development cycles.

Financial Inclusion: Open Banking has the potential to enhance financial inclusion by making financial services more accessible. By allowing third-party providers to leverage banking infrastructure, Open Banking can reach underserved segments and address gaps in traditional banking services.

Market Restraints:

Data Security Concerns: The sharing of sensitive financial data raises concerns about data security and privacy. Addressing these concerns is crucial to building trust among consumers and ensuring the widespread adoption of Open Banking.

Regulatory Compliance: Compliance with evolving regulatory frameworks poses challenges for financial institutions. Adhering to stringent data protection and security standards requires significant investments in technology and infrastructure.

Legacy System Integration: Many traditional banks operate on legacy systems that may not be inherently compatible with Open Banking APIs. The integration of modern Open Banking infrastructure with legacy systems presents technical challenges that require careful planning.

Change Management: Embracing Open Banking necessitates a cultural shift within financial institutions. Adapting to new business models, collaboration paradigms, and a more open approach to data sharing requires effective change management strategies.

Market Opportunities:

API Monetization: Banks can explore revenue opportunities through API monetization. By offering APIs to third-party developers and charging for their usage, financial institutions can create new revenue streams and drive ecosystem growth.

Wealth Management Solutions: Open Banking opens up possibilities for innovative wealth management solutions. Banks can collaborate with FinTechs to offer advanced wealth management tools that leverage comprehensive financial data to provide personalized advice.

Cross-Border Financial Services: The adoption of Open Banking facilitates cross-border financial services. Banks can explore partnerships with international counterparts to offer seamless financial experiences for customers with global financial footprints.

Digital Identity Services: Open Banking can serve as a foundation for the development of secure and interoperable digital identity solutions. Banks can play a central role in offering identity services that enhance security and streamline customer onboarding processes.

Market Dynamics: The Asia-Pacific Open Banking market operates within a dynamic environment shaped by technological evolution, regulatory changes, and evolving consumer expectations. Understanding these dynamics is crucial for financial institutions seeking to harness the full potential of Open Banking and stay competitive in the evolving financial landscape.

Regional Analysis:

China: China has emerged as a leader in Open Banking adoption, driven by a vibrant FinTech ecosystem and supportive regulatory initiatives. The integration of Open Banking principles aligns with China’s broader goals of digital transformation in the financial sector.

India: India is witnessing a gradual shift toward Open Banking, with regulatory bodies encouraging banks to adopt API-driven models. The push for financial inclusion and the rise of digital payment platforms contribute to the growth of Open Banking in India.

Australia: Australia has embraced Open Banking through the Consumer Data Right (CDR) framework. The phased implementation of CDR is opening up opportunities for financial institutions to enhance competition and offer innovative services.

Southeast Asia: Countries in Southeast Asia are exploring Open Banking as a means to drive financial inclusion and innovation. Regulatory frameworks are evolving to accommodate the changing dynamics of the financial services sector.

Japan: Japan, with its highly developed banking sector, is gradually exploring Open Banking to stimulate innovation and competition. The integration of Open Banking principles aligns with Japan’s efforts to modernize its financial infrastructure.

Competitive Landscape:

Leading Companies in the Asia-Pacific Open Banking Market:

Plaid Inc.

Yodlee, Inc. (Envestnet, Inc.)

Tink AB

Salt Edge Inc.

BBVA Open Platform, Inc.

Figo GmbH

Token, Inc.

Axway Software

MuleSoft, LLC (Salesforce)

Fiserv, Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

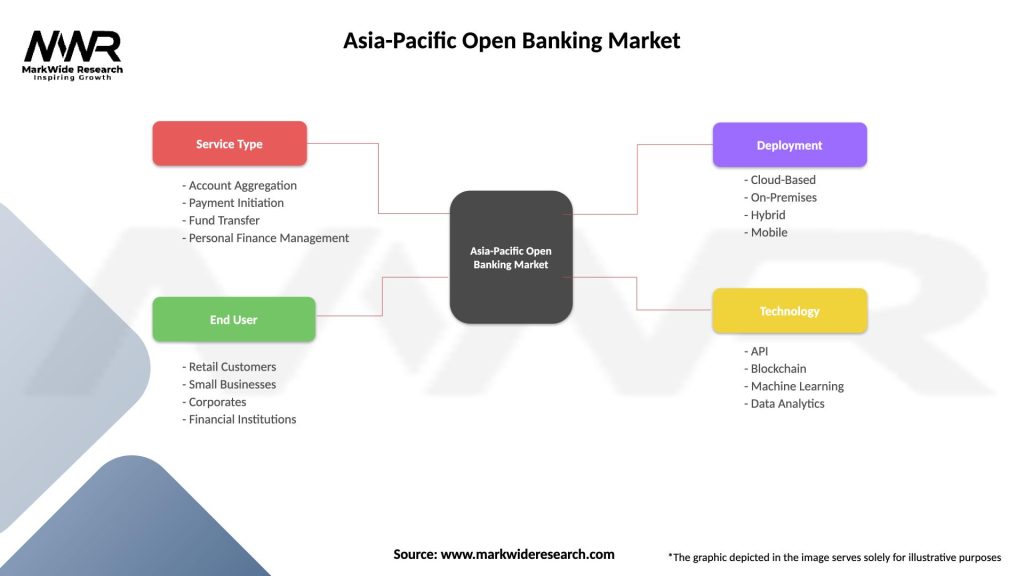

Segmentation: The Asia-Pacific Open Banking market can be segmented based on various factors, including:

Segmentation allows for a more nuanced understanding of the diverse market dynamics across different service types, end-users, and countries.

Category-wise Insights:

API-Based Services: The adoption of API-based services is a cornerstone of Open Banking. Banks and FinTechs are developing and offering a range of API-based services, including payment initiation, account information, and fund confirmation.

Digital Payments: Open Banking is driving innovation in the digital payments space. Collaborations between banks and FinTechs are resulting in seamless and secure digital payment solutions that leverage Open Banking infrastructure.

Data Analytics Solutions: The wealth of data available through Open Banking is fueling the development of advanced data analytics solutions. Banks are leveraging analytics to gain insights into customer behavior, enhance risk management, and personalize services.

Regulatory Technology (RegTech): The regulatory landscape surrounding Open Banking requires robust compliance solutions. The emergence of RegTech solutions tailored for Open Banking is helping financial institutions navigate complex regulatory requirements.

Key Benefits for Industry Participants and Stakeholders:

Enhanced Customer Engagement: Open Banking enables financial institutions to engage customers more effectively by offering personalized and relevant financial products and services.

Innovation and Agility: Banks and FinTechs can achieve greater innovation and agility by leveraging Open Banking APIs. The ability to collaborate and build on existing infrastructure accelerates the development and deployment of new solutions.

Competitive Differentiation: Open Banking allows financial institutions to differentiate themselves by offering unique and innovative services. This differentiation is crucial in a market where customer expectations are evolving rapidly.

Ecosystem Growth: The Open Banking ecosystem thrives on collaboration. Financial institutions that actively participate in the ecosystem contribute to its growth while benefiting from the diverse range of services and solutions offered by partners.

SWOT Analysis: A SWOT analysis provides a comprehensive overview of the Asia-Pacific Open Banking market’s strengths, weaknesses, opportunities, and threats:

Strengths:

Growing FinTech Ecosystem

Supportive Regulatory Environment

Increasing Digital Adoption

Weaknesses:

Data Security Concerns

Legacy System Integration Challenges

Compliance Complexity

Opportunities:

Cross-Border Financial Services

API Monetization

Enhanced Financial Inclusion

Threats:

Cybersecurity Risks

Intense Competition

Regulatory Uncertainty

Understanding these factors through a SWOT analysis empowers industry participants to capitalize on strengths, address weaknesses, seize opportunities, and mitigate potential threats.

Market Key Trends:

Open Banking Platforms: The emergence of Open Banking platforms that facilitate seamless collaboration between banks, FinTechs, and other service providers is a notable trend. These platforms act as hubs for innovation, enabling participants to leverage shared infrastructure.

Blockchain Integration: Some players in the Open Banking space are exploring the integration of blockchain technology to enhance security, transparency, and efficiency in financial transactions. Blockchain has the potential to address data security concerns and build trust in Open Banking.

API Security Solutions: With the critical role that APIs play in Open Banking, there is a growing focus on API security solutions. Financial institutions are investing in robust security measures to safeguard API endpoints and protect sensitive customer data.

Regulatory Sandbox Participation: Financial institutions and FinTechs are increasingly participating in regulatory sandboxes to test and refine Open Banking solutions in a controlled environment. Regulatory sandboxes provide a platform for experimentation while ensuring compliance with regulatory requirements.

Covid-19 Impact: The Covid-19 pandemic has accelerated the digital transformation of the financial services sector, including the adoption of Open Banking. Some key impacts of Covid-19 on the Asia-Pacific Open Banking market include:

Contactless Payments Surge: The fear of physical contact has led to a surge in contactless payments, driving the adoption of digital payment solutions facilitated by Open Banking infrastructure.

Remote Financial Services: With lockdowns and social distancing measures in place, there is an increased demand for remote financial services. Open Banking enables the delivery of a wide range of financial services through digital channels.

Focus on Digital Identity: The need for secure and seamless digital interactions has heightened the focus on digital identity solutions. Open Banking can play a role in developing interoperable and secure digital identity frameworks.

Acceleration of Open Banking Initiatives: The pandemic has underscored the importance of digital financial services, prompting governments and regulatory bodies to accelerate Open Banking initiatives to foster innovation and resilience.

Key Industry Developments:

Expansion of Open Banking Ecosystems: The Open Banking ecosystem in Asia-Pacific is expanding, with more banks, FinTechs, and technology firms joining the fray. The collaborative nature of Open Banking is driving the creation of a vibrant and interconnected ecosystem.

Regulatory Evolution: Regulatory frameworks governing Open Banking are evolving to keep pace with technological advancements. Regulators are actively engaging with industry stakeholders to create a conducive environment for innovation while ensuring consumer protection.

Global Alliances: Financial institutions in the region are forming global alliances to extend the reach of Open Banking services. Collaborations between Asian and non-Asian banks aim to create a global Open Banking network.

Focus on API Standardization: The adoption of standardized APIs is gaining momentum to enhance interoperability and simplify the integration of Open Banking solutions. Standardization efforts contribute to a more seamless and efficient ecosystem.

Analyst Suggestions:

Invest in Cybersecurity: Given the data-centric nature of Open Banking, investing in robust cybersecurity measures is paramount. Financial institutions should prioritize the implementation of advanced security solutions to protect customer data and maintain trust.

Collaborate Strategically: Strategic collaborations between banks, FinTechs, and technology firms can unlock new opportunities and drive innovation. Financial institutions should actively seek partnerships that complement their strengths and contribute to the growth of the Open Banking ecosystem.

Embrace Agile Technologies: The adoption of agile and scalable technologies, such as cloud computing and microservices architecture, is essential for navigating the rapidly evolving Open Banking landscape. These technologies enable flexibility and rapid adaptation to changing market dynamics.

Customer Education and Communication: As Open Banking introduces new concepts and services, effective customer education and communication are crucial. Financial institutions should proactively communicate the benefits, risks, and safeguards associated with Open Banking to build customer trust.

Future Outlook: The future outlook for the Asia-Pacific Open Banking market is poised for significant growth and transformation, driven by a convergence of factors including regulatory reforms, technological advancements, and shifting consumer expectations. As governments in the region increasingly embrace open banking frameworks and digitalization initiatives, the market presents vast opportunities for financial institutions, fintech startups, and technology providers. Key trends such as the proliferation of APIs (Application Programming Interfaces), the rise of digital payment solutions, and the emergence of collaborative ecosystems will shape the trajectory of the market. Additionally, the integration of artificial intelligence, blockchain, and machine learning technologies will drive innovation in product offerings and customer experiences. By leveraging these trends and fostering strategic partnerships, stakeholders in the Asia-Pacific Open Banking market can unlock new revenue streams, improve operational efficiency, and enhance financial inclusion across the region.

Conclusion: The Asia-Pacific Open Banking market represents a transformative force reshaping the financial services landscape. Regulatory support, technological advancements, and a growing appetite for innovation are propelling the adoption of Open Banking across the region. As financial institutions, FinTechs, and technology players collaborate to unlock the full potential of Open Banking, the market is poised for continued growth and evolution.

What is Open Banking?

Open Banking refers to a financial services model that allows third-party developers to build applications and services around financial institutions. It enables secure access to consumer banking data, fostering innovation and competition in the financial sector.

What are the key players in the Asia-Pacific Open Banking Market?

Key players in the Asia-Pacific Open Banking Market include companies like Ant Financial, DBS Bank, and Commonwealth Bank of Australia, which are actively developing open banking solutions and partnerships to enhance customer experiences, among others.

What are the main drivers of the Asia-Pacific Open Banking Market?

The main drivers of the Asia-Pacific Open Banking Market include the increasing demand for personalized financial services, advancements in technology such as APIs, and regulatory support promoting transparency and competition in the banking sector.

What challenges does the Asia-Pacific Open Banking Market face?

Challenges in the Asia-Pacific Open Banking Market include concerns over data security and privacy, the need for standardization across different jurisdictions, and resistance from traditional banks wary of sharing customer data.

What opportunities exist in the Asia-Pacific Open Banking Market?

Opportunities in the Asia-Pacific Open Banking Market include the potential for fintech startups to innovate new financial products, the ability for banks to enhance customer engagement through personalized services, and the expansion of cross-border banking solutions.

What trends are shaping the Asia-Pacific Open Banking Market?

Trends shaping the Asia-Pacific Open Banking Market include the rise of digital wallets, increased collaboration between banks and fintechs, and the growing emphasis on customer-centric services that leverage data analytics for better decision-making.

Leading Companies in the Asia-Pacific Open Banking Market:

Plaid Inc.

Yodlee, Inc. (Envestnet, Inc.)

Tink AB

Salt Edge Inc.

BBVA Open Platform, Inc.

Figo GmbH

Token, Inc.

Axway Software

MuleSoft, LLC (Salesforce)

Fiserv, Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.