444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The APAC automotive lubricants market represents one of the most dynamic and rapidly expanding segments within the global automotive industry. This comprehensive market encompasses a diverse range of lubricating products specifically designed for automotive applications across the Asia-Pacific region, including engine oils, transmission fluids, brake fluids, gear oils, and specialty automotive lubricants. The region’s automotive lubricants sector has experienced remarkable transformation driven by increasing vehicle production, rising consumer awareness about vehicle maintenance, and stringent environmental regulations promoting advanced lubricant technologies.

Market dynamics in the APAC region reflect the unique characteristics of diverse economies, ranging from mature automotive markets in Japan and South Korea to rapidly developing markets in India, China, and Southeast Asian countries. The automotive lubricants market growth trajectory shows consistent expansion at a 6.2% CAGR, supported by increasing vehicle parc, growing industrial activities, and rising demand for high-performance lubricants. Regional variations in market development create opportunities for both established international players and emerging local manufacturers to capture market share through strategic positioning and product innovation.

Technology advancement continues to reshape the automotive lubricants landscape, with synthetic and semi-synthetic lubricants gaining significant traction due to their superior performance characteristics and extended service intervals. The market demonstrates strong correlation with automotive production trends, urbanization rates, and economic development across APAC countries, positioning it as a critical component of the region’s automotive ecosystem.

The APAC automotive lubricants market refers to the comprehensive ecosystem of lubricating products, services, and technologies specifically designed for automotive applications across Asia-Pacific countries, encompassing engine oils, transmission fluids, hydraulic fluids, and specialty automotive lubricants used in passenger cars, commercial vehicles, and two-wheelers throughout the region.

Automotive lubricants serve essential functions in vehicle operation, including friction reduction, heat dissipation, corrosion protection, and component cleaning within automotive engines and mechanical systems. These specialized formulations are engineered to meet specific performance standards established by automotive manufacturers and international organizations, ensuring optimal vehicle performance, fuel efficiency, and component longevity across diverse operating conditions prevalent in APAC markets.

Market scope extends beyond traditional lubricant products to include value-added services such as lubricant analysis, condition monitoring, and technical support services that enhance customer relationships and drive market differentiation. The automotive lubricants ecosystem encompasses multiple distribution channels, including automotive dealerships, independent service centers, retail outlets, and direct-to-consumer platforms, creating comprehensive market coverage across urban and rural areas throughout the Asia-Pacific region.

Strategic market analysis reveals that the APAC automotive lubricants market stands at a pivotal juncture, characterized by robust growth momentum, technological innovation, and evolving consumer preferences toward premium lubricant products. The market benefits from strong automotive industry fundamentals, including increasing vehicle production, expanding vehicle parc, and growing awareness about preventive maintenance practices across diverse APAC economies.

Key growth drivers include rapid urbanization, rising disposable incomes, and increasing vehicle ownership rates, particularly in emerging markets such as India, Indonesia, and Vietnam. The market demonstrates resilience through diversified product portfolios, strong distribution networks, and strategic partnerships between international lubricant manufacturers and local automotive industry stakeholders. Premium segment growth accelerates at 8.4% annually, reflecting consumer willingness to invest in high-performance lubricants that deliver enhanced fuel economy and extended service intervals.

Competitive landscape features a balanced mix of global multinational corporations and regional players, creating dynamic market conditions that foster innovation and competitive pricing strategies. The market’s future trajectory appears promising, supported by ongoing automotive industry expansion, increasing focus on environmental sustainability, and continuous technological advancement in lubricant formulations and applications across the APAC region.

Market intelligence reveals several critical insights that shape the APAC automotive lubricants landscape and influence strategic decision-making for industry participants:

Automotive industry expansion serves as the primary catalyst driving APAC automotive lubricants market growth, with increasing vehicle production, expanding automotive manufacturing capacity, and rising vehicle ownership rates creating sustained demand for lubricant products across all market segments. The region’s position as a global automotive manufacturing hub generates substantial original equipment manufacturer demand while supporting robust aftermarket lubricant consumption patterns.

Economic development across APAC countries translates directly into increased automotive lubricants consumption through multiple channels, including rising disposable incomes, urbanization trends, and infrastructure development that supports increased vehicle utilization. Middle-class expansion in key markets such as India, Indonesia, and Vietnam creates new customer segments with higher quality expectations and willingness to invest in premium lubricant products that deliver superior performance and protection.

Technological advancement in automotive engineering drives demand for specialized lubricant formulations that meet increasingly stringent performance requirements, including extended drain intervals, improved fuel economy, and enhanced component protection under extreme operating conditions. Environmental consciousness among consumers and regulatory bodies promotes adoption of eco-friendly lubricant technologies, creating market opportunities for bio-based and synthetic lubricant products that reduce environmental impact while delivering superior performance characteristics.

Infrastructure development throughout the APAC region supports market expansion through improved transportation networks, expanded service station coverage, and enhanced distribution capabilities that increase lubricant accessibility in previously underserved markets, particularly in rural and semi-urban areas where vehicle ownership continues to grow rapidly.

Price volatility in raw material markets, particularly crude oil and base oil prices, creates significant challenges for automotive lubricants manufacturers in maintaining stable pricing strategies while preserving profit margins. Economic uncertainties and currency fluctuations across APAC markets compound these challenges, making long-term planning and investment decisions more complex for industry participants operating across multiple countries with varying economic conditions.

Regulatory complexity across diverse APAC markets creates compliance challenges for lubricant manufacturers, with varying environmental standards, quality specifications, and import regulations requiring significant investment in regulatory expertise and product adaptation. Market fragmentation in some regions limits economies of scale and increases distribution costs, particularly for international players seeking to establish comprehensive market coverage across multiple countries with different market characteristics.

Counterfeit products pose ongoing challenges to legitimate market participants, particularly in price-sensitive segments where consumers may prioritize cost over quality, potentially damaging brand reputation and creating safety concerns. Extended drain intervals and improved lubricant performance paradoxically reduce consumption frequency, requiring manufacturers to focus on value creation and customer retention strategies rather than volume-based growth approaches.

Competitive intensity from both international and local players creates margin pressure, particularly in commodity segments where product differentiation opportunities are limited and price competition becomes the primary competitive factor influencing customer purchasing decisions.

Electric vehicle transition creates new market opportunities for specialized lubricants designed for electric powertrains, including transmission fluids, thermal management fluids, and battery cooling systems that require unique performance characteristics different from traditional internal combustion engine applications. Hybrid vehicle growth generates demand for lubricants that can perform effectively in both electric and conventional powertrain applications, creating opportunities for innovative product development and market positioning.

Digital transformation enables new business models including predictive maintenance services, condition monitoring systems, and data-driven lubricant recommendations that create additional revenue streams while strengthening customer relationships. E-commerce expansion provides opportunities for direct customer engagement, improved inventory management, and enhanced customer service delivery through digital platforms that complement traditional distribution channels.

Sustainability focus drives demand for bio-based lubricants, recycled lubricant products, and environmentally friendly packaging solutions that appeal to environmentally conscious consumers and meet corporate sustainability objectives. Premium segment growth offers opportunities for value creation through high-performance products that command premium pricing while delivering superior customer value through enhanced performance, extended service intervals, and improved fuel economy.

Emerging markets in Southeast Asia and other developing APAC regions present significant growth opportunities as vehicle ownership rates increase, infrastructure develops, and consumer awareness about lubricant quality and performance benefits continues to expand, creating new customer segments with substantial long-term growth potential.

Supply chain evolution continues to reshape the APAC automotive lubricants market, with manufacturers investing in regional production facilities, strategic partnerships, and distribution network optimization to improve market responsiveness and reduce logistics costs. Technology integration throughout the value chain enhances operational efficiency, product quality consistency, and customer service delivery while enabling real-time market intelligence and demand forecasting capabilities.

Customer behavior patterns demonstrate increasing sophistication, with consumers becoming more knowledgeable about lubricant specifications, performance benefits, and total cost of ownership considerations that influence purchasing decisions. Service provider consolidation creates opportunities for lubricant manufacturers to develop strategic partnerships with large fleet operators, automotive service chains, and industrial customers seeking comprehensive lubricant solutions and technical support services.

Innovation cycles accelerate as manufacturers invest in research and development capabilities to address evolving automotive technologies, environmental regulations, and customer performance expectations. Market consolidation trends create both challenges and opportunities, with larger players gaining scale advantages while creating market space for specialized niche players focused on specific applications or customer segments.

Regulatory harmonization efforts across APAC regions gradually reduce compliance complexity while maintaining environmental and quality standards, facilitating market expansion and product standardization initiatives that benefit both manufacturers and customers through improved product availability and consistency.

Comprehensive market analysis employs multiple research methodologies to ensure accuracy, reliability, and depth of market insights for the APAC automotive lubricants market. Primary research includes extensive interviews with industry executives, automotive manufacturers, lubricant distributors, and end-users across major APAC markets to gather firsthand insights about market trends, competitive dynamics, and future growth prospects.

Secondary research incorporates analysis of industry reports, company financial statements, regulatory filings, trade association data, and government statistics to validate primary research findings and provide comprehensive market context. Quantitative analysis utilizes statistical modeling techniques to project market trends, segment growth patterns, and regional development trajectories based on historical data and identified market drivers.

Market validation processes include cross-referencing multiple data sources, expert panel reviews, and industry stakeholder feedback to ensure research accuracy and reliability. Regional expertise leverages local market knowledge and cultural understanding to provide nuanced insights about market conditions, consumer behavior, and competitive dynamics specific to individual APAC countries and sub-regions.

Continuous monitoring systems track market developments, regulatory changes, and industry innovations to maintain current market intelligence and identify emerging trends that may impact market dynamics and growth projections throughout the research period.

China dominates the APAC automotive lubricants market with 42% regional market share, driven by massive automotive production capacity, large vehicle parc, and growing consumer awareness about lubricant quality and performance benefits. The Chinese market demonstrates strong growth in premium lubricant segments while maintaining significant volume in conventional products, creating opportunities for both international and domestic manufacturers across multiple price points and performance categories.

India represents the fastest-growing major market with 11.2% annual growth rate, supported by increasing vehicle ownership, expanding automotive manufacturing, and rising consumer disposable incomes. The Indian market shows particular strength in two-wheeler lubricants and commercial vehicle applications, reflecting the country’s unique transportation patterns and economic development characteristics.

Japan maintains market leadership in premium and synthetic lubricant segments, with 67% synthetic penetration rate reflecting advanced automotive technology adoption and consumer preference for high-performance products. The Japanese market serves as a technology development center for the region, with innovations often spreading to other APAC markets through automotive manufacturer relationships and technology transfer initiatives.

Southeast Asian markets including Indonesia, Thailand, Malaysia, and Vietnam collectively contribute 18% of regional demand, demonstrating strong growth potential driven by economic development, urbanization, and increasing vehicle ownership rates. These markets show particular promise for motorcycle and small vehicle lubricants, reflecting regional transportation preferences and economic conditions.

South Korea and Australia represent mature markets with stable demand patterns and focus on premium product segments, contributing 8% combined market share while serving as important technology adoption centers and market development laboratories for new product introductions and innovative marketing approaches.

Market leadership in the APAC automotive lubricants sector features a diverse competitive landscape combining global multinational corporations with strong regional players and emerging local manufacturers. The competitive environment demonstrates healthy dynamics with multiple pathways to success through different strategic approaches including technology leadership, cost optimization, distribution excellence, and customer service differentiation.

Leading market participants include:

Competitive strategies focus on product innovation, distribution network expansion, strategic partnerships with automotive manufacturers, and development of value-added services that enhance customer relationships and create differentiation opportunities in increasingly competitive market conditions.

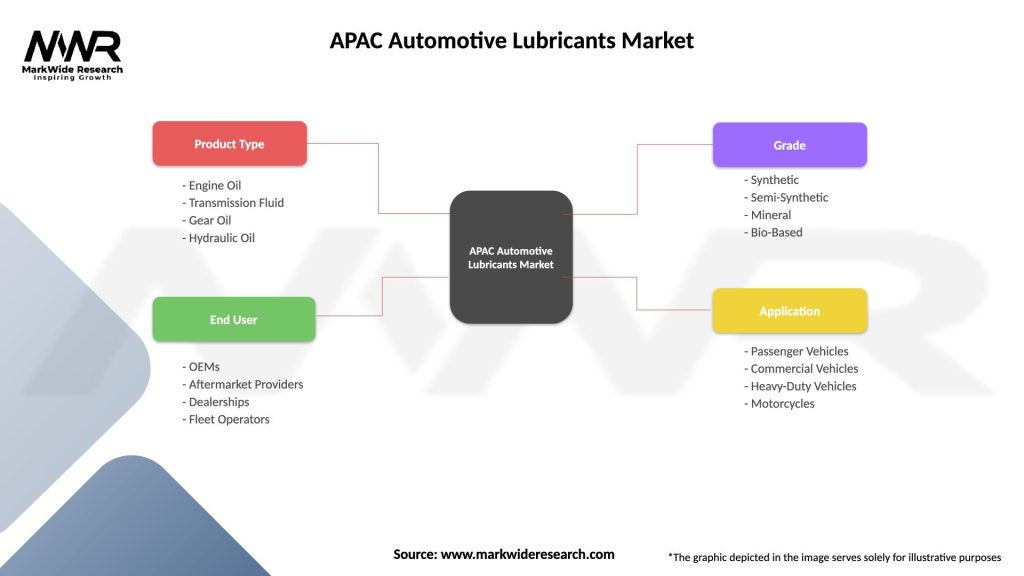

Product type segmentation reveals diverse market structure with multiple product categories serving different automotive applications and customer requirements across the APAC region:

By Product Type:

By Vehicle Type:

By Technology:

Engine oils category demonstrates the strongest market fundamentals with consistent demand growth driven by increasing vehicle parc and growing awareness about engine protection benefits. Synthetic engine oils show particular momentum with 31% annual growth rate as consumers recognize superior performance characteristics including extended drain intervals, improved fuel economy, and enhanced engine protection under extreme operating conditions prevalent in APAC climates.

Transmission fluids segment benefits from increasing automatic transmission adoption across APAC markets, particularly in passenger cars where consumer preferences shift toward convenience and driving comfort. Advanced transmission technologies including continuously variable transmissions and dual-clutch systems require specialized fluid formulations that command premium pricing while delivering enhanced performance and durability characteristics.

Two-wheeler lubricants represent the most dynamic category with exceptional growth potential driven by urbanization trends, traffic congestion, and fuel economy considerations that favor motorcycle and scooter adoption. Premium two-wheeler oils gain traction as consumers invest in higher-quality lubricants to protect increasingly sophisticated engines and extend service intervals in demanding urban operating conditions.

Commercial vehicle lubricants focus on total cost of ownership optimization, with fleet operators increasingly selecting high-performance products that reduce maintenance costs, extend component life, and improve fuel efficiency. Heavy-duty applications drive demand for specialized formulations that can withstand extreme operating conditions while meeting stringent environmental regulations across different APAC markets.

Manufacturers benefit from expanding market opportunities, technological advancement requirements, and premium product demand that support revenue growth and margin improvement initiatives. Product innovation capabilities enable differentiation strategies while regulatory compliance requirements create barriers to entry that protect established market positions and investment returns.

Distributors gain from market expansion, increasing product complexity, and service integration opportunities that enhance customer relationships and create additional revenue streams. Digital transformation initiatives improve operational efficiency, inventory management, and customer service delivery while reducing distribution costs and expanding market reach capabilities.

Automotive manufacturers benefit from improved lubricant technologies that enhance vehicle performance, reduce warranty costs, and support environmental compliance objectives. Strategic partnerships with lubricant suppliers enable co-development opportunities, technical support services, and marketing collaboration that strengthen competitive positioning in automotive markets.

End customers receive value through improved vehicle performance, extended component life, enhanced fuel economy, and reduced maintenance requirements that lower total cost of ownership. Premium lubricant adoption delivers measurable benefits including longer drain intervals, better engine protection, and improved driving experience that justify investment in higher-quality products.

Service providers benefit from increasing lubricant complexity, extended service intervals, and value-added service opportunities that enhance customer relationships and create differentiation opportunities in competitive automotive service markets throughout the APAC region.

Strengths:

Weaknesses:

Opportunities:

Threats:

Synthetic lubricant adoption accelerates across all vehicle segments as consumers recognize performance benefits including extended drain intervals, improved fuel economy, and enhanced engine protection. Premium positioning strategies focus on value demonstration rather than price competition, with manufacturers investing in customer education and technical support services that highlight total cost of ownership advantages.

Digital integration transforms customer engagement through mobile applications, online ordering platforms, and predictive maintenance services that enhance customer experience while creating new revenue opportunities. Data analytics capabilities enable personalized product recommendations, optimized inventory management, and improved customer service delivery across multiple touchpoints and distribution channels.

Sustainability initiatives drive product development toward bio-based formulations, recycled content integration, and environmentally friendly packaging solutions that meet corporate responsibility objectives while appealing to environmentally conscious consumers. Circular economy principles influence business model development with increased focus on used oil collection, reprocessing, and sustainable supply chain practices.

Electric vehicle preparation includes development of specialized lubricants for electric powertrains, thermal management systems, and hybrid applications that require different performance characteristics compared to traditional internal combustion engine lubricants. Technology partnerships with automotive manufacturers accelerate product development and market introduction timelines for next-generation lubricant solutions.

Manufacturing capacity expansion continues across the APAC region with major lubricant producers investing in new production facilities and technology upgrades to meet growing demand and improve operational efficiency. Strategic acquisitions and partnerships reshape competitive dynamics as companies seek to strengthen market positions, expand geographic coverage, and enhance technological capabilities through consolidation activities.

Product innovation accelerates with introduction of advanced synthetic formulations, extended drain interval products, and specialized lubricants for new automotive technologies including hybrid and electric vehicles. MarkWide Research analysis indicates that new product launches increased by 24% over the past year, reflecting industry commitment to innovation and market differentiation strategies.

Distribution modernization includes digital platform development, supply chain optimization, and customer service enhancement initiatives that improve market responsiveness and operational efficiency. Regulatory compliance investments address evolving environmental standards and quality requirements across different APAC markets, ensuring continued market access and competitive positioning.

Sustainability programs expand with increased focus on renewable feedstocks, carbon footprint reduction, and circular economy initiatives that align with corporate responsibility objectives and customer expectations for environmentally responsible products and business practices.

Market participants should prioritize investment in synthetic lubricant technologies and premium product development to capture growing demand for high-performance solutions that deliver superior customer value. Distribution network optimization through digital integration and strategic partnerships will enhance market coverage and customer service capabilities while reducing operational costs and improving competitive positioning.

Regional expansion strategies should focus on emerging APAC markets with strong growth potential, particularly in Southeast Asia where vehicle ownership rates continue to increase and consumer awareness about lubricant quality benefits expands. Technology partnerships with automotive manufacturers will accelerate product development for next-generation vehicle technologies and create competitive advantages through early market entry and technical expertise.

Sustainability initiatives require immediate attention as environmental regulations tighten and consumer preferences shift toward eco-friendly products, creating both compliance requirements and market opportunities for companies that proactively address environmental concerns. Digital transformation investments should focus on customer engagement platforms, data analytics capabilities, and predictive maintenance services that create additional revenue streams while strengthening customer relationships.

Brand building activities should emphasize performance differentiation, technical expertise, and customer education to support premium pricing strategies and reduce price-based competition in commodity segments. Supply chain resilience improvements through diversified sourcing, strategic inventory management, and regional production capabilities will mitigate risk and ensure consistent product availability across volatile market conditions.

Long-term growth prospects for the APAC automotive lubricants market remain highly favorable, supported by continued automotive industry expansion, increasing vehicle ownership rates, and growing consumer awareness about lubricant quality and performance benefits. Market evolution will be shaped by technological advancement, environmental regulations, and changing consumer preferences that favor premium products and sustainable solutions.

Electric vehicle transition will create new market segments while potentially reducing demand in traditional applications, requiring industry adaptation and product development investments to maintain growth momentum. MWR projections indicate that electric vehicle lubricant applications will represent 15% of market volume by 2030, creating significant opportunities for companies that successfully develop specialized products for emerging powertrain technologies.

Regional market development will continue to vary significantly, with emerging markets offering the strongest growth potential while mature markets focus on premium products and value-added services. Technology convergence between automotive and industrial lubricant applications will create cross-segment opportunities for diversified manufacturers with comprehensive product portfolios and technical expertise.

Competitive dynamics will intensify as market growth attracts new entrants while established players invest in differentiation strategies, creating both challenges and opportunities for companies with strong market positions and innovative capabilities. Sustainability requirements will become increasingly important competitive factors, influencing product development priorities, supply chain decisions, and customer purchasing criteria throughout the forecast period.

The APAC automotive lubricants market represents a dynamic and rapidly evolving industry sector with substantial growth potential driven by automotive industry expansion, technological advancement, and increasing consumer sophistication across diverse regional markets. Market fundamentals remain strong with multiple growth drivers including vehicle ownership increases, premium product adoption, and emerging technology requirements that create opportunities for innovation and value creation.

Strategic success in this market requires balanced approaches that combine technological leadership, distribution excellence, customer service differentiation, and sustainability initiatives to address evolving market requirements and competitive challenges. Industry participants that successfully navigate market complexities while investing in future technologies and customer relationships will be well-positioned to capture growth opportunities and maintain competitive advantages in this essential automotive industry segment.

The future trajectory of the APAC automotive lubricants market appears highly promising, with continued expansion expected across multiple dimensions including geographic coverage, product sophistication, and application diversity, creating sustained opportunities for growth and value creation throughout the forecast period.

What is Automotive Lubricants?

Automotive lubricants are substances used to reduce friction between surfaces in automotive engines and machinery. They play a crucial role in enhancing performance, reducing wear, and improving the efficiency of vehicles.

What are the key players in the APAC Automotive Lubricants Market?

Key players in the APAC Automotive Lubricants Market include companies like Castrol, Mobil, and Shell, which are known for their extensive product ranges and innovations in lubricant technology, among others.

What are the main drivers of the APAC Automotive Lubricants Market?

The main drivers of the APAC Automotive Lubricants Market include the increasing vehicle production and sales, rising consumer awareness about vehicle maintenance, and advancements in lubricant formulations that enhance engine performance.

What challenges does the APAC Automotive Lubricants Market face?

Challenges in the APAC Automotive Lubricants Market include stringent environmental regulations, the growing trend towards electric vehicles, and the need for continuous innovation to meet changing consumer demands.

What opportunities exist in the APAC Automotive Lubricants Market?

Opportunities in the APAC Automotive Lubricants Market include the expansion of the automotive sector in emerging economies, the development of bio-based lubricants, and the increasing demand for high-performance lubricants in various automotive applications.

What trends are shaping the APAC Automotive Lubricants Market?

Trends shaping the APAC Automotive Lubricants Market include the shift towards synthetic lubricants, the integration of smart technology in lubricant formulations, and a growing focus on sustainability and eco-friendly products.

APAC Automotive Lubricants Market

| Segmentation Details | Description |

|---|---|

| Product Type | Engine Oil, Transmission Fluid, Gear Oil, Hydraulic Oil |

| End User | OEMs, Aftermarket Providers, Dealerships, Fleet Operators |

| Grade | Synthetic, Semi-Synthetic, Mineral, Bio-Based |

| Application | Passenger Vehicles, Commercial Vehicles, Heavy-Duty Vehicles, Motorcycles |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the APAC Automotive Lubricants Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.