444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The United Kingdom domestic courier, express, and parcel (CEP) market represents a dynamic and rapidly evolving sector that serves as the backbone of modern commerce and logistics infrastructure. This comprehensive market encompasses a diverse range of services including same-day delivery, next-day express services, standard parcel delivery, and specialized courier solutions across England, Scotland, Wales, and Northern Ireland. The market has experienced unprecedented transformation driven by the exponential growth of e-commerce, changing consumer expectations, and technological innovations that have revolutionized last-mile delivery operations.

Market dynamics indicate robust expansion with the sector demonstrating resilience and adaptability in response to evolving consumer demands and digital transformation initiatives. The integration of advanced technologies such as artificial intelligence, machine learning, and Internet of Things (IoT) solutions has enhanced operational efficiency by approximately 35% across leading service providers. Furthermore, the market has witnessed significant consolidation activities and strategic partnerships aimed at expanding service capabilities and geographic coverage throughout the UK.

Consumer behavior patterns have fundamentally shifted toward demanding faster, more flexible, and transparent delivery options, with same-day delivery services experiencing growth rates exceeding 28% annually. The market serves diverse customer segments ranging from individual consumers and small businesses to large enterprises and government organizations, each requiring tailored solutions that address specific logistical challenges and operational requirements.

The United Kingdom domestic courier, express, and parcel market refers to the comprehensive ecosystem of logistics and delivery services that facilitate the transportation of packages, documents, and goods within the geographical boundaries of the United Kingdom. This market encompasses three primary service categories: courier services for time-sensitive and high-value deliveries, express services for expedited shipping with guaranteed delivery timeframes, and parcel services for standard package transportation across various weight and size specifications.

Service differentiation within this market is characterized by delivery speed, tracking capabilities, insurance coverage, and specialized handling requirements. Courier services typically focus on same-day or next-day delivery of critical documents and small packages, while express services provide guaranteed delivery windows for business-critical shipments. Parcel services encompass the broader category of package delivery with varying service levels from standard delivery to premium options with enhanced tracking and customer support.

Market participants include established international logistics companies, domestic specialists, regional carriers, and emerging technology-driven platforms that leverage innovative delivery models such as crowdsourced logistics and autonomous delivery systems. The market operates through complex networks of distribution centers, sorting facilities, transportation fleets, and last-mile delivery infrastructure that collectively ensure efficient package movement across urban and rural areas throughout the UK.

Strategic market positioning reveals the UK domestic CEP market as a critical component of the nation’s economic infrastructure, supporting millions of transactions daily and enabling seamless commerce across multiple industry sectors. The market demonstrates exceptional growth momentum driven by accelerating digitalization trends, with online retail penetration reaching approximately 32% of total retail sales, significantly higher than the European average.

Competitive landscape analysis indicates a multi-tiered market structure featuring global logistics giants, established domestic players, and innovative technology startups that collectively serve diverse customer segments with differentiated value propositions. Market leaders have invested heavily in automation technologies, sustainable delivery solutions, and customer experience enhancements to maintain competitive advantages in an increasingly crowded marketplace.

Technology adoption has emerged as a key differentiator, with leading companies implementing advanced route optimization algorithms, real-time tracking systems, and predictive analytics capabilities that improve delivery efficiency by up to 42% while reducing operational costs. The integration of artificial intelligence and machine learning technologies has enabled more accurate demand forecasting, optimized resource allocation, and enhanced customer service capabilities.

Sustainability initiatives have gained significant traction as companies respond to environmental concerns and regulatory requirements, with electric vehicle adoption in delivery fleets increasing by 67% over the past two years. These efforts align with broader corporate social responsibility objectives and government initiatives aimed at reducing carbon emissions in the transportation sector.

Market segmentation analysis reveals distinct growth patterns across different service categories and customer segments, with express delivery services demonstrating the strongest expansion trajectory. The following key insights characterize current market dynamics:

E-commerce proliferation stands as the primary catalyst driving unprecedented growth in the UK domestic CEP market. The accelerated shift toward online shopping, particularly following global events that reshaped consumer behavior, has created sustained demand for reliable and efficient delivery services. Online retail sales continue to capture increasing market share, with consumers expecting seamless integration between digital purchasing experiences and physical delivery fulfillment.

Consumer expectations evolution has fundamentally transformed service requirements, with customers demanding faster delivery times, greater flexibility, and enhanced transparency throughout the delivery process. The concept of instant gratification has extended to logistics services, creating opportunities for companies that can provide same-day or even same-hour delivery capabilities in major metropolitan areas.

Digital transformation initiatives across industries have increased reliance on efficient document and package delivery services for business operations. Companies are increasingly outsourcing logistics functions to specialized providers that can offer superior service levels and cost efficiency compared to in-house delivery capabilities.

Urbanization trends continue to concentrate population density in major cities, creating economies of scale for delivery operations while simultaneously increasing the complexity of last-mile logistics. Urban environments present both opportunities for efficient route optimization and challenges related to traffic congestion, parking limitations, and environmental restrictions.

Technological advancement in areas such as mobile applications, GPS tracking, and automated sorting systems has enhanced service capabilities while reducing operational costs. These innovations enable better customer communication, improved delivery accuracy, and more efficient resource utilization across delivery networks.

Operational cost pressures represent significant challenges for CEP service providers, particularly in areas such as fuel costs, labor expenses, and vehicle maintenance. Rising operational costs can compress profit margins and limit the ability to invest in service improvements or expansion initiatives, especially for smaller market participants with limited economies of scale.

Regulatory compliance requirements continue to evolve, particularly in areas related to environmental standards, driver working time regulations, and data protection requirements. Compliance costs can be substantial, and regulatory changes may require significant operational adjustments or technology investments that strain financial resources.

Infrastructure limitations in certain geographic areas, particularly rural regions, can constrain service expansion and increase delivery costs. Limited transportation infrastructure, challenging terrain, and low population density make it economically difficult to provide comprehensive coverage with competitive service levels.

Labor market challenges including driver shortages, wage inflation, and high turnover rates impact service reliability and operational costs. The gig economy has created alternative employment opportunities that compete for the same labor pool, while regulatory changes regarding worker classification add complexity to workforce management strategies.

Competitive intensity has intensified pricing pressure across the market, with customers increasingly price-sensitive while simultaneously demanding enhanced service levels. This dynamic creates challenges for maintaining profitability while investing in necessary technology upgrades and service improvements.

Technology integration opportunities present substantial potential for market expansion and service enhancement. The adoption of artificial intelligence, machine learning, and predictive analytics can optimize delivery routes, improve demand forecasting, and enhance customer service capabilities. Companies that successfully leverage these technologies can achieve significant competitive advantages through improved efficiency and customer satisfaction.

Sustainable delivery solutions represent a growing market opportunity as environmental consciousness increases among consumers and businesses. Electric vehicle adoption, carbon-neutral delivery options, and packaging optimization initiatives can differentiate service providers while addressing regulatory requirements and corporate sustainability objectives.

Specialized service segments offer opportunities for market expansion, including healthcare logistics, automotive parts delivery, and temperature-controlled transportation. These niche markets often command premium pricing and provide opportunities for long-term customer relationships with specialized requirements.

Rural market penetration remains an underserved opportunity, with innovative delivery models such as consolidated delivery points, mobile delivery units, and partnership arrangements with local businesses potentially expanding service coverage to previously uneconomical areas.

International expansion through strategic partnerships or acquisitions can provide growth opportunities for established UK operators seeking to leverage their operational expertise and technology capabilities in other markets with similar characteristics and growth potential.

Competitive dynamics within the UK domestic CEP market are characterized by intense rivalry among established players and continuous entry of innovative startups that challenge traditional business models. Market leaders maintain advantages through extensive infrastructure networks, established customer relationships, and economies of scale, while newer entrants compete through technology innovation, specialized services, and competitive pricing strategies.

Customer relationship management has become increasingly sophisticated, with companies investing in customer data analytics, personalized service offerings, and proactive communication systems. The ability to anticipate customer needs, provide flexible delivery options, and resolve issues quickly has become essential for maintaining market share in a highly competitive environment.

Supply chain integration trends indicate deeper collaboration between CEP providers and their customers, with many companies offering value-added services such as inventory management, returns processing, and supply chain consulting. These expanded service offerings create additional revenue streams while strengthening customer relationships through increased dependency and switching costs.

Seasonal demand fluctuations create both challenges and opportunities for market participants, with peak periods such as holiday seasons requiring significant capacity scaling while off-peak periods may result in underutilized resources. Successful companies have developed flexible operational models that can efficiently manage these demand variations while maintaining service quality.

Technology disruption continues to reshape market dynamics, with emerging solutions such as autonomous delivery vehicles, drone technology, and blockchain-based tracking systems potentially transforming traditional delivery models. Companies must balance investment in proven technologies with exploration of emerging innovations that may provide future competitive advantages.

Comprehensive market analysis was conducted through a multi-faceted research approach combining primary and secondary research methodologies to ensure accuracy and completeness of market insights. The research framework incorporated quantitative data analysis, qualitative stakeholder interviews, and industry expert consultations to develop a holistic understanding of market dynamics and future trends.

Primary research activities included structured interviews with key industry executives, customer surveys across different market segments, and operational assessments of leading service providers. These activities provided direct insights into market challenges, opportunities, and strategic priorities from multiple stakeholder perspectives including service providers, customers, and industry experts.

Secondary research sources encompassed industry publications, government statistics, regulatory filings, company annual reports, and academic research papers. This comprehensive data collection approach ensured broad coverage of market factors and validation of primary research findings through multiple independent sources.

Data validation processes included cross-referencing information from multiple sources, statistical analysis of quantitative data, and expert review of research findings. Quality assurance measures were implemented throughout the research process to ensure accuracy, reliability, and objectivity of market analysis and conclusions.

Analytical frameworks utilized advanced statistical modeling techniques, trend analysis methodologies, and competitive benchmarking approaches to identify key market patterns and develop predictive insights regarding future market evolution and growth opportunities.

Geographic market distribution across the United Kingdom reveals significant concentration in major metropolitan areas, with London and the Greater London area representing approximately 35% of total market activity. This concentration reflects population density, economic activity levels, and the prevalence of e-commerce adoption in urban environments where consumers have higher disposable incomes and greater comfort with digital purchasing channels.

England dominates the market landscape, accounting for the majority of delivery volume and revenue generation across all service categories. Major cities including Manchester, Birmingham, Liverpool, and Leeds serve as important regional hubs that support extensive distribution networks and provide economies of scale for service providers operating in these markets.

Scotland presents unique market characteristics with Edinburgh and Glasgow serving as primary commercial centers while rural areas pose logistical challenges due to geographic terrain and population dispersion. The Scottish market demonstrates strong demand for express services, particularly in business-to-business segments, with growth rates exceeding 18% annually in urban areas.

Wales and Northern Ireland represent smaller but strategically important market segments with distinct operational requirements. These regions require specialized delivery networks that can efficiently serve both urban centers and rural communities, often necessitating partnerships with local delivery providers to ensure comprehensive coverage.

Rural market dynamics across all regions present both challenges and opportunities, with lower population density increasing per-delivery costs while creating demand for innovative delivery solutions such as consolidated delivery points, mobile delivery services, and flexible delivery scheduling options that accommodate rural lifestyle patterns.

Market leadership is distributed among several major players, each with distinct competitive advantages and market positioning strategies. The competitive environment encompasses international logistics corporations, established domestic operators, and innovative technology-driven startups that collectively serve diverse customer segments with differentiated value propositions.

Competitive strategies vary significantly across market participants, with some companies focusing on operational excellence and cost efficiency while others emphasize technology innovation and customer experience enhancements. Market consolidation activities continue to reshape competitive dynamics through strategic acquisitions and partnership arrangements.

Service-based segmentation reveals distinct market categories with unique characteristics, growth patterns, and customer requirements. The market can be analyzed across multiple dimensions including service type, customer segment, delivery speed, and geographic coverage to understand specific market dynamics and opportunities.

By Service Type:

By Customer Segment:

By Delivery Speed:

Express delivery services demonstrate the strongest growth momentum, driven by increasing customer expectations for rapid fulfillment and the expansion of same-day delivery capabilities in major metropolitan areas. This segment commands premium pricing while requiring significant investment in technology infrastructure, vehicle fleets, and operational capabilities to maintain service reliability and customer satisfaction.

Standard parcel delivery represents the foundation of the market, providing steady revenue streams and operational scale that supports infrastructure investments and service expansion initiatives. This segment faces intense pricing pressure but offers opportunities for differentiation through enhanced tracking capabilities, flexible delivery options, and superior customer service.

Specialized courier services serve niche markets with unique requirements such as healthcare logistics, legal document delivery, and high-value item transportation. These segments often provide higher profit margins and long-term customer relationships while requiring specialized operational capabilities and compliance with industry-specific regulations.

Business-to-business services focus on reliability, integration capabilities, and value-added services such as supply chain management and inventory optimization. This segment values operational efficiency and cost predictability while requiring sophisticated technology platforms that integrate with customer business systems.

Consumer delivery services emphasize convenience, flexibility, and customer experience with features such as real-time tracking, delivery time windows, and alternative delivery locations. This segment drives innovation in last-mile delivery solutions and customer communication technologies.

Service providers benefit from expanding market opportunities driven by e-commerce growth, technological advancement, and evolving customer expectations. Companies that successfully adapt to market changes can achieve sustainable competitive advantages through operational excellence, technology innovation, and customer relationship management capabilities.

Technology integration enables service providers to optimize operational efficiency, reduce costs, and enhance customer satisfaction through improved tracking capabilities, route optimization, and predictive analytics. These technological advantages can translate into improved profit margins and market share growth in competitive environments.

Customers gain access to increasingly sophisticated delivery services with enhanced convenience, reliability, and transparency. Business customers benefit from improved supply chain efficiency and reduced logistics costs, while consumers enjoy greater flexibility and control over their delivery experiences.

Economic stakeholders including suppliers, technology providers, and financial institutions benefit from market growth through increased demand for vehicles, technology solutions, and financing services. The expanding market creates employment opportunities and supports economic development in logistics and related industries.

Environmental benefits emerge from efficiency improvements, route optimization, and sustainable delivery initiatives that reduce carbon emissions and environmental impact. These improvements align with broader sustainability objectives while potentially reducing operational costs for service providers.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability transformation has emerged as a defining trend, with companies increasingly adopting electric vehicles, optimizing delivery routes to reduce emissions, and implementing packaging reduction initiatives. This trend reflects both regulatory requirements and consumer preferences for environmentally responsible services, with electric vehicle adoption in delivery fleets growing by 73% over recent periods.

Technology convergence is revolutionizing operational capabilities through the integration of artificial intelligence, Internet of Things sensors, and advanced analytics platforms. These technologies enable predictive maintenance, dynamic route optimization, and enhanced customer communication that improve service quality while reducing operational costs.

Customer experience focus continues to drive service innovation, with companies investing in mobile applications, real-time tracking systems, and flexible delivery options that provide customers with greater control and transparency. The emphasis on customer experience has become a key differentiator in competitive markets.

Last-mile innovation encompasses various approaches including autonomous delivery vehicles, drone technology, and alternative delivery locations such as locker networks and pickup points. These innovations address the challenges and costs associated with final delivery while providing customers with additional convenience options.

Data analytics utilization has become essential for operational optimization, customer insights, and strategic decision-making. Companies are leveraging big data capabilities to improve demand forecasting, optimize resource allocation, and identify new business opportunities through detailed analysis of delivery patterns and customer behavior.

Strategic partnerships between traditional logistics companies and technology firms have accelerated innovation and service enhancement capabilities. These collaborations combine operational expertise with technological innovation to develop next-generation delivery solutions that address evolving market requirements and customer expectations.

Infrastructure investments in automated sorting facilities, distribution centers, and technology platforms have enhanced operational capacity and efficiency across the market. Leading companies have committed substantial resources to modernizing their infrastructure to support growing volume demands and service complexity requirements.

Regulatory developments including environmental standards, data protection requirements, and labor regulations continue to shape operational practices and strategic planning. Companies must adapt to evolving regulatory frameworks while maintaining service quality and cost competitiveness in dynamic market conditions.

Market consolidation activities through acquisitions and mergers have reshaped competitive dynamics and created opportunities for enhanced service capabilities and geographic expansion. These strategic transactions reflect the importance of scale and operational efficiency in competitive market environments.

Innovation initiatives in areas such as sustainable delivery solutions, autonomous vehicles, and advanced tracking technologies demonstrate the industry’s commitment to continuous improvement and adaptation to changing market conditions and customer requirements.

MarkWide Research analysis indicates that successful market participants should prioritize technology investment and customer experience enhancement to maintain competitive advantages in evolving market conditions. Companies that effectively leverage data analytics, automation technologies, and customer feedback systems are positioned to achieve superior performance and market share growth.

Strategic recommendations emphasize the importance of developing flexible operational models that can efficiently manage demand fluctuations while maintaining service quality standards. This includes investment in scalable infrastructure, workforce management systems, and technology platforms that support operational agility and responsiveness.

Sustainability initiatives should be integrated into core business strategies rather than treated as peripheral activities. Companies that proactively address environmental concerns through electric vehicle adoption, route optimization, and packaging reduction can differentiate themselves while preparing for future regulatory requirements.

Customer relationship management capabilities require continuous enhancement through investment in communication technologies, service personalization, and proactive issue resolution systems. Companies that excel in customer experience management are more likely to achieve customer loyalty and premium pricing opportunities.

Market expansion strategies should focus on underserved segments and geographic areas where innovative delivery models can create competitive advantages. This includes rural markets, specialized industry segments, and emerging service categories that offer growth potential beyond traditional market boundaries.

Market evolution will be characterized by continued technology integration, sustainability focus, and customer experience enhancement as primary drivers of competitive differentiation and growth. The market is expected to maintain robust expansion momentum with projected growth rates of 12-15% annually across key service segments, driven by sustained e-commerce growth and evolving consumer expectations.

Technology transformation will accelerate with broader adoption of artificial intelligence, autonomous delivery systems, and advanced analytics platforms that optimize operational efficiency and customer service capabilities. Companies that successfully integrate these technologies will achieve significant competitive advantages through improved cost structures and service quality.

Sustainability requirements will become increasingly important as regulatory frameworks evolve and customer preferences shift toward environmentally responsible services. The transition to electric vehicle fleets, carbon-neutral delivery options, and sustainable packaging solutions will reshape operational models and competitive dynamics.

Market consolidation trends are expected to continue as companies seek scale advantages and operational synergies through strategic acquisitions and partnerships. This consolidation will create opportunities for enhanced service capabilities while potentially reducing competitive intensity in certain market segments.

MWR projections indicate that successful companies will be those that effectively balance operational efficiency, technology innovation, and customer experience enhancement while adapting to evolving regulatory requirements and market conditions. The future market landscape will reward companies that demonstrate agility, innovation, and customer-centricity in their strategic approaches.

The United Kingdom domestic courier, express, and parcel market represents a dynamic and rapidly evolving sector that continues to demonstrate strong growth potential driven by e-commerce expansion, technological innovation, and changing consumer expectations. Market participants that successfully adapt to evolving conditions through strategic investment in technology, sustainability initiatives, and customer experience enhancement are positioned to achieve sustainable competitive advantages and long-term success.

Strategic success factors include operational excellence, technology integration, customer relationship management, and adaptability to regulatory and market changes. Companies that prioritize these areas while maintaining focus on cost efficiency and service quality will be best positioned to capitalize on market opportunities and navigate competitive challenges in the evolving logistics landscape.

Future market development will be shaped by continued technology advancement, sustainability requirements, and customer experience expectations that demand innovative solutions and operational excellence. The market outlook remains positive with substantial opportunities for growth and differentiation through strategic positioning and execution excellence across all service segments and customer categories.

What is Domestic Courier, Express, And Parcel (CEP)?

Domestic Courier, Express, And Parcel (CEP) refers to the services that facilitate the transportation of goods and documents within a country. This includes various delivery options such as same-day, next-day, and standard delivery, catering to both businesses and individual consumers.

What are the key players in the United Kingdom Domestic Courier, Express, And Parcel (CEP) Market?

Key players in the United Kingdom Domestic Courier, Express, And Parcel (CEP) Market include Royal Mail, DPD, Hermes, and UPS, among others. These companies compete on service speed, reliability, and pricing to capture market share.

What are the growth factors driving the United Kingdom Domestic Courier, Express, And Parcel (CEP) Market?

The growth of the United Kingdom Domestic Courier, Express, And Parcel (CEP) Market is driven by the rise of e-commerce, increasing consumer demand for fast delivery services, and advancements in logistics technology. Additionally, the shift towards online shopping has significantly boosted parcel volumes.

What challenges does the United Kingdom Domestic Courier, Express, And Parcel (CEP) Market face?

The United Kingdom Domestic Courier, Express, And Parcel (CEP) Market faces challenges such as rising operational costs, regulatory compliance issues, and intense competition among service providers. These factors can impact profitability and service quality.

What opportunities exist in the United Kingdom Domestic Courier, Express, And Parcel (CEP) Market?

Opportunities in the United Kingdom Domestic Courier, Express, And Parcel (CEP) Market include the expansion of same-day delivery services, the integration of sustainable practices, and the adoption of advanced technologies like automation and AI. These trends can enhance efficiency and customer satisfaction.

What trends are shaping the United Kingdom Domestic Courier, Express, And Parcel (CEP) Market?

Trends shaping the United Kingdom Domestic Courier, Express, And Parcel (CEP) Market include the increasing use of technology for tracking and managing deliveries, the growth of green logistics initiatives, and the rise of contactless delivery options. These trends reflect changing consumer preferences and environmental concerns.

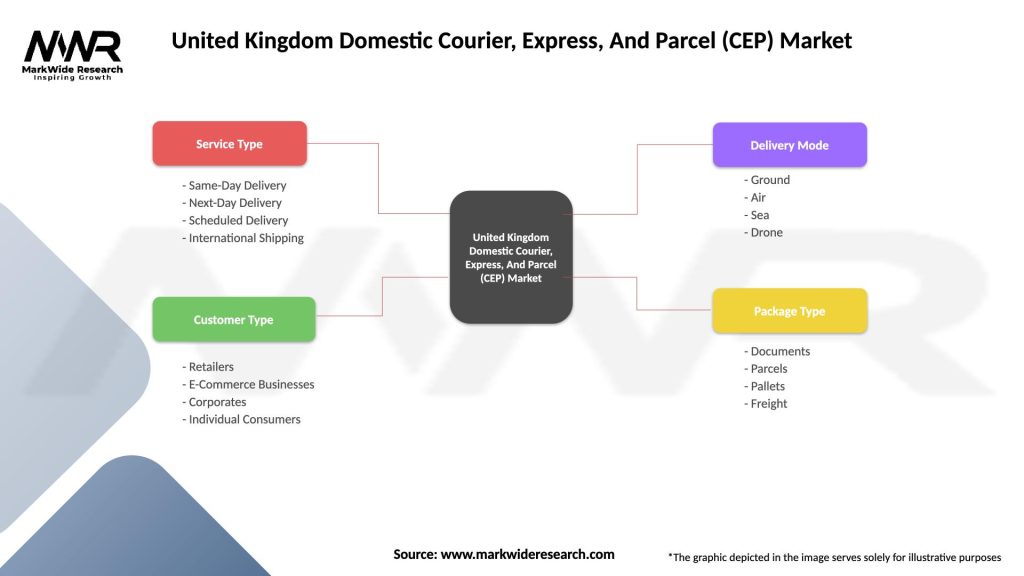

United Kingdom Domestic Courier, Express, And Parcel (CEP) Market

| Segmentation Details | Description |

|---|---|

| Service Type | Same-Day Delivery, Next-Day Delivery, Scheduled Delivery, International Shipping |

| Customer Type | Retailers, E-Commerce Businesses, Corporates, Individual Consumers |

| Delivery Mode | Ground, Air, Sea, Drone |

| Package Type | Documents, Parcels, Pallets, Freight |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the United Kingdom Domestic Courier, Express, And Parcel (CEP) Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.