444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The aerospace and defense ducting market is an integral part of the aerospace and defense industry, playing a critical role in the efficient operation and safety of aircraft and defense systems. Ducting systems are responsible for directing and controlling the flow of air, fluids, and gases within these systems, ensuring optimal performance and functionality. The market for aerospace and defense ducting is driven by the increasing demand for lightweight and high-performance ducting solutions that can withstand extreme operating conditions.

Meaning

Aerospace and defense ducting refers to the specialized systems of pipes, tubes, and hoses used in the aerospace and defense sectors to carry and regulate the flow of air, fluids, and gases. These ducting systems are designed to meet stringent requirements for durability, weight reduction, fire resistance, chemical resistance, and flexibility. They are crucial for the proper functioning of various aircraft components, including engines, air conditioning systems, fuel systems, hydraulic systems, and environmental control systems.

Executive Summary

The aerospace and defense ducting market is witnessing steady growth due to the increasing focus on aircraft weight reduction, fuel efficiency, and safety. The demand for lightweight and high-performance ducting solutions is driven by the need to improve aircraft performance, reduce maintenance costs, and enhance passenger comfort. Moreover, the growing defense expenditure and the modernization of military aircraft are contributing to the market’s expansion.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The aerospace and defense ducting market is characterized by intense competition, technological advancements, and stringent regulatory requirements. The market dynamics are influenced by factors such as aircraft production cycles, defense budgets, environmental regulations, and the overall economic landscape. Manufacturers in this market need to stay agile and innovative to meet evolving customer demands and industry standards.

Regional Analysis

The aerospace and defense ducting market is segmented into various regions, including North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa. North America dominates the market, owing to the presence of major aircraft manufacturers, defense contractors, and a robust aerospace industry. Europe follows closely, driven by the strong aerospace manufacturing base in countries like France, Germany, and the United Kingdom. The Asia-Pacific region is expected to witness significant growth due to the increasing defense expenditure and the expansion of the commercial aviation sector in countries like China and India.

Competitive Landscape

Leading Companies in Aerospace and Defense Ducting Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

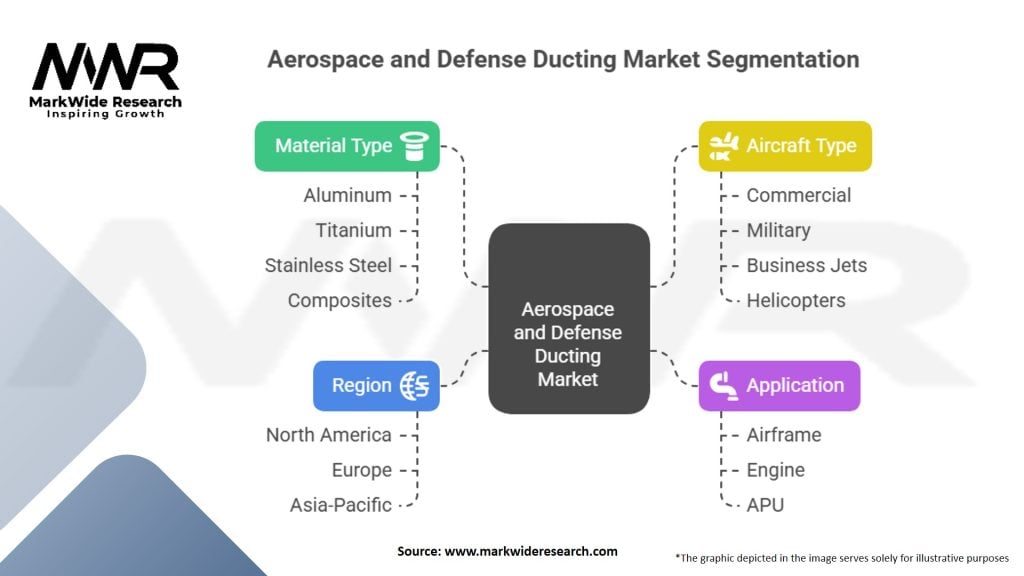

The aerospace and defense ducting market can be segmented based on product type, material type, application, and end-user.

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Market Key Trends

Covid-19 Impact

The aerospace and defense industry, including the ducting market, experienced a significant impact due to the COVID-19 pandemic. The pandemic led to a sharp decline in air travel demand, resulting in reduced aircraft production rates and deferred fleet expansion plans. Supply chain disruptions, factory closures, and travel restrictions also affected the industry’s operations. However, the market showed resilience, with governments providing support to the aerospace sector and a gradual recovery expected as air travel resumes.

Key Industry Developments

Analyst Suggestions

Future Outlook

The aerospace and defense ducting market is expected to witness steady growth in the coming years. Factors such as increasing aircraft production, the emphasis on lightweight and high-performance solutions, technological advancements, and the growing defense expenditure will drive market expansion. The market will continue to evolve with the adoption of new materials, manufacturing techniques, and smart technologies. Emerging trends, such as electric aircraft and additive manufacturing, will create new opportunities for industry participants. However, companies need to navigate challenges related to costs, certifications, and environmental regulations to sustain their growth in a highly competitive landscape.

Conclusion

The aerospace and defense ducting market plays a vital role in ensuring the efficient operation and safety of aircraft and defense systems. The market is driven by the demand for lightweight and high-performance ducting solutions that meet stringent industry requirements. Despite challenges such as high costs, complex certifications, and supply chain disruptions, the market offers opportunities in emerging sectors, additive manufacturing, and aftermarket services. Manufacturers need to invest in R&D, focus on lightweight materials, strengthen partnerships, adapt to regulations, and enhance supply chain resilience to capitalize on the market’s potential. The future outlook for the market is positive, with steady growth expected in the coming years, driven by increasing aircraft production, technological advancements, and defense modernization initiatives.

What is Aerospace and Defense Ducting?

Aerospace and Defense Ducting refers to the systems used for the transportation of air, fluids, and gases in aircraft and defense equipment. These ducting systems are crucial for maintaining environmental control, cooling, and structural integrity in aerospace applications.

What are the key players in the Aerospace and Defense Ducting Market?

Key players in the Aerospace and Defense Ducting Market include companies like Zodiac Aerospace, Meggitt PLC, and Parker Hannifin. These companies are known for their innovative ducting solutions and extensive experience in aerospace applications, among others.

What are the growth factors driving the Aerospace and Defense Ducting Market?

The growth of the Aerospace and Defense Ducting Market is driven by increasing demand for lightweight materials, advancements in aerospace technology, and the expansion of defense budgets globally. Additionally, the rise in air travel and the need for efficient thermal management systems contribute to market growth.

What challenges does the Aerospace and Defense Ducting Market face?

The Aerospace and Defense Ducting Market faces challenges such as stringent regulatory requirements, high manufacturing costs, and the need for continuous innovation. These factors can hinder the development and adoption of new ducting technologies in the industry.

What opportunities exist in the Aerospace and Defense Ducting Market?

Opportunities in the Aerospace and Defense Ducting Market include the development of advanced composite materials and the integration of smart technologies for better performance. Additionally, the increasing focus on sustainability and eco-friendly solutions presents new avenues for growth.

What trends are shaping the Aerospace and Defense Ducting Market?

Current trends in the Aerospace and Defense Ducting Market include the shift towards lightweight and durable materials, the use of additive manufacturing for ducting components, and the growing emphasis on energy efficiency. These trends are influencing product development and design strategies in the sector.

Aerospace and Defense Ducting Market

| Segmentation Details | Description |

|---|---|

| Material Type | Aluminum, Titanium, Stainless Steel, Composites, Others |

| Application | Airframe, Engine, APU (Auxiliary Power Unit), Others |

| Aircraft Type | Commercial, Military, Business Jets, Helicopters, Others |

| Region | Global |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in Aerospace and Defense Ducting Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA