444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Canada equity lending market represents a sophisticated financial ecosystem where institutional investors, pension funds, and asset managers participate in securities lending arrangements to generate additional revenue streams. This market has experienced substantial growth driven by increasing demand for short-selling activities, regulatory changes, and the expansion of exchange-traded funds (ETFs). Market participants are leveraging advanced technology platforms to streamline lending operations and enhance risk management capabilities.

Institutional adoption has accelerated significantly, with pension funds and insurance companies recognizing equity lending as a valuable source of incremental income. The market demonstrates robust activity across various sectors, including technology, energy, and financial services. Growth rates have remained consistently strong, with the market expanding at approximately 8.5% CAGR over recent years, reflecting increased participation from both domestic and international investors.

Regulatory frameworks established by Canadian securities regulators have provided clarity and confidence for market participants, fostering an environment conducive to sustainable growth. The integration of environmental, social, and governance (ESG) considerations has also influenced lending decisions, with many institutions incorporating sustainability criteria into their equity lending strategies.

The Canada equity lending market refers to the financial marketplace where securities owners temporarily lend their equity holdings to borrowers in exchange for fees and collateral, facilitating various investment strategies including short selling, market making, and arbitrage activities. This market enables institutional investors to monetize their long-term equity positions while maintaining ownership rights and dividend entitlements.

Securities lending transactions involve three primary parties: the beneficial owner (lender), the borrower, and often an intermediary agent who facilitates the transaction. The lender receives compensation in the form of lending fees, typically calculated as a percentage of the borrowed securities’ value, while providing the borrower with temporary access to specific equity instruments needed for their investment strategies.

Collateral management plays a crucial role in these transactions, with borrowers required to provide collateral exceeding the value of borrowed securities. This collateral, often in the form of cash or high-quality securities, serves as protection for lenders against counterparty risk and market volatility.

Market dynamics in the Canada equity lending sector reflect a mature and increasingly sophisticated landscape characterized by technological innovation and regulatory compliance. The market has demonstrated resilience through various economic cycles, with institutional participation rates reaching approximately 72% among major pension funds and asset managers.

Technology adoption has transformed traditional lending operations, with automated matching systems and real-time risk monitoring becoming standard practice. These technological advancements have reduced operational costs while improving transparency and efficiency across the lending ecosystem. Digital platforms now facilitate approximately 85% of all equity lending transactions in the Canadian market.

Revenue generation from equity lending activities has become an essential component of institutional investment strategies, with many organizations reporting that lending income contributes between 15-25 basis points to their overall portfolio returns. This additional income stream has proven particularly valuable during periods of low interest rates and compressed investment margins.

Market concentration remains relatively balanced, with the top five lending agents managing approximately 60% of total lending activity, while smaller specialized providers serve niche segments and specific client requirements. This competitive landscape ensures competitive pricing and service innovation across the market.

Institutional participation continues to expand as more Canadian pension funds and asset managers recognize the value proposition of equity lending programs. The market has evolved from a supplementary activity to a core component of institutional investment operations.

Market efficiency has improved significantly through the adoption of standardized processes and industry best practices. MarkWide Research analysis indicates that operational efficiency gains have reduced transaction costs by approximately 20% over the past three years, benefiting both lenders and borrowers.

Institutional demand for additional revenue streams represents the primary driver of equity lending market growth in Canada. As traditional investment returns face pressure from low interest rates and market volatility, institutional investors increasingly view securities lending as an essential portfolio enhancement strategy.

Regulatory clarity provided by Canadian securities regulators has created a stable operating environment that encourages institutional participation. Clear guidelines regarding collateral requirements, reporting obligations, and risk management standards have reduced regulatory uncertainty and compliance costs for market participants.

Technology advancement has streamlined lending operations and reduced barriers to entry for smaller institutional investors. Cloud-based platforms and automated systems enable efficient portfolio management and real-time decision-making, making equity lending accessible to a broader range of market participants.

Short-selling activity continues to drive borrowing demand across various market segments. Hedge funds, proprietary trading desks, and market makers require access to borrowable securities to implement their investment strategies, creating consistent demand for lending services.

ETF growth has significantly expanded the universe of lendable securities, with ETF providers actively participating in lending programs to reduce fund operating expenses. The proliferation of sector-specific and thematic ETFs has created new lending opportunities across diverse market segments.

Counterparty risk remains a significant concern for institutional lenders, particularly during periods of market stress when borrower defaults may occur. Despite robust collateral requirements, the potential for losses during extreme market conditions continues to influence lending decisions and risk appetite.

Operational complexity associated with securities lending programs can deter smaller institutional investors from participating in the market. The need for specialized systems, compliance procedures, and risk management capabilities requires substantial investment in technology and human resources.

Market volatility can impact lending revenues and create challenges for risk management systems. During periods of high volatility, lending fees may fluctuate significantly, and the value of collateral may require frequent adjustments to maintain appropriate coverage ratios.

Regulatory changes pose ongoing challenges for market participants who must continuously adapt their operations to comply with evolving requirements. New regulations regarding capital adequacy, reporting standards, and risk management can increase compliance costs and operational complexity.

Competition pressure from alternative revenue-generating strategies may reduce institutional focus on equity lending programs. As new investment opportunities emerge, institutions must evaluate the relative attractiveness of securities lending compared to other portfolio enhancement strategies.

ESG integration presents significant opportunities for market expansion as institutional investors increasingly incorporate sustainability criteria into their investment decisions. Sustainable lending programs that align with ESG objectives can attract environmentally conscious investors and differentiate service providers in a competitive market.

Technology innovation continues to create opportunities for operational efficiency improvements and new service offerings. Artificial intelligence and machine learning applications can enhance risk assessment, optimize lending decisions, and improve client service delivery across the equity lending ecosystem.

Cross-border expansion offers Canadian institutions opportunities to participate in international lending markets and access a broader universe of borrowable securities. Strategic partnerships with global lending agents can facilitate international market access and portfolio diversification.

Product development initiatives focused on specialized lending structures and customized solutions can address specific client needs and create competitive advantages. Innovation in collateral management, fee structures, and risk-sharing arrangements can attract new market participants and expand existing relationships.

Market education efforts targeting smaller institutional investors can expand market participation and increase overall lending activity. Educational programs highlighting the benefits and risk management aspects of equity lending can encourage broader adoption across the Canadian institutional investment community.

Supply and demand dynamics in the Canada equity lending market reflect the interplay between institutional lending capacity and borrower requirements across various market segments. The balance between available securities and borrowing demand influences lending fees and market efficiency.

Seasonal patterns affect lending activity, with increased demand typically observed during earnings seasons and around dividend payment dates. These cyclical variations create opportunities for lenders to optimize their revenue generation through strategic timing of lending activities.

Interest rate environment significantly impacts the attractiveness of cash collateral reinvestment opportunities for lenders. When interest rates are low, the spread between lending fees and collateral reinvestment returns becomes more critical to overall program profitability.

Market concentration dynamics continue to evolve as larger institutions expand their lending programs while smaller players seek specialized niches. This trend toward consolidation in some segments coexists with innovation and specialization in others, creating a diverse and competitive marketplace.

International influences from global equity lending markets affect Canadian market conditions through cross-border lending arrangements and international investor participation. Global market trends and regulatory developments can have spillover effects on Canadian market dynamics and participant behavior.

Primary research methodologies employed in analyzing the Canada equity lending market include comprehensive surveys of institutional investors, lending agents, and borrowers to gather firsthand insights into market practices, challenges, and opportunities. These surveys provide quantitative data on participation rates, revenue generation, and operational efficiency metrics.

Secondary research involves extensive analysis of regulatory filings, industry reports, and public disclosures from major market participants. This research provides historical context and trend analysis essential for understanding market evolution and future prospects.

Expert interviews with industry professionals, including portfolio managers, risk officers, and compliance specialists, offer qualitative insights into market dynamics and emerging trends. These interviews provide valuable perspectives on regulatory changes, technology adoption, and competitive developments.

Data validation processes ensure accuracy and reliability of research findings through cross-referencing multiple sources and verification with industry experts. Statistical analysis and trend modeling support quantitative assessments of market growth and participant behavior.

Market monitoring involves continuous tracking of lending rates, transaction volumes, and participant activity to identify emerging trends and market developments. This ongoing surveillance provides real-time insights into market conditions and competitive dynamics.

Ontario dominates the Canadian equity lending market, accounting for approximately 55% of total lending activity due to the concentration of major institutional investors and financial services firms in Toronto. The province’s robust regulatory framework and sophisticated financial infrastructure support extensive lending operations.

Quebec represents the second-largest regional market, with approximately 25% market share, driven by the presence of large pension funds and insurance companies headquartered in Montreal. The province’s institutional investors have been early adopters of equity lending programs and maintain active lending operations.

Western Canada accounts for approximately 15% of market activity, with Alberta and British Columbia leading regional participation. Energy sector pension funds and resource-focused investment managers contribute significantly to lending activity in these provinces.

Atlantic Canada maintains a smaller but growing presence in the equity lending market, representing approximately 5% of total activity. Regional pension funds and credit unions are increasingly exploring equity lending opportunities as part of their investment strategies.

Cross-provincial collaboration has increased as institutions seek to optimize their lending programs through partnerships and shared resources. This collaboration has improved market efficiency and expanded opportunities for smaller regional players to participate in national lending programs.

Market leadership in the Canada equity lending sector is distributed among several key players, each offering specialized services and competitive advantages to institutional clients.

Competitive differentiation focuses on technology capabilities, risk management expertise, and client service quality. Market participants invest heavily in platform development and automation to improve operational efficiency and client experience.

Strategic partnerships between Canadian institutions and international lending agents have expanded market access and enhanced service offerings. These collaborations enable smaller Canadian players to compete effectively with larger global providers.

By Participant Type:

By Security Type:

By Lending Duration:

Pension Fund Lending represents the most significant category within the Canadian equity lending market, driven by the substantial asset bases and long-term investment horizons of major pension plans. These institutions view equity lending as a natural extension of their investment management activities, generating incremental returns while maintaining their strategic asset allocation.

Insurance Company Participation has grown substantially as life insurance companies and property & casualty insurers recognize the value of securities lending in enhancing portfolio returns. Their stable, long-term equity holdings provide an ideal foundation for active lending programs.

Asset Manager Engagement varies significantly based on client mandates and investment strategies. Many asset managers operate lending programs on behalf of their clients, sharing lending revenues according to predetermined arrangements that align interests and incentivize active program management.

ETF Lending Programs have become increasingly sophisticated as ETF providers seek to reduce fund operating expenses through lending revenue. The growth of the Canadian ETF market has created substantial lending opportunities across various sectors and investment themes.

Sovereign Wealth Fund Activities in the Canadian market reflect the international nature of modern equity lending, with foreign sovereign investors participating in Canadian lending markets while Canadian institutions access international opportunities through reciprocal arrangements.

Revenue Enhancement represents the primary benefit for institutional lenders, with equity lending programs typically contributing 10-30 basis points to overall portfolio returns. This additional income stream helps offset management fees and improves net returns for beneficiaries.

Portfolio Optimization benefits extend beyond direct lending revenue to include improved portfolio liquidity and enhanced risk management capabilities. Active lending programs often provide valuable insights into market demand and security-specific dynamics that inform broader investment decisions.

Operational Efficiency gains result from the integration of lending operations with existing custody and portfolio management systems. Modern lending platforms streamline administrative processes and reduce operational overhead while improving transparency and reporting capabilities.

Risk Diversification advantages emerge from the uncorrelated nature of lending revenues relative to traditional investment returns. This diversification can improve overall portfolio risk-adjusted returns and provide stability during volatile market periods.

Market Liquidity Enhancement benefits the broader equity market ecosystem by facilitating price discovery, market making, and arbitrage activities. Active lending markets contribute to overall market efficiency and reduce transaction costs for all participants.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital Transformation continues to reshape the equity lending landscape through the adoption of cloud-based platforms, artificial intelligence, and automated decision-making systems. These technologies improve operational efficiency while reducing costs and enhancing client service delivery.

ESG Integration has emerged as a significant trend, with institutional investors incorporating environmental, social, and governance criteria into their lending decisions. This trend reflects broader institutional commitments to sustainable investing and responsible stewardship practices.

Collateral Optimization strategies are becoming more sophisticated as market participants seek to maximize the efficiency of their collateral usage. Advanced collateral management systems enable real-time optimization and reduce funding costs for borrowers.

Cross-Border Activity has increased as Canadian institutions seek access to international lending opportunities while foreign investors participate in Canadian markets. This globalization trend expands market opportunities and enhances diversification benefits.

Product Innovation focuses on developing new lending structures and instruments that address specific client needs and market conditions. Customized solutions and flexible arrangements are becoming more common as competition intensifies.

Regulatory Evolution has seen Canadian securities regulators enhance disclosure requirements and risk management standards for equity lending activities. These developments aim to improve market transparency and protect investor interests while maintaining market efficiency.

Technology Partnerships between traditional lending agents and fintech companies have accelerated platform development and innovation. These collaborations combine established market expertise with cutting-edge technology capabilities to create superior client solutions.

Market Consolidation trends have emerged as larger institutions acquire specialized lending capabilities and smaller players seek scale through strategic partnerships. This consolidation aims to achieve operational efficiencies and enhance competitive positioning.

International Expansion initiatives by Canadian institutions have increased their participation in global lending markets. MWR research indicates that international lending activity by Canadian institutions has grown by approximately 35% over the past two years.

Sustainability Initiatives have gained prominence as market participants develop ESG-focused lending policies and reporting frameworks. These initiatives align with broader institutional sustainability commitments and stakeholder expectations.

Technology Investment should remain a priority for market participants seeking to maintain competitive advantages and operational efficiency. Institutions should focus on platforms that offer scalability, integration capabilities, and advanced analytics to support decision-making and risk management.

Risk Management Enhancement requires continuous attention as market conditions evolve and new risks emerge. Institutions should regularly review and update their risk management frameworks to address counterparty risk, operational risk, and market risk effectively.

Client Education efforts should target smaller institutional investors who may benefit from equity lending programs but lack awareness or understanding of the opportunities. Educational initiatives can expand market participation and increase overall lending activity.

ESG Integration strategies should be developed to address growing institutional demand for sustainable investment practices. Lending policies that incorporate ESG criteria can differentiate service providers and attract environmentally conscious clients.

Partnership Development opportunities should be explored to enhance service offerings and expand market access. Strategic alliances with international partners, technology providers, and specialized service firms can create competitive advantages and improve client value propositions.

Market expansion is expected to continue as more Canadian institutional investors recognize the value proposition of equity lending programs. The market is projected to grow at a CAGR of approximately 9.2% over the next five years, driven by increased institutional participation and technological advancement.

Technology adoption will accelerate as market participants seek to improve operational efficiency and reduce costs. Artificial intelligence and machine learning applications are expected to become standard features of lending platforms, enabling more sophisticated risk assessment and decision-making capabilities.

Regulatory development will likely focus on enhancing market transparency and investor protection while maintaining market efficiency. Future regulations may address areas such as collateral management, reporting standards, and cross-border lending arrangements.

International integration is expected to increase as Canadian institutions expand their global lending activities and foreign investors increase their participation in Canadian markets. This trend will create new opportunities for diversification and revenue generation.

Product innovation will continue as market participants develop new lending structures and services to address evolving client needs. Customized solutions and flexible arrangements are likely to become more prevalent as competition intensifies and client sophistication increases.

The Canada equity lending market represents a mature and sophisticated financial ecosystem that continues to evolve through technological innovation, regulatory development, and changing institutional needs. The market has demonstrated resilience and growth potential, with strong participation from major institutional investors and expanding opportunities for smaller players.

Key success factors for market participants include technology investment, risk management excellence, and client service innovation. Institutions that effectively leverage these capabilities while adapting to changing market conditions are well-positioned to capture growth opportunities and generate sustainable value for their stakeholders.

Future prospects remain positive, supported by continued institutional adoption, technological advancement, and regulatory stability. The integration of ESG considerations and international expansion opportunities provide additional avenues for market growth and development. As the market continues to mature, participants who focus on operational excellence, client service, and strategic innovation will be best positioned to succeed in this dynamic and competitive environment.

What is Equity Lending?

Equity lending refers to the practice of lending shares of stock to investors or institutions, allowing them to sell the shares short. This process is commonly used in the financial markets to facilitate short selling and enhance liquidity.

What are the key players in the Canada Equity Lending Market?

Key players in the Canada Equity Lending Market include major financial institutions such as Bank of Montreal, Toronto-Dominion Bank, and National Bank of Canada, among others. These companies provide equity lending services to institutional investors and hedge funds.

What are the growth factors driving the Canada Equity Lending Market?

The growth of the Canada Equity Lending Market is driven by increasing demand for short selling, the rise of hedge funds, and the growing need for liquidity in the stock market. Additionally, advancements in technology and trading platforms are facilitating easier access to equity lending services.

What challenges does the Canada Equity Lending Market face?

The Canada Equity Lending Market faces challenges such as regulatory scrutiny, market volatility, and the potential for increased borrowing costs. These factors can impact the willingness of investors to engage in equity lending activities.

What opportunities exist in the Canada Equity Lending Market?

Opportunities in the Canada Equity Lending Market include the expansion of alternative investment strategies and the increasing participation of institutional investors. Additionally, the growth of fintech solutions is creating new avenues for equity lending services.

What trends are shaping the Canada Equity Lending Market?

Trends in the Canada Equity Lending Market include the rise of automated lending platforms, increased transparency in lending practices, and a focus on sustainable investing. These trends are influencing how equity lending is conducted and perceived in the market.

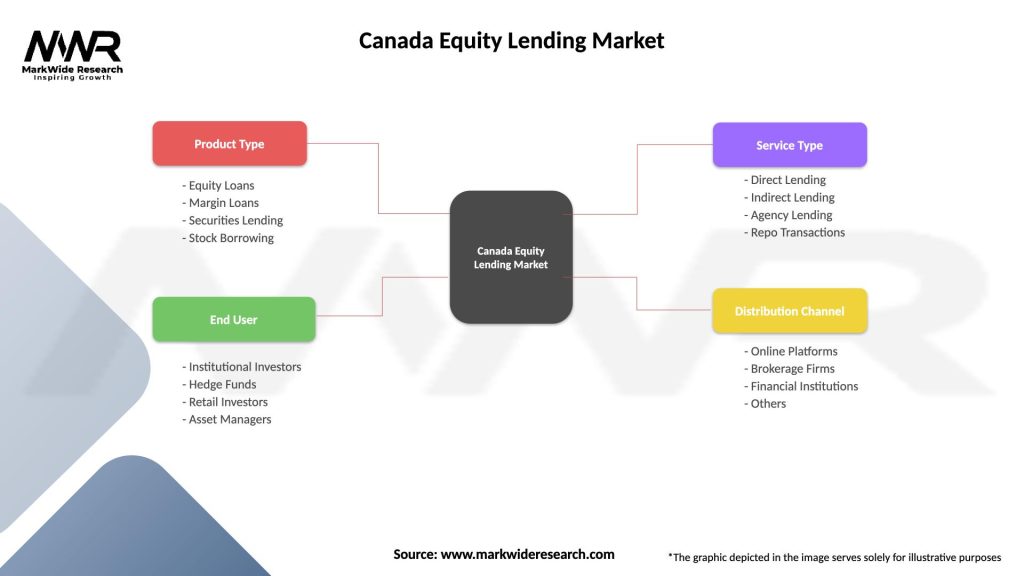

Canada Equity Lending Market

| Segmentation Details | Description |

|---|---|

| Product Type | Equity Loans, Margin Loans, Securities Lending, Stock Borrowing |

| End User | Institutional Investors, Hedge Funds, Retail Investors, Asset Managers |

| Service Type | Direct Lending, Indirect Lending, Agency Lending, Repo Transactions |

| Distribution Channel | Online Platforms, Brokerage Firms, Financial Institutions, Others |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Canada Equity Lending Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.