The Airplane GPS Market represents a crucial segment within the aviation industry, providing essential navigation and positioning capabilities to aircraft worldwide. Global Positioning System (GPS) technology has revolutionized air navigation, offering precise location information, route guidance, and situational awareness to pilots and air traffic controllers. The airplane GPS market encompasses a wide range of GPS equipment, including receivers, antennas, and navigation systems, designed to enhance flight safety, efficiency, and operational capabilities.

Meaning

Airplane GPS refers to the use of GPS technology in aircraft for navigation, flight planning, and position tracking purposes. GPS receivers installed onboard aircraft receive signals from a constellation of satellites orbiting the Earth, allowing pilots to determine their precise location, altitude, speed, and heading. Airplane GPS systems provide critical situational awareness to flight crews, enabling them to navigate accurately, avoid hazards, and adhere to prescribed flight paths during all phases of flight.

Executive Summary

The airplane GPS market is witnessing steady growth driven by increasing air traffic, rising demand for efficient navigation solutions, and advancements in GPS technology. The adoption of satellite-based navigation systems, such as GPS, enhances flight safety, reduces operational costs, and improves airspace capacity. Key market players are investing in research and development to develop next-generation GPS technologies tailored to the specific needs of the aviation industry, driving innovation and market competitiveness.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Growing Air Traffic: The exponential growth in air traffic worldwide has propelled the demand for airplane GPS systems. Commercial airlines, general aviation operators, and military aircraft rely on GPS technology for precise navigation, route optimization, and airspace management, contributing to market expansion.

Technological Advancements: Ongoing advancements in GPS technology, including multi-constellation receivers, augmentation systems, and satellite-based augmentation systems (SBAS), enhance the accuracy, reliability, and availability of airplane GPS systems. Innovations such as GPS-aided landing systems (GLS) and synthetic vision technology (SVT) improve flight safety and operational efficiency.

Regulatory Compliance: Regulatory mandates and standards, such as Required Navigation Performance (RNP) and Performance-Based Navigation (PBN), drive the adoption of airplane GPS systems to meet airspace requirements and operational performance criteria. Compliance with international aviation regulations, such as those set by the International Civil Aviation Organization (ICAO) and Federal Aviation Administration (FAA), influences market dynamics and product development.

Integration with Avionics: Airplane GPS systems are integrated with avionics suites, flight management systems (FMS), and cockpit displays to provide seamless navigation, guidance, and flight planning capabilities. Integration with other avionics systems, such as autopilot and terrain awareness and warning systems (TAWS), enhances overall flight situational awareness and crew decision-making.

Market Drivers

Enhanced Safety: Airplane GPS systems improve flight safety by providing accurate position information, terrain awareness, and obstacle avoidance capabilities. Enhanced situational awareness enables pilots to navigate safely in challenging weather conditions, congested airspace, and remote regions, reducing the risk of accidents and incidents.

Operational Efficiency: GPS-enabled flight planning and navigation streamline flight operations, reduce fuel consumption, and minimize flight delays. Efficient route optimization, direct-to-navigation capabilities, and precision approach procedures optimize flight paths, shorten flight times, and enhance operational productivity for airlines and operators.

Airspace Modernization: Global initiatives to modernize airspace infrastructure, such as Next Generation Air Transportation System (NextGen) in the United States and Single European Sky (SES) in Europe, drive the adoption of satellite-based navigation technologies, including airplane GPS systems. Airspace redesign, performance-based navigation (PBN), and continuous descent approaches (CDA) rely on GPS technology to increase airspace capacity and efficiency.

Rapid Urbanization: Urbanization and population growth lead to increased demand for air travel, particularly in densely populated regions and emerging markets. Airplane GPS systems support the expansion of air transportation networks, enable airport access, and facilitate regional connectivity, meeting the growing demand for reliable and efficient air navigation solutions.

Market Restraints

Cybersecurity Concerns: The susceptibility of GPS signals to jamming, spoofing, and cyber attacks poses cybersecurity risks to airplane GPS systems. Unauthorized interference with GPS signals can disrupt navigation, compromise flight safety, and undermine the reliability of GPS-dependent avionics systems, necessitating robust cybersecurity measures and mitigation strategies.

Satellite Signal Interference: Environmental factors, electromagnetic interference, and satellite constellation anomalies can degrade GPS signal quality and accuracy, affecting the performance of airplane GPS systems. Signal blockage in urban canyons, mountainous terrain, and adverse weather conditions may impair navigation reliability and necessitate backup navigation methods.

Cost and Complexity: The initial acquisition cost, installation expenses, and maintenance requirements associated with airplane GPS systems can be significant for aircraft operators, particularly for retrofitting older aircraft with modern avionics equipment. The complexity of GPS integration with existing avionics architectures and regulatory compliance obligations may further add to implementation challenges and costs.

Regulatory Compliance Burden: Compliance with evolving regulatory mandates, standards, and certification requirements for airplane GPS systems imposes administrative burdens and certification costs on manufacturers, operators, and maintenance organizations. Adherence to stringent aviation regulations and airworthiness standards necessitates rigorous testing, documentation, and validation processes, potentially delaying product development timelines and market entry.

Market Opportunities

Unmanned Aerial Vehicles (UAVs): The proliferation of unmanned aerial vehicles (UAVs) and drones creates opportunities for airplane GPS manufacturers to supply lightweight, compact, and cost-effective GPS solutions tailored to the needs of the UAV market. GPS-enabled autopilot systems, waypoint navigation, and geofencing capabilities enhance UAV autonomy, mission flexibility, and operational safety.

Urban Air Mobility (UAM): The emergence of urban air mobility (UAM) concepts and electric vertical takeoff and landing (eVTOL) aircraft presents opportunities for airplane GPS suppliers to develop navigation systems optimized for urban airspace operations. GPS-based traffic management, collision avoidance, and vertiport navigation solutions support the integration of eVTOL aircraft into urban transportation networks.

Satellite Constellation Expansion: The expansion of satellite navigation constellations, such as GPS, Galileo, GLONASS, and BeiDou, increases the availability, redundancy, and coverage of GPS signals worldwide. Airplane GPS manufacturers can leverage multi-constellation receivers and augmentation systems to enhance signal reception, accuracy, and integrity for aviation applications, including precision approaches and unmanned aerial systems (UAS).

Remote and Regional Connectivity: Airplane GPS systems play a vital role in supporting remote and regional air transportation connectivity, enabling access to underserved communities, remote islands, and rural areas. GPS-enabled flight planning, instrument approaches, and airport navigation aid in improving accessibility, reliability, and safety for air travel in remote regions, promoting economic development and tourism.

Market Dynamics

The airplane GPS market operates in a dynamic environment shaped by technological innovation, regulatory requirements, market competition, and evolving customer needs. Key market dynamics include:

Technology Innovation: Continuous innovation in GPS technology, satellite navigation systems, and avionics integration drives product development, differentiation, and market leadership. Advancements in receiver sensitivity, anti-jamming capabilities, and augmentation services enhance GPS performance and reliability for aviation applications.

Regulatory Evolution: Regulatory changes, standards updates, and certification requirements influence product design, testing, and market acceptance of airplane GPS systems. Compliance with aviation regulations, airspace mandates, and safety standards is essential for market access and customer confidence in GPS-equipped aircraft.

Market Competition: Intense competition among airplane GPS manufacturers, avionics suppliers, and technology vendors fuels innovation, price competition, and market segmentation. Differentiation strategies based on product features, performance, reliability, and customer support drive market positioning and customer preferences in the highly competitive aviation navigation market.

Customer Requirements: Customer demands for enhanced navigation capabilities, interoperability, and integration drive product customization, aftermarket upgrades, and service offerings. Tailoring GPS solutions to meet specific customer requirements, mission profiles, and operational environments enhances customer satisfaction and loyalty in the competitive airplane GPS market.

Regional Analysis

The airplane GPS market exhibits regional variations influenced by factors such as aviation infrastructure, regulatory frameworks, technological adoption, and market demand. Regional analysis highlights key market trends and opportunities across major geographic regions:

North America: North America dominates the airplane GPS market, driven by robust air transportation infrastructure, technological innovation, and regulatory compliance. The presence of leading GPS manufacturers, avionics suppliers, and aerospace companies fosters market growth and innovation in the region.

Europe: Europe is a significant market for airplane GPS systems, characterized by stringent safety standards, airspace modernization initiatives, and regulatory harmonization. The European Union’s Single European Sky (SES) initiative and Galileo satellite navigation program contribute to market expansion and adoption of satellite-based navigation solutions.

Asia Pacific: Asia Pacific represents a growing market for airplane GPS technology, fueled by rapid economic growth, urbanization, and increasing air travel demand. Emerging economies, such as China, India, and Southeast Asian countries, invest in aviation infrastructure development, airspace modernization, and fleet expansion, driving demand for GPS-enabled navigation systems.

Middle East and Africa: The Middle East and Africa region witness opportunities for airplane GPS market growth, driven by airport expansion projects, tourism development, and air transportation connectivity initiatives. Investments in aviation infrastructure, airspace management, and fleet modernization support the adoption of GPS technology for safe and efficient air navigation.

Competitive Landscape

Leading Companies in the Airplane GPS Market:

Garmin Ltd.

Honeywell International Inc.

Rockwell Collins, Inc. (Collins Aerospace, Raytheon Technologies Corporation)

L3Harris Technologies, Inc.

Cobham plc

Trimble Inc.

NovAtel Inc. (Hexagon AB)

u-blox AG

Hemisphere GNSS

Topcon Positioning Systems, Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

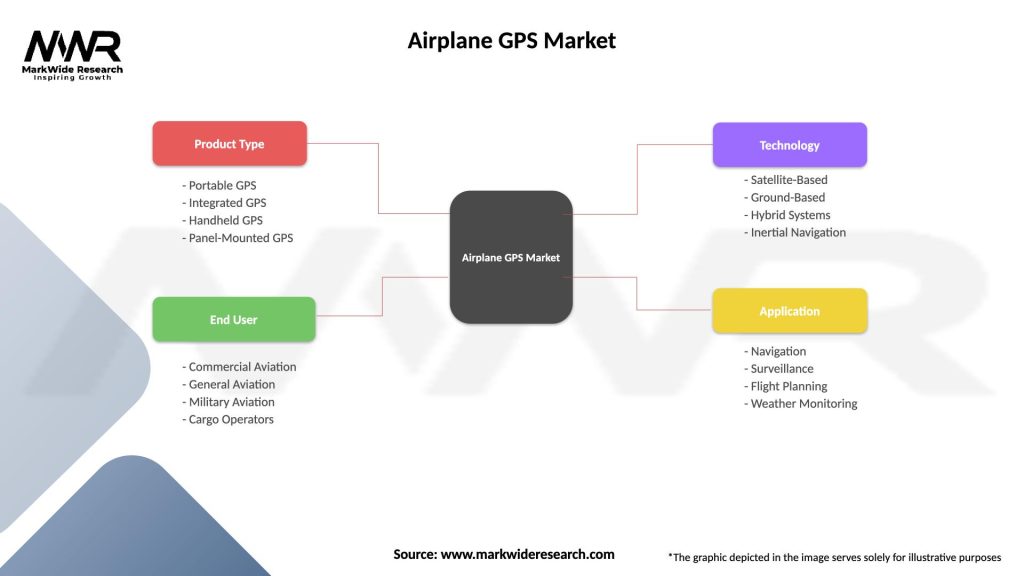

Segmentation

The airplane GPS market can be segmented based on various factors, including:

Product Type: Segmentation by product type includes GPS receivers, navigation systems, flight management systems (FMS), and integrated cockpit displays.

Aircraft Type: Segmentation by aircraft type includes commercial airliners, business jets, general aviation aircraft, military aircraft, and unmanned aerial vehicles (UAVs).

Application: Segmentation by application includes navigation, flight planning, route optimization, surveillance, and air traffic management.

End User: Segmentation by end user includes airlines, aircraft operators, military organizations, government agencies, and aviation service providers.

Segmentation provides a detailed understanding of market dynamics, customer requirements, and product applications, enabling airplane GPS manufacturers to tailor their offerings to specific market segments and customer needs.

Category-wise Insights

Commercial Aviation: Commercial airlines and operators rely on airplane GPS systems for precision navigation, flight planning, and route optimization to ensure safe and efficient air transportation services. GPS-enabled flight management systems (FMS) and cockpit displays enhance situational awareness and operational performance for commercial aviation operations.

General Aviation: General aviation pilots and aircraft owners utilize airplane GPS equipment for navigation, flight tracking, and situational awareness during private, recreational, and business flights. Portable GPS receivers, tablet-based navigation apps, and integrated avionics suites support general aviation missions, including cross-country navigation, aerial photography, and flight training.

Military Aviation: Military aircraft employ airplane GPS technology for mission planning, target designation, and combat operations across various theaters of operation. GPS-guided munitions, tactical navigation systems, and integrated avionics enhance the operational effectiveness and survivability of military aviation platforms, including fighter jets, helicopters, and transport aircraft.

Unmanned Aerial Vehicles (UAVs): UAVs and drones utilize airplane GPS systems for autonomous navigation, waypoint navigation, and mission execution in civilian and military applications. GPS-enabled autopilot systems, real-time telemetry, and geofencing capabilities support UAV operations, including aerial surveillance, reconnaissance, mapping, and cargo delivery.

Key Benefits for Industry Participants and Stakeholders

Enhanced Safety: Airplane GPS systems improve flight safety by providing accurate position information, terrain awareness, and obstacle avoidance capabilities, reducing the risk of accidents and incidents during all phases of flight.

Operational Efficiency: GPS-enabled flight planning, navigation, and route optimization streamline flight operations, reduce fuel consumption, and minimize flight delays, enhancing operational productivity and cost-effectiveness for airlines and operators.

Mission Flexibility: Airplane GPS technology enables mission flexibility and adaptability for military, commercial, and general aviation applications, supporting diverse mission profiles, operational environments, and mission requirements with precision navigation and situational awareness capabilities.

Global Connectivity: Airplane GPS systems provide global connectivity and interoperability, enabling seamless navigation, communication, and coordination across international airspace, ensuring safe and efficient air transportation services for global travelers and cargo operators.

SWOT Analysis

Strengths:

Precise Positioning: Airplane GPS systems provide precise positioning, navigation, and timing capabilities, enhancing flight safety and operational efficiency for aircraft worldwide.

Global Coverage: GPS satellite constellations offer global coverage, enabling seamless navigation and communication connectivity across diverse geographic regions and operational environments.

Reliability and Redundancy: GPS redundancy and integrity monitoring ensure reliable and resilient navigation solutions, mitigating the risk of signal interference, outage, or degradation during flight operations.

Versatility: Airplane GPS systems support a wide range of aviation applications, including commercial, military, general aviation, and unmanned aerial systems, demonstrating versatility and adaptability to diverse mission requirements.

Weaknesses:

Vulnerability to Interference: GPS signals are susceptible to interference, jamming, and spoofing attacks, posing cybersecurity risks and operational challenges for airplane GPS systems in hostile or contested environments.

Signal Degradation: Environmental factors, terrain obstructions, and atmospheric conditions can degrade GPS signal quality and accuracy, affecting navigation reliability and performance during adverse weather conditions or urban environments.

Dependence on Satellite Infrastructure: Airplane GPS systems rely on satellite infrastructure and ground control segments, introducing dependencies and vulnerabilities to satellite constellation availability, maintenance, and system upgrades.

Integration Complexity: Integration of airplane GPS systems with existing avionics architectures, flight management systems, and cockpit displays may pose technical challenges, certification requirements, and implementation complexities for aircraft operators and manufacturers.

Opportunities:

Emerging Markets: Emerging markets, including urban air mobility, unmanned aerial vehicles, and satellite constellation expansion, present growth opportunities for airplane GPS manufacturers to supply navigation solutions tailored to specific market segments and emerging applications.

Technological Innovation: Advances in GPS technology, satellite navigation systems, and avionics integration drive innovation and differentiation in the airplane GPS market, offering opportunities for product development, differentiation, and market leadership.

Regulatory Compliance: Evolving aviation regulations, airspace mandates, and safety standards create opportunities for airplane GPS suppliers to develop compliant solutions, support regulatory compliance, and address customer requirements in the global aviation market.

Partnerships and Collaborations: Strategic partnerships, collaborations, and joint ventures with satellite operators, avionics suppliers, and aerospace companies enhance market presence, expand product portfolios, and address customer needs in the competitive airplane GPS market.

Threats:

Cybersecurity Risks: Cybersecurity threats, including GPS jamming, spoofing, and cyber attacks, pose risks to airplane GPS systems, compromising navigation integrity, flight safety, and operational effectiveness in contested or hostile environments.

Competitive Pressures: Intense competition among airplane GPS manufacturers, technology vendors, and avionics suppliers may exert pricing pressures, margin erosion, and market consolidation, affecting profitability and market share in the highly competitive aviation navigation market.

Regulatory Changes: Changes in aviation regulations, standards updates, and certification requirements may introduce compliance challenges, certification delays, and market entry barriers for airplane GPS manufacturers, impacting product development and market competitiveness.

Technological Disruption: Technological disruption, including alternative navigation solutions, emerging technologies, and disruptive innovations, may challenge the relevance, competitiveness, and market positioning of traditional airplane GPS systems in the evolving aviation landscape.

Market Key Trends

Multi-Constellation Receivers: Airplane GPS systems leverage multi-constellation receivers, including GPS, Galileo, GLONASS, and BeiDou, to enhance signal availability, accuracy, and integrity, improving navigation performance and reliability for aviation applications.

Augmentation Services: Satellite-based augmentation systems (SBAS), including Wide Area Augmentation System (WAAS) in the United States and European Geostationary Navigation Overlay Service (EGNOS) in Europe, provide precision approach and landing capabilities, enabling GPS-guided approaches and vertical navigation.

Integration with Avionics: Airplane GPS systems are integrated with avionics suites, flight management systems (FMS), and cockpit displays to provide seamless navigation, guidance, and situational awareness for flight crews, enhancing operational efficiency and flight safety.

Enhanced Navigation Capabilities: GPS-enabled navigation features, such as Required Navigation Performance (RNP), Area Navigation (RNAV), and vertical navigation (VNAV), support precision approaches, curved flight paths, and optimized descent profiles, improving airspace capacity and operational flexibility.

Covid-19 Impact

The COVID-19 pandemic has had a profound impact on the aviation industry, including the airplane GPS market. While the initial phase of the pandemic led to unprecedented disruptions in air travel, flight operations, and aircraft manufacturing, the aviation sector has shown resilience and adaptability in response to the crisis. Some key impacts of COVID-19 on the airplane GPS market include:

Operational Adjustments: Airlines and operators adjusted their flight schedules, routes, and fleet utilization in response to changing passenger demand, travel restrictions, and border closures, affecting GPS usage and navigation requirements.

Supply Chain Disruptions: Supply chain disruptions, production delays, and inventory management challenges impacted airplane GPS manufacturers, component suppliers, and aftermarket service providers, affecting product availability, delivery lead times, and customer support.

Cost Optimization: Cost optimization initiatives, including fleet rationalization, deferred maintenance, and workforce adjustments, influenced investment decisions, capital expenditures, and technology upgrades for airplane GPS systems, prioritizing essential operational needs and cost-saving measures.

Operational Resilience: Aviation stakeholders demonstrated operational resilience and agility in adapting to evolving public health guidelines, safety protocols, and regulatory requirements, implementing measures to safeguard passenger health, ensure crew safety, and maintain operational continuity amidst the pandemic.

Key Industry Developments

Satellite Constellation Expansion: The expansion of satellite navigation constellations, including GPS III, Galileo, and BeiDou-3, enhances the availability, reliability, and coverage of GPS signals worldwide, supporting airplane GPS market growth and adoption in diverse aviation applications.

Next Generation Navigation Systems: Next-generation airplane GPS systems, including GPS-III satellites, Galileo Second Generation (G2) satellites, and advanced augmentation services, offer improved performance, accuracy, and integrity for aviation navigation and surveillance requirements.

Avionics Integration: Avionics manufacturers integrate airplane GPS systems with advanced flight management systems (FMS), cockpit displays, and autopilot systems to provide seamless navigation, guidance, and flight control capabilities, enhancing situational awareness and operational efficiency for flight crews.

Autonomous Navigation: Autonomous navigation technologies, such as satellite-based autonomous landing systems (SBAS), GPS-aided navigation, and autonomous flight control algorithms, enable unmanned aerial vehicles (UAVs) and autonomous aircraft to operate safely and efficiently in civilian and military missions.

Analyst Suggestions

Invest in Next-Generation Technology: Airplane GPS manufacturers should invest in next-generation GPS technology, including multi-constellation receivers, augmentation services, and satellite navigation solutions, to enhance product performance, reliability, and competitiveness in the aviation market.

Address Cybersecurity Risks: Aircraft operators and avionics suppliers should address cybersecurity risks associated with airplane GPS systems by implementing robust encryption, authentication, and intrusion detection measures to safeguard against GPS jamming, spoofing, and cyber attacks.

Enhance Regulatory Compliance: Airplane GPS manufacturers and aircraft operators should enhance regulatory compliance with evolving aviation regulations, safety standards, and certification requirements for GPS-equipped aircraft, ensuring adherence to airworthiness criteria and operational performance criteria.

Strengthen Partnerships and Alliances: Collaboration with satellite operators, avionics suppliers, and industry stakeholders strengthens market presence, expands product portfolios, and addresses customer needs in the competitive airplane GPS market, fostering innovation and market leadership.

Future Outlook

The future outlook for the Airplane GPS Market is positive, with continued growth and innovation expected in the coming years. As air travel demand rebounds and airlines invest in modernizing their fleets, the need for advanced GPS solutions will likely increase. The integration of new technologies and a focus on user training will further drive market growth. Companies that prioritize innovation, collaboration, and sustainability will be well-equipped to capitalize on the opportunities presented by this evolving market.

Conclusion

The airplane GPS market plays a pivotal role in modern aviation, providing essential navigation, positioning, and situational awareness capabilities to aircraft worldwide. Advances in GPS technology, satellite navigation systems, and avionics integration drive market growth, innovation, and competitiveness, enabling safer, more efficient, and more connected air transportation services. While the airplane GPS market faces challenges such as cybersecurity risks, regulatory compliance, and competitive pressures, strategic investments, technological innovation, and industry collaboration position the market for continued growth and evolution in the dynamic aviation landscape. As aircraft operators, manufacturers, and aviation stakeholders embrace the benefits of airplane GPS technology, the market is poised for further expansion, innovation, and transformation in the years to come.

What is Airplane GPS?

Airplane GPS refers to the Global Positioning System technology specifically designed for aviation applications, providing accurate navigation, positioning, and timing information to enhance flight safety and efficiency.

What are the key companies in the Airplane GPS Market?

Key companies in the Airplane GPS Market include Garmin, Honeywell, and Rockwell Collins, which are known for their advanced navigation systems and avionics solutions, among others.

What are the main drivers of growth in the Airplane GPS Market?

The growth of the Airplane GPS Market is driven by increasing air traffic, advancements in navigation technology, and the demand for enhanced safety features in aviation.

What challenges does the Airplane GPS Market face?

Challenges in the Airplane GPS Market include regulatory compliance issues, the high cost of advanced systems, and the need for continuous updates to maintain accuracy and reliability.

What opportunities exist in the Airplane GPS Market?

Opportunities in the Airplane GPS Market include the integration of GPS with other technologies like ADS-B and the growing demand for unmanned aerial vehicles (UAVs) that require precise navigation systems.

What trends are shaping the Airplane GPS Market?

Trends in the Airplane GPS Market include the shift towards satellite-based augmentation systems, increased use of GPS in commercial and private aviation, and the development of more compact and efficient GPS devices.

Rockwell Collins, Inc. (Collins Aerospace, Raytheon Technologies Corporation)

L3Harris Technologies, Inc.

Cobham plc

Trimble Inc.

NovAtel Inc. (Hexagon AB)

u-blox AG

Hemisphere GNSS

Topcon Positioning Systems, Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.