444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Asia-Pacific EV battery pack market represents one of the most dynamic and rapidly evolving segments within the global electric vehicle ecosystem. This region has emerged as the epicenter of electric vehicle adoption and battery technology innovation, driven by aggressive government policies, substantial manufacturing capabilities, and increasing consumer acceptance of electric mobility solutions. Market dynamics in the Asia-Pacific region are characterized by intense competition among battery manufacturers, continuous technological advancements, and significant investments in research and development.

Regional leadership in this market is primarily concentrated in countries such as China, Japan, South Korea, and increasingly India, where major battery manufacturers have established comprehensive production facilities. The market encompasses various battery chemistries, including lithium-ion, lithium iron phosphate, and emerging solid-state technologies. Growth trajectories indicate that the region is experiencing unprecedented expansion, with adoption rates reaching 45% annually in key metropolitan areas.

Manufacturing excellence has positioned Asia-Pacific as the global hub for EV battery pack production, with the region accounting for approximately 75% of global battery manufacturing capacity. This dominance is supported by established supply chains, advanced manufacturing technologies, and significant economies of scale that enable competitive pricing and rapid innovation cycles.

The Asia-Pacific EV battery pack market refers to the comprehensive ecosystem encompassing the design, manufacturing, distribution, and integration of battery systems specifically engineered for electric vehicles across the Asia-Pacific region. This market includes various stakeholders from raw material suppliers to end-vehicle manufacturers, creating a complex value chain that supports the electric mobility transformation.

Battery pack systems in this context represent complete energy storage solutions that combine individual battery cells, thermal management systems, battery management systems, and protective housing designed to power electric vehicles efficiently and safely. The market encompasses passenger vehicles, commercial vehicles, two-wheelers, and emerging mobility solutions such as electric buses and delivery vehicles.

Technological scope includes various battery chemistries, energy densities, charging capabilities, and integration technologies that enable seamless vehicle operation. The market also encompasses aftermarket services, recycling solutions, and second-life applications that extend the value proposition of battery investments throughout their lifecycle.

Strategic positioning of the Asia-Pacific EV battery pack market demonstrates exceptional growth momentum driven by supportive regulatory frameworks, technological innovation, and increasing consumer adoption of electric vehicles. The region has established itself as the global leader in battery manufacturing, with comprehensive capabilities spanning from raw material processing to advanced battery management systems.

Market leadership is characterized by the presence of major battery manufacturers who have invested heavily in production capacity expansion and technology development. These companies are driving innovation in energy density improvements, charging speed enhancements, and cost reduction initiatives that make electric vehicles more accessible to mainstream consumers.

Growth drivers include government incentives representing up to 30% of vehicle purchase price in some markets, declining battery costs, and improving charging infrastructure. The market is experiencing rapid technological evolution with next-generation battery technologies promising significant improvements in performance, safety, and sustainability.

Competitive dynamics reveal intense competition among established players and emerging companies, fostering continuous innovation and driving down costs. This competitive environment is accelerating the development of advanced battery technologies and manufacturing processes that enhance overall market growth and consumer value proposition.

Market intelligence reveals several critical insights that shape the Asia-Pacific EV battery pack landscape:

Government policies serve as the primary catalyst for market expansion, with countries across the Asia-Pacific region implementing comprehensive electric vehicle promotion strategies. These policies include purchase subsidies, tax incentives, and regulatory mandates that create favorable conditions for electric vehicle adoption and battery demand growth.

Environmental concerns are driving consumer preference shifts toward cleaner transportation alternatives, particularly in highly polluted urban areas where air quality improvements are critical. This environmental consciousness is supported by increasing awareness of climate change impacts and the role of transportation in carbon emissions reduction.

Technological advancements in battery chemistry and manufacturing processes are continuously improving performance characteristics while reducing costs. These improvements include higher energy densities, faster charging capabilities, longer lifespans, and enhanced safety features that address previous consumer concerns about electric vehicle adoption.

Infrastructure development is accelerating across the region, with charging networks expanding rapidly to support growing electric vehicle populations. This infrastructure expansion reduces range anxiety and makes electric vehicles more practical for daily use, thereby increasing consumer confidence and adoption rates.

Economic factors including declining battery costs and improving total cost of ownership calculations are making electric vehicles increasingly competitive with traditional internal combustion engine vehicles, particularly when considering fuel savings and maintenance cost reductions over the vehicle lifecycle.

High initial costs continue to present barriers for mainstream consumer adoption, despite declining battery prices and government incentives. The upfront investment required for electric vehicles remains significantly higher than comparable conventional vehicles, limiting market penetration in price-sensitive segments.

Raw material dependencies create supply chain vulnerabilities, particularly for critical materials such as lithium, cobalt, and rare earth elements. Price volatility and supply constraints for these materials can impact battery production costs and availability, affecting overall market stability.

Charging infrastructure limitations in rural and remote areas restrict electric vehicle adoption outside major metropolitan centers. The uneven distribution of charging facilities creates practical challenges for consumers who require reliable access to charging options for daily transportation needs.

Technical challenges related to battery performance in extreme weather conditions, particularly in regions with very hot or cold climates, can affect vehicle reliability and consumer confidence. These performance variations require ongoing technological development and may limit adoption in certain geographic areas.

Recycling and disposal concerns present long-term sustainability challenges as the volume of end-of-life batteries increases. The lack of comprehensive recycling infrastructure and processes for battery materials creates environmental and economic concerns that require systematic solutions.

Emerging markets within the Asia-Pacific region present substantial growth opportunities as economic development increases disposable income and environmental awareness. Countries with developing automotive markets are positioned to leapfrog traditional vehicle technologies and adopt electric mobility solutions directly.

Commercial vehicle electrification represents a significant opportunity as businesses seek to reduce operational costs and meet sustainability targets. Fleet operators are increasingly recognizing the total cost of ownership advantages of electric vehicles, particularly for urban delivery and transportation applications.

Energy storage applications beyond transportation are creating new market segments for battery technologies. Grid-scale energy storage, residential energy systems, and industrial applications provide additional revenue streams and market diversification opportunities for battery manufacturers.

Technology partnerships between battery manufacturers, automotive companies, and technology firms are enabling innovative solutions and market expansion. These collaborations facilitate knowledge sharing, risk distribution, and accelerated development of next-generation battery technologies.

Second-life applications for used EV batteries are creating circular economy opportunities that extend battery value and improve overall economics. These applications include stationary energy storage, backup power systems, and grid stabilization services that provide additional revenue streams.

Competitive intensity in the Asia-Pacific EV battery pack market is driving rapid innovation and cost reduction initiatives. Major manufacturers are investing heavily in research and development to maintain technological leadership while simultaneously expanding production capacity to meet growing demand.

Supply chain evolution is characterized by increasing vertical integration and regional localization strategies. Companies are developing comprehensive supply chains that reduce dependencies on external suppliers while improving quality control and cost management throughout the production process.

Technology convergence is occurring as battery manufacturers collaborate with automotive companies, technology firms, and research institutions to develop integrated solutions. This convergence is accelerating innovation cycles and enabling more sophisticated battery management and integration technologies.

Market consolidation trends are emerging as smaller players struggle to compete with the scale and resources of major manufacturers. This consolidation is leading to increased market concentration while driving efficiency improvements and technological advancement across the industry.

Regulatory evolution continues to shape market dynamics as governments refine policies to support electric vehicle adoption while addressing safety, environmental, and economic considerations. These regulatory changes create both opportunities and challenges for market participants.

Comprehensive analysis of the Asia-Pacific EV battery pack market employs multiple research methodologies to ensure accurate and reliable insights. Primary research includes extensive interviews with industry executives, technology experts, and market participants across the value chain to gather firsthand perspectives on market trends and developments.

Secondary research encompasses detailed analysis of industry reports, government publications, company financial statements, and technical literature to establish market context and validate primary research findings. This approach ensures comprehensive coverage of market dynamics and competitive landscape factors.

Data triangulation methods are employed to cross-verify information from multiple sources and ensure accuracy of market insights and projections. This rigorous approach includes validation of quantitative data through multiple independent sources and expert consultation.

Market modeling techniques incorporate various analytical frameworks to project future market trends and growth patterns. These models consider multiple variables including technological advancement rates, policy impacts, economic factors, and consumer adoption patterns to provide robust market forecasts.

Expert validation processes involve consultation with industry specialists and academic researchers to ensure research findings accurately reflect market realities and future prospects. This validation step enhances the credibility and reliability of research conclusions and recommendations.

China dominates the Asia-Pacific EV battery pack market with approximately 60% regional market share, driven by massive government support, extensive manufacturing capabilities, and the world’s largest electric vehicle market. Chinese manufacturers have established comprehensive supply chains and achieved significant economies of scale that enable competitive pricing and rapid innovation.

Japan maintains technological leadership in advanced battery chemistries and manufacturing processes, contributing approximately 20% of regional production capacity. Japanese companies focus on high-quality, premium battery solutions and are pioneering next-generation technologies including solid-state batteries and advanced thermal management systems.

South Korea represents a major manufacturing hub with approximately 15% of regional capacity, specializing in high-energy-density batteries for premium electric vehicles. Korean manufacturers are known for technological innovation and quality excellence, serving both domestic and international automotive markets.

India is emerging as a significant growth market with rapidly expanding local manufacturing capabilities and increasing electric vehicle adoption. The Indian market is characterized by strong government support for domestic manufacturing and growing consumer acceptance of electric mobility solutions, particularly in urban areas.

Southeast Asian markets including Thailand, Indonesia, and Vietnam are developing as important manufacturing and consumption centers, supported by favorable government policies and increasing foreign investment in electric vehicle and battery production facilities.

Market leadership in the Asia-Pacific EV battery pack sector is characterized by intense competition among established manufacturers and emerging players. The competitive landscape includes:

Competitive strategies include capacity expansion, technology development, vertical integration, and strategic partnerships with automotive manufacturers. Companies are investing heavily in research and development to maintain technological leadership while scaling production to meet growing demand.

By Battery Type:

By Vehicle Type:

By Application:

Passenger vehicle batteries represent the largest market segment, driven by increasing consumer adoption and expanding model availability. This category is characterized by continuous improvements in energy density, charging speed, and cost reduction that make electric vehicles more attractive to mainstream consumers.

Commercial vehicle applications are experiencing rapid growth as businesses recognize the operational cost advantages of electric vehicles. Fleet operators are particularly interested in total cost of ownership benefits, including reduced fuel costs, lower maintenance requirements, and potential regulatory advantages in urban areas.

Two-wheeler batteries constitute a significant market segment in Asia-Pacific, where electric scooters and motorcycles are gaining popularity for urban transportation. This segment is characterized by cost-sensitive consumers who prioritize affordability and practical performance over premium features.

Energy storage applications are creating new opportunities for battery manufacturers as grid-scale storage, residential systems, and industrial applications expand. These applications often utilize different performance characteristics than automotive applications, creating opportunities for specialized battery solutions.

Premium vehicle segments demand high-performance batteries with advanced features such as fast charging, extended range, and sophisticated thermal management. These applications drive technological innovation and often serve as testing grounds for next-generation battery technologies.

Battery manufacturers benefit from expanding market opportunities, technological advancement requirements, and increasing demand across multiple application segments. The growing market provides opportunities for capacity expansion, technology development, and strategic partnerships that enhance competitive positioning.

Automotive companies gain access to advanced battery technologies that enable competitive electric vehicle offerings. Partnerships with battery manufacturers provide technological expertise, supply chain security, and cost optimization opportunities that support electric vehicle market expansion.

Consumers benefit from improving battery performance, declining costs, and expanding vehicle options that make electric mobility more practical and affordable. Enhanced charging infrastructure and government incentives further improve the value proposition of electric vehicle ownership.

Government stakeholders achieve environmental and economic policy objectives through electric vehicle adoption, including reduced emissions, energy security improvements, and industrial development opportunities. The growing battery industry supports job creation and technological leadership in the clean energy transition.

Investors find opportunities in a rapidly growing market with strong government support and clear long-term growth trends. The battery industry offers exposure to multiple growth drivers including electric vehicles, energy storage, and sustainable technology development.

Strengths:

Weaknesses:

Opportunities:

Threats:

Solid-state battery development is emerging as a transformative trend that promises significant improvements in energy density, safety, and charging speed. Major manufacturers are investing heavily in this technology, with commercial applications expected to begin within the next few years.

Vertical integration strategies are becoming increasingly common as battery manufacturers seek to control supply chains and reduce costs. This trend includes investments in raw material processing, cell manufacturing, and recycling capabilities to create comprehensive value chains.

Fast charging technology advancement is addressing one of the primary consumer concerns about electric vehicle adoption. New battery chemistries and charging protocols are enabling charging times comparable to conventional fuel filling, improving the practical appeal of electric vehicles.

Sustainability initiatives are gaining prominence as companies focus on environmental responsibility throughout the battery lifecycle. This includes sustainable sourcing of raw materials, clean manufacturing processes, and comprehensive recycling programs that support circular economy principles.

Artificial intelligence integration in battery management systems is enabling more sophisticated performance optimization, predictive maintenance, and safety monitoring. These smart battery systems can adapt to usage patterns and environmental conditions to maximize performance and longevity.

Capacity expansion announcements from major manufacturers indicate continued confidence in market growth prospects. Recent investments include multi-billion-dollar facility expansions across China, Japan, and South Korea that will significantly increase regional production capacity.

Technology partnerships between battery manufacturers and automotive companies are accelerating innovation and market development. These collaborations focus on developing customized battery solutions that meet specific vehicle requirements while optimizing performance and cost characteristics.

Government policy updates across the region continue to strengthen support for electric vehicle adoption and domestic battery manufacturing. Recent policy developments include extended incentive programs, infrastructure investment commitments, and regulatory frameworks that support industry growth.

Research breakthroughs in battery chemistry and manufacturing processes are promising significant performance improvements and cost reductions. According to MarkWide Research analysis, these developments could accelerate market adoption and expand application opportunities across multiple sectors.

Supply chain investments in critical material processing and recycling capabilities are addressing long-term sustainability and security concerns. These investments include lithium processing facilities, cobalt recycling plants, and comprehensive material recovery systems.

Investment priorities should focus on next-generation battery technologies that offer significant performance improvements and cost advantages. Companies that successfully develop and commercialize advanced battery chemistries will likely capture substantial market share and premium pricing opportunities.

Supply chain diversification strategies are essential for managing raw material risks and ensuring production continuity. Companies should develop multiple sourcing options and consider vertical integration opportunities that reduce dependence on external suppliers.

Market expansion into emerging applications beyond automotive transportation presents significant growth opportunities. Energy storage, industrial applications, and consumer electronics represent substantial markets that can leverage automotive battery technology developments.

Sustainability integration throughout business operations will become increasingly important for long-term competitiveness. Companies should invest in clean manufacturing processes, sustainable sourcing practices, and comprehensive recycling capabilities that support circular economy principles.

Strategic partnerships with automotive manufacturers, technology companies, and research institutions can accelerate innovation and market development. These collaborations provide access to complementary capabilities and shared risk in developing next-generation solutions.

Market trajectory for the Asia-Pacific EV battery pack market indicates continued robust growth driven by accelerating electric vehicle adoption, technological advancement, and supportive government policies. MWR projections suggest that the market will experience sustained expansion with growth rates exceeding 25% annually over the next five years.

Technology evolution will continue to drive market development with solid-state batteries, advanced thermal management systems, and artificial intelligence integration becoming mainstream. These technological improvements will address current limitations and expand market opportunities across multiple application segments.

Geographic expansion within the Asia-Pacific region will see emerging markets such as India, Indonesia, and Vietnam becoming increasingly important. These markets offer substantial growth potential as economic development increases disposable income and environmental awareness drives electric vehicle adoption.

Industry consolidation trends are expected to continue as smaller players struggle to compete with the scale and resources required for success in this capital-intensive industry. This consolidation will likely result in a more concentrated market structure with stronger competitive positions for leading manufacturers.

Circular economy development will become increasingly important as the volume of end-of-life batteries grows. Comprehensive recycling infrastructure and second-life applications will create additional value streams while addressing environmental sustainability concerns that support long-term market growth.

The Asia-Pacific EV battery pack market represents one of the most dynamic and promising sectors within the global clean energy transition. With strong government support, technological leadership, and rapidly expanding manufacturing capabilities, the region is well-positioned to maintain its dominance in global battery production while serving growing domestic and international demand.

Market fundamentals remain exceptionally strong, supported by accelerating electric vehicle adoption, continuous technological advancement, and comprehensive policy frameworks that encourage sustainable transportation solutions. The combination of established manufacturing excellence and ongoing innovation creates a compelling investment and growth opportunity for industry participants.

Future success in this market will depend on companies’ ability to navigate technological transitions, manage supply chain complexities, and capitalize on emerging application opportunities. Organizations that successfully balance innovation, scale, and sustainability will be best positioned to capture the substantial growth opportunities that lie ahead in the Asia-Pacific EV battery pack market.

What is EV Battery Pack?

EV Battery Pack refers to a collection of battery cells that are assembled together to store energy for electric vehicles. These packs are crucial for the performance, range, and efficiency of electric vehicles, powering everything from small cars to large buses.

What are the key players in the Asia-Pacific EV Battery Pack Market?

Key players in the Asia-Pacific EV Battery Pack Market include companies like Panasonic, LG Chem, and CATL, which are known for their advanced battery technologies and significant market presence, among others.

What are the growth factors driving the Asia-Pacific EV Battery Pack Market?

The Asia-Pacific EV Battery Pack Market is driven by increasing demand for electric vehicles, advancements in battery technology, and government initiatives promoting sustainable transportation. Additionally, rising environmental concerns are pushing consumers towards electric mobility.

What challenges does the Asia-Pacific EV Battery Pack Market face?

Challenges in the Asia-Pacific EV Battery Pack Market include high production costs, supply chain disruptions, and the need for improved recycling methods for battery materials. These factors can hinder market growth and sustainability efforts.

What opportunities exist in the Asia-Pacific EV Battery Pack Market?

The Asia-Pacific EV Battery Pack Market presents opportunities in the development of solid-state batteries and enhanced energy density technologies. Additionally, increasing investments in charging infrastructure and renewable energy integration are expected to boost market growth.

What trends are shaping the Asia-Pacific EV Battery Pack Market?

Trends in the Asia-Pacific EV Battery Pack Market include the shift towards lighter and more efficient battery designs, the rise of battery-as-a-service models, and the integration of smart technologies for better energy management. These trends are influencing both consumer preferences and manufacturer strategies.

Asia-Pacific EV Battery Pack Market

| Segmentation Details | Description |

|---|---|

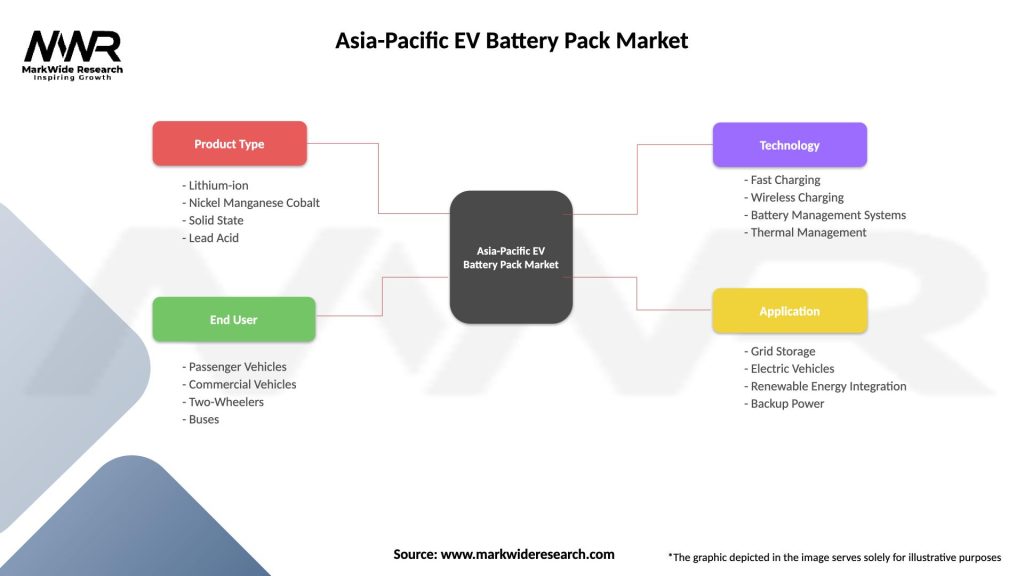

| Product Type | Lithium-ion, Nickel Manganese Cobalt, Solid State, Lead Acid |

| End User | Passenger Vehicles, Commercial Vehicles, Two-Wheelers, Buses |

| Technology | Fast Charging, Wireless Charging, Battery Management Systems, Thermal Management |

| Application | Grid Storage, Electric Vehicles, Renewable Energy Integration, Backup Power |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Asia-Pacific EV Battery Pack Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.