444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The global semiconductor packaging and assembly equipment market is a thriving sector within the semiconductor industry. It plays a crucial role in the production and assembly of semiconductor chips, which are essential components of various electronic devices. This market encompasses a wide range of equipment and technologies used for packaging and assembling semiconductor chips, including die attach, wire bonding, encapsulation, and testing equipment.

Meaning

Semiconductor packaging and assembly equipment refer to the machinery, tools, and processes involved in the packaging and assembly of semiconductor chips. Packaging is the final stage of semiconductor manufacturing, where the chips are encapsulated to protect them from external factors such as moisture, temperature variations, and physical damage. Assembly, on the other hand, involves connecting the packaged chips to other electronic components, such as circuit boards or substrates, to form a complete electronic device.

Executive Summary

The global semiconductor packaging and assembly equipment market has witnessed significant growth in recent years, driven by the rising demand for advanced electronic devices across various industries. The increasing complexity and miniaturization of semiconductor chips have fueled the need for highly efficient and precise packaging and assembly equipment. Additionally, technological advancements in semiconductor packaging techniques, such as 3D packaging and wafer-level packaging, have further contributed to the market’s growth.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

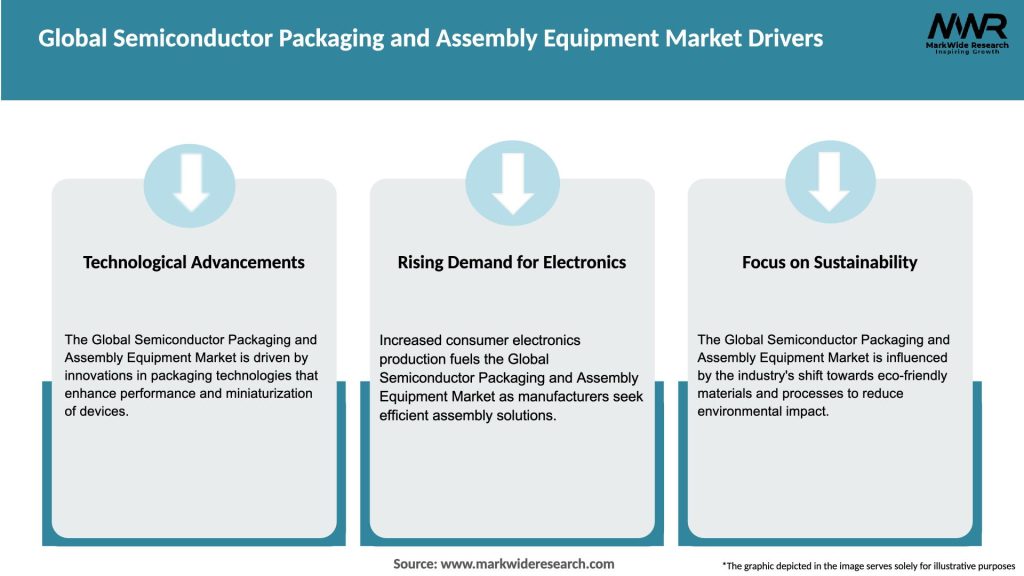

Market Drivers

Several key factors are driving the growth of the global semiconductor packaging and assembly equipment market:

Market Restraints

Despite the positive growth prospects, the global semiconductor packaging and assembly equipment market faces certain challenges:

Market Opportunities

The global semiconductor packaging and assembly equipment market presents several opportunities for growth and innovation:

Market Dynamics

The global semiconductor packaging and assembly equipment market is influenced by various dynamic factors:

Regional Analysis

The global semiconductor packaging and assembly equipment market is segmented into several key regions:

Competitive Landscape

Leading Companies in the Global Semiconductor Packaging and Assembly Equipment Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

The global semiconductor packaging and assembly equipment market can be segmented based on equipment type, packaging technology, end-user industry, and region:

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

A SWOT analysis of the global semiconductor packaging and assembly equipment market provides insights into the industry’s strengths, weaknesses, opportunities, and threats:

Market Key Trends

The global semiconductor packaging and assembly equipment market is witnessing several key trends:

Covid-19 Impact

The global semiconductor packaging and assembly equipment market experienced a temporary setback due to the Covid-19 pandemic. The initial disruptions in the supply chain, manufacturing operations, and global trade impacted the market’s growth. However, the semiconductor industry quickly recovered due to the increased demand for electronic devices, including laptops, gaming consoles, and medical equipment, during lockdowns and remote working scenarios.

The pandemic highlighted the importance of reliable supply chains and accelerated the digital transformation across various industries. The demand for semiconductor chips used in data centers, cloud computing, and communication infrastructure increased significantly. This drove the need for advanced packaging and assembly equipment to support the production of these critical components.

The semiconductor industry adapted to the new normal by implementing safety measures, adopting remote work practices, and ensuring business continuity. The market witnessed increased investments in automation, robotics, and advanced manufacturing technologies to improve efficiency and reduce dependence on manual labor.

Key Industry Developments

Analyst Suggestions

Future Outlook

The global semiconductor packaging and assembly equipment market is poised for significant growth in the coming years. The increasing demand for advanced electronic devices, the proliferation of IoT devices, the expansion of 5G networks, and the adoption of electric vehicles will drive the market’s expansion.

Technological advancements in packaging techniques, materials, and equipment will continue to shape the industry. The development of heterogeneous integration, advanced interconnect technologies, and eco-friendly packaging solutions will open new avenues for growth.

Companies that focus on innovation, strategic collaborations, and sustainability will be well-positioned to capture market opportunities. Moreover, continued investments in research and development, workforce development, and automation will be crucial for staying competitive in the dynamic semiconductor packaging and assembly equipment market.

Conclusion

The global semiconductor packaging and assembly equipment market is witnessing robust growth, driven by the increasing demand for advanced electronic devices, miniaturization of semiconductor chips, and technological advancements in packaging techniques. Despite challenges such as high costs, skill requirements, and environmental concerns, the market presents ample opportunities for innovation and expansion.

With the adoption of advanced packaging technologies, strategic collaborations, and a focus on sustainability, companies can thrive in this competitive landscape. The future outlook for the market remains optimistic, fueled by the growing electronics industry, emerging technologies, and evolving consumer demands.

What is Semiconductor Packaging and Assembly Equipment?

Semiconductor Packaging and Assembly Equipment refers to the tools and machinery used in the packaging and assembly processes of semiconductor devices. This includes equipment for die bonding, wire bonding, and encapsulation, which are essential for protecting and connecting semiconductor chips.

What are the key players in the Global Semiconductor Packaging and Assembly Equipment Market?

Key players in the Global Semiconductor Packaging and Assembly Equipment Market include companies like ASM International, Tokyo Electron, and Applied Materials, among others. These companies are known for their innovative technologies and extensive product offerings in semiconductor manufacturing.

What are the main drivers of growth in the Global Semiconductor Packaging and Assembly Equipment Market?

The growth of the Global Semiconductor Packaging and Assembly Equipment Market is driven by the increasing demand for advanced semiconductor devices in consumer electronics, automotive applications, and IoT devices. Additionally, the trend towards miniaturization and higher performance in electronics is fueling the need for advanced packaging solutions.

What challenges does the Global Semiconductor Packaging and Assembly Equipment Market face?

The Global Semiconductor Packaging and Assembly Equipment Market faces challenges such as the high cost of advanced packaging technologies and the complexity of manufacturing processes. Additionally, supply chain disruptions and the need for skilled labor can hinder market growth.

What opportunities exist in the Global Semiconductor Packaging and Assembly Equipment Market?

Opportunities in the Global Semiconductor Packaging and Assembly Equipment Market include the growing adoption of 5G technology and the expansion of artificial intelligence applications. These trends are expected to drive demand for more sophisticated packaging solutions that enhance performance and efficiency.

What are the current trends in the Global Semiconductor Packaging and Assembly Equipment Market?

Current trends in the Global Semiconductor Packaging and Assembly Equipment Market include the shift towards heterogeneous integration and the development of advanced materials for packaging. Additionally, there is a growing focus on sustainability and reducing the environmental impact of semiconductor manufacturing processes.

Global Semiconductor Packaging and Assembly Equipment Market

| Segmentation | Details |

|---|---|

| By Equipment Type | Die Bonding Equipment, Wire Bonding Equipment, Packaging Equipment, Others |

| By Packaging Technology | Flip-Chip, Fan-Out, Wafer-Level Packaging, Others |

| By Region | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the Global Semiconductor Packaging and Assembly Equipment Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA