444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The Africa microinsurance market is gaining significant traction in recent years. Microinsurance refers to the provision of insurance products and services tailored to the specific needs and affordability of low-income individuals and communities. It aims to address the insurance gap in developing countries, where a large portion of the population remains underserved or completely excluded from traditional insurance offerings.

Meaning

Microinsurance in Africa encompasses various types of coverage, including life insurance, health insurance, property insurance, agriculture insurance, and others. The policies are designed to be affordable, accessible, and relevant to the unique challenges faced by low-income households and individuals in Africa.

Executive Summary

The Africa microinsurance market has witnessed substantial growth in recent years, driven by the increasing awareness about the importance of insurance protection and the efforts made by governments, non-governmental organizations (NGOs), and insurance providers to extend coverage to underserved communities. The market presents numerous opportunities for insurers to expand their customer base and contribute to financial inclusion in the region.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The Africa microinsurance market is characterized by dynamic and evolving trends. Key dynamics include changing consumer behaviors, advancements in technology, regulatory developments, and partnerships across sectors. These factors collectively shape the market’s growth trajectory and offer new avenues for innovation and expansion.

Regional Analysis

The Africa microinsurance market exhibits regional variations in terms of market size, penetration, and consumer preferences. East Africa, West Africa, Southern Africa, and North Africa are the major regions contributing to the growth of microinsurance in Africa. Each region has its unique characteristics and presents specific opportunities and challenges for insurance providers.

Competitive Landscape

Leading Companies in the Africa Microinsurance Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

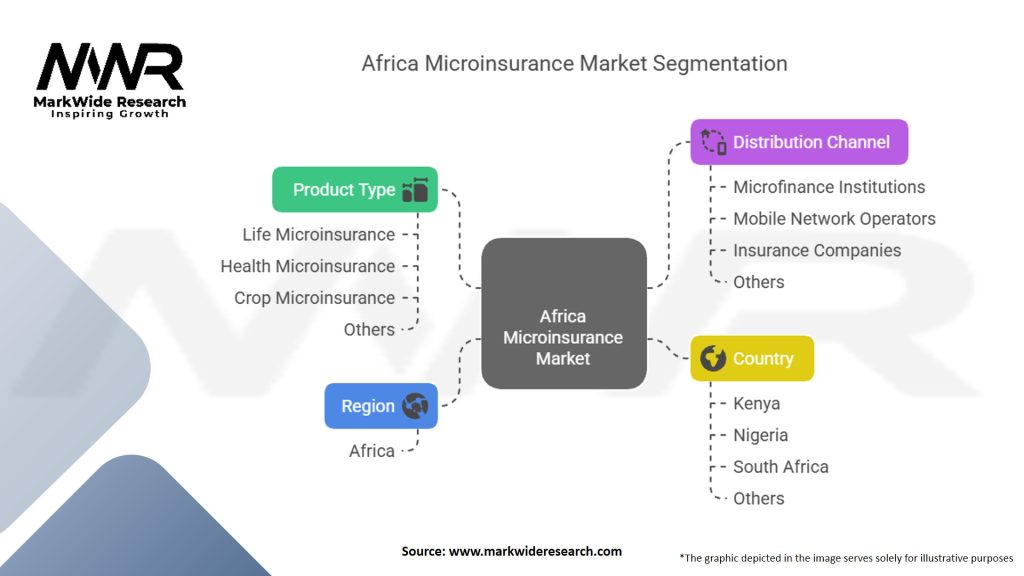

The Africa microinsurance market can be segmented based on insurance type, distribution channel, and target market. Insurance types include life insurance, health insurance, property insurance, agriculture insurance, and others. Distribution channels comprise microfinance institutions, insurance agents, mobile network operators, and digital platforms. The target market encompasses low-income individuals, micro-entrepreneurs, smallholder farmers, and informal sector workers.

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Strengths:

Weaknesses:

Opportunities:

Threats:

Market Key Trends

Covid-19 Impact

The COVID-19 pandemic has had significant implications for the Africa microinsurance market. While the crisis highlighted the need for insurance protection, it also posed challenges due to economic disruptions and the increased demand for healthcare coverage. Insurers responded by adapting their products and processes to address the emerging risks and provide support to policyholders during these challenging times.

Key Industry Developments

Analyst Suggestions

Future Outlook

The Africa microinsurance market is poised for continued growth in the coming years. The combination of favorable regulatory environments, increasing awareness about insurance, and technological advancements will drive market expansion. Insurers that can effectively navigate the unique challenges and opportunities in the African context and provide innovative, customer-centric solutions will be well-positioned for success.

Conclusion

The Africa microinsurance market represents a significant opportunity to address the insurance gap and contribute to financial inclusion in the region. With the increasing demand for insurance protection, favorable regulatory environments, and technological advancements, the market is witnessing steady growth. Insurers that can adapt to the needs of low-income individuals and communities, leverage partnerships and digital technologies, and drive product innovation will be at the forefront of this transformative market, creating value for both the industry and the communities they serve.

What is Africa microinsurance?

Africa microinsurance refers to insurance products designed to provide coverage to low-income individuals and communities in Africa. These products typically offer affordable premiums and are tailored to meet the specific needs of underserved populations, covering risks such as health, agriculture, and property.

Who are the key players in the Africa microinsurance market?

Key players in the Africa microinsurance market include companies like MicroEnsure, BIMA, and Hollard Insurance, which focus on providing accessible insurance solutions to low-income consumers. These companies are working to expand their reach and improve financial inclusion across the continent, among others.

What are the main drivers of growth in the Africa microinsurance market?

The main drivers of growth in the Africa microinsurance market include increasing awareness of insurance benefits, the rise of mobile technology facilitating access to insurance products, and the growing need for financial protection against risks such as health emergencies and crop failures.

What challenges does the Africa microinsurance market face?

The Africa microinsurance market faces several challenges, including low levels of financial literacy among potential customers, regulatory hurdles that can impede product development, and the difficulty of reaching remote populations effectively.

What opportunities exist for the future of the Africa microinsurance market?

Opportunities for the future of the Africa microinsurance market include the potential for partnerships with mobile network operators to enhance distribution, the development of innovative products tailored to specific community needs, and the increasing interest from investors in supporting inclusive insurance initiatives.

What trends are shaping the Africa microinsurance market?

Trends shaping the Africa microinsurance market include the integration of technology in product delivery, such as mobile apps and digital platforms, and a growing focus on sustainability and social impact, as companies aim to address climate risks and promote financial resilience among vulnerable populations.

Africa Microinsurance Market:

| Segmentation Details | Description |

|---|---|

| Product Type | Life Microinsurance, Health Microinsurance, Crop Microinsurance, Others |

| Distribution Channel | Microfinance Institutions, Mobile Network Operators, Insurance Companies, Others |

| Country | Kenya, Nigeria, South Africa, Others |

| Region | Africa |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the Africa Microinsurance Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.