444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Russia car rentals market represents a dynamic and evolving sector within the country’s transportation and tourism industry. This market encompasses various vehicle rental services, from short-term tourist rentals to long-term corporate leasing solutions across Russia’s vast geographical landscape. Market dynamics indicate substantial growth potential driven by increasing domestic tourism, business travel recovery, and evolving consumer preferences toward flexible mobility solutions.

Regional distribution shows concentrated activity in major metropolitan areas including Moscow, St. Petersburg, and key tourist destinations along the Trans-Siberian route. The market demonstrates resilience despite economic challenges, with local operators adapting to changing consumer demands and technological advancements. Growth projections suggest the sector will expand at a compound annual growth rate of 8.2% over the forecast period, driven by digital transformation and improved service offerings.

Consumer behavior patterns reveal shifting preferences toward contactless rental processes, flexible booking options, and diverse vehicle categories. The market serves multiple segments including leisure travelers, business professionals, and local residents seeking temporary transportation solutions. Technology adoption has accelerated significantly, with mobile applications and digital platforms becoming primary booking channels for approximately 67% of rental transactions.

The Russia car rentals market refers to the comprehensive ecosystem of vehicle rental services operating throughout the Russian Federation, encompassing short-term and long-term rental solutions for various customer segments. This market includes traditional car rental companies, peer-to-peer sharing platforms, corporate fleet services, and specialized vehicle rental providers serving both domestic and international customers across Russia’s diverse regions.

Service categories within this market range from economy vehicle rentals for budget-conscious travelers to luxury car rentals for premium customers, along with specialized vehicles for specific purposes such as winter driving conditions or off-road adventures. The market definition also encompasses emerging mobility solutions including electric vehicle rentals and subscription-based car access services that cater to evolving transportation preferences in urban and rural areas.

Market fundamentals demonstrate robust growth potential within Russia’s car rental sector, supported by recovering tourism activities, increased business travel, and growing acceptance of shared mobility concepts. The market exhibits strong regional variations, with Moscow and St. Petersburg commanding significant market shares while emerging opportunities develop in secondary cities and tourist destinations.

Key performance indicators reveal positive trends across multiple metrics, including customer satisfaction rates exceeding 78% and digital booking adoption reaching new highs. The competitive landscape features both international operators and strong domestic players, creating a diverse service ecosystem that caters to various customer preferences and budget requirements.

Strategic developments include significant investments in fleet modernization, technology infrastructure, and customer experience enhancement. Market participants are increasingly focusing on sustainability initiatives, with electric and hybrid vehicles representing a growing portion of rental fleets. Future prospects indicate continued expansion opportunities, particularly in underserved regions and emerging mobility segments.

Primary market drivers include the following critical factors shaping industry development:

Market segmentation reveals distinct customer categories with varying needs, preferences, and spending patterns. Understanding these segments enables rental companies to develop targeted service offerings and pricing strategies that maximize market penetration and customer satisfaction.

Tourism sector recovery serves as a fundamental driver for Russia’s car rental market, with domestic travel showing particularly strong growth patterns. The resurgence of leisure travel, combined with increased interest in exploring Russia’s diverse regions, creates sustained demand for rental vehicles across multiple destinations. Seasonal tourism patterns generate predictable demand cycles that enable rental companies to optimize fleet management and pricing strategies.

Business travel normalization contributes significantly to market growth, as corporate activities resume and companies seek flexible transportation solutions for their employees. The trend toward hybrid work arrangements has created new demand patterns, with some businesses preferring rental solutions over maintaining corporate fleets. Corporate partnerships with rental companies have increased by approximately 34% as organizations prioritize cost-effective mobility solutions.

Digital adoption acceleration transforms customer interactions and operational processes throughout the rental ecosystem. Mobile applications, contactless pickup procedures, and digital payment systems enhance convenience while reducing operational costs. Technology integration enables rental companies to offer personalized services, dynamic pricing, and improved customer support, driving market expansion and customer loyalty.

Infrastructure development across Russia’s regions improves accessibility and creates new market opportunities for rental operators. Enhanced road networks, airport expansions, and tourism facility developments support market growth by making previously remote destinations more accessible to travelers requiring rental vehicles.

Economic volatility presents ongoing challenges for Russia’s car rental market, affecting both consumer spending patterns and operational costs for rental companies. Currency fluctuations impact vehicle procurement costs, particularly for international brands, while economic uncertainty influences consumer discretionary spending on travel and transportation services.

Regulatory complexities create operational challenges for rental companies, particularly regarding cross-border travel restrictions, documentation requirements, and varying regional regulations. Compliance costs and administrative burdens can limit market entry for smaller operators while creating operational inefficiencies for established companies.

Seasonal demand fluctuations pose significant challenges for fleet utilization and revenue optimization. The concentration of tourism activities during specific periods creates capacity management difficulties, with rental companies struggling to balance fleet sizes against varying seasonal demand patterns. Utilization rates can drop to as low as 45% during off-peak periods, impacting profitability.

Competition from alternative transportation modes, including ride-sharing services, public transportation improvements, and car-sharing platforms, creates market pressure on traditional rental models. These alternatives often provide more convenient or cost-effective solutions for specific use cases, requiring rental companies to differentiate their value propositions.

Electric vehicle integration presents substantial growth opportunities as Russia develops its electric vehicle infrastructure and environmental awareness increases among consumers. Rental companies can position themselves as early adopters of sustainable transportation solutions while benefiting from government incentives and evolving consumer preferences toward environmentally friendly options.

Regional market expansion offers significant potential for rental companies willing to invest in underserved areas. Many secondary cities and tourist destinations lack adequate rental services, creating opportunities for both established operators and new market entrants to capture untapped demand.

Corporate mobility solutions represent a growing opportunity as businesses seek flexible alternatives to traditional fleet ownership. Subscription-based models, long-term rental agreements, and comprehensive mobility packages can generate stable revenue streams while meeting evolving corporate transportation needs.

Technology-enabled services create opportunities for differentiation and market expansion through innovative customer experiences. Advanced booking systems, predictive maintenance, IoT-enabled vehicles, and personalized service offerings can enhance customer satisfaction while improving operational efficiency.

Partnership development with tourism operators, hotels, airlines, and other travel service providers can create integrated mobility solutions that enhance customer convenience while expanding market reach. Strategic alliances can provide access to new customer segments and distribution channels.

Supply and demand equilibrium in Russia’s car rental market reflects complex interactions between seasonal tourism patterns, business travel cycles, and economic conditions. Market participants must navigate fluctuating demand while maintaining adequate fleet capacity to serve peak periods effectively. Demand elasticity varies significantly across customer segments, with leisure travelers showing higher price sensitivity compared to business customers.

Competitive intensity continues to increase as both domestic and international operators vie for market share across different segments and regions. Price competition remains significant in economy segments, while premium and specialty vehicle categories offer better margin opportunities. Market consolidation trends suggest that larger operators are acquiring smaller regional players to expand geographic coverage and achieve operational efficiencies.

Technology disruption reshapes traditional rental models through digital platforms, automated processes, and data-driven decision making. Companies investing in technology infrastructure gain competitive advantages through improved customer experiences, operational efficiency, and market responsiveness. Digital transformation initiatives have improved operational efficiency by approximately 28% among leading market participants.

Customer expectations evolution drives continuous service improvements and innovation throughout the rental ecosystem. Modern consumers demand seamless digital experiences, flexible booking options, transparent pricing, and high-quality vehicles, forcing rental companies to continuously upgrade their service offerings and operational capabilities.

Primary research methodologies employed in analyzing Russia’s car rental market include comprehensive surveys of rental operators, customer interviews, and industry expert consultations. These approaches provide direct insights into market conditions, competitive dynamics, and emerging trends affecting industry development.

Secondary research sources encompass industry reports, government statistics, tourism data, and economic indicators relevant to transportation and travel sectors. Analysis of publicly available information from rental companies, industry associations, and regulatory bodies provides additional context for market assessment.

Data validation processes ensure accuracy and reliability through cross-referencing multiple sources, statistical verification, and expert review procedures. Quantitative analysis combines with qualitative insights to provide comprehensive market understanding and reliable forecasting capabilities.

Market segmentation analysis utilizes demographic data, geographic information, and behavioral patterns to identify distinct customer groups and market opportunities. This approach enables detailed assessment of market potential across different segments and regions within Russia’s diverse market landscape.

Moscow metropolitan area dominates Russia’s car rental market, accounting for approximately 42% of total market activity. The capital region benefits from high business travel volumes, international tourism, and strong economic activity that supports premium rental services. Corporate demand remains particularly strong in Moscow, with business travelers requiring reliable transportation solutions for meetings, conferences, and client visits.

St. Petersburg region represents the second-largest market segment, driven by cultural tourism, business activities, and its role as a major transportation hub. The city’s historical attractions and business centers create consistent demand for rental vehicles throughout the year, though seasonal variations remain significant due to tourism patterns.

Sochi and southern regions demonstrate strong seasonal demand patterns aligned with tourism cycles and recreational activities. These areas experience peak demand during summer months and winter sports seasons, requiring rental companies to implement flexible fleet management strategies to optimize utilization rates.

Siberian markets present emerging opportunities as infrastructure development and regional economic growth create new demand for rental services. Cities like Novosibirsk, Yekaterinburg, and Irkutsk show increasing rental activity, though market penetration remains relatively low compared to western regions.

Far East territories represent frontier markets with significant growth potential, particularly in areas experiencing tourism development and business expansion. These regions require specialized service approaches due to geographic challenges and unique customer requirements.

Market leadership in Russia’s car rental sector features a mix of international operators and strong domestic companies, each with distinct competitive advantages and market positioning strategies. The competitive environment continues evolving as companies adapt to changing customer preferences and market conditions.

Competitive strategies focus on differentiation through service quality, technology integration, fleet diversity, and customer experience enhancement. Companies are investing in digital platforms, mobile applications, and automated processes to improve operational efficiency and customer satisfaction.

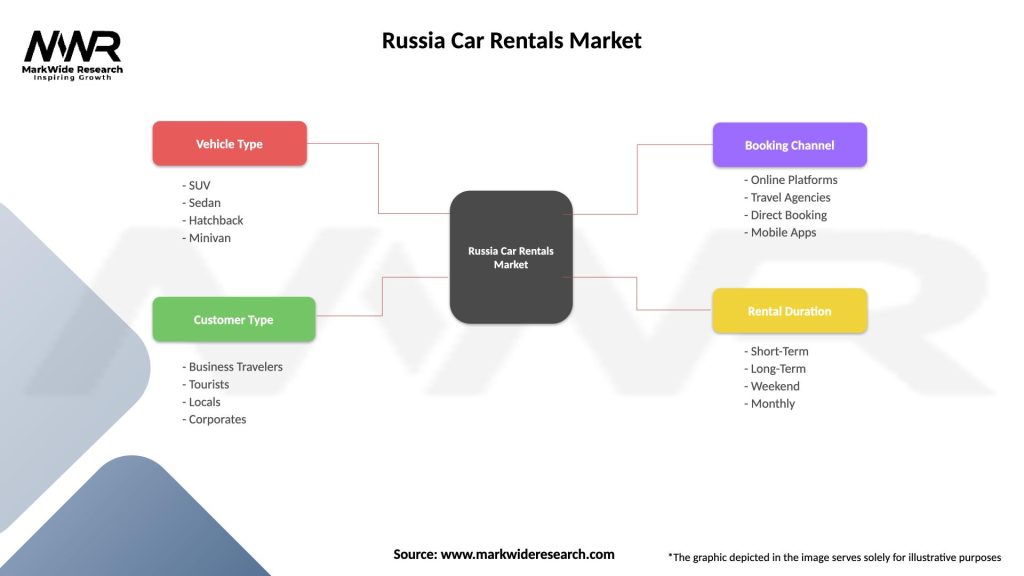

By vehicle type, the market demonstrates diverse preferences across different customer segments and use cases:

By customer type, distinct segments exhibit different behavior patterns and service requirements:

Short-term rentals dominate market volume, with daily and weekly rentals representing the core business model for most operators. This category serves diverse customer needs from airport pickups to vacation transportation, requiring efficient fleet turnover and comprehensive service networks. Average rental duration for leisure customers extends to 5.3 days, while business rentals typically last 2-3 days.

Long-term rentals provide stable revenue streams and higher customer lifetime value, appealing to customers requiring vehicles for extended periods. This segment includes corporate clients, temporary residents, and individuals awaiting vehicle purchases or repairs. Monthly and annual rental agreements offer predictable income while reducing fleet turnover costs.

Specialty vehicle rentals cater to specific customer requirements including winter-equipped vehicles, off-road capable SUVs, and luxury cars for special events. This high-margin segment requires specialized fleet management and targeted marketing approaches to reach appropriate customer segments.

One-way rentals address customer convenience needs while presenting operational challenges for fleet positioning and logistics. This service category supports tourism patterns and business travel requirements but requires sophisticated fleet management systems to optimize vehicle distribution.

Rental operators benefit from diversified revenue streams, scalable business models, and opportunities for technology-driven efficiency improvements. The market offers potential for geographic expansion, service diversification, and customer base growth through strategic investments and operational excellence.

Customers gain access to flexible transportation solutions without the commitments and costs associated with vehicle ownership. Benefits include access to diverse vehicle types, maintenance-free mobility, and convenient booking processes that enhance travel experiences and business operations.

Tourism industry stakeholders benefit from enhanced destination accessibility and visitor mobility options that support tourism development and economic growth. Car rental services complement other tourism infrastructure by enabling independent travel and exploration of diverse destinations.

Economic development receives support through job creation, tax revenue generation, and infrastructure utilization that contributes to regional economic growth. The rental industry creates employment opportunities across multiple skill levels while supporting related service sectors.

Environmental benefits emerge through improved vehicle utilization rates, newer fleet technologies, and reduced individual vehicle ownership needs. Shared mobility concepts contribute to more efficient transportation systems and reduced environmental impact per trip.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital transformation acceleration continues reshaping customer interactions and operational processes throughout the rental ecosystem. Mobile applications, contactless services, and automated systems become standard expectations rather than competitive advantages. Digital booking penetration has reached 73% of all rental transactions, demonstrating the critical importance of technology infrastructure.

Sustainability initiatives gain momentum as environmental consciousness increases among consumers and businesses. Rental companies are expanding electric and hybrid vehicle offerings while implementing carbon offset programs and sustainable operational practices. This trend aligns with broader environmental goals and regulatory developments promoting cleaner transportation.

Flexible service models emerge to meet evolving customer preferences for convenience and customization. Subscription-based rentals, hourly options, and integrated mobility packages provide alternatives to traditional daily rental models. These innovations address changing urban mobility patterns and customer lifestyle preferences.

Partnership ecosystem development creates integrated travel and mobility solutions through collaborations with airlines, hotels, tourism operators, and technology platforms. These strategic alliances enhance customer convenience while expanding market reach and revenue opportunities for rental operators.

Data-driven decision making becomes increasingly sophisticated as companies leverage analytics for pricing optimization, fleet management, and customer experience enhancement. Predictive analytics and machine learning applications improve operational efficiency while enabling personalized service delivery.

Fleet electrification initiatives represent major industry developments as rental companies begin incorporating electric vehicles into their offerings. These investments demonstrate commitment to sustainability while positioning companies for future regulatory requirements and customer preferences. Early adopters gain competitive advantages in environmentally conscious market segments.

Technology platform upgrades continue across the industry as companies invest in modern booking systems, mobile applications, and customer management platforms. These developments improve operational efficiency while enhancing customer experiences through streamlined processes and personalized services.

Market consolidation activities include acquisitions and partnerships as companies seek to expand geographic coverage, achieve operational efficiencies, and strengthen competitive positions. Strategic combinations enable resource sharing and market expansion while improving service capabilities.

Service diversification efforts expand beyond traditional car rentals to include comprehensive mobility solutions, corporate services, and specialized vehicle categories. These developments address evolving customer needs while creating new revenue streams and market opportunities.

Infrastructure investments in pickup locations, service centers, and technology systems support market expansion and service quality improvements. Companies are establishing presence in new markets while upgrading existing facilities to meet growing customer expectations.

Strategic positioning recommendations emphasize the importance of technology investment, customer experience enhancement, and market differentiation strategies. According to MarkWide Research analysis, companies should prioritize digital transformation initiatives while maintaining focus on service quality and operational efficiency to achieve sustainable competitive advantages.

Market expansion strategies should consider regional opportunities in underserved areas while building strategic partnerships with tourism and business service providers. Selective geographic expansion combined with service diversification can create sustainable growth opportunities while managing operational risks.

Fleet optimization approaches require sophisticated demand forecasting and dynamic pricing strategies to maximize utilization rates and profitability. Companies should invest in analytics capabilities while maintaining fleet flexibility to respond to seasonal demand variations and market changes.

Customer retention initiatives should focus on loyalty programs, personalized services, and seamless digital experiences that encourage repeat business and positive word-of-mouth referrals. Building strong customer relationships provides sustainable competitive advantages in increasingly competitive markets.

Sustainability integration represents both opportunity and necessity as environmental considerations become more important to customers and regulators. Early investment in electric vehicles and sustainable practices can create competitive differentiation while preparing for future market requirements.

Market growth projections indicate continued expansion driven by tourism recovery, business travel normalization, and evolving mobility preferences. The sector is expected to maintain steady growth momentum with projected annual growth rates of 8.2% over the medium term, supported by technology adoption and service innovation.

Technology evolution will continue transforming the rental experience through artificial intelligence, Internet of Things applications, and advanced analytics. These developments will enable more personalized services, predictive maintenance, and operational optimization that enhance both customer satisfaction and business performance.

Market structure changes may include further consolidation as companies seek scale advantages and geographic expansion opportunities. Strategic partnerships and acquisitions will likely reshape competitive dynamics while creating more comprehensive service offerings for customers.

Regulatory developments regarding environmental standards, safety requirements, and digital services may influence operational practices and investment priorities. Companies must remain adaptable to evolving regulatory frameworks while maintaining compliance and service quality standards.

Customer behavior evolution toward sustainable transportation options and flexible mobility solutions will drive continued service innovation and fleet diversification. MWR forecasts indicate that electric vehicle rentals could represent 15% of fleet composition within five years, reflecting changing customer preferences and environmental considerations.

Russia’s car rental market demonstrates resilient growth potential supported by recovering tourism activities, evolving business travel patterns, and increasing acceptance of flexible mobility solutions. The market benefits from strong domestic demand, technology adoption, and continuous service improvements that enhance customer experiences and operational efficiency.

Strategic opportunities exist across multiple dimensions including geographic expansion, service diversification, technology integration, and sustainability initiatives. Companies that successfully navigate market challenges while investing in customer-centric innovations and operational excellence are positioned to capture significant growth opportunities in this dynamic market environment.

Future success will depend on adaptability to changing customer preferences, effective technology utilization, and strategic positioning within the evolving mobility ecosystem. The market outlook remains positive for operators that embrace innovation while maintaining focus on service quality and customer satisfaction in Russia’s diverse and expanding car rental landscape.

What is Car Rentals?

Car rentals refer to the service of renting vehicles for short periods, typically ranging from a few hours to several weeks. This service is popular among travelers and businesses needing temporary transportation solutions.

What are the key players in the Russia Car Rentals Market?

Key players in the Russia Car Rentals Market include companies like Sixt, Europcar, and Avis, which offer a range of vehicles for both leisure and business purposes. These companies compete on pricing, vehicle availability, and customer service, among others.

What are the growth factors driving the Russia Car Rentals Market?

The growth of the Russia Car Rentals Market is driven by increasing domestic and international tourism, a rise in business travel, and the growing trend of urban mobility solutions. Additionally, the expansion of online booking platforms has made car rentals more accessible.

What challenges does the Russia Car Rentals Market face?

The Russia Car Rentals Market faces challenges such as regulatory hurdles, fluctuating fuel prices, and competition from ride-sharing services. These factors can impact profitability and operational efficiency for rental companies.

What opportunities exist in the Russia Car Rentals Market?

Opportunities in the Russia Car Rentals Market include the potential for growth in electric vehicle rentals, partnerships with travel agencies, and the expansion of services in underserved regions. Additionally, the increasing demand for flexible transportation options presents new avenues for growth.

What trends are shaping the Russia Car Rentals Market?

Trends shaping the Russia Car Rentals Market include the rise of digital platforms for booking and managing rentals, an emphasis on sustainability with eco-friendly vehicle options, and the integration of technology for enhanced customer experiences. These trends are influencing how consumers approach car rentals.

Russia Car Rentals Market

| Segmentation Details | Description |

|---|---|

| Vehicle Type | SUV, Sedan, Hatchback, Minivan |

| Customer Type | Business Travelers, Tourists, Locals, Corporates |

| Booking Channel | Online Platforms, Travel Agencies, Direct Booking, Mobile Apps |

| Rental Duration | Short-Term, Long-Term, Weekend, Monthly |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Russia Car Rentals Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.