444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Asia-Pacific Less-than Container Load (LCL) market represents a dynamic and rapidly evolving segment of the global logistics industry, characterized by exceptional growth potential and increasing demand for flexible shipping solutions. This market encompasses the consolidation and transportation of smaller cargo shipments that do not require a full container, making international trade more accessible to small and medium-sized enterprises across the region.

Market dynamics in the Asia-Pacific region demonstrate robust expansion, with the LCL segment experiencing a compound annual growth rate (CAGR) of 8.2% driven by the proliferation of e-commerce, manufacturing diversification, and enhanced trade relationships between regional economies. The market’s growth trajectory reflects the increasing sophistication of supply chain networks and the growing demand for cost-effective shipping solutions among businesses of varying sizes.

Regional significance cannot be overstated, as Asia-Pacific accounts for approximately 45% of global LCL cargo volume, positioning the region as the world’s largest and most influential LCL market. Countries such as China, Japan, South Korea, Singapore, and India serve as major hubs for LCL operations, benefiting from advanced port infrastructure, strategic geographic positioning, and robust manufacturing capabilities.

Technology integration has become a defining characteristic of the modern LCL market, with digital platforms, automated cargo handling systems, and advanced tracking technologies transforming traditional consolidation processes. These innovations have improved operational efficiency by approximately 35% while reducing transit times and enhancing cargo visibility for shippers and consignees throughout the supply chain.

The Asia-Pacific Less-than Container Load (LCL) market refers to the comprehensive ecosystem of logistics services, infrastructure, and operational frameworks that facilitate the consolidation, transportation, and distribution of partial container shipments across the Asia-Pacific region, enabling cost-effective international trade for businesses with smaller cargo volumes.

LCL shipping fundamentally differs from Full Container Load (FCL) services by allowing multiple shippers to share container space, thereby reducing individual shipping costs and making international trade more accessible to small and medium enterprises. This consolidation model requires sophisticated coordination between freight forwarders, consolidation centers, and destination deconsolidation facilities to ensure efficient cargo handling and timely delivery.

Operational complexity within the LCL market involves multiple stakeholders, including consolidators, carriers, customs brokers, and final delivery agents, each playing crucial roles in the seamless movement of goods from origin to destination. The process typically involves cargo collection, consolidation at origin ports, ocean transportation, deconsolidation at destination ports, and final delivery to consignees.

Market participants range from global logistics giants to specialized regional consolidators, each offering unique value propositions tailored to specific trade lanes, cargo types, and customer requirements. The competitive landscape emphasizes service reliability, transit time optimization, and comprehensive door-to-door solutions that address the diverse needs of Asia-Pacific businesses engaged in international trade.

Strategic market positioning reveals the Asia-Pacific LCL market as a cornerstone of regional trade facilitation, driven by unprecedented growth in cross-border commerce, manufacturing expansion, and the increasing globalization of supply chains. The market demonstrates exceptional resilience and adaptability, successfully navigating challenges while capitalizing on emerging opportunities in digital transformation and sustainable logistics practices.

Growth catalysts include the rapid expansion of e-commerce platforms, which has increased demand for smaller, more frequent shipments by approximately 28% over recent years. Additionally, the region’s manufacturing sector diversification has created new trade patterns requiring flexible shipping solutions that can accommodate varying cargo volumes and delivery schedules.

Technological advancement serves as a primary differentiator in the competitive landscape, with leading service providers investing heavily in digital platforms, artificial intelligence, and blockchain technologies to enhance operational efficiency and customer experience. These innovations have resulted in improved cargo tracking accuracy rates exceeding 95% and reduced documentation processing times.

Market consolidation trends indicate increasing collaboration between traditional freight forwarders and technology-enabled logistics platforms, creating hybrid service models that combine operational expertise with digital innovation. This convergence has enhanced service quality while expanding market reach to previously underserved segments and geographic areas.

Future trajectory projections suggest continued robust growth, supported by ongoing infrastructure development, trade agreement implementations, and the increasing adoption of sustainable shipping practices that align with regional environmental objectives and corporate sustainability initiatives.

Fundamental market insights reveal several critical trends shaping the Asia-Pacific LCL landscape, providing valuable intelligence for stakeholders seeking to understand market dynamics and capitalize on emerging opportunities.

Market intelligence indicates that successful LCL operators are those who effectively balance operational efficiency with customer-centric service delivery, leveraging technology to create competitive advantages while maintaining the personal relationships that characterize the logistics industry.

Primary growth drivers propelling the Asia-Pacific LCL market forward encompass a diverse range of economic, technological, and structural factors that collectively create a favorable environment for sustained expansion and innovation.

E-commerce proliferation stands as the most significant driver, with online retail growth generating unprecedented demand for flexible shipping solutions capable of handling smaller, more frequent shipments. The rise of cross-border e-commerce has particularly benefited LCL services, as online sellers require cost-effective methods to reach international customers without committing to full container loads.

Manufacturing diversification across the Asia-Pacific region has created new trade patterns and shipping requirements, with companies seeking to optimize supply chains through strategic sourcing from multiple locations. This trend has increased demand for LCL services that can efficiently handle varied cargo types and volumes from different origins to diverse destinations.

SME internationalization represents another crucial driver, as small and medium enterprises increasingly participate in global trade. LCL services provide these businesses with access to international markets that would otherwise be cost-prohibitive, democratizing global commerce and expanding the customer base for logistics service providers.

Infrastructure development throughout the region has enhanced the operational capabilities of LCL providers, with improved port facilities, transportation networks, and cargo handling equipment enabling more efficient consolidation and deconsolidation processes. These improvements have reduced operational costs while improving service reliability and transit times.

Trade agreement implementations have facilitated increased regional commerce, creating new opportunities for LCL services as businesses explore previously inaccessible markets. Reduced trade barriers and simplified customs procedures have made international shipping more attractive and feasible for a broader range of companies.

Operational challenges within the Asia-Pacific LCL market present significant constraints that service providers must navigate to maintain competitiveness and profitability. These restraints require strategic planning and innovative solutions to minimize their impact on market growth and service quality.

Complexity management represents a fundamental challenge, as LCL operations involve coordinating multiple shipments, diverse cargo types, and varying customer requirements within shared container space. This complexity increases the risk of delays, cargo damage, and documentation errors, potentially impacting customer satisfaction and operational efficiency.

Regulatory variations across different Asia-Pacific countries create compliance challenges for LCL operators, requiring extensive knowledge of local customs procedures, documentation requirements, and trade regulations. These variations can lead to delays, additional costs, and operational complications that affect service reliability and profitability.

Infrastructure limitations in certain regional markets constrain LCL operations, particularly in developing economies where port facilities, transportation networks, and cargo handling capabilities may be inadequate for efficient consolidation and deconsolidation processes. These limitations can result in extended transit times and increased operational costs.

Capacity constraints during peak shipping seasons can significantly impact LCL services, as space allocation on vessels becomes competitive and expensive. Limited container availability and vessel capacity can force operators to delay shipments or increase rates, affecting customer relationships and market competitiveness.

Technology integration costs represent a significant barrier for smaller LCL operators seeking to modernize their operations and compete with larger, technology-enabled competitors. The investment required for digital platforms, tracking systems, and automated processes can strain financial resources and limit growth opportunities.

Emerging opportunities within the Asia-Pacific LCL market present substantial potential for growth, innovation, and market expansion, driven by evolving customer needs, technological advancement, and changing trade patterns across the region.

Digital platform development offers significant opportunities for LCL operators to differentiate their services and improve operational efficiency. Advanced booking systems, real-time tracking capabilities, and automated documentation processes can enhance customer experience while reducing operational costs and improving service reliability.

Sustainable logistics initiatives present opportunities for market leaders to develop environmentally responsible shipping solutions that appeal to increasingly eco-conscious customers. Carbon-neutral shipping options, optimized routing algorithms, and green consolidation practices can create competitive advantages while supporting corporate sustainability objectives.

Value-added services expansion enables LCL operators to increase revenue per shipment while providing comprehensive solutions that address diverse customer needs. Services such as cargo insurance, customs clearance, warehousing, and last-mile delivery can transform basic consolidation services into complete logistics solutions.

Emerging market penetration offers substantial growth potential, particularly in developing Asia-Pacific economies where LCL services remain underutilized. Strategic expansion into these markets can capture first-mover advantages while supporting local businesses’ international trade aspirations.

Partnership ecosystem development creates opportunities for collaborative growth through strategic alliances with carriers, technology providers, and complementary service providers. These partnerships can expand service capabilities, improve geographic coverage, and enhance competitive positioning without requiring significant capital investment.

Specialized sector focus allows LCL operators to develop expertise in specific industries or cargo types, creating niche market positions with higher margins and stronger customer relationships. Sectors such as automotive parts, electronics, textiles, and perishables offer specialized opportunities for tailored LCL solutions.

Dynamic market forces continuously shape the Asia-Pacific LCL landscape, creating an environment characterized by rapid change, competitive intensity, and evolving customer expectations. Understanding these dynamics is essential for stakeholders seeking to navigate market complexities and capitalize on emerging trends.

Competitive intensity has increased significantly as traditional freight forwarders face competition from technology-enabled platforms and integrated logistics providers. This competition has driven innovation, improved service quality, and reduced margins, forcing operators to differentiate through specialized services, superior customer experience, or operational efficiency.

Customer expectations continue to evolve, with shippers demanding greater transparency, faster transit times, and more flexible service options. The influence of e-commerce has particularly elevated expectations for real-time tracking, predictable delivery schedules, and responsive customer support, pushing LCL operators to invest in technology and service enhancement initiatives.

Technology disruption is reshaping traditional LCL operations through artificial intelligence, blockchain, and Internet of Things applications. These technologies are improving cargo visibility, optimizing consolidation processes, and enhancing operational efficiency by approximately 25% among early adopters, creating competitive advantages for technologically advanced operators.

Regulatory evolution across the Asia-Pacific region continues to impact LCL operations, with new trade agreements, customs procedures, and security requirements creating both opportunities and challenges. Operators must maintain compliance while adapting to changing regulatory landscapes that affect operational procedures and cost structures.

Supply chain integration trends are driving demand for LCL services that seamlessly connect with broader logistics networks, requiring operators to develop capabilities beyond traditional consolidation services. This integration includes warehousing, distribution, and value-added services that support comprehensive supply chain solutions.

Comprehensive research methodology employed in analyzing the Asia-Pacific LCL market incorporates multiple data sources, analytical techniques, and validation processes to ensure accuracy, reliability, and actionable insights for market stakeholders and decision-makers.

Primary research forms the foundation of market analysis, involving extensive interviews with industry executives, logistics professionals, and key stakeholders across the Asia-Pacific region. This primary data collection includes structured surveys, in-depth interviews, and focus group discussions with representatives from freight forwarders, shipping lines, consolidators, and end-user companies.

Secondary research encompasses comprehensive analysis of industry reports, trade publications, government statistics, and regulatory documents from relevant authorities across major Asia-Pacific markets. This secondary data provides historical context, market sizing information, and regulatory framework understanding essential for comprehensive market assessment.

Data validation processes ensure information accuracy through cross-referencing multiple sources, expert review panels, and statistical analysis techniques. Quantitative data undergoes rigorous verification procedures, while qualitative insights are validated through industry expert consultations and peer review processes.

Analytical frameworks employed include Porter’s Five Forces analysis, SWOT assessment, and competitive positioning models specifically adapted for the logistics industry. These frameworks provide structured approaches to understanding market dynamics, competitive landscapes, and strategic opportunities within the LCL sector.

Geographic coverage encompasses all major Asia-Pacific markets, including China, Japan, South Korea, Singapore, Hong Kong, India, Australia, Thailand, Malaysia, Indonesia, and other significant regional economies. This comprehensive geographic scope ensures representative market insights and identifies regional variations in market characteristics and growth patterns.

Regional market dynamics across the Asia-Pacific LCL sector reveal significant variations in market maturity, growth potential, and operational characteristics, reflecting the diverse economic conditions, infrastructure capabilities, and trade patterns present throughout the region.

China dominates the regional LCL market, accounting for approximately 38% of total market share, driven by its position as the world’s manufacturing hub and largest exporter. Chinese ports such as Shanghai, Shenzhen, and Ningbo serve as major consolidation centers, handling vast volumes of LCL cargo destined for global markets while also serving growing domestic demand for imported goods.

Japan represents a mature and sophisticated LCL market characterized by high service standards, advanced technology adoption, and strong demand for premium logistics services. Japanese companies prioritize reliability and precision in their shipping requirements, creating opportunities for value-added LCL services that command premium pricing.

Singapore functions as a critical regional hub, leveraging its strategic location, world-class port infrastructure, and business-friendly environment to serve as a consolidation and transshipment center for Southeast Asian LCL cargo. The country’s advanced logistics capabilities and regulatory efficiency make it an attractive base for regional LCL operations.

South Korea demonstrates strong LCL market growth, supported by its advanced manufacturing sector, particularly in electronics, automotive, and petrochemicals. Korean companies increasingly utilize LCL services for both export and import activities, driving demand for specialized handling capabilities and integrated logistics solutions.

India presents exceptional growth potential, with LCL market expansion driven by manufacturing diversification, e-commerce growth, and increasing participation in global trade. However, infrastructure constraints and regulatory complexities present challenges that operators must navigate to capitalize on market opportunities.

Southeast Asian markets including Thailand, Malaysia, Indonesia, and Vietnam demonstrate rapid LCL market development, supported by manufacturing growth, trade liberalization, and infrastructure investment. These markets offer significant expansion opportunities for established LCL operators seeking geographic diversification.

Competitive dynamics within the Asia-Pacific LCL market reflect a complex ecosystem of global logistics giants, regional specialists, and technology-enabled platforms, each competing through different value propositions and strategic approaches to capture market share and customer loyalty.

Market leaders include established global freight forwarders and logistics companies that leverage extensive networks, operational expertise, and financial resources to provide comprehensive LCL services across multiple trade lanes and geographic markets.

Competitive strategies vary significantly among market participants, with some focusing on technology differentiation, others emphasizing service quality and reliability, and still others competing primarily on price and operational efficiency. Successful companies typically combine multiple competitive advantages to create sustainable market positions.

Technology adoption has become a critical differentiator, with leading companies investing heavily in digital platforms, automated processes, and data analytics capabilities. According to MarkWide Research analysis, companies with advanced technology platforms demonstrate approximately 20% higher customer retention rates compared to traditional operators.

Market segmentation within the Asia-Pacific LCL sector reveals distinct categories based on various criteria including cargo type, trade lane, customer segment, and service level, each presenting unique characteristics, growth patterns, and competitive dynamics.

By Cargo Type:

By Trade Lane:

By Customer Segment:

Detailed category analysis provides deeper understanding of specific market segments within the Asia-Pacific LCL sector, revealing unique characteristics, growth drivers, and competitive dynamics that influence strategic decision-making and operational planning.

General Cargo Category represents the foundation of LCL operations, encompassing diverse manufactured goods, consumer products, and industrial materials. This category benefits from standardized handling procedures, established consolidation patterns, and predictable demand cycles. Growth in this segment correlates strongly with overall regional trade volumes and manufacturing activity.

Automotive Parts Segment demonstrates specialized requirements including precise handling protocols, temperature-controlled environments, and just-in-time delivery capabilities. The automotive industry’s shift toward regional supply chains has increased demand for reliable LCL services that can support lean manufacturing processes while maintaining quality standards.

Electronics Category requires premium service levels due to high cargo values, theft risks, and sensitivity to environmental conditions. This segment commands higher margins but demands significant investment in security systems, climate-controlled facilities, and comprehensive insurance coverage. The growth of consumer electronics and technology products drives continued expansion in this category.

E-commerce Segment represents the fastest-growing category, driven by cross-border online retail expansion and changing consumer shopping patterns. This segment requires specialized services including small parcel consolidation, fast transit times, and comprehensive tracking capabilities that align with e-commerce customer expectations.

Textiles and Apparel category exhibits seasonal demand patterns aligned with fashion cycles and retail seasons. This segment benefits from LCL services that can accommodate varying shipment sizes, provide flexible scheduling, and support fast-fashion supply chain requirements with quick turnaround times.

Industrial Machinery segment requires specialized handling capabilities, comprehensive documentation support, and often involves project cargo characteristics despite utilizing LCL services. This category typically generates higher revenue per shipment due to complex service requirements and value-added services.

Comprehensive benefits derived from participation in the Asia-Pacific LCL market extend across multiple stakeholder categories, creating value propositions that support business growth, operational efficiency, and strategic competitive advantages.

For Shippers:

For Logistics Service Providers:

For Regional Economies:

Strategic analysis of the Asia-Pacific LCL market through SWOT framework reveals critical internal capabilities and external factors that influence market development, competitive positioning, and future growth potential.

Strengths:

Weaknesses:

Opportunities:

Threats:

Transformative trends shaping the Asia-Pacific LCL market landscape reflect broader changes in global trade, technology adoption, and customer expectations, creating both opportunities and challenges for market participants.

Digital Platform Integration has emerged as a dominant trend, with LCL operators investing heavily in user-friendly booking systems, real-time tracking capabilities, and automated documentation processes. This digitalization has improved customer experience while reducing operational costs and increasing service transparency.

Sustainability Initiatives are gaining momentum as environmental consciousness increases among shippers and regulatory authorities. LCL operators are implementing carbon footprint reduction programs, optimizing routing algorithms, and developing green logistics solutions that appeal to environmentally conscious customers.

Service Consolidation trends show LCL providers expanding beyond traditional consolidation services to offer comprehensive logistics solutions including warehousing, customs clearance, and last-mile delivery. This trend toward integrated service offerings creates higher customer value and stronger competitive positioning.

Artificial Intelligence Adoption is revolutionizing LCL operations through predictive analytics, demand forecasting, and automated decision-making systems. AI applications are improving consolidation efficiency, optimizing routing decisions, and enhancing customer service capabilities.

Cross-border E-commerce Integration represents a significant trend as online retail platforms increasingly require specialized LCL services that can handle small parcel consolidation, provide fast transit times, and offer comprehensive tracking capabilities aligned with e-commerce customer expectations.

Regional Hub Development continues as operators establish strategic consolidation centers in key locations to optimize cargo flows, reduce transit times, and improve service reliability. This trend reflects the importance of geographic positioning in competitive LCL operations.

Blockchain Implementation is emerging as a solution for documentation challenges, supply chain transparency, and fraud prevention. Early adopters are exploring blockchain applications for bill of lading management, customs documentation, and cargo tracking systems.

Recent industry developments within the Asia-Pacific LCL market demonstrate the dynamic nature of the sector, with continuous innovation, strategic partnerships, and operational improvements driving market evolution and competitive repositioning.

Technology Partnerships between traditional freight forwarders and technology companies have accelerated digital transformation initiatives. These collaborations are producing advanced platforms that combine operational expertise with cutting-edge technology capabilities, improving service quality and operational efficiency.

Infrastructure Investments across major regional ports have enhanced LCL handling capabilities, with new consolidation facilities, automated cargo handling systems, and improved connectivity supporting increased throughput and service reliability. These investments reflect the growing importance of LCL services in regional trade facilitation.

Service Innovation initiatives include the development of specialized LCL solutions for specific industries, cargo types, and trade lanes. Companies are creating tailored services that address unique customer requirements while commanding premium pricing for specialized capabilities.

Regulatory Harmonization efforts across the region are simplifying customs procedures, standardizing documentation requirements, and reducing trade barriers. These developments improve operational efficiency and reduce costs for LCL operators while facilitating increased trade volumes.

Sustainability Programs launched by major LCL operators include carbon-neutral shipping options, optimized routing systems, and green consolidation practices. These programs respond to growing environmental awareness while creating competitive differentiation opportunities.

Acquisition Activity in the market reflects consolidation trends as larger operators acquire specialized companies to expand service capabilities, geographic coverage, or technology platforms. This activity is reshaping the competitive landscape and creating new market dynamics.

Customer Experience Initiatives focus on improving service transparency, communication, and problem resolution capabilities. Companies are investing in customer service platforms, mobile applications, and proactive communication systems to enhance customer satisfaction and loyalty.

Strategic recommendations for Asia-Pacific LCL market participants emphasize the importance of balancing operational excellence with innovation, customer focus with efficiency, and regional expertise with global capabilities to achieve sustainable competitive advantages.

Technology Investment Priorities should focus on customer-facing platforms that improve booking experience, provide real-time visibility, and enable self-service capabilities. Companies should prioritize investments that directly impact customer satisfaction while improving operational efficiency through automation and data analytics.

Service Differentiation Strategies must go beyond basic consolidation services to include value-added offerings that address specific customer needs and industry requirements. Successful differentiation requires deep understanding of customer pain points and the development of solutions that provide measurable value.

Geographic Expansion Approaches should prioritize markets with strong growth potential while considering infrastructure capabilities, regulatory environments, and competitive landscapes. Companies should develop market entry strategies that leverage existing strengths while adapting to local market characteristics.

Partnership Development initiatives should focus on creating strategic alliances that expand service capabilities, improve geographic coverage, or enhance technology platforms. Successful partnerships require clear value propositions for all parties and well-defined operational integration plans.

Sustainability Integration must become a core component of business strategy rather than an add-on service. Companies should develop comprehensive sustainability programs that reduce environmental impact while creating competitive advantages and meeting customer expectations.

Customer Relationship Management strategies should emphasize long-term partnership development through consistent service delivery, proactive communication, and continuous improvement initiatives. Strong customer relationships provide stability and growth opportunities in competitive markets.

Operational Excellence Programs should focus on continuous improvement initiatives that enhance service reliability, reduce costs, and improve customer satisfaction. Companies must balance efficiency improvements with service quality maintenance to achieve sustainable competitive positioning.

Future market projections for the Asia-Pacific LCL sector indicate continued robust growth driven by technological advancement, trade expansion, and evolving customer requirements, creating a dynamic environment with significant opportunities for well-positioned market participants.

Growth trajectory analysis suggests the market will maintain strong expansion momentum, with MWR projections indicating sustained growth rates exceeding 7.5% annually over the next five years. This growth will be supported by continued e-commerce expansion, manufacturing diversification, and infrastructure development across the region.

Technology evolution will continue reshaping LCL operations, with artificial intelligence, blockchain, and Internet of Things applications becoming standard operational tools rather than competitive differentiators. Companies that successfully integrate these technologies will achieve significant operational advantages and improved customer experiences.

Market consolidation trends are expected to continue, with larger operators acquiring specialized companies and technology platforms to expand capabilities and geographic coverage. This consolidation will create more comprehensive service providers while potentially reducing the number of independent operators.

Service sophistication will increase as customers demand more comprehensive logistics solutions that extend beyond basic consolidation services. Future LCL providers will need to offer integrated supply chain solutions that address diverse customer requirements across multiple touchpoints.

Regulatory evolution will continue simplifying trade procedures and reducing barriers to international commerce, creating opportunities for increased LCL volumes while requiring operators to maintain compliance with evolving requirements across multiple jurisdictions.

Sustainability requirements will become increasingly important, with environmental considerations influencing customer decisions and regulatory compliance. Companies that proactively develop sustainable operations will gain competitive advantages in an increasingly environmentally conscious market.

Regional integration will deepen as trade agreements and infrastructure development improve connectivity between Asia-Pacific economies, creating new opportunities for LCL services while intensifying competition across traditional market boundaries.

The Asia-Pacific less-than container load (LCL) market represents a fundamental pillar of the region’s international trade infrastructure, embodying the complex logistics ecosystem that enables efficient movement of smaller cargo shipments across diverse economies and geographical territories. This comprehensive analysis has revealed a market characterized by strategic importance in global supply chains, technological innovation in consolidation processes, and critical role in supporting small and medium enterprises’ international trade participation throughout the dynamic Asia-Pacific region.

Market significance extends far beyond simple cargo consolidation services, encompassing sophisticated logistics solutions that democratize international shipping access for businesses that cannot justify full container loads. The evolution of LCL service offerings has created comprehensive trade facilitation platforms that combine transportation, warehousing, customs clearance, and value-added services in integrated solutions tailored to diverse shipper requirements and destination market characteristics.

Operational excellence has emerged as the primary differentiator in competitive positioning, with successful LCL providers investing heavily in consolidation facility optimization, cargo handling automation, and tracking technology integration. The development of hub-and-spoke network models has enabled efficient cargo distribution while maintaining cost-effectiveness and service reliability across the region’s vast geographical distances and diverse port infrastructures.

Digital transformation has revolutionized LCL operations through advanced visibility platforms, automated documentation systems, and predictive analytics that enhance operational efficiency while improving customer experience. MarkWide Research findings indicate that LCL providers implementing comprehensive digital solutions achieve superior on-time performance, reduced cargo damage rates, and enhanced customer satisfaction compared to traditional service models.

Trade facilitation impact demonstrates the LCL market’s essential role in supporting regional economic development by enabling smaller businesses to access international markets without prohibitive shipping costs or complex logistics requirements. The sector’s contribution to inclusive trade growth has been particularly significant in emerging economies where SME exporters rely heavily on consolidated shipping services to compete in global markets.

Supply chain integration has evolved from basic transportation services to comprehensive logistics partnerships that include inventory management, distribution planning, and supply chain optimization consulting. The development of end-to-end visibility solutions has enabled shippers to make informed decisions about inventory positioning, production planning, and market entry strategies based on real-time cargo status information.

Sustainability initiatives have become increasingly important as environmental consciousness influences shipping decisions and regulatory requirements. The LCL sector’s inherent efficiency in cargo consolidation contributes to reduced carbon footprint per unit compared to alternative shipping methods, while ongoing investments in clean transportation technologies and optimized routing algorithms further enhance environmental performance.

Regional connectivity enhancement has been facilitated through expanded service networks, improved intermodal connections, and strategic partnerships that create seamless cargo flows between major trade centers and secondary markets. The establishment of specialized LCL corridors for high-volume trade lanes has improved service frequency and reduced transit times while maintaining competitive pricing structures.

As the Asia-Pacific LCL market continues to evolve and expand, stakeholders must navigate emerging challenges including capacity constraints, port congestion, and evolving trade patterns while capitalizing on opportunities in e-commerce growth, cross-border trade facilitation, and technology-enabled service enhancement. The successful adaptation to changing market dynamics will require continued investment in infrastructure development, technology advancement, and service innovation that maintains the LCL sector’s critical role in supporting efficient, accessible, and sustainable international trade across the Asia-Pacific region’s diverse and interconnected economic landscape.

What is Less-than Container Load (LCL)?

Less-than Container Load (LCL) refers to a shipping method where multiple shipments from different customers are consolidated into a single container. This approach is cost-effective for businesses that do not have enough goods to fill an entire container, allowing for efficient transportation of smaller loads.

What are the key companies in the Asia-Pacific Less-than Container Load (LCL) Market?

Key companies in the Asia-Pacific Less-than Container Load (LCL) Market include DHL Supply Chain, Kuehne + Nagel, and DB Schenker, among others. These companies provide various logistics and freight forwarding services tailored to LCL shipping needs.

What are the growth factors driving the Asia-Pacific Less-than Container Load (LCL) Market?

The growth of the Asia-Pacific Less-than Container Load (LCL) Market is driven by increasing international trade, the rise of e-commerce, and the demand for cost-effective shipping solutions. Additionally, the need for flexible logistics options is contributing to market expansion.

What challenges does the Asia-Pacific Less-than Container Load (LCL) Market face?

The Asia-Pacific Less-than Container Load (LCL) Market faces challenges such as fluctuating freight rates, port congestion, and regulatory compliance issues. These factors can impact shipping efficiency and costs for businesses relying on LCL services.

What opportunities exist in the Asia-Pacific Less-than Container Load (LCL) Market?

Opportunities in the Asia-Pacific Less-than Container Load (LCL) Market include the expansion of digital freight platforms and the increasing demand for sustainable shipping practices. Companies are also exploring innovative logistics solutions to enhance service offerings.

What trends are shaping the Asia-Pacific Less-than Container Load (LCL) Market?

Trends shaping the Asia-Pacific Less-than Container Load (LCL) Market include the adoption of technology for tracking shipments, increased focus on sustainability, and the growth of multi-modal transport solutions. These trends are enhancing operational efficiency and customer satisfaction.

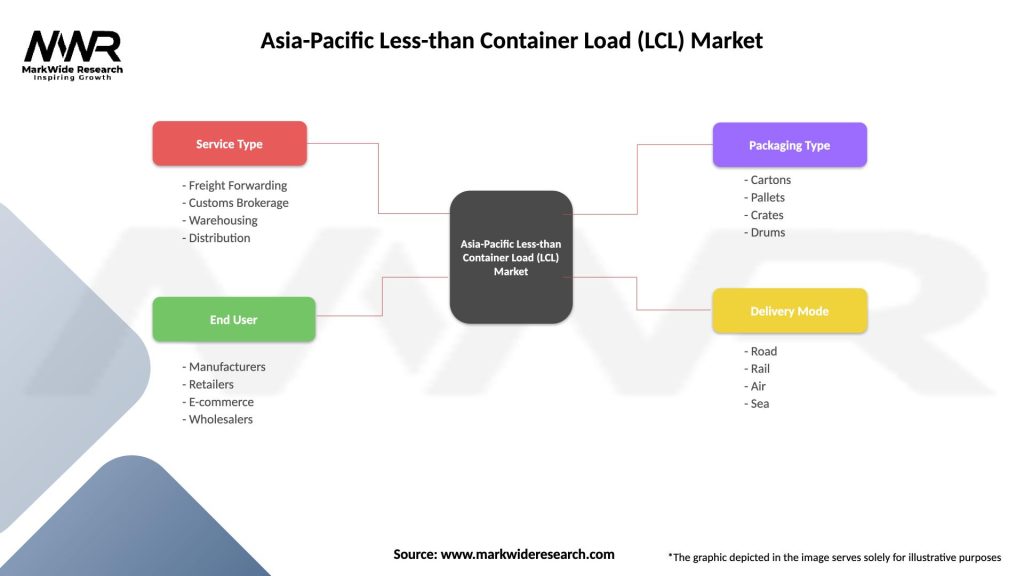

Asia-Pacific Less-than Container Load (LCL) Market

| Segmentation Details | Description |

|---|---|

| Service Type | Freight Forwarding, Customs Brokerage, Warehousing, Distribution |

| End User | Manufacturers, Retailers, E-commerce, Wholesalers |

| Packaging Type | Cartons, Pallets, Crates, Drums |

| Delivery Mode | Road, Rail, Air, Sea |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Asia-Pacific Less-than Container Load (LCL) Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.