444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Asia Pacific negative pressure wound therapy market represents one of the fastest-growing segments in the global wound care industry, driven by increasing healthcare investments, rising prevalence of chronic wounds, and advancing medical technologies. This innovative therapeutic approach utilizes controlled negative pressure to promote wound healing through enhanced blood flow, reduced bacterial load, and accelerated tissue regeneration. The region’s expanding elderly population, coupled with growing incidence of diabetes and cardiovascular diseases, has created substantial demand for advanced wound care solutions.

Market dynamics in the Asia Pacific region are characterized by rapid technological adoption, increasing healthcare infrastructure development, and rising awareness about advanced wound care management. Countries such as Japan, China, India, and Australia are leading the adoption of negative pressure wound therapy systems, with healthcare providers increasingly recognizing the clinical and economic benefits of these advanced treatment modalities. The market is experiencing robust growth at a CAGR of 8.2%, reflecting the region’s commitment to improving patient outcomes and reducing healthcare costs.

Healthcare modernization across Asia Pacific nations has accelerated the integration of sophisticated wound care technologies into clinical practice. The region’s diverse healthcare landscape, ranging from highly developed systems in Japan and Singapore to rapidly evolving markets in Southeast Asia, presents unique opportunities for negative pressure wound therapy adoption. This growth trajectory is supported by increasing government healthcare spending, which accounts for approximately 6.8% of regional GDP, and growing private healthcare investments.

The Asia Pacific negative pressure wound therapy market refers to the comprehensive ecosystem of medical devices, consumables, and services that utilize controlled vacuum pressure to enhance wound healing processes across the Asia Pacific region. This therapeutic approach involves the application of sub-atmospheric pressure to wound sites through specialized dressing systems and vacuum pumps, creating an environment that promotes faster healing, reduces infection risk, and improves patient comfort.

Negative pressure wound therapy encompasses various treatment modalities including traditional vacuum-assisted closure systems, portable devices for home care applications, and advanced smart systems with integrated monitoring capabilities. The technology works by removing excess fluid from wound sites, increasing local blood flow, promoting granulation tissue formation, and reducing bacterial colonization. This comprehensive approach to wound management has revolutionized treatment protocols for complex wounds, surgical sites, and chronic conditions across healthcare facilities throughout the Asia Pacific region.

Strategic market analysis reveals that the Asia Pacific negative pressure wound therapy market is experiencing unprecedented growth driven by demographic shifts, technological advancements, and evolving healthcare delivery models. The region’s aging population, with individuals over 65 representing approximately 12.4% of the total population, is creating sustained demand for advanced wound care solutions. This demographic trend, combined with increasing prevalence of lifestyle-related diseases, positions negative pressure wound therapy as a critical component of modern healthcare infrastructure.

Key market drivers include rising healthcare expenditure, expanding hospital networks, growing awareness of advanced wound care benefits, and increasing adoption of value-based healthcare models. The market is characterized by strong competition among international and regional players, with continuous innovation in device portability, user-friendliness, and treatment efficacy. MarkWide Research indicates that the integration of digital health technologies and telemedicine capabilities is becoming increasingly important for market differentiation and clinical effectiveness.

Regional variations in market development reflect diverse healthcare systems, regulatory environments, and economic conditions across Asia Pacific countries. Developed markets such as Japan and Australia demonstrate high adoption rates and sophisticated treatment protocols, while emerging markets including India, Indonesia, and Vietnam present significant growth opportunities driven by healthcare infrastructure expansion and increasing medical tourism activities.

Critical market insights reveal several transformative trends shaping the Asia Pacific negative pressure wound therapy landscape:

Demographic transformation across the Asia Pacific region serves as the primary catalyst for negative pressure wound therapy market expansion. The rapidly aging population, particularly in developed countries like Japan where seniors comprise over 28% of the population, creates sustained demand for advanced wound care solutions. This demographic shift coincides with increasing prevalence of chronic conditions such as diabetes, which affects approximately 11.1% of adults in the region, leading to higher incidence of complex wounds requiring specialized treatment.

Healthcare infrastructure development represents another significant driver, with governments across the region investing heavily in hospital construction, medical equipment procurement, and healthcare professional training. Countries such as China and India are expanding their healthcare networks rapidly, creating new opportunities for negative pressure wound therapy adoption. The growing emphasis on quality healthcare delivery and patient safety standards is encouraging healthcare providers to invest in advanced wound care technologies.

Economic factors including rising disposable incomes, expanding health insurance coverage, and growing medical tourism industry are contributing to market growth. The region’s increasing focus on value-based healthcare delivery models is driving adoption of technologies that demonstrate clear clinical and economic benefits. Cost-effectiveness studies consistently show that negative pressure wound therapy reduces overall treatment costs by minimizing complications, shortening healing times, and reducing hospital readmissions.

Technological advancement in device design, including development of quieter, more portable, and user-friendly systems, is expanding the application scope of negative pressure wound therapy. Integration of smart technologies, wireless connectivity, and data analytics capabilities is enhancing treatment monitoring and outcomes measurement, making these systems more attractive to healthcare providers focused on evidence-based care delivery.

High initial costs associated with negative pressure wound therapy systems present significant barriers to adoption, particularly in price-sensitive markets across developing Asia Pacific countries. The substantial capital investment required for equipment procurement, along with ongoing consumable costs, can strain healthcare budgets and limit accessibility for smaller healthcare facilities. This cost consideration is particularly challenging in rural and underserved areas where healthcare resources are already constrained.

Limited reimbursement coverage in several Asia Pacific countries restricts patient access to negative pressure wound therapy, as many healthcare systems have not yet established comprehensive coverage policies for advanced wound care technologies. The absence of standardized reimbursement frameworks creates uncertainty for healthcare providers and patients, potentially limiting treatment adoption despite proven clinical benefits.

Training and expertise requirements pose additional challenges, as effective negative pressure wound therapy implementation requires specialized knowledge and skills among healthcare professionals. The need for comprehensive training programs and ongoing education can create implementation delays and increase operational costs for healthcare facilities. Additionally, the complexity of device operation and maintenance may deter adoption in resource-limited settings.

Regulatory complexities across different Asia Pacific countries create market entry barriers for manufacturers and can delay product availability. Varying approval processes, quality standards, and documentation requirements necessitate significant regulatory investment and expertise, potentially limiting innovation and competition in certain markets.

Emerging market penetration presents substantial growth opportunities as developing Asia Pacific countries continue expanding their healthcare infrastructure and increasing healthcare spending. Countries such as Vietnam, Thailand, and the Philippines are experiencing rapid economic growth and healthcare modernization, creating favorable conditions for negative pressure wound therapy adoption. The growing middle class in these markets is driving demand for quality healthcare services and advanced treatment options.

Home healthcare expansion represents a transformative opportunity, with portable negative pressure wound therapy devices enabling treatment delivery in home settings. This trend aligns with regional preferences for home-based care and government initiatives to reduce healthcare costs while improving patient satisfaction. The development of user-friendly, cost-effective home care systems could significantly expand the addressable market.

Digital health integration offers opportunities for market differentiation and improved patient outcomes through incorporation of telemedicine capabilities, remote monitoring, and data analytics. The Asia Pacific region’s rapid adoption of digital technologies creates favorable conditions for smart wound care solutions that can provide real-time treatment monitoring and clinical decision support.

Medical tourism growth in countries such as Thailand, Singapore, and Malaysia creates opportunities for advanced wound care service provision to international patients seeking high-quality, cost-effective treatment options. The region’s reputation for medical excellence and competitive pricing positions it well for capturing medical tourism revenue through advanced wound care capabilities.

Competitive dynamics in the Asia Pacific negative pressure wound therapy market are characterized by intense competition among global leaders and emerging regional players. Market participants are focusing on product innovation, strategic partnerships, and geographic expansion to capture market share. The competitive landscape is evolving rapidly with new entrants introducing cost-effective solutions tailored to regional market needs and preferences.

Supply chain considerations play a crucial role in market dynamics, with manufacturers establishing regional distribution networks and local partnerships to ensure product availability and technical support. The COVID-19 pandemic highlighted the importance of supply chain resilience, leading to increased focus on regional manufacturing capabilities and inventory management strategies.

Innovation cycles are accelerating as companies invest in research and development to create next-generation negative pressure wound therapy systems. Focus areas include device miniaturization, battery life improvement, noise reduction, and integration of smart technologies. The rapid pace of innovation is creating opportunities for market disruption and competitive advantage.

Regulatory evolution across the region is creating both challenges and opportunities, with harmonization efforts aimed at streamlining approval processes while maintaining safety and efficacy standards. Regulatory agencies are increasingly collaborating to establish common frameworks and mutual recognition agreements, potentially accelerating market access for innovative products.

Comprehensive market analysis employs a multi-faceted research approach combining primary and secondary research methodologies to ensure accuracy and reliability of market insights. Primary research involves extensive interviews with healthcare professionals, hospital administrators, device manufacturers, and regulatory experts across key Asia Pacific markets to gather firsthand insights into market trends, challenges, and opportunities.

Secondary research encompasses analysis of published clinical studies, regulatory filings, company financial reports, industry publications, and government healthcare statistics. This approach provides comprehensive coverage of market dynamics, competitive landscape, and regulatory environment across different countries and market segments within the Asia Pacific region.

Data validation processes include cross-referencing multiple sources, conducting expert interviews for verification, and applying statistical analysis techniques to ensure data accuracy and consistency. Market sizing and forecasting models incorporate historical trends, current market conditions, and future growth drivers to provide reliable projections for strategic planning purposes.

Geographic coverage includes detailed analysis of major Asia Pacific markets including China, Japan, India, Australia, South Korea, Singapore, Thailand, Malaysia, Indonesia, Philippines, and Vietnam. Country-specific analysis considers unique healthcare systems, regulatory environments, economic conditions, and cultural factors that influence negative pressure wound therapy adoption and market development.

China represents the largest and fastest-growing market for negative pressure wound therapy in the Asia Pacific region, driven by massive healthcare infrastructure investments, growing elderly population, and increasing prevalence of chronic diseases. The country’s healthcare reform initiatives and emphasis on quality improvement are creating favorable conditions for advanced wound care technology adoption. China accounts for approximately 35% of regional market share, with continued growth expected as healthcare access expands to rural areas.

Japan maintains a leadership position in technology adoption and clinical sophistication, with high penetration rates of advanced negative pressure wound therapy systems across hospitals and long-term care facilities. The country’s aging society and well-established healthcare infrastructure support sustained market growth, though market maturity limits expansion potential compared to emerging markets.

India presents significant growth opportunities driven by expanding healthcare infrastructure, increasing healthcare spending, and growing awareness of advanced wound care benefits. The country’s large population base, rising incidence of diabetes, and expanding private healthcare sector create substantial market potential. Government initiatives to improve healthcare access and quality are supporting market development.

Australia and New Zealand demonstrate high adoption rates and sophisticated treatment protocols, with strong emphasis on evidence-based care and cost-effectiveness. These markets serve as important reference points for clinical outcomes and treatment protocols that influence adoption in other regional markets.

Southeast Asian markets including Thailand, Malaysia, Singapore, Indonesia, and the Philippines are experiencing rapid growth driven by economic development, healthcare modernization, and increasing medical tourism. These markets collectively represent approximately 18% of regional demand, with strong growth potential as healthcare infrastructure continues expanding.

Market leadership is contested among several global and regional players, each bringing unique strengths and market positioning strategies. The competitive landscape is characterized by continuous innovation, strategic partnerships, and geographic expansion efforts aimed at capturing market share in this rapidly growing segment.

By Product Type:

By Wound Type:

By End User:

Traditional NPWT systems continue to dominate the market, representing approximately 58% of total demand, driven by their proven clinical efficacy and comprehensive treatment capabilities. These systems are particularly favored in hospital settings where complex wounds require intensive monitoring and treatment protocols. The segment benefits from extensive clinical evidence and established reimbursement frameworks in developed markets.

Portable NPWT devices are experiencing the fastest growth, with adoption rates increasing by 15.3% annually, as healthcare systems seek to reduce costs while improving patient satisfaction through home-based care delivery. These devices are particularly popular in countries with well-developed home healthcare infrastructure and supportive reimbursement policies.

Chronic wound applications represent the largest treatment category, driven by increasing prevalence of diabetes and aging populations across the Asia Pacific region. Diabetic foot ulcers alone account for approximately 42% of chronic wound treatments, reflecting the growing diabetes epidemic and need for specialized wound care management.

Hospital end users maintain the largest market share, though home healthcare applications are growing rapidly as portable technologies improve and healthcare delivery models evolve. The shift toward value-based care is encouraging hospitals to invest in technologies that reduce readmissions and improve patient outcomes while controlling costs.

Healthcare providers benefit from improved patient outcomes, reduced treatment costs, and enhanced operational efficiency through negative pressure wound therapy adoption. Clinical benefits include faster healing times, reduced infection rates, and lower complication rates, leading to improved patient satisfaction and reduced liability exposure. Economic benefits include shorter hospital stays, reduced readmissions, and more efficient resource utilization.

Patients experience significant advantages including accelerated healing, reduced pain, improved mobility, and enhanced quality of life during treatment. The technology’s ability to reduce dressing changes and enable home-based care provides convenience and comfort while maintaining clinical effectiveness. Long-term benefits include reduced scarring and improved functional outcomes.

Healthcare systems realize substantial cost savings through reduced overall treatment costs, decreased hospital resource utilization, and improved care coordination. The technology supports value-based care initiatives by demonstrating clear clinical and economic outcomes that align with quality improvement and cost containment objectives.

Medical device manufacturers benefit from growing market demand, opportunities for innovation, and potential for market expansion into emerging Asia Pacific countries. The market’s growth trajectory provides sustainable revenue opportunities and incentives for continued research and development investment.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital transformation is revolutionizing negative pressure wound therapy through integration of IoT connectivity, mobile applications, and cloud-based data management systems. These smart technologies enable remote monitoring, real-time treatment adjustments, and comprehensive outcome tracking, improving both clinical effectiveness and operational efficiency. Healthcare providers are increasingly demanding systems that provide data analytics and clinical decision support capabilities.

Personalized medicine approaches are gaining traction as healthcare providers seek to optimize treatment protocols based on individual patient characteristics, wound types, and healing patterns. Advanced systems now offer customizable pressure settings, treatment cycles, and monitoring parameters tailored to specific patient needs and clinical conditions.

Sustainability initiatives are influencing product development as healthcare systems focus on environmental responsibility and waste reduction. Manufacturers are developing more sustainable packaging, recyclable components, and energy-efficient devices to meet growing environmental consciousness among healthcare providers and patients.

Value-based care adoption is driving demand for negative pressure wound therapy systems that demonstrate clear clinical and economic outcomes. Healthcare providers are increasingly evaluating technologies based on their ability to improve patient outcomes while reducing overall treatment costs and resource utilization.

Recent innovations in negative pressure wound therapy technology include development of ultra-portable devices weighing less than 300 grams, enabling greater patient mobility and comfort during treatment. Advanced battery technologies now provide up to 7 days of continuous operation, reducing maintenance requirements and improving treatment continuity.

Regulatory approvals for new indications and patient populations are expanding the addressable market, with recent approvals for pediatric applications and specific wound types previously considered challenging for negative pressure therapy. These expanded indications are creating new growth opportunities and clinical applications.

Strategic partnerships between device manufacturers and healthcare providers are becoming more common, with collaborative agreements focusing on clinical research, outcome measurement, and technology optimization. MWR analysis indicates that these partnerships are crucial for driving evidence-based adoption and market expansion.

Manufacturing expansion in the Asia Pacific region is reducing costs and improving product availability, with several major manufacturers establishing regional production facilities to serve growing local demand while reducing supply chain risks and logistics costs.

Market entry strategies for new participants should focus on emerging markets with growing healthcare infrastructure and limited competition from established players. Success requires understanding local healthcare systems, regulatory requirements, and cultural preferences that influence technology adoption and clinical practice patterns.

Product development priorities should emphasize cost-effectiveness, ease of use, and integration with existing healthcare workflows. Manufacturers should invest in developing solutions specifically tailored to Asia Pacific market needs, including multilingual interfaces, local technical support, and culturally appropriate training programs.

Partnership opportunities with regional distributors, healthcare providers, and technology companies can accelerate market penetration and provide valuable local market insights. Strategic alliances should focus on clinical education, outcome measurement, and evidence generation to support broader adoption.

Investment focus areas should include digital health integration, artificial intelligence applications, and sustainable technology development. These areas represent significant opportunities for differentiation and competitive advantage in an increasingly sophisticated market environment.

Market growth trajectory indicates continued expansion driven by demographic trends, technological advancement, and healthcare system evolution across the Asia Pacific region. The market is expected to maintain robust growth rates exceeding 8% annually through the forecast period, supported by increasing healthcare investments and expanding clinical applications.

Technology evolution will focus on artificial intelligence integration, predictive analytics, and automated treatment optimization. Future systems will likely incorporate machine learning algorithms to personalize treatment protocols and predict healing outcomes, further improving clinical effectiveness and cost-efficiency.

Geographic expansion will continue into underserved markets as healthcare infrastructure develops and economic conditions improve. Countries such as Myanmar, Cambodia, and Laos represent emerging opportunities as their healthcare systems modernize and adopt advanced medical technologies.

Regulatory harmonization efforts across the region will likely streamline market access and reduce barriers to innovation, creating more favorable conditions for new product introductions and market expansion. This trend will benefit both manufacturers and healthcare providers by reducing complexity and costs associated with multi-country operations.

The Asia Pacific negative pressure wound therapy market represents a dynamic and rapidly expanding segment of the global healthcare industry, driven by compelling demographic trends, technological innovation, and evolving healthcare delivery models. The region’s aging population, increasing prevalence of chronic diseases, and expanding healthcare infrastructure create sustained demand for advanced wound care solutions that demonstrate clear clinical and economic benefits.

Market opportunities are particularly significant in emerging economies where healthcare modernization and increasing healthcare spending are creating favorable conditions for technology adoption. The shift toward value-based care, emphasis on patient outcomes, and growing recognition of negative pressure wound therapy’s cost-effectiveness position this market for continued robust growth throughout the forecast period.

Success factors for market participants include understanding diverse regional healthcare systems, investing in clinical evidence generation, developing culturally appropriate solutions, and building strong local partnerships. The market’s evolution toward smart, connected devices with integrated digital health capabilities presents opportunities for differentiation and competitive advantage in an increasingly sophisticated healthcare environment.

What is Negative Pressure Wound Therapy?

Negative Pressure Wound Therapy (NPWT) is a medical treatment that uses a vacuum dressing to promote healing in acute and chronic wounds. It involves the application of negative pressure to the wound site, which helps to remove excess fluid, reduce edema, and enhance blood flow to the area.

What are the key players in the Asia Pacific Negative Pressure Wound Therapy Market?

Key players in the Asia Pacific Negative Pressure Wound Therapy Market include Acelity L.P. Inc., Smith & Nephew, and Mölnlycke Health Care, among others. These companies are known for their innovative products and solutions in wound care management.

What are the growth factors driving the Asia Pacific Negative Pressure Wound Therapy Market?

The growth of the Asia Pacific Negative Pressure Wound Therapy Market is driven by factors such as the increasing prevalence of chronic wounds, a rise in surgical procedures, and advancements in NPWT technology. Additionally, the growing awareness of wound care management is contributing to market expansion.

What challenges does the Asia Pacific Negative Pressure Wound Therapy Market face?

The Asia Pacific Negative Pressure Wound Therapy Market faces challenges such as high treatment costs, limited reimbursement policies, and the need for skilled healthcare professionals to operate NPWT devices. These factors can hinder market growth and accessibility.

What opportunities exist in the Asia Pacific Negative Pressure Wound Therapy Market?

Opportunities in the Asia Pacific Negative Pressure Wound Therapy Market include the development of advanced NPWT systems, increasing investments in healthcare infrastructure, and the rising demand for home healthcare services. These trends are expected to enhance market potential.

What trends are shaping the Asia Pacific Negative Pressure Wound Therapy Market?

Trends shaping the Asia Pacific Negative Pressure Wound Therapy Market include the integration of smart technology in NPWT devices, the growing focus on personalized wound care solutions, and the increasing adoption of NPWT in outpatient settings. These innovations are transforming wound management practices.

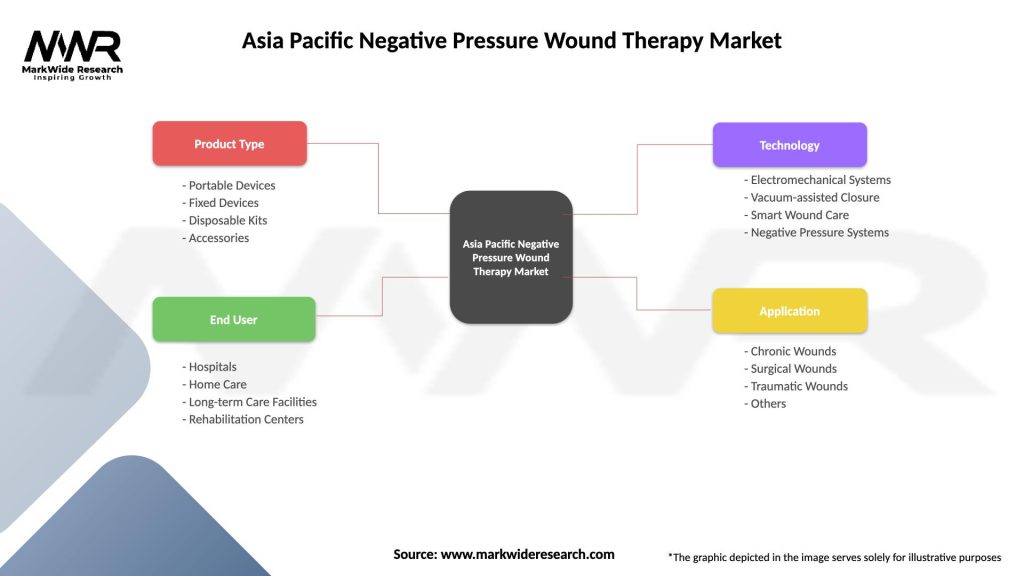

Asia Pacific Negative Pressure Wound Therapy Market

| Segmentation Details | Description |

|---|---|

| Product Type | Portable Devices, Fixed Devices, Disposable Kits, Accessories |

| End User | Hospitals, Home Care, Long-term Care Facilities, Rehabilitation Centers |

| Technology | Electromechanical Systems, Vacuum-assisted Closure, Smart Wound Care, Negative Pressure Systems |

| Application | Chronic Wounds, Surgical Wounds, Traumatic Wounds, Others |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Asia Pacific Negative Pressure Wound Therapy Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.