The Asia-Pacific region has witnessed significant growth in the Neo banking sector in recent years. Neo banking, also known as digital or online banking, refers to financial services provided by digital platforms without the need for physical branches. These platforms leverage technology and innovation to offer a wide range of banking services, including payments, transfers, savings, and loans, among others. The Asia-Pacific Neo banking market has emerged as a disruptive force in the traditional banking landscape, attracting a large number of customers seeking convenient and user-friendly financial solutions.

Meaning

Neo banking is a modern banking concept that combines technology and finance to provide customers with innovative and digital banking services. It aims to redefine traditional banking by offering streamlined and efficient financial solutions through digital platforms. Neo banks typically operate entirely online, allowing customers to access their accounts and perform various banking activities through mobile applications or web portals. These digital banks often focus on user experience, personalization, and advanced technologies to deliver enhanced financial services.

Executive Summary

The Asia-Pacific Neo banking market has experienced rapid growth in recent years, driven by the increasing adoption of smartphones, internet penetration, and changing customer preferences. The region’s large population, particularly in countries such as China and India, presents immense market potential for Neo banking providers. These digital banks have successfully tapped into the growing demand for convenient and accessible financial services, attracting tech-savvy customers who prefer digital interactions over traditional banking methods.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Rising Adoption of Mobile Banking: The proliferation of smartphones and the availability of affordable internet connectivity have led to a surge in mobile banking adoption. Customers find it more convenient to access banking services through mobile applications, contributing to the growth of Neo banking in the Asia-Pacific region.

Changing Customer Expectations: Customers now demand faster, more personalized, and hassle-free banking experiences. Neo banks, with their user-friendly interfaces, advanced features, and personalized offerings, have gained popularity among digitally-driven customers who seek seamless financial solutions.

Competitive Landscape: The Asia-Pacific Neo banking market is highly competitive, with both established financial institutions and emerging fintech startups vying for market share. Incumbent banks are also exploring partnerships and collaborations with Neo banks to stay relevant and tap into the growing digital banking trend.

Regulatory Challenges: Neo banks face regulatory challenges in some countries, as regulators strive to strike a balance between promoting innovation and ensuring customer protection. Compliance with regulatory requirements and building trust among customers are crucial for the sustained growth of Neo banking in the Asia-Pacific region.

Expansion into Adjacent Services: To differentiate themselves and expand their customer base, Neo banks are diversifying into adjacent financial services such as insurance, wealth management, and investment products. This strategy allows them to offer a comprehensive suite of financial solutions and increase customer engagement.

Market Drivers

Increasing Smartphone Penetration: The Asia-Pacific region has witnessed a surge in smartphone adoption, providing a favorable environment for Neo banking growth. With smartphones becoming ubiquitous, more people have access to digital banking services, enabling Neo banks to reach a wider customer base.

Rising Internet Penetration: The availability of affordable internet connectivity and the expansion of 4G and 5G networks have boosted internet penetration in the region. This has facilitated the adoption of online banking services, as customers can conveniently access financial products and services from their devices.

Convenience and Accessibility: Neo banks offer convenient and accessible banking services, eliminating the need for physical branches. Customers can perform transactions, manage accounts, and access financial services anytime, anywhere, using their smartphones or computers.

Technological Advancements: Advancements in technology, such as artificial intelligence, machine learning, and blockchain, have enabled Neo banks to enhance their offerings and provide personalized financial solutions. These technologies improve customer experience, security, and operational efficiency.

Changing Demographics and Consumer Behavior: The rise of digital-native generations, such as millennials and Gen Z, who are more inclined towards digital channels, has fueled the demand for Neo banking services. These tech-savvy customers prefer seamless digital experiences and are open to adopting innovative financial solutions.

Market Restraints

Regulatory and Compliance Challenges: Neo banks face regulatory challenges in navigating complex regulatory frameworks in different countries. Compliance with financial regulations, data privacy laws, and anti-money laundering measures can pose hurdles for Neo banking providers, requiring them to invest in robust compliance systems.

Trust and Security Concerns: While Neo banks prioritize security, customers may still have concerns about the safety of their financial information and transactions. Building trust among customers is crucial for Neo banks to gain wider acceptance and retain customers.

Limited Awareness and Adoption in Rural Areas: Despite the growth of Neo banking in urban areas, there is limited awareness and adoption in rural and remote areas of the Asia-Pacific region. Lack of internet connectivity, digital literacy, and trust in online platforms are some of the factors hindering the expansion of Neo banking services in these areas.

Fragmented Market Landscape: The Asia-Pacific region is diverse, comprising multiple countries with varying levels of economic development, regulatory environments, and customer preferences. Neo banks face the challenge of adapting their offerings and strategies to suit the unique characteristics of each market.

Competitive Pressure from Incumbent Banks: Traditional banks have started to recognize the potential of Neo banking and are launching their own digital banking services. This increased competition from established financial institutions poses a challenge for Neo banks in terms of differentiation and customer acquisition.

Market Opportunities

Untapped Market Potential: Despite the rapid growth of Neo banking in the Asia-Pacific region, there is still significant untapped market potential. As more people gain access to smartphones and the internet, the addressable market for Neo banks continues to expand, especially in emerging economies.

Partnerships and Collaborations: Neo banks can explore partnerships and collaborations with established financial institutions, fintech startups, and technology companies to leverage their expertise, customer base, and distribution networks. Collaborative efforts can help Neo banks accelerate their growth and offer a broader range of financial services.

Financial Inclusion: Neo banks have the opportunity to contribute to financial inclusion by providing banking services to the unbanked and underbanked populations in the Asia-Pacific region. Through their digital platforms, Neo banks can offer basic banking services, savings accounts, and microloans to individuals who previously had limited access to formal financial services.

Cross-Border Expansion: As the Neo banking market matures in certain countries, Neo banks can explore expansion opportunities across borders. The Asia-Pacific region offers diverse markets with varying levels of digital banking penetration, presenting opportunities for Neo banks to replicate their success in new geographies.

Focus on Niche Segments: Neo banks can differentiate themselves by targeting specific niche segments, such as freelancers, small businesses, or the gig economy. By understanding the unique financial needs of these segments and tailoring their offerings accordingly, Neo banks can attract and retain a loyal customer base.

Market Dynamics

The Asia-Pacific Neo banking market is characterized by intense competition, evolving customer expectations, regulatory developments, and technological advancements. These dynamics shape the strategies and operations of Neo banking providers, driving innovation and market growth.

Customers’ preference for convenience, personalized experiences, and seamless digital interactions is one of the key drivers of the Neo banking market. Neo banks leverage technology to offer user-friendly interfaces, real-time access to financial information, and personalized recommendations. This customer-centric approach enables them to attract and retain customers in an increasingly competitive landscape.

Furthermore, regulatory developments play a significant role in shaping the Neo banking market in the Asia-Pacific region. Regulatory bodies are adapting their frameworks to accommodate the rise ofdigital banking and fintech, aiming to strike a balance between promoting innovation and ensuring consumer protection. Neo banks need to navigate these evolving regulations to remain compliant and build trust among customers.

Technological advancements continue to drive the growth of the Neo banking market. Artificial intelligence and machine learning enable Neo banks to analyze customer data, personalize offerings, and automate processes, enhancing the overall customer experience. Blockchain technology also holds promise for Neo banks, offering secure and transparent transactions.

The competitive landscape of the Asia-Pacific Neo banking market is evolving rapidly. Traditional banks are launching their own digital banking platforms to stay relevant and cater to the changing preferences of customers. Fintech startups, with their agility and focus on innovation, are also entering the market, intensifying the competition. Established players and emerging Neo banks need to differentiate themselves through unique value propositions, partnerships, and continuous innovation to gain a competitive edge.

Customer education and awareness play a crucial role in driving the adoption of Neo banking services. Neo banks need to invest in marketing campaigns, customer education programs, and partnerships with local communities to raise awareness and build trust among potential customers. Addressing security concerns and showcasing the benefits of digital banking can help accelerate the adoption of Neo banking services in the region.

As the Neo banking market in the Asia-Pacific region continues to evolve, partnerships and collaborations between Neo banks, fintech startups, and traditional banks are likely to increase. Such collaborations can leverage the strengths of each player, allowing for the development of innovative products and services, expansion into new markets, and enhanced customer experiences.

Regulatory developments will remain a key factor shaping the market dynamics. Neo banks need to closely monitor regulatory changes, adapt their processes and systems accordingly, and engage with regulators to contribute to the development of a conducive regulatory environment for digital banking.

Regional Analysis

The Asia-Pacific Neo banking market is geographically diverse, encompassing countries with varying levels of economic development, regulatory frameworks, and customer preferences. Each country presents unique opportunities and challenges for Neo banking providers.

China, with its large population and rapidly growing middle class, has witnessed significant growth in the Neo banking sector. Digital payment platforms such as Alipay and WeChat Pay have gained widespread adoption, laying the foundation for Neo banks to offer additional financial services. The Chinese government’s push for financial inclusion and regulatory reforms has further facilitated the growth of Neo banking in the country.

India, another populous country in the region, has a rapidly expanding digital ecosystem. The government’s initiatives, such as the Digital India campaign and the Unified Payments Interface (UPI), have contributed to the growth of digital payments and provided a favorable environment for Neo banks. The Indian Neo banking market is highly competitive, with both homegrown players and international Neo banks vying for market share.

Southeast Asian countries, including Indonesia, Thailand, and Vietnam, present immense market potential for Neo banking providers. These countries have experienced significant growth in internet and smartphone penetration, driving the demand for digital banking services. Regulatory frameworks are evolving in these markets, providing opportunities for Neo banks to enter and expand their presence.

Australia, Japan, and South Korea have relatively mature digital banking ecosystems. Established financial institutions and fintech startups are actively competing in these markets. Neo banks in these countries focus on offering differentiated services, personalized experiences, and innovative products to attract customers.

It is important for Neo banking providers to tailor their strategies and offerings to the unique characteristics of each market. This includes understanding local regulatory requirements, customer preferences, and cultural factors to effectively penetrate and succeed in specific regions.

Competitive Landscape

Leading Companies in the Asia-Pacific Neo Banking Market:

WeBank (Tencent Holdings Limited)

MYbank (Alibaba Group Holding Limited)

Kakaobank Corporation

Atom Bank plc

Chime Financial, Inc.

N26 GmbH

Monzo Bank Limited

Revolut Ltd.

Starling Bank Limited

Varo Money, Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

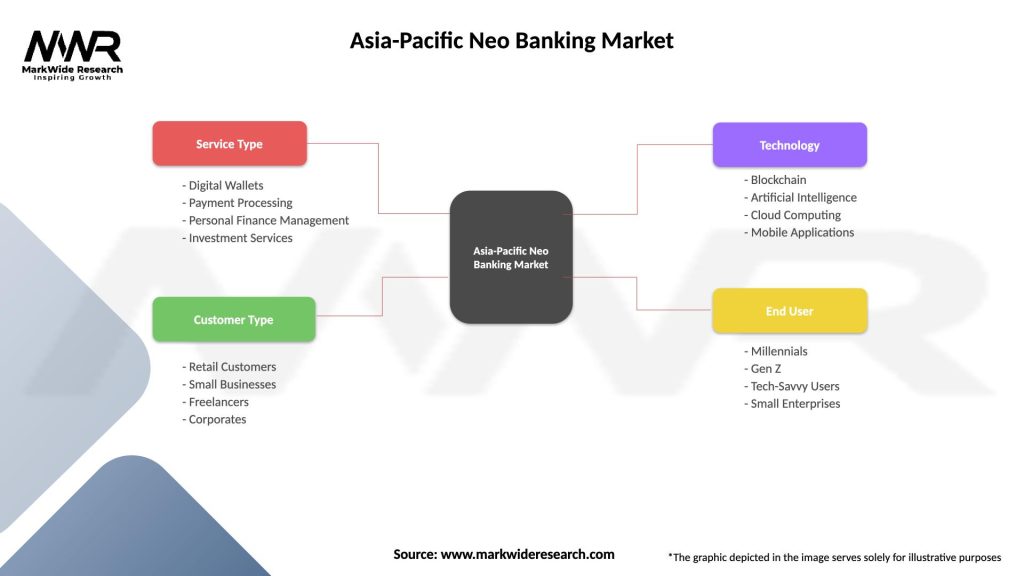

Segmentation

The Asia-Pacific Neo banking market can be segmented based on various factors, including customer segments, services offered, and business models. The segmentation helps Neo banks identify target customers, tailor their offerings, and address specific market needs.

Customer Segments:

Retail Customers: Neo banks cater to individual retail customers, offering them a range of digital banking services, including payments, transfers, savings accounts, loans, and investment products. These services are typically accessible through mobile applications or web portals, providing customers with convenient and user-friendly banking experiences.

Small and Medium Enterprises (SMEs): Neo banks also target small and medium-sized enterprises, providing them with digital banking solutions tailored to their specific needs. These solutions may include business accounts, invoicing and payment services, lending options, and financial management tools to support the growth and operations of SMEs.

Freelancers and Gig Economy Workers: Neo banks recognize the unique financial needs of freelancers and gig economy workers who may have irregular income streams and require flexible banking solutions. These customers benefit from Neo banks’ simplified account opening processes, quick payment settlements, and value-added services that help them manage their finances efficiently.

Services Offered:

Payments and Transfers: Neo banks focus on providing seamless and convenient payment and transfer services to their customers. This includes peer-to-peer (P2P) transfers, domestic and international remittances, bill payments, and mobile wallet integration.

Savings and Investments: Neo banks offer savings accounts with competitive interest rates and investment options tailored to customers’ risk profiles. They leverage technology to provide personalized investment recommendations, automated portfolio management, and access to a wide range of investment products.

Loans and Credit Facilities: Neo banks provide digital lending solutions, including personal loans, credit cards, and business loans. They leverage customer data and advanced algorithms to offer quick loan approvals, competitive interest rates, and flexible repayment options.

Financial Management Tools: Neo banks offer financial management tools and features that help customers track and analyze their spending, set budgets, and achieve their financial goals. These tools provide insights into spending patterns, offer personalized recommendations, and promote financial literacy.

Business Models:

Neo banks with Banking Licenses: Some Neo banks obtain banking licenses, allowing them to offer a full suite of banking services, including deposits, lending, and other regulated activities. These Neo banks operate as licensed financial institutions and are subject to banking regulations and oversight.

Neo banks as Technology Providers: Some Neo banks operate as technology providers, partnering with traditional banks or financial institutions to offer digital banking solutions. These Neo banks provide the technology infrastructure, mobile applications, and user interfaces, while the partnering institution handles the regulatory compliance and banking operations.

Neo banks as Collaborative Platforms: Certain Neo banks act as collaborative platforms, integrating various financial products and services from multiple providers into a single digital platform. These platforms offer customers a consolidated view of their finances and allow them to access multiple financial services through a single application.

The segmentation of the Asia-Pacific Neo banking market helps Neo banks identify specific customer needs, tailor their offerings, and position themselves effectively in the competitive landscape. By understanding the unique requirements of different customer segments and offering specialized services, Neo banks can attract and retain a loyal customer base.

Category-wise Insights

Payments and Transfers: Neo banks have transformed the payments and transfers landscape in the Asia-Pacific region. They provide customers with convenient, secure, and real-time payment options, including peer-to-peer transfers, QR code payments, and mobile wallet integration. Neo banks leverage advanced technologies such as blockchain and digital wallets to offer seamless payment experiences and eliminate the need for traditional cash-based transactions.

Savings and Investments: Neo banks have disrupted the traditional savings and investment landscape by offering innovative and user-friendly solutions. They provide customers with digital savings accounts that offer competitive interest rates, flexible withdrawal options, and automated savings features. Neo banks also offer investment products such as mutual funds, stocks, and exchange-traded funds (ETFs), allowing customers to access diversified investment options and personalized recommendations through their digital platforms.

Loans and Credit Facilities: Neo banks have streamlined the loan application and approval process, making it quicker and more accessible for customers. They leverage technology to analyze customer data and provide instant loan approvals, competitive interest rates, and flexible repayment options. Neo banks also cater to underserved segments such as freelancers and gig economy workers, offering them specialized loan products that meet their unique financial needs.

Financial Management Tools: Neo banks provide customers with advanced financial management tools that help them track their expenses, set budgets, and achieve their financial goals. These tools offer personalized insights into spending patterns, categorize expenses, and provide recommendations for optimizing financial health. Neo banks empower customers with greater control and transparency over their finances through easy-to-use interfaces and real-time updates.

Business Banking Solutions: Neo banks are increasingly targeting small and medium-sized enterprises (SMEs) with digital banking solutions tailored to their specific needs. They offer business accounts, invoicing and payment services, working capital financing, and cash flow management tools. Neo banks simplify and automate financial processes for SMEs, allowing them to focus on business growth and operations.

Category-wise insights highlight the impact of Neo banks in transforming specific areas of banking services. By leveraging technology, customer-centric approaches, and innovative products, Neo banks have revolutionized payments, savings, investments, lending, and financial management experiences for customers in the Asia-Pacific region.

Key Benefits for Industry Participants and Stakeholders

The Asia-Pacific Neo banking market offers several key benefits for industry participants and stakeholders, including:

Enhanced Customer Experience: Neo banks prioritize customer experience by offering intuitive user interfaces, personalized services, and real-time access to financial information. Customers can conveniently perform banking transactions, manage their accounts, and access a wide range of financial products and services through user-friendly mobile applications or web portals.

Convenience and Accessibility: Neo banks provide customers with anytime, anywhere access to financial services, eliminating the need for physical branch visits. Customers can perform transactions, make payments, and access their accounts through their smartphones or computers. This convenience and accessibility appeal to digitally-driven customers who seek seamless and efficient banking experiences.

Innovation and Technological Advancements: Neo banks leverage technology and innovation to provide advanced financial solutions. They incorporate artificial intelligence, machine learning, and data analytics to offer personalized recommendations, automated processes, and enhanced security measures. Neo banks drive technological advancements in the banking industry and set new standards for digital banking experiences.

Financial Inclusion: Neo banks contribute to financial inclusion by reaching unbanked and underbanked populations in the Asia-Pacific region. Through their digital platforms, Neo banks provide basic banking services, savings accounts, and microloans to individuals who previously had limited access to formal financial services. This inclusion helps drive economic growth and empowerment for underserved communities.

Collaboration and Partnerships: The Neo banking ecosystem encourages collaboration and partnerships between traditional banks, fintech startups, technology companies, and regulators. This collaboration fosters knowledge sharing, innovation, and the development of new products and services. Traditional banks can leverage the agility and technology expertise of Neo banks, while Neo banks can benefit from the established customer base and regulatory compliance of traditional banks.

Market Growth and Expansion Opportunities: The Asia-Pacific Neo banking market presents significant growth opportunities for industry participants. With the increasing adoption of smartphones, internet penetration, and changing customer preferences, Neo banks have the potential to expand their customer base and market share. Untapped markets, such as rural areas and emerging economies, offer further expansion opportunities for Neo banks in the region.

The key benefits offered by the Asia-Pacific Neo banking market demonstrate its potential to transform the banking industry, improve customer experiences, promote financial inclusion, and drive innovation and collaboration among industry participants and stakeholders.

SWOT Analysis

A SWOT (Strengths, Weaknesses, Opportunities, and Threats) analysis provides an overview of the internal and external factors that can impact the success of the Asia-Pacific Neo banking market.

Strengths:

Technological Innovation: Neo banks leverage advanced technologies to deliver seamless and user-friendly banking experiences. They harness the power of artificial intelligence, machine learning, and blockchain to provide personalized services, automate processes, and enhance security measures.

Customer-Centric Approach: Neo banks prioritize customer experience by offering convenient, accessible, and personalized financial services. They focus on user-friendly interfaces, real-time access to information, and personalized recommendations, attracting digitally-driven customers who value convenience and efficiency.

Agility and Speed: Neo banks, compared to traditional banks, are more agile and able to quickly adapt to changing customer needs and market trends. Their digital-first approach allows them to launch innovative products and services, respond to market demands, and stay ahead of competitors.

Cost Efficiency: Neo banks operate without physical branches, allowing them to save on operational costs associated with maintaining a branch network. This cost efficiency enables them to offer competitive interest rates, lower fees, and attractive rewards programs to customers.

Weaknesses:

Regulatory Challenges: Neo banks face regulatory challenges in navigating complex regulatory frameworks across different countries. Compliance with financial regulations, data privacy laws, and anti-money laundering measures can pose hurdles and require significant investments in compliance systems.

Limited Brand Recognition: Compared to traditional banks, Neo banks may have limited brand recognition, especially among older and more conservative customers. Building trust and establishing a strong brand presence are crucial for Neo banks to attract and retain customers in a competitive market.

Reliance on Technology: Neo banks heavily rely on technology for their operations. Any disruption in technology infrastructure, cybersecurity breaches, or system failures can impact the delivery of services and erode customer trust. Neo banks must invest in robust technology infrastructure and cybersecurity measures toensure uninterrupted service and maintain data security.

Customer Acquisition: The Asia-Pacific Neo banking market is highly competitive, with both established financial institutions and emerging fintech startups vying for market share. Neo banks need to invest in marketing and customer acquisition strategies to stand out in the crowded market and attract a significant customer base.

Opportunities:

Growing Smartphone Penetration: The Asia-Pacific region has witnessed a rapid increase in smartphone penetration, providing a favorable environment for Neo banking growth. As more people gain access to smartphones, the addressable market for Neo banks expands, presenting significant growth opportunities.

Financial Inclusion: Neo banks have the opportunity to promote financial inclusion by reaching unbanked and underbanked populations. By offering basic banking services, savings accounts, and microloans through their digital platforms, Neo banks can empower individuals who previously had limited access to formal financial services.

Partnerships and Collaborations: Neo banks can explore partnerships and collaborations with traditional banks, fintech startups, and technology companies. Collaborative efforts can help Neo banks leverage existing customer bases, distribution networks, and expertise, enabling faster market penetration and expansion into new geographies.

Cross-Border Expansion: As the Neo banking market matures in certain countries, Neo banks can explore expansion opportunities across borders. The Asia-Pacific region offers diverse markets with varying levels of digital banking penetration, providing opportunities for Neo banks to replicate their success in new geographies.

Threats:

Regulatory Environment: Neo banks operate in a highly regulated environment, with regulatory frameworks evolving to address the challenges and risks associated with digital banking. Regulatory changes can impose compliance costs, limit certain activities, or introduce new market entry requirements, posing challenges for Neo banks to adapt and comply with regulatory requirements.

Security and Privacy Concerns: Security breaches and data privacy issues are significant threats to Neo banks. Any cybersecurity breach can undermine customer trust and lead to financial and reputational damage. Neo banks must continuously invest in robust security measures and educate customers about the security features and protocols in place.

Competitive Pressure: Traditional banks are recognizing the potential of Neo banking and launching their own digital banking platforms. This increased competition from established financial institutions can pose challenges for Neo banks in terms of differentiation, customer acquisition, and market share.

Economic and Geopolitical Factors: Economic downturns, political instability, and geopolitical tensions can impact the overall business environment and consumer sentiment. Neo banks must be prepared to navigate through challenging economic conditions and adapt their strategies accordingly.

The SWOT analysis highlights the internal strengths and weaknesses of Neo banks, as well as the external opportunities and threats they face in the Asia-Pacific Neo banking market. Understanding these factors is crucial for Neo banks to formulate effective strategies, mitigate risks, and capitalize on growth opportunities.

Market Key Trends

Open Banking: Open banking initiatives are gaining traction in the Asia-Pacific region. Open banking promotes collaboration and data sharing between financial institutions and third-party providers, allowing customers to access a broader range of financial services through a single platform. Neo banks can leverage open banking frameworks to offer customers a consolidated view of their finances and access to specialized products and services.

Personalization and Customization: Customers expect personalized and customized financial solutions that cater to their specific needs. Neo banks are leveraging customer data, advanced analytics, and artificial intelligence to offer personalized recommendations, targeted offers, and tailored financial products. By delivering personalized experiences, Neo banks can enhance customer engagement and loyalty.

Expansion into Adjacent Services: Neo banks are expanding their offerings beyond core banking services. They are diversifying into adjacent financial services such as insurance, wealth management, and investment products. By providing a comprehensive suite of financial solutions, Neo banks can deepen customer relationships and increase customer lifetime value.

Sustainability and ESG Investing: Environmental, Social, and Governance (ESG) investing is gaining prominence in the Asia-Pacific region. Neo banks are incorporating ESG principles into their investment offerings, providing customers with options to invest in sustainable and socially responsible assets. This trend aligns with the increasing demand for responsible investing and reflects customers’ values and preferences.

Embedded Finance: Neo banks are exploring opportunities for embedded finance, where financial services are seamlessly integrated into non-financial platforms. For example, Neo banks can offer banking services within e-commerce platforms, ride-hailing apps, or social media platforms. Embedded finance allows Neo banks to expand their customer reach and provide convenient financial services in the context of customers’ everyday activities.

These key trends shape the evolution of the Asia-Pacific Neo banking market. Neo banks that embrace these trends and adapt their strategies accordingly can gain a competitive edge, attract customers, and drive market growth.

Covid-19 Impact

The Covid-19 pandemic has had a profound impact on the Asia-Pacific Neo banking market, accelerating the adoption of digital banking services and shaping customer preferences.

Accelerated Digital Transformation: The pandemic-induced lockdowns and social distancing measures compelled customers to shift to digital channels for their banking needs. Neo banks, with their digital-first approach and user-friendly interfaces, were well-positioned to cater to the increased demand for remote banking services. The pandemic served as a catalyst for digital transformation in the banking industry.

Contactless Payments and Transactions: The fear of virus transmission through physical cash led to a surge in contactless payments and digital transactions. Neo banks, with their emphasis on digital payments and mobile wallets, witnessed increased adoption and transaction volumes. Customers embraced the convenience and safety of contactless transactions offered by Neo banks.

Remote Account Opening and Onboarding: The closure of physical branches during the pandemic highlighted the importance of remote account opening and onboarding processes. Neo banks, with their streamlined digital onboarding procedures, enabled customers to open accounts and access banking services from the safety of their homes. This remote account opening capability became a key advantage for Neo banks during the pandemic.

Increased Demand for Financial Management Tools: The economic uncertainty caused by the pandemic heightened the need for financial management tools and budgeting capabilities. Neo banks, with their advanced financial management features, helped customers track expenses, set savings goals, and manage their finances during challenging times. The pandemic highlighted the value of such tools and positioned Neo banks as providers of holistic financial solutions.

Customer Support and Assistance: Neo banks quickly adapted their customer support channels to provide assistance and guidance to customers facing financial difficulties due to the pandemic. They offered flexible repayment options, extended loan moratoriums, and introduced relief programs to support customers during the crisis. Neo banks’ responsiveness and customer-centric approach strengthened customer trust and loyalty.

The Covid-19 pandemic accelerated the shift towards digital banking and underscored the importance of digital channels and remote banking capabilities. Neo banks, with their technology-driven offerings and focus on customer experience, emerged as resilient and innovative players during the crisis.

Key Industry Developments

The Asia-Pacific Neo banking market has witnessed several key industry developments that have shaped its landscape and dynamics. These developments include:

Regulatory Reforms: Governments and regulatory bodies across the Asia-Pacific region have introduced reforms to accommodate the growth of Neo banking and fintech. They have revised regulations, issued new licenses, and created sandboxes to foster innovation while ensuring consumer protection and financial stability. These regulatory reforms have provided a conducive environment for Neo banks to operate and expand their services.

Partnerships between Neo Banks and Traditional Banks: Traditional banks have recognized the potential of Neo banking and have formed partnerships and collaborations with Neo banks. These partnerships allow traditional banks to leverage the technological capabilities and customer-centric approach of Neo banks, while Neo banks benefit from the established customer base and regulatory complianceof traditional banks. Such partnerships enable both parties to offer innovative and comprehensive financial solutions to customers.

Increased Funding and Investments: The Asia-Pacific Neo banking market has attracted significant funding and investments from venture capital firms, private equity investors, and strategic investors. Funding rounds and investments have enabled Neo banks to expand their operations, enhance their technology infrastructure, and fuel their growth strategies. This influx of capital has contributed to the competitiveness and growth of the Neo banking sector.

Expansion into New Markets: Neo banks in the Asia-Pacific region have expanded their operations beyond their home markets, venturing into new geographies. They have entered neighboring countries or targeted specific markets with favorable regulatory environments and high growth potential. This expansion has allowed Neo banks to tap into new customer segments and diversify their revenue streams.

Emphasis on Data Privacy and Security: Data privacy and security have become paramount concerns for Neo banks. They have implemented robust security measures, complied with data protection regulations, and focused on building trust among customers by ensuring the confidentiality and integrity of customer data. Neo banks have invested in cybersecurity technologies and established robust risk management frameworks to safeguard customer information.

These key industry developments reflect the dynamic nature of the Asia-Pacific Neo banking market. Regulatory reforms, partnerships, investments, expansion into new markets, and a strong focus on data privacy and security have shaped the growth and competitiveness of Neo banks in the region.

Analyst Suggestions

Embrace Customer-Centricity: Neo banks should continue to prioritize customer experience and tailor their offerings to meet evolving customer needs and preferences. By leveraging customer data, advanced analytics, and artificial intelligence, Neo banks can offer personalized recommendations, customized financial products, and seamless user experiences.

Strengthen Regulatory Compliance: Neo banks must remain vigilant about regulatory changes and invest in robust compliance systems. They should establish strong partnerships with regulators, engage in open dialogue, and proactively adopt best practices to ensure compliance while driving innovation. Building trust with regulators is essential for sustained growth and market expansion.

Foster Collaboration and Partnerships: Neo banks should actively seek collaboration and partnerships with traditional banks, fintech startups, and technology companies. Collaborative efforts can leverage complementary strengths and enable Neo banks to offer a broader range of financial services, access larger customer bases, and drive innovation through knowledge sharing and joint initiatives.

Invest in Technology and Innovation: Neo banks should continue to invest in technology infrastructure, data analytics capabilities, and cybersecurity measures. Staying at the forefront of technological advancements allows Neo banks to deliver innovative products, streamline operations, and enhance security, ensuring a competitive edge in the market.

Educate and Raise Awareness: Neo banks should invest in customer education programs to raise awareness about the benefits and safety of digital banking. Educating customers about the convenience, security, and value-added services offered by Neo banks can help overcome trust barriers and accelerate adoption in both urban and rural areas.

Foster Financial Inclusion: Neo banks should actively contribute to financial inclusion by reaching unbanked and underbanked populations. They should develop tailored solutions, simplified account opening processes, and localized customer support to cater to the unique needs of these segments. Neo banks can collaborate with local communities, governments, and non-profit organizations to drive financial literacy and empower underserved populations.

Future Outlook

The future of the Asia-Pacific Neo banking market appears promising, with several trends and factors driving its growth and evolution.

Continued Growth and Market Expansion: The Asia-Pacific Neo banking market is expected to continue its growth trajectory, driven by factors such as increasing smartphone penetration, rising internet connectivity, and changing customer preferences. Untapped markets, particularly in rural areas and emerging economies, offer significant growth opportunities for Neo banks to expand their customer base and market share.

Regulatory Frameworks and Compliance: Regulatory frameworks will continue to evolve to accommodate the growth of Neo banking and fintech. Regulators will focus on striking a balance between promoting innovation and ensuring consumer protection, requiring Neo banks to remain agile and compliant with changing regulations. Collaboration between Neo banks and regulators will be crucial for shaping the regulatory landscape and fostering a conducive environment for digital banking.

Technology Advancements and Innovation: Technological advancements, including artificial intelligence, machine learning, and blockchain, will continue to drive innovation in the Neo banking sector. Neo banks will leverage these technologies to enhance customer experiences, automate processes, and improve security measures. Emerging technologies such as decentralized finance (DeFi) and central bank digital currencies (CBDCs) may also shape the future landscape of Neo banking.

Enhanced Collaboration and Partnerships: Collaboration and partnerships between Neo banks, traditional banks, fintech startups, and technology companies will increase in the future. These collaborations will enable knowledge sharing, accelerate innovation, and create synergies to offer comprehensive financial solutions to customers. Neo banks will also explore partnerships with e-commerce platforms, ride-hailing apps, and other non-financial platforms to provide embedded financial services.

Focus on Sustainability and Responsible Banking: Neo banks are likely to place greater emphasis on sustainability and responsible banking practices. Customers’ demand for ESG investing and sustainable financial solutions will drive Neo banks to integrate ESG principles into their offerings. Neo banks will also contribute to social causes, support financial literacy programs, and promote financial inclusion to create a positive impact in the communities they serve.

Evolving Customer Expectations: Customer expectations will continue to evolve, driven by advancements in technology, changing demographics, and socioeconomic factors. Neo banks will need to stay attuned to these evolving expectations and tailor their offerings to meet the unique needs of different customer segments. Personalization, convenience, and seamless user experiences will remain key drivers of customer satisfaction and loyalty.

Conclusion

In conclusion, the Asia-Pacific Neo banking market is poised for significant growth and transformation. Neo banks have disrupted the traditional banking landscape by offering convenient, user-friendly, and innovative financial solutions. Through technology, collaboration, and a customer-centric approach, Neo banks have the potential to drive financial inclusion, shape the future of banking, and meet the evolving needs of customers in the Asia-Pacific region.

What is Neo Banking?

Neo Banking refers to digital-only banks that operate without physical branches, offering services such as savings accounts, loans, and payment solutions through mobile apps and online platforms. They leverage technology to provide a seamless banking experience to consumers and businesses.

What are the key players in the Asia-Pacific Neo Banking Market?

Key players in the Asia-Pacific Neo Banking Market include companies like Revolut, N26, and Monzo, which are known for their innovative banking solutions. Additionally, local players such as Judo Bank and Up Bank are also making significant strides in this space, among others.

What are the main drivers of growth in the Asia-Pacific Neo Banking Market?

The growth of the Asia-Pacific Neo Banking Market is driven by increasing smartphone penetration, a growing preference for digital financial services, and the demand for faster and more convenient banking solutions. Additionally, the rise of fintech innovations is reshaping consumer expectations.

What challenges does the Asia-Pacific Neo Banking Market face?

The Asia-Pacific Neo Banking Market faces challenges such as regulatory compliance, cybersecurity threats, and competition from traditional banks. These factors can hinder the growth and operational efficiency of neo banks in the region.

What opportunities exist in the Asia-Pacific Neo Banking Market?

Opportunities in the Asia-Pacific Neo Banking Market include expanding into underserved markets, offering personalized financial products, and leveraging artificial intelligence for enhanced customer service. The increasing adoption of digital wallets also presents a significant growth avenue.

What trends are shaping the Asia-Pacific Neo Banking Market?

Trends shaping the Asia-Pacific Neo Banking Market include the rise of open banking, the integration of advanced technologies like blockchain, and a focus on sustainability in banking practices. These trends are influencing how neo banks operate and engage with customers.

Leading Companies in the Asia-Pacific Neo Banking Market:

WeBank (Tencent Holdings Limited)

MYbank (Alibaba Group Holding Limited)

Kakaobank Corporation

Atom Bank plc

Chime Financial, Inc.

N26 GmbH

Monzo Bank Limited

Revolut Ltd.

Starling Bank Limited

Varo Money, Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.