444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The ASEAN cloud computing market represents one of the most dynamic and rapidly evolving technology sectors in Southeast Asia, encompassing ten member nations with diverse economic landscapes and digital transformation priorities. Cloud adoption across the region has accelerated significantly, driven by increasing digitalization initiatives, government support for technology infrastructure, and growing demand for scalable computing solutions. The market demonstrates remarkable growth potential with a projected compound annual growth rate (CAGR) of 15.2% through the forecast period, reflecting the region’s commitment to digital innovation and technological advancement.

Digital transformation initiatives across ASEAN countries have created substantial opportunities for cloud service providers, with organizations increasingly migrating from traditional on-premises infrastructure to flexible cloud-based solutions. The region’s unique characteristics, including varying levels of digital maturity, regulatory frameworks, and infrastructure development, present both challenges and opportunities for market participants. Enterprise adoption rates have shown consistent improvement, with approximately 68% of businesses across major ASEAN markets implementing some form of cloud technology.

Market dynamics indicate strong momentum across multiple sectors, including financial services, healthcare, education, and government agencies. The increasing focus on data sovereignty, cybersecurity, and compliance requirements has shaped market development patterns, with local and international providers adapting their offerings to meet specific regional needs. Infrastructure investments by major cloud providers have established robust foundations for continued market expansion throughout the ASEAN region.

The ASEAN cloud computing market refers to the comprehensive ecosystem of cloud-based services, infrastructure, and solutions deployed across the ten member nations of the Association of Southeast Asian Nations, including Singapore, Malaysia, Thailand, Indonesia, Philippines, Vietnam, Myanmar, Cambodia, Laos, and Brunei. This market encompasses various service models including Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS), delivered through public, private, and hybrid cloud deployment models.

Cloud computing in the ASEAN context represents the delivery of computing services over the internet, enabling organizations to access scalable resources, applications, and storage solutions without maintaining physical infrastructure. The market includes both international cloud providers establishing regional presence and local providers developing indigenous solutions tailored to specific market requirements. Service delivery models vary significantly across countries, reflecting different levels of technological infrastructure, regulatory environments, and market maturity.

Regional characteristics of the ASEAN cloud market include diverse languages, currencies, regulatory frameworks, and business practices that influence service design and delivery approaches. The market represents a convergence of traditional IT services with modern cloud technologies, creating opportunities for innovation and digital transformation across multiple industry sectors.

Market leadership in the ASEAN cloud computing sector is characterized by intense competition between global technology giants and emerging regional players, each seeking to capture market share in this rapidly expanding digital economy. The region’s cloud adoption trajectory demonstrates accelerating momentum, with government digitalization initiatives contributing approximately 35% of total market growth through public sector modernization programs and smart city developments.

Technology trends shaping the market include artificial intelligence integration, edge computing deployment, and multi-cloud strategies that enable organizations to optimize performance and costs. The increasing emphasis on data localization and sovereignty has created opportunities for regional providers while challenging international players to establish local infrastructure and comply with varying regulatory requirements across different ASEAN markets.

Investment patterns reveal significant capital allocation toward infrastructure development, with major cloud providers establishing data centers and edge computing facilities throughout the region. The market demonstrates strong fundamentals supported by favorable demographics, increasing internet penetration, and growing smartphone adoption rates that facilitate cloud service consumption across diverse user segments.

Future prospects indicate sustained growth driven by digital transformation imperatives, emerging technologies adoption, and increasing recognition of cloud computing’s role in enabling business agility and innovation. The market’s evolution reflects broader economic development patterns across ASEAN nations, with cloud adoption serving as both a catalyst and enabler of digital economic growth.

Strategic insights from comprehensive market analysis reveal several critical factors driving ASEAN cloud computing market development:

Market maturity varies significantly across ASEAN countries, with Singapore and Malaysia leading adoption rates while emerging markets like Cambodia and Laos present substantial growth potential. This diversity creates opportunities for tailored service offerings and phased market entry strategies that align with local market conditions and customer requirements.

Digital transformation imperatives across ASEAN organizations serve as the primary catalyst for cloud computing adoption, with businesses recognizing the need for agile, scalable technology infrastructure to remain competitive in rapidly evolving markets. The acceleration of remote work practices and digital business models has intensified demand for cloud-based collaboration tools, data storage solutions, and application hosting services.

Government initiatives promoting digital economy development create substantial market opportunities through public sector modernization programs, smart city projects, and e-government service implementations. National digitalization strategies across ASEAN countries increasingly emphasize cloud computing as a foundational technology for achieving digital transformation objectives and improving public service delivery efficiency.

Cost optimization requirements drive organizations toward cloud solutions that eliminate capital expenditure for hardware infrastructure while providing predictable operational expense models. The ability to scale resources dynamically based on demand patterns enables businesses to optimize technology costs while maintaining operational flexibility and performance standards.

Innovation acceleration through cloud-based development platforms and services enables organizations to rapidly deploy new applications, experiment with emerging technologies, and bring products to market faster. The availability of artificial intelligence, machine learning, and analytics services through cloud platforms democratizes access to advanced technologies previously available only to large enterprises.

Regulatory compliance requirements increasingly favor cloud solutions that provide robust security, data protection, and audit capabilities. Cloud providers’ investments in compliance certifications and security infrastructure help organizations meet regulatory requirements while reducing internal compliance management overhead.

Data sovereignty concerns represent significant challenges for cloud adoption across ASEAN markets, with varying national regulations regarding data storage, processing, and cross-border transfer creating complexity for both providers and customers. Organizations must navigate diverse regulatory landscapes while ensuring compliance with local data protection requirements and industry-specific regulations.

Infrastructure limitations in certain ASEAN countries constrain cloud service delivery and adoption, particularly in rural areas where internet connectivity remains unreliable or insufficient for cloud-based applications. The digital divide between urban and rural regions creates uneven market development patterns and limits the addressable market for cloud services.

Skills shortage challenges affect both cloud service providers and customer organizations, with limited availability of qualified professionals capable of designing, implementing, and managing cloud solutions. The rapid pace of technology evolution requires continuous skills development and training investments that strain organizational resources and budgets.

Security concerns regarding data protection, privacy, and cyber threats continue to influence cloud adoption decisions, particularly among organizations handling sensitive information or operating in highly regulated industries. Despite improvements in cloud security capabilities, perceived risks and compliance uncertainties create adoption barriers for risk-averse organizations.

Integration complexity with existing legacy systems presents technical and financial challenges for organizations considering cloud migration. The costs and risks associated with system integration, data migration, and business process changes can delay or prevent cloud adoption initiatives, particularly for organizations with substantial investments in existing infrastructure.

Emerging market penetration presents substantial growth opportunities as developing ASEAN countries accelerate digital transformation initiatives and improve technology infrastructure. Countries like Vietnam, Indonesia, and the Philippines demonstrate significant potential for cloud adoption as their economies modernize and businesses embrace digital technologies.

Industry verticalization creates opportunities for specialized cloud solutions tailored to specific sector requirements, including healthcare, education, financial services, and manufacturing. The development of industry-specific compliance capabilities, applications, and services enables providers to capture higher value segments and establish competitive differentiation.

Edge computing deployment opportunities arise from increasing demand for low-latency applications, Internet of Things (IoT) implementations, and real-time data processing capabilities. The convergence of cloud and edge computing creates new service categories and revenue streams for providers willing to invest in distributed infrastructure.

Artificial intelligence and machine learning service integration offers opportunities to enhance cloud platforms with advanced analytics, automation, and intelligent capabilities. Organizations seeking to leverage AI technologies without substantial internal investments represent a growing market for cloud-based AI services and platforms.

Hybrid cloud solutions address organizations’ needs for flexibility, control, and gradual migration strategies, creating opportunities for providers offering seamless integration between on-premises and cloud infrastructure. The ability to support diverse deployment models enables providers to serve customers with varying requirements and risk tolerance levels.

Competitive dynamics in the ASEAN cloud computing market reflect intense rivalry between global technology leaders and regional specialists, each pursuing different strategies to capture market share and establish sustainable competitive advantages. The market demonstrates characteristics of both consolidation and fragmentation, with large providers acquiring smaller specialists while new entrants continue to emerge with innovative solutions.

Technology evolution drives continuous market transformation as cloud providers enhance their service portfolios with emerging technologies, improved performance capabilities, and expanded geographic coverage. The integration of artificial intelligence, machine learning, and automation technologies into cloud platforms creates new value propositions and competitive differentiators that influence customer selection criteria.

Customer behavior patterns show increasing sophistication in cloud service evaluation and procurement, with organizations developing multi-vendor strategies and demanding greater transparency in pricing, performance, and security capabilities. The shift toward outcome-based purchasing models and consumption-based pricing creates pressure on providers to demonstrate clear business value and return on investment.

Regulatory evolution across ASEAN countries continues to shape market development through data protection laws, cybersecurity requirements, and industry-specific compliance mandates. According to MarkWide Research analysis, regulatory harmonization efforts may reduce compliance complexity while maintaining necessary protections for data sovereignty and national security interests.

Partnership ecosystems play increasingly important roles in market development as cloud providers collaborate with system integrators, software vendors, and industry specialists to deliver comprehensive solutions. These alliances enable providers to extend their market reach, enhance service capabilities, and address specific customer requirements more effectively.

Comprehensive analysis of the ASEAN cloud computing market employs multiple research methodologies to ensure accuracy, reliability, and depth of insights. Primary research activities include structured interviews with industry executives, technology leaders, and key decision-makers across major ASEAN markets to gather firsthand perspectives on market trends, challenges, and opportunities.

Secondary research incorporates analysis of industry reports, government publications, regulatory documents, and company financial statements to establish market context and validate primary research findings. The methodology includes examination of technology adoption patterns, investment flows, and competitive positioning across different market segments and geographic regions.

Quantitative analysis utilizes statistical modeling and trend analysis to project market growth rates, segment performance, and regional development patterns. The research methodology incorporates economic indicators, technology adoption curves, and demographic factors that influence cloud computing demand across ASEAN countries.

Market validation processes include cross-referencing multiple data sources, conducting expert interviews, and applying analytical frameworks to ensure research conclusions accurately reflect market realities. The methodology addresses potential biases and limitations through triangulation of findings and sensitivity analysis of key assumptions.

Continuous monitoring of market developments, regulatory changes, and competitive activities ensures research findings remain current and relevant. The methodology includes regular updates to market models and projections based on emerging trends and new information that may impact market dynamics.

Singapore maintains its position as the regional leader in cloud adoption and infrastructure development, with approximately 78% of enterprises utilizing cloud services and serving as the preferred location for regional data centers and cloud service provider headquarters. The country’s advanced digital infrastructure, supportive regulatory environment, and strategic location make it the gateway for cloud services throughout Southeast Asia.

Malaysia demonstrates strong cloud market development with government-led digitalization initiatives and growing enterprise adoption across multiple sectors. The country’s focus on becoming a regional technology hub has attracted significant cloud infrastructure investments and created opportunities for both international and local service providers.

Thailand shows accelerating cloud adoption driven by digital transformation initiatives in both public and private sectors, with particular strength in financial services and manufacturing applications. The government’s Thailand 4.0 strategy emphasizes cloud computing as a key enabler of economic modernization and competitiveness.

Indonesia represents the largest potential market in terms of population and economic size, with cloud adoption gaining momentum despite infrastructure challenges in certain regions. The country’s large domestic market and growing digital economy create substantial opportunities for cloud service providers willing to invest in local infrastructure and partnerships.

Philippines demonstrates growing cloud adoption particularly in business process outsourcing and financial services sectors, supported by improving telecommunications infrastructure and government digitalization programs. The country’s English-speaking workforce and established IT services industry provide advantages for cloud service delivery and support operations.

Vietnam shows rapid cloud market development driven by economic growth, increasing foreign investment, and government support for digital transformation. The country’s manufacturing sector modernization and growing technology industry create demand for cloud-based solutions and services.

Market leadership in the ASEAN cloud computing sector is contested among several categories of providers, each bringing distinct advantages and strategic approaches to market development:

Competitive strategies vary significantly among market participants, with global providers emphasizing scale, comprehensive service portfolios, and advanced technology capabilities while regional providers focus on local market knowledge, regulatory compliance, and specialized industry solutions. The competitive landscape continues evolving as providers adapt their strategies to address specific ASEAN market requirements and opportunities.

Partnership strategies play crucial roles in competitive positioning as providers collaborate with local system integrators, telecommunications companies, and industry specialists to enhance market reach and service delivery capabilities. These alliances enable providers to address local market requirements while leveraging partner expertise and relationships.

Service Model Segmentation:

Deployment Model Segmentation:

Organization Size Segmentation:

Infrastructure as a Service (IaaS) represents the largest segment of the ASEAN cloud market, driven by organizations’ needs for scalable computing resources and storage capabilities. The segment benefits from increasing virtualization adoption and the desire to reduce capital expenditure on physical infrastructure. Growth drivers include disaster recovery requirements, development and testing environments, and the need for rapid resource scaling to meet fluctuating demand patterns.

Platform as a Service (PaaS) demonstrates the highest growth rate among service models, reflecting increasing developer productivity requirements and the need for rapid application development and deployment capabilities. The segment particularly benefits from digital transformation initiatives that require organizations to quickly develop and deploy new applications and services. Market adoption is accelerating as organizations recognize the value of managed development environments and integrated development tools.

Software as a Service (SaaS) shows strong adoption across all organization sizes, with particular strength in productivity applications, customer relationship management, and collaboration tools. The segment benefits from the shift toward subscription-based software consumption and the need for applications that support remote work and digital business processes. Industry-specific SaaS solutions continue gaining traction in healthcare, education, and financial services sectors.

Public cloud deployment maintains the largest market share due to cost advantages and comprehensive service availability, while hybrid cloud adoption accelerates as organizations seek to balance cost, control, and compliance requirements. The trend toward multi-cloud strategies creates opportunities for providers offering integration and management tools that simplify complex cloud environments.

Cloud Service Providers benefit from expanding market opportunities across diverse industry sectors and geographic regions within ASEAN. The growing demand for cloud services creates revenue growth potential while the region’s improving digital infrastructure reduces service delivery costs and complexity. Competitive advantages emerge from early market entry, local partnerships, and specialized service offerings that address specific regional requirements.

Enterprise Customers gain access to advanced technology capabilities without substantial capital investments, enabling digital transformation initiatives and improved operational efficiency. Cloud adoption provides organizations with scalability, flexibility, and access to emerging technologies that support innovation and competitive advantage. Cost optimization through cloud services enables organizations to redirect resources toward core business activities and strategic initiatives.

System Integrators and consulting firms benefit from increased demand for cloud migration services, integration expertise, and ongoing management support. The complexity of cloud adoption creates opportunities for specialized service providers that can guide organizations through transformation processes and optimize cloud implementations. Partnership opportunities with cloud providers create additional revenue streams and competitive differentiation.

Government Agencies benefit from improved public service delivery capabilities, cost-effective technology infrastructure, and enhanced citizen engagement through digital channels. Cloud adoption enables government modernization initiatives while providing scalability and security capabilities that support public sector requirements. Economic development benefits include job creation in technology sectors and improved business environment for digital economy growth.

Technology Vendors gain access to broader markets through cloud-based service delivery models and partnership opportunities with cloud providers. The shift toward cloud consumption creates new business models and revenue opportunities while reducing traditional software licensing complexity. Innovation acceleration through cloud platforms enables vendors to develop and deploy new solutions more rapidly and cost-effectively.

Strengths:

Weaknesses:

Opportunities:

Threats:

Artificial Intelligence Integration represents a dominant trend as cloud providers embed AI and machine learning capabilities into their service offerings, enabling organizations to leverage advanced analytics and automation without substantial internal investments. The democratization of AI through cloud platforms creates new application possibilities and competitive advantages for businesses across various sectors.

Edge Computing Deployment accelerates as organizations require low-latency processing capabilities for Internet of Things applications, real-time analytics, and content delivery optimization. The convergence of cloud and edge computing creates distributed infrastructure models that support diverse application requirements while maintaining centralized management and control capabilities.

Multi-Cloud Strategies gain adoption as organizations seek to avoid vendor lock-in, optimize costs, and leverage best-of-breed solutions from multiple providers. This trend drives demand for cloud management platforms and integration services that simplify multi-cloud operations and enable seamless workload portability across different environments.

Industry-Specific Solutions emerge as cloud providers develop specialized offerings tailored to specific sector requirements, compliance needs, and business processes. Vertical market focus enables providers to deliver higher value solutions while addressing unique challenges in healthcare, financial services, manufacturing, and government sectors.

Sustainability Focus influences cloud adoption decisions as organizations prioritize environmental responsibility and energy efficiency in their technology choices. Cloud providers’ investments in renewable energy and efficient data center operations create competitive advantages while supporting customers’ sustainability objectives.

Zero Trust Security models gain prominence as organizations implement comprehensive security frameworks that verify all users and devices regardless of location. Cloud providers enhance their security offerings to support zero trust architectures while addressing evolving cybersecurity threats and compliance requirements.

Infrastructure Expansion continues across the region as major cloud providers establish new data centers and edge computing facilities to improve service delivery and meet data sovereignty requirements. Recent announcements include substantial investments in Singapore, Indonesia, and Thailand that will enhance regional cloud computing capabilities and reduce latency for local customers.

Strategic Partnerships between international cloud providers and local telecommunications companies create opportunities for enhanced service delivery and market penetration. These collaborations leverage local market knowledge and existing customer relationships while providing cloud providers with infrastructure and regulatory compliance support.

Regulatory Developments across ASEAN countries continue shaping market dynamics through data protection laws, cybersecurity requirements, and industry-specific compliance mandates. Recent regulatory changes in several countries emphasize data localization requirements while maintaining provisions for cross-border data flows under specific conditions.

Acquisition Activity increases as cloud providers seek to enhance their capabilities through strategic acquisitions of specialized technology companies and regional service providers. These transactions enable providers to expand their service portfolios, acquire local market expertise, and accelerate market penetration in specific sectors or geographic areas.

Government Initiatives promote cloud adoption through public sector modernization programs, smart city projects, and digital government service implementations. MWR analysis indicates that government cloud adoption serves as a catalyst for broader market development by demonstrating cloud capabilities and building confidence among private sector organizations.

Market Entry Strategy recommendations emphasize the importance of local partnerships and gradual market development approaches that address specific country requirements and regulatory frameworks. Organizations considering ASEAN market entry should prioritize understanding local business practices, compliance requirements, and customer preferences before implementing standardized global strategies.

Investment Priorities should focus on infrastructure development, skills training, and partnership development to establish sustainable competitive advantages in the region. Cloud providers should consider investments in local data centers, edge computing facilities, and talent development programs that support long-term market development objectives.

Service Development recommendations include emphasis on industry-specific solutions, hybrid deployment models, and comprehensive security capabilities that address regional market requirements. Providers should develop offerings that balance global best practices with local market needs and regulatory compliance requirements.

Partnership Strategy suggestions emphasize collaboration with local system integrators, telecommunications providers, and industry specialists to enhance market reach and service delivery capabilities. Strategic alliances enable providers to leverage local expertise while focusing on core cloud technology development and innovation.

Risk Management approaches should address regulatory compliance, cybersecurity, and geopolitical considerations that may impact market operations and customer relationships. Organizations should develop comprehensive risk assessment and mitigation strategies that address both technical and business risks associated with ASEAN market participation.

Market evolution projections indicate sustained growth momentum driven by accelerating digital transformation initiatives, improving infrastructure capabilities, and increasing recognition of cloud computing’s strategic value. The market is expected to maintain a robust growth trajectory of 15.2% CAGR as organizations across all sectors embrace cloud technologies to enhance operational efficiency and competitive positioning.

Technology advancement will continue shaping market development through artificial intelligence integration, edge computing deployment, and enhanced security capabilities. The convergence of cloud computing with emerging technologies creates new service categories and value propositions that expand market opportunities and customer applications.

Regional integration efforts may harmonize regulatory frameworks and create larger addressable markets for cloud service providers, while maintaining necessary protections for data sovereignty and national security interests. The development of common standards and interoperability requirements could simplify multi-country service delivery and reduce compliance complexity.

Industry maturation will likely result in increased specialization, with providers focusing on specific market segments, industry verticals, or technology capabilities to establish competitive differentiation. The market may experience consolidation among smaller providers while new entrants continue emerging with innovative solutions and business models.

Investment patterns indicate continued capital allocation toward infrastructure development, technology innovation, and market expansion initiatives. According to MarkWide Research projections, the combination of public and private investment in cloud computing infrastructure and services will support sustained market growth and technology advancement throughout the forecast period.

The ASEAN cloud computing market represents one of the most promising technology sectors in Southeast Asia, characterized by strong growth fundamentals, supportive government policies, and increasing enterprise adoption across diverse industry sectors. The market’s evolution reflects broader digital transformation trends while addressing specific regional requirements for data sovereignty, regulatory compliance, and local market adaptation.

Market dynamics indicate sustained growth opportunities driven by infrastructure development, technology innovation, and expanding customer demand for scalable, cost-effective computing solutions. The region’s unique characteristics create both challenges and opportunities for market participants, requiring tailored strategies that balance global best practices with local market requirements and regulatory frameworks.

Future success in the ASEAN cloud computing market will depend on providers’ ability to navigate diverse regulatory environments, establish local partnerships, and develop solutions that address specific regional needs while maintaining global technology standards. The market’s continued development will play a crucial role in supporting Southeast Asia’s digital economy growth and technological advancement objectives, creating value for all stakeholders in the cloud computing ecosystem.

What is Cloud Computing?

Cloud computing refers to the delivery of computing services over the internet, including storage, processing, and software applications. It allows businesses and individuals to access and manage data remotely, enhancing flexibility and scalability.

What are the key players in the ASEAN Cloud Computing Market?

Key players in the ASEAN Cloud Computing Market include companies like Alibaba Cloud, Microsoft Azure, and Google Cloud. These companies provide a range of services such as infrastructure as a service (IaaS) and software as a service (SaaS), among others.

What are the main drivers of growth in the ASEAN Cloud Computing Market?

The main drivers of growth in the ASEAN Cloud Computing Market include the increasing demand for digital transformation, the rise of remote work, and the need for scalable IT solutions. Additionally, the growing adoption of big data analytics and IoT applications is fueling market expansion.

What challenges does the ASEAN Cloud Computing Market face?

The ASEAN Cloud Computing Market faces challenges such as data security concerns, regulatory compliance issues, and the lack of skilled professionals. These factors can hinder the adoption of cloud services among businesses in the region.

What opportunities exist in the ASEAN Cloud Computing Market?

Opportunities in the ASEAN Cloud Computing Market include the potential for growth in sectors like e-commerce, healthcare, and education. As more businesses seek to leverage cloud technologies, there is a significant opportunity for service providers to innovate and expand their offerings.

What trends are shaping the ASEAN Cloud Computing Market?

Trends shaping the ASEAN Cloud Computing Market include the rise of hybrid cloud solutions, increased focus on artificial intelligence and machine learning, and the growing importance of edge computing. These trends are influencing how businesses deploy and utilize cloud services.

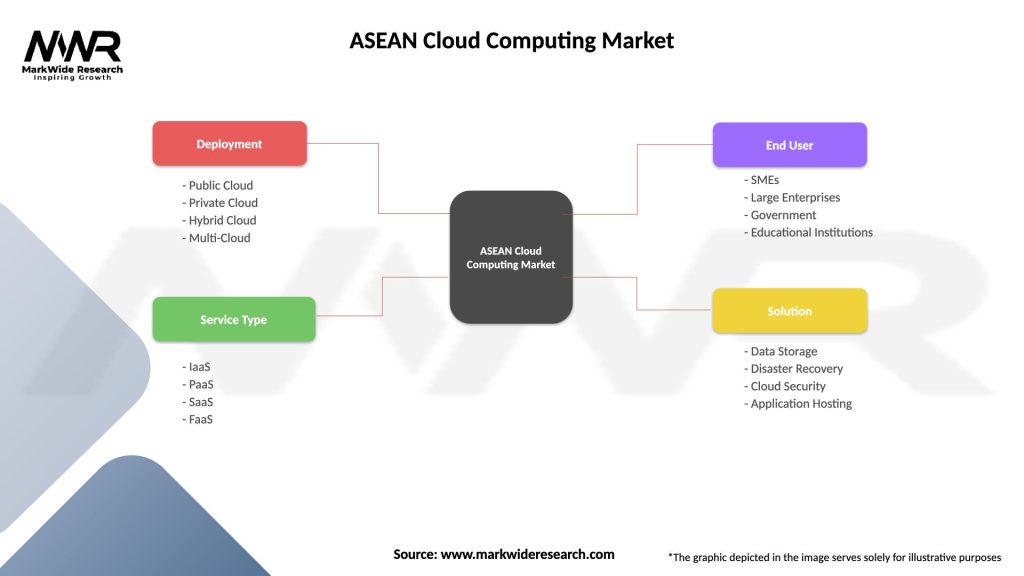

ASEAN Cloud Computing Market

| Segmentation Details | Description |

|---|---|

| Deployment | Public Cloud, Private Cloud, Hybrid Cloud, Multi-Cloud |

| Service Type | IaaS, PaaS, SaaS, FaaS |

| End User | SMEs, Large Enterprises, Government, Educational Institutions |

| Solution | Data Storage, Disaster Recovery, Cloud Security, Application Hosting |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the ASEAN Cloud Computing Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.