444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The APAC semiconductor device for industrial applications market represents one of the most dynamic and rapidly evolving sectors within the global technology landscape. This market encompasses a comprehensive range of semiconductor components specifically designed for industrial automation, manufacturing processes, power management, and control systems across the Asia-Pacific region. Industrial semiconductor devices serve as the backbone of modern manufacturing infrastructure, enabling enhanced productivity, precision control, and energy efficiency in diverse industrial environments.

Market dynamics in the APAC region are particularly compelling due to the concentration of manufacturing hubs, technological innovation centers, and rapidly expanding industrial automation initiatives. Countries such as China, Japan, South Korea, Taiwan, and India are driving substantial demand for advanced semiconductor solutions that support Industry 4.0 transformation. The market is experiencing robust growth with a projected CAGR of 8.2% through the forecast period, reflecting the increasing adoption of smart manufacturing technologies and industrial IoT implementations.

Regional manufacturing capabilities in APAC have positioned this market as a global leader in semiconductor production and consumption. The convergence of established semiconductor manufacturing infrastructure, growing industrial automation needs, and supportive government policies creates a favorable environment for sustained market expansion. Industrial applications ranging from automotive manufacturing to renewable energy systems are increasingly dependent on sophisticated semiconductor devices that deliver enhanced performance, reliability, and cost-effectiveness.

The APAC semiconductor device for industrial applications market refers to the comprehensive ecosystem of semiconductor components, integrated circuits, and electronic devices specifically engineered for industrial use cases across the Asia-Pacific region. These devices include power semiconductors, microcontrollers, sensors, analog integrated circuits, and specialized chips designed to operate in demanding industrial environments while delivering precise control, monitoring, and automation capabilities.

Industrial semiconductor devices encompass a broad spectrum of technologies including power management ICs, motor control semiconductors, industrial communication chips, and safety-critical components. These devices are characterized by their ability to withstand harsh operating conditions, provide long-term reliability, and support complex industrial processes. The market includes both discrete semiconductor components and integrated solutions that enable advanced manufacturing automation, process control, and industrial digitalization initiatives.

Key characteristics of industrial semiconductor devices include enhanced temperature tolerance, electromagnetic interference resistance, extended operational lifespans, and compliance with stringent industrial safety standards. These devices serve as fundamental building blocks for industrial equipment, robotics systems, power conversion units, and smart factory implementations throughout the APAC region.

Strategic market positioning of the APAC semiconductor device for industrial applications market reflects the region’s dominant role in global manufacturing and technology innovation. The market demonstrates exceptional growth potential driven by accelerating industrial automation adoption, expanding renewable energy infrastructure, and increasing demand for energy-efficient manufacturing processes. Key market drivers include the rapid deployment of Industry 4.0 technologies, growing emphasis on sustainable manufacturing practices, and the need for enhanced operational efficiency across diverse industrial sectors.

Market segmentation reveals significant opportunities across multiple application areas including factory automation, power management, industrial communication, and safety systems. The automotive sector represents approximately 28% of market demand, followed by industrial machinery and equipment applications. Technology advancement in areas such as wide bandgap semiconductors, artificial intelligence integration, and edge computing capabilities is reshaping the competitive landscape and creating new market opportunities.

Regional distribution shows China maintaining the largest market share at approximately 42% of total APAC demand, with Japan, South Korea, and India contributing significantly to market growth. The market is characterized by intense competition among global semiconductor manufacturers, regional technology companies, and specialized industrial solution providers. Investment trends indicate substantial capital allocation toward research and development, manufacturing capacity expansion, and strategic partnerships to capture emerging market opportunities.

Technological evolution within the APAC semiconductor device for industrial applications market is driving unprecedented innovation in manufacturing processes and industrial automation systems. The following key insights highlight the most significant market developments:

Industrial automation acceleration serves as the primary catalyst for semiconductor device demand across APAC manufacturing sectors. The transition toward smart factories and autonomous production systems requires sophisticated semiconductor solutions that enable precise control, real-time monitoring, and adaptive manufacturing processes. Government initiatives supporting Industry 4.0 adoption, particularly in China’s “Made in China 2025” strategy and Japan’s Society 5.0 vision, are creating substantial market opportunities for industrial semiconductor suppliers.

Energy efficiency mandates and sustainability requirements are driving significant demand for advanced power management semiconductors. Industrial facilities across the APAC region are implementing energy-efficient technologies to reduce operational costs and meet environmental compliance standards. Power semiconductor devices that enable variable frequency drives, smart motor control, and renewable energy integration are experiencing particularly strong demand growth.

Digital transformation initiatives in traditional manufacturing industries are creating new requirements for communication semiconductors, sensor interfaces, and data processing capabilities. The integration of IoT technologies, cloud connectivity, and artificial intelligence in industrial applications requires specialized semiconductor devices that can handle complex data processing while maintaining industrial-grade reliability. Supply chain optimization efforts and the need for enhanced operational visibility are further accelerating semiconductor adoption in industrial tracking and monitoring systems.

Supply chain vulnerabilities represent a significant challenge for the APAC semiconductor device market, particularly following recent global disruptions that highlighted the fragility of semiconductor supply networks. Component shortages and extended lead times have created uncertainty for industrial equipment manufacturers and delayed critical automation projects across the region. The concentration of semiconductor manufacturing in specific geographic areas increases supply risk and creates potential bottlenecks during periods of high demand.

High development costs associated with industrial-grade semiconductor devices pose barriers for smaller manufacturers and emerging technology companies. The stringent qualification requirements, extensive testing protocols, and long certification processes for industrial applications require substantial investment in research and development. Technical complexity in designing semiconductor devices that meet diverse industrial standards while maintaining cost competitiveness creates challenges for market participants.

Skilled workforce shortages in semiconductor design, manufacturing, and application engineering limit the industry’s ability to scale production and develop innovative solutions rapidly. The specialized knowledge required for industrial semiconductor applications, combined with intense competition for technical talent, creates recruitment and retention challenges. Regulatory compliance requirements across different APAC countries add complexity and cost to market entry strategies, particularly for international semiconductor manufacturers seeking regional expansion.

Emerging application areas present substantial growth opportunities for semiconductor device manufacturers targeting industrial markets across APAC. The rapid expansion of electric vehicle manufacturing, renewable energy infrastructure, and smart grid implementations creates demand for specialized power semiconductors and control devices. Green technology initiatives supported by government policies and corporate sustainability commitments are driving investment in energy-efficient industrial semiconductor solutions.

Edge computing proliferation in industrial environments offers significant opportunities for semiconductor companies developing processing and memory solutions optimized for distributed intelligence applications. The need for real-time data processing, reduced latency, and enhanced security in industrial IoT deployments requires innovative semiconductor architectures. Artificial intelligence integration in manufacturing processes creates demand for AI-optimized semiconductor devices that can handle machine learning workloads while meeting industrial reliability standards.

Regional manufacturing expansion initiatives, including supply chain diversification efforts and government incentives for domestic semiconductor production, create opportunities for capacity building and technology transfer. The development of semiconductor manufacturing ecosystems in countries such as India, Vietnam, and Thailand presents opportunities for both established players and new market entrants. Strategic partnerships between semiconductor manufacturers and industrial equipment companies enable collaborative innovation and accelerated market penetration.

Competitive intensity within the APAC semiconductor device for industrial applications market continues to escalate as global technology leaders and regional specialists compete for market share. The market dynamics are characterized by rapid technological advancement, aggressive pricing strategies, and continuous innovation in product development. Market consolidation through mergers and acquisitions is reshaping the competitive landscape, with larger companies acquiring specialized industrial semiconductor capabilities to strengthen their market position.

Customer requirements are evolving toward more integrated solutions that combine multiple semiconductor functions in single packages or modules. Industrial customers increasingly demand comprehensive support services, including design assistance, technical documentation, and long-term product availability guarantees. Customization demands for application-specific semiconductor solutions are growing, requiring manufacturers to develop flexible design and manufacturing capabilities.

Technology convergence between different semiconductor categories is creating new market dynamics, with traditional boundaries between power devices, control semiconductors, and communication chips becoming increasingly blurred. The integration of multiple functions in single semiconductor devices offers cost and space advantages but requires sophisticated design capabilities. Time-to-market pressures are intensifying as industrial customers seek to accelerate their digital transformation initiatives and maintain competitive advantages in rapidly evolving markets.

Comprehensive market analysis for the APAC semiconductor device for industrial applications market employs a multi-faceted research approach combining primary and secondary data sources. Primary research includes extensive interviews with industry executives, technology specialists, and key decision-makers across semiconductor manufacturers, industrial equipment companies, and end-user organizations throughout the APAC region.

Secondary research encompasses analysis of industry reports, company financial statements, patent filings, and regulatory documents to establish market trends and competitive positioning. MarkWide Research utilizes proprietary databases and analytical frameworks to validate market data and ensure accuracy of growth projections and market sizing estimates. The research methodology incorporates both quantitative analysis of market metrics and qualitative assessment of industry dynamics.

Data validation processes include cross-referencing multiple sources, conducting expert interviews for verification, and applying statistical analysis techniques to ensure reliability of market insights. The research approach considers regional variations in market development, regulatory environments, and competitive dynamics across different APAC countries. Continuous monitoring of market developments through industry networks and technology partnerships ensures ongoing accuracy of market intelligence and trend identification.

China dominates the APAC semiconductor device for industrial applications market with approximately 42% market share, driven by massive manufacturing capacity, government support for industrial automation, and substantial investment in smart factory initiatives. The country’s comprehensive industrial ecosystem, from automotive manufacturing to renewable energy production, creates diverse demand for industrial semiconductor devices. Chinese manufacturers are increasingly developing domestic semiconductor capabilities to reduce dependence on international suppliers.

Japan maintains a strong market position with approximately 22% regional market share, leveraging its advanced manufacturing technologies and expertise in precision industrial equipment. Japanese companies excel in developing high-reliability semiconductor devices for automotive, robotics, and industrial automation applications. Innovation leadership in areas such as power semiconductors and sensor technologies positions Japan as a key technology contributor to the regional market.

South Korea represents approximately 18% of the APAC market, with strong capabilities in memory semiconductors, display technologies, and industrial communication devices. The country’s focus on advanced manufacturing and technology innovation drives demand for sophisticated semiconductor solutions. India’s emerging market shows rapid growth potential with increasing industrial automation adoption and government initiatives supporting domestic manufacturing expansion. Southeast Asian countries including Taiwan, Singapore, and Thailand contribute significantly to regional market growth through manufacturing expansion and technology development initiatives.

Market leadership in the APAC semiconductor device for industrial applications market is distributed among several global technology companies and regional specialists. The competitive landscape reflects a combination of established semiconductor giants and innovative companies focused on specific industrial applications:

Competitive strategies include aggressive research and development investment, strategic acquisitions, and partnerships with industrial equipment manufacturers. Companies are focusing on developing application-specific solutions and providing comprehensive technical support to differentiate their offerings in the competitive market.

Technology-based segmentation of the APAC semiconductor device for industrial applications market reveals distinct categories with varying growth trajectories and application requirements:

By Device Type:

By Application Sector:

Power semiconductor devices represent the largest category within the APAC industrial applications market, accounting for approximately 35% of total demand. This segment includes silicon-based power MOSFETs, IGBTs, and emerging wide bandgap semiconductors such as silicon carbide and gallium nitride devices. Growth drivers include increasing adoption of variable frequency drives, renewable energy inverters, and electric vehicle charging infrastructure across the region.

Microcontroller and processor categories demonstrate strong growth potential with approximately 25% market share, driven by the proliferation of smart manufacturing systems and industrial IoT applications. These devices provide the computational intelligence required for advanced automation, predictive maintenance, and real-time process optimization. Edge computing capabilities integrated into industrial microcontrollers enable distributed processing and reduced latency in time-critical applications.

Analog and mixed-signal semiconductors maintain steady demand representing approximately 22% of the market, supporting critical functions such as sensor interfaces, signal conditioning, and data conversion in industrial systems. The increasing complexity of industrial sensors and the need for precise measurement and control drive continued innovation in this category. Communication semiconductor devices show rapid growth as industrial facilities implement wireless connectivity, industrial Ethernet, and 5G technologies for enhanced operational efficiency and remote monitoring capabilities.

Semiconductor manufacturers benefit from substantial growth opportunities in the APAC industrial applications market through expanding customer base, diversified revenue streams, and premium pricing for specialized industrial-grade devices. The market offers long-term customer relationships and stable demand patterns compared to consumer electronics markets. Technology innovation requirements in industrial applications drive continuous product development and intellectual property creation, strengthening competitive positioning.

Industrial equipment manufacturers gain access to advanced semiconductor technologies that enable enhanced product performance, energy efficiency, and smart functionality. The availability of specialized industrial semiconductor devices supports product differentiation and competitive advantage in global markets. Cost optimization through integrated semiconductor solutions reduces system complexity and manufacturing costs while improving reliability.

End-user industries realize significant operational benefits including improved productivity, reduced energy consumption, enhanced safety, and predictive maintenance capabilities. Digital transformation enabled by advanced semiconductor devices supports competitive advantage through optimized manufacturing processes and data-driven decision making. Regulatory compliance and sustainability goals are supported through energy-efficient semiconductor solutions and environmentally responsible manufacturing processes.

Strengths:

Weaknesses:

Opportunities:

Threats:

Artificial intelligence integration represents a transformative trend in industrial semiconductor devices, with manufacturers incorporating AI acceleration capabilities directly into microcontrollers and processors. This enables real-time machine learning inference at the edge of industrial networks, supporting predictive maintenance, quality control, and autonomous manufacturing processes. AI-optimized semiconductors are becoming essential components in smart factory implementations across the APAC region.

Wide bandgap semiconductor adoption is accelerating in high-power industrial applications, with silicon carbide and gallium nitride devices offering superior efficiency and performance compared to traditional silicon-based solutions. These advanced materials enable smaller, more efficient power conversion systems and support the growing demand for renewable energy integration. Cost reduction trends in wide bandgap manufacturing are making these technologies accessible for broader industrial applications.

Cybersecurity enhancement in industrial semiconductor devices is becoming increasingly critical as manufacturing systems become more connected and vulnerable to cyber threats. Semiconductor manufacturers are integrating hardware-based security features, encryption capabilities, and secure boot mechanisms into industrial devices. Functional safety compliance requirements are driving development of semiconductor devices that meet stringent safety standards for critical industrial applications, particularly in automotive and process industries.

Strategic partnerships between semiconductor manufacturers and industrial automation companies are accelerating innovation and market penetration. Recent collaborations focus on developing integrated solutions that combine semiconductor devices with software platforms and system-level expertise. Technology licensing agreements enable broader access to advanced semiconductor technologies while supporting regional manufacturing capabilities.

Manufacturing capacity expansion initiatives across the APAC region are addressing supply chain constraints and supporting growing demand for industrial semiconductor devices. Major investments in new fabrication facilities and advanced packaging technologies are enhancing regional production capabilities. Government support programs in countries such as China, India, and Japan are providing incentives for domestic semiconductor manufacturing development.

Acquisition activities continue to reshape the competitive landscape as companies seek to strengthen their industrial semiconductor portfolios and expand market reach. Recent transactions focus on acquiring specialized technologies, customer relationships, and regional market presence. Research and development investments are increasing substantially as companies compete to develop next-generation semiconductor technologies for emerging industrial applications.

MarkWide Research recommends that semiconductor manufacturers focus on developing comprehensive industrial solutions that combine multiple device functions and provide integrated software support. The market trend toward system-level solutions requires companies to expand beyond traditional component supply to offer complete platforms that address specific industrial applications. Investment priorities should emphasize wide bandgap technologies, AI integration capabilities, and cybersecurity features to capture emerging market opportunities.

Market entry strategies for new participants should focus on specialized application niches where established players may have limited presence. Developing expertise in specific industrial sectors such as renewable energy, electric vehicles, or smart manufacturing can provide competitive advantages and customer loyalty. Partnership approaches with regional industrial equipment manufacturers and system integrators can accelerate market penetration and provide valuable application insights.

Supply chain resilience should be a priority for all market participants, with strategies including geographic diversification of manufacturing, strategic inventory management, and development of alternative sourcing options. Companies should invest in supply chain visibility and risk management capabilities to navigate potential disruptions. Talent development programs focusing on industrial application expertise and advanced semiconductor technologies are essential for long-term competitive success in this specialized market.

Long-term growth prospects for the APAC semiconductor device for industrial applications market remain highly favorable, with sustained demand driven by ongoing industrial digitalization and automation initiatives. The market is expected to maintain robust growth with projected CAGR of 8.2% through the next decade, supported by expanding manufacturing capacity and technological innovation. Emerging technologies including quantum computing, advanced AI, and next-generation communication standards will create new categories of industrial semiconductor devices.

Regional market evolution will see continued leadership from established manufacturing hubs while emerging markets in Southeast Asia and India gain increasing importance. The development of regional semiconductor ecosystems and government support for domestic manufacturing will reshape competitive dynamics. Technology convergence trends will blur traditional product boundaries and create opportunities for innovative companies that can integrate multiple semiconductor functions effectively.

Sustainability requirements will increasingly influence product development and manufacturing processes, with emphasis on energy efficiency, recyclability, and environmental compliance. MWR analysis indicates that companies investing in green semiconductor technologies and sustainable manufacturing practices will gain competitive advantages in environmentally conscious markets. The integration of circular economy principles in semiconductor design and manufacturing will become increasingly important for long-term market success.

The APAC semiconductor device for industrial applications market represents a dynamic and rapidly evolving sector with exceptional growth potential driven by industrial automation, digital transformation, and technological innovation. The market’s strong fundamentals, including robust demand from diverse industrial sectors, advanced manufacturing capabilities, and supportive government policies, create a favorable environment for sustained expansion and innovation.

Key success factors for market participants include technological leadership in emerging areas such as wide bandgap semiconductors and AI integration, strong customer relationships with industrial equipment manufacturers, and comprehensive support capabilities that address complex application requirements. The market rewards companies that can deliver reliable, high-performance solutions while maintaining competitive pricing and superior technical support.

Future market development will be characterized by increasing integration of advanced technologies, growing emphasis on sustainability and energy efficiency, and continued expansion of industrial automation across the APAC region. Companies that successfully navigate the challenges of supply chain management, talent acquisition, and technological complexity while capitalizing on emerging opportunities will achieve leadership positions in this strategically important market segment.

What is Semiconductor Device For Industrial Applications?

Semiconductor devices for industrial applications refer to electronic components that utilize semiconductor materials to control electrical currents. These devices are essential in various industrial sectors, including manufacturing, automation, and energy management.

What are the key players in the APAC Semiconductor Device For Industrial Applications Market?

Key players in the APAC Semiconductor Device For Industrial Applications Market include companies like Infineon Technologies, Texas Instruments, and STMicroelectronics, among others. These companies are known for their innovative solutions and extensive product portfolios in semiconductor technology.

What are the main drivers of the APAC Semiconductor Device For Industrial Applications Market?

The main drivers of the APAC Semiconductor Device For Industrial Applications Market include the increasing demand for automation in manufacturing processes, the growth of renewable energy technologies, and the rising need for energy-efficient solutions across various industries.

What challenges does the APAC Semiconductor Device For Industrial Applications Market face?

Challenges in the APAC Semiconductor Device For Industrial Applications Market include supply chain disruptions, rapid technological changes, and the high cost of research and development. These factors can hinder the growth and adoption of new semiconductor technologies.

What opportunities exist in the APAC Semiconductor Device For Industrial Applications Market?

Opportunities in the APAC Semiconductor Device For Industrial Applications Market include the expansion of smart manufacturing initiatives, the integration of IoT technologies, and the increasing investment in electric vehicles. These trends are expected to drive demand for advanced semiconductor solutions.

What trends are shaping the APAC Semiconductor Device For Industrial Applications Market?

Trends shaping the APAC Semiconductor Device For Industrial Applications Market include the rise of Industry Four Point Zero, advancements in AI and machine learning applications, and the growing focus on sustainability in semiconductor manufacturing processes. These trends are influencing product development and market strategies.

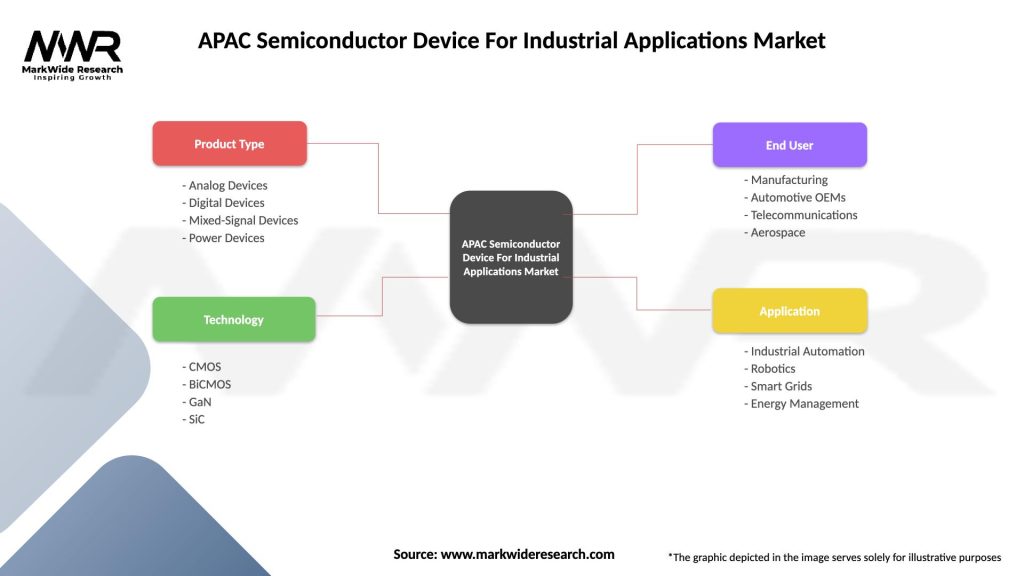

APAC Semiconductor Device For Industrial Applications Market

| Segmentation Details | Description |

|---|---|

| Product Type | Analog Devices, Digital Devices, Mixed-Signal Devices, Power Devices |

| Technology | CMOS, BiCMOS, GaN, SiC |

| End User | Manufacturing, Automotive OEMs, Telecommunications, Aerospace |

| Application | Industrial Automation, Robotics, Smart Grids, Energy Management |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the APAC Semiconductor Device For Industrial Applications Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.