Rural banking plays a vital role in providing financial services to the rural population and fostering economic development in rural areas. It encompasses various financial institutions and services designed to cater to the unique needs and challenges faced by rural communities. These services include savings accounts, loans, insurance, and other banking products tailored specifically for the rural population. The rural banking market is driven by the goal of financial inclusion, ensuring that individuals in remote and underdeveloped areas have access to formal banking services. This article provides a comprehensive analysis of the rural banking market, including its meaning, key insights, market drivers, restraints, opportunities, dynamics, regional analysis, competitive landscape, segmentation, industry trends, and future outlook.

Meaning

Rural banking refers to the provision of financial services in rural areas, typically characterized by low population density, limited infrastructure, and agricultural-based economies. The primary objective of rural banking is to ensure that individuals and communities in these areas have access to affordable and convenient banking services. It aims to bridge the gap between urban and rural areas in terms of financial inclusion and economic development. Rural banking institutions, such as rural banks, credit unions, and microfinance institutions, offer a range of financial products and services tailored to meet the unique needs of rural customers.

Executive Summary

The rural banking market is witnessing significant growth due to the increasing focus on financial inclusion and rural development. Governments, central banks, and financial institutions worldwide are recognizing the importance of providing banking services to rural areas to promote economic growth and reduce poverty. The market is characterized by the expansion of banking infrastructure, the introduction of innovative technology solutions, and the development of tailored financial products for the rural population. However, challenges such as limited connectivity, low literacy rates, and inadequate awareness of financial services still persist. Overcoming these challenges and leveraging the untapped potential of rural markets will be key to the future success of the rural banking sector.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

The rural banking market is driven by the need to address the financial exclusion of rural communities and promote economic development.

Governments and regulatory bodies are implementing initiatives and policies to encourage rural banking and financial inclusion.

Technological advancements, particularly in mobile banking and digital payment solutions, are transforming the rural banking landscape.

The agricultural sector plays a significant role in rural banking, with loans and financing options tailored to meet the needs of farmers and agribusinesses.

Collaborations between financial institutions and government agencies are essential for expanding rural banking services and reaching underserved communities.

Market Drivers

Several factors are driving the growth of the rural banking market:

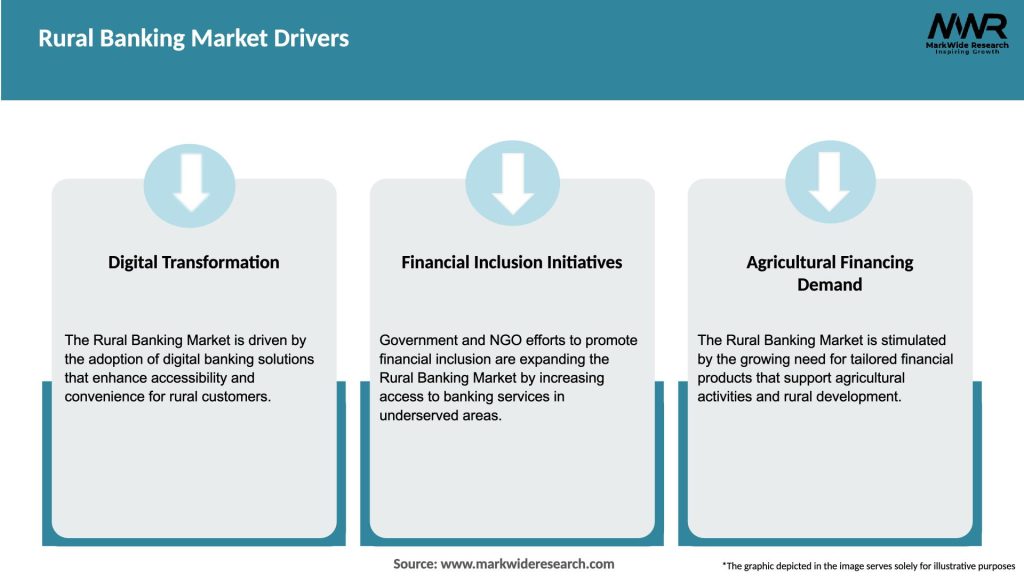

Financial Inclusion Initiatives: Governments and regulatory authorities are actively promoting financial inclusion and rural development by encouraging the expansion of banking services in rural areas. This has led to the establishment of rural banking institutions and the adoption of policies that support affordable and accessible financial services.

Technological Advancements: The advancement of technology, particularly in mobile banking and digital payment solutions, has revolutionized the rural banking landscape. Mobile banking allows individuals in remote areas to access banking services through their mobile phones, eliminating the need for physical branches.

Agricultural Sector Growth: The agricultural sector is a significant driver of the rural banking market. With specialized loan products, insurance schemes, and financing options tailored for farmers and agribusinesses, rural banks play a crucial role in supporting the growth and development of the agricultural sector.

Government Support: Governments provide financial support and incentives to rural banks, credit unions, and microfinance institutions to expand their operations in rural areas. These initiatives aim to enhance financial services and stimulate economic growth in underserved regions.

Market Restraints

Despite the growth potential, the rural banking market faces certain challenges:

Limited Connectivity: Many rural areas lack reliable internet connectivity and communication infrastructure, making it difficult for rural banks to provide digital banking services. This poses a significant obstacle to expanding financial inclusion in remote regions.

Low Awareness and Financial Literacy: Rural communities often have lower levels of financial literacy and awareness compared to urban areas. Educating the rural population about the benefits and usage of banking services is crucial for driving adoption and usage.

Infrastructure and Logistic Challenges: Rural areas may face inadequate transportation and logistical infrastructure, making it challenging for financial institutions to establish physical branches and deliver banking services effectively.

Credit Risks and Limited Collateral: The agriculture-based economies prevalent in many rural areas pose unique credit risks for rural banks. Limited collateral availability and income volatility of farmers and rural entrepreneurs can affect loan repayment rates and profitability.

Market Opportunities

The rural banking market presents several opportunities for growth and expansion:

Digital Transformation: Investing in digital banking solutions can significantly enhance the reach and efficiency of rural banking services. Mobile banking apps, online payment platforms, and digital loan processing systems can help overcome the challenges of limited physical infrastructure.

Product Diversification: Rural banks can explore opportunities to diversify their product offerings beyond traditional banking services. For example, offering microinsurance products tailored for the agricultural sector or introducing savings schemes specific to the needs of rural customers.

Collaborations and Partnerships: Collaborations between rural banks, government agencies, and development organizations can leverage their respective strengths to address the challenges of rural banking. Such partnerships can facilitate the sharing of resources, knowledge, and expertise.

Focus on Financial Literacy: Enhancing financial literacy among rural communities is crucial for promoting the usage of banking services and fostering trust in formal financial institutions. Investing in financial education programs can empower individuals to make informed financial decisions.

Market Dynamics

The rural banking market is characterized by dynamic factors that shape its growth and development:

Changing Regulatory Landscape: Regulatory policies and initiatives play a significant role in shaping the rural banking market. Governments and central banks introduce regulations and incentives to encourage rural banking, support financial inclusion, and ensure consumer protection.

Technological Advancements: Technological innovations continue to disrupt the rural banking sector. Mobile banking, biometric authentication, and digital payment solutions enable financial institutions to provide convenient and accessible services to rural customers.

Customer Demands and Expectations: The evolving needs and expectations of rural customers influence the development of banking products and services. Understanding the unique requirements of rural communities and tailoring offerings accordingly is essential for market growth.

Economic and social Factors: Economic conditions, agricultural productivity, and social factors such as population growth and migration patterns impact the demand for rural banking services. Economic fluctuations and changing demographics can influence the market dynamics.

Regional Analysis

The rural banking market varies across different regions due to variations in economic development, cultural factors, and government policies. In developed economies, rural banking services are well-established and supported by comprehensive financial infrastructure. Conversely, in developing economies, rural banking may still be in its early stages, with limited accessibility and awareness. Factors such as population density, agricultural activities, and geographical characteristics also influence the regional dynamics of the rural banking market.

Competitive Landscape

Leading Companies in the Rural Banking Market:

National Bank for Agriculture and Rural Development (NABARD)

Bharatiya Mahila Bank (Now merged with State Bank of India)

The Kangra Central Cooperative Bank Ltd.

Bandhan Bank Ltd.

Rabobank

Grameen Bank

CRDB Bank Plc

Rural Development Bank Ltd.

Agribank

BRAC Bank Limited

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

The rural banking market can be segmented based on various criteria, including:

Type of Institution: This includes rural banks, credit unions, microfinance institutions, and other financial service providers catering to rural areas.

Banking Services: Segmentation can be done based on the types of banking services offered, such as savings accounts, loans, insurance, remittances, and payment solutions.

Geographic Regions: The market can be segmented based on different geographical regions or countries, considering the specific characteristics and requirements of each area.

Category-wise Insights

Savings Accounts: Rural banks offer savings accounts tailored to the needs of rural customers, often with lower minimum balance requirements and simplified account opening procedures.

Agricultural Loans: Agriculture plays a crucial role in rural economies, and rural banks provide specialized agricultural loans to farmers for crop cultivation, livestock rearing, farm equipment purchases, and other agricultural activities.

Microfinance Services: Microfinance institutions operating in rural areas provide small loans, typically without collateral requirements, to micro-entrepreneurs and self-help groups. These loans empower rural individuals to start or expand small businesses.

Remittances and Payment Solutions: Rural banking services include remittance services that allow rural residents to receive funds from family members working in urban areas. Additionally, payment solutions, such as mobile banking and digital wallets, facilitate convenient transactions for rural customers.

Key Benefits for Industry Participants and Stakeholders

Industry participants and stakeholders involved in the rural banking market can benefit in several ways:

Market Expansion: Rural banking offers an opportunity for financial institutions to expand their customer base and geographical reach, tapping into underserved rural markets.

Social Impact: By providing banking services to rural communities, industry participants contribute to financial inclusion, poverty reduction, and overall rural development.

Revenue Generation: Rural banking can generate sustainable revenue streams for financial institutions through the provision of various banking products and services tailored to the needs of rural customers.

Collaboration Opportunities: Collaborations with government agencies, development organizations, and other stakeholders can lead to knowledge sharing, resource pooling, and increased market penetration.

SWOT Analysis

A SWOT analysis of the rural banking market provides insights into its strengths, weaknesses, opportunities, and threats:

Strengths:

Strong focus on financial inclusion and rural development.

Tailored financial products and services for rural customers.

Potential for market expansion and revenue growth.

Weaknesses:

Limited infrastructure and connectivity in rural areas.

Low levels of financial literacy and awareness among rural communities.

Credit risks associated with agricultural lending.

Opportunities:

Technological advancements enabling digital banking solutions.

Collaboration and partnerships to leverage resources and expertise.

Diversification of product offerings to cater to specific rural needs.

Threats:

Competition from informal financial service providers.

Economic fluctuations affecting the demand for banking services.

Regulatory challenges and compliance requirements.

Market Key Trends

Several key trends are shaping the rural banking market:

Digital Transformation: The integration of technology, particularly mobile banking and digital payment solutions, is transforming the rural banking landscape. Digital channels enable remote access to banking services and provide cost-effective solutions for financial institutions.

Data Analytics and AI: The use of data analytics and artificial intelligence allows rural banks to gain valuable insights into customer behavior, improve risk assessment, and enhance operational efficiency.

Customer-Centric Approach: Rural banks are adopting a customer-centric approach by customizing their products and services to meet the unique needs of rural customers. This includes the development of tailored loan products, insurance schemes, and savings options.

Sustainable Finance: There is an increasing emphasis on sustainable finance in the rural banking sector. Banks are incorporating environmental and social factors into their lending decisions, promoting environmentally friendly practices, and supporting sustainable agricultural initiatives.

Covid-19 Impact

The COVID-19 pandemic has had both immediate and long-term impacts on the rural banking market:

Immediate Impact: The pandemic disrupted the normal functioning of rural banking operations, particularly physical branch services. Lockdowns and restrictions limited customer access to banking services, leading to a greater reliance on digital channels.

Digital Transformation: The pandemic accelerated the adoption of digital banking solutions in rural areas. Banks and financial institutions swiftly implemented mobile banking, online payment, and digital loan processing to ensure uninterrupted services.

Economic Challenges: The pandemic resulted in economic challenges for rural communities, affecting the income and livelihoods of rural customers. Rural banks played a crucial role in providing financial assistance, loan restructuring, and support to affected individuals and businesses.

Policy Reforms: Governments and regulatory bodies introduced policy reforms and stimulus measures to mitigate the impact of the pandemic on rural communities. These measures included loan moratoriums, interest rate reductions, and financial support programs.

Key Industry Developments

Key industry developments in the rural banking market include:

Collaboration with Fintech Startups: Rural banks are partnering with fintech startups to leverage innovative technology solutions, expand their service offerings, and enhance customer experience.

Expansion of Digital Banking Services: Rural banks are investing in digital banking infrastructure, including mobile banking apps, online platforms, and digital payment solutions, to reach underserved rural customers.

Government Support and Incentives: Governments are introducing policies, incentives, and subsidies to promote rural banking and financial inclusion. These initiatives encourage financial institutions to expand their presence in rural areas.

Sustainable Finance Initiatives: Rural banks are adopting sustainable finance practices, promoting responsible lending, and supporting environmentally friendly agricultural practices in line with global sustainability goals.

Analyst Suggestions

Based on the analysis of the rural banking market, analysts suggest the following strategies for industry participants:

Embrace Digital Transformation: Invest in digital banking solutions to enhance accessibility and convenience for rural customers. Focus on mobile banking, online platforms, and digital payment solutions to overcome infrastructure challenges.

Strengthen Financial Literacy: Develop financial education programs to improve financial literacy and awareness among rural communities. Educate customers about the benefits and usage of banking services to drive adoption and usage.

Collaborate for Market Expansion: Collaborate with government agencies, development organizations, and fintech startups to expand market reach and leverage resources. Partnerships can enable knowledge sharing, innovation, and the provision of comprehensive financial solutions.

Customized Product Offerings: Develop tailored financial products and services that cater to the specific needs of rural customers. Customize loan products, insurance schemes, and savings options to address the unique challenges and opportunities in rural areas.

Future Outlook

The future of the rural banking market is promising, with several trends and factors driving its growth:

Technological Advancements: Ongoing technological advancements, including the proliferation of smartphones and improved connectivity in rural areas, will continue to revolutionize the rural banking landscape. Digital banking solutions will become increasingly prevalent.

Financial Inclusion as a Priority: Financial inclusion will remain a top priority for governments and regulatory bodies worldwide. Continued support and incentives will encourage financial institutions to expand their operations in rural areas and provide accessible banking services.

Sustainable and Responsible Banking: The focus on sustainability and responsible banking practices will intensify. Rural banks will adopt environmental and social factors into their lending decisions and support initiatives that promote sustainable agriculture and rural development.

Data-driven Decision-making: The use of data analytics and artificial intelligence will play a crucial role in improving risk assessment, customer segmentation, and decision-making processes. Rural banks will harness data to enhance operational efficiency and customer experience.

Conclusion

The rural banking market holds significant potential for driving financial inclusion, economic development, and poverty reduction in rural areas. Governments, financial institutions, and stakeholders must work together to overcome challenges such as limited connectivity, low financial literacy, and credit risks. By embracing digital transformation, customizing products and services, and fostering collaborations, the rural banking sector can unlock opportunities for growth and provide accessible and tailored financial services to rural communities. The future outlook is optimistic, with technology advancements and sustainable finance driving the market towards a more inclusive and prosperous rural economy.

What is Rural Banking?

Rural Banking refers to financial services specifically designed to meet the needs of rural populations. It includes services such as savings accounts, loans, and insurance tailored for agricultural and rural development.

What are the key players in the Rural Banking Market?

Key players in the Rural Banking Market include institutions like Grameen Bank, NABARD, and various cooperative banks that focus on providing financial services to rural communities, among others.

What are the main drivers of growth in the Rural Banking Market?

The main drivers of growth in the Rural Banking Market include increasing financial inclusion, the rise of digital banking solutions, and government initiatives aimed at supporting rural development.

What challenges does the Rural Banking Market face?

Challenges in the Rural Banking Market include limited infrastructure, low financial literacy among rural populations, and high operational costs for banks serving remote areas.

What opportunities exist in the Rural Banking Market?

Opportunities in the Rural Banking Market include the expansion of mobile banking services, partnerships with fintech companies, and the potential for microfinance to empower rural entrepreneurs.

What trends are shaping the Rural Banking Market?

Trends shaping the Rural Banking Market include the adoption of technology for better service delivery, increased focus on sustainable financing, and the growing importance of customer-centric banking solutions.

National Bank for Agriculture and Rural Development (NABARD)

Bharatiya Mahila Bank (Now merged with State Bank of India)

The Kangra Central Cooperative Bank Ltd.

Bandhan Bank Ltd.

Rabobank

Grameen Bank

CRDB Bank Plc

Rural Development Bank Ltd.

Agribank

BRAC Bank Limited

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.