444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The data center market in Japan represents one of Asia-Pacific’s most sophisticated and rapidly evolving digital infrastructure landscapes. Japan’s strategic position as a technological powerhouse, combined with its advanced telecommunications infrastructure and robust regulatory framework, has positioned the country as a critical hub for data center operations in the region. Digital transformation initiatives across industries, coupled with the increasing adoption of cloud computing services, artificial intelligence, and Internet of Things applications, are driving unprecedented demand for data center capacity throughout Japan.

Market dynamics in Japan’s data center sector are characterized by significant investments in hyperscale facilities, edge computing infrastructure, and sustainable energy solutions. The market is experiencing robust growth driven by enterprise digitalization, government initiatives promoting digital society transformation, and the increasing data localization requirements of multinational corporations. Tokyo metropolitan area continues to dominate the market landscape, accounting for approximately 65% of total data center capacity, while emerging markets in Osaka, Nagoya, and other regional centers are gaining momentum.

Technological advancement remains at the forefront of Japan’s data center evolution, with operators increasingly focusing on energy-efficient cooling systems, renewable energy integration, and advanced automation technologies. The market is witnessing a shift toward colocation services and managed hosting solutions, as organizations seek to optimize their IT infrastructure costs while maintaining high performance and reliability standards. Hyperscale operators are establishing significant presence in Japan, driven by the growing demand for cloud services and content delivery networks.

The data center market in Japan refers to the comprehensive ecosystem of facilities, services, and infrastructure designed to house, manage, and operate computing systems, data storage equipment, and networking components across the Japanese archipelago. This market encompasses various facility types including enterprise data centers, colocation facilities, hyperscale cloud data centers, and edge computing nodes that collectively support Japan’s digital economy and technological advancement.

Data center operations in Japan involve the provision of critical infrastructure services including power supply, cooling systems, physical security, network connectivity, and technical support to enable organizations to maintain their digital operations. The market includes both traditional data center services such as server hosting and managed IT services, as well as emerging solutions like edge computing, hybrid cloud integration, and disaster recovery services tailored to meet Japan’s unique geographical and regulatory requirements.

Japan’s data center market stands as a cornerstone of the nation’s digital infrastructure, supporting everything from financial services and manufacturing to entertainment and government operations. The market has demonstrated remarkable resilience and growth, particularly accelerated by the COVID-19 pandemic which highlighted the critical importance of robust digital infrastructure for business continuity and remote operations.

Key market characteristics include the dominance of the Tokyo metropolitan area as a primary data center hub, the increasing adoption of sustainable and energy-efficient technologies, and the growing presence of international hyperscale operators. The market is experiencing significant transformation driven by 5G network deployment, which is creating demand for edge computing infrastructure, and the government’s Society 5.0 initiative promoting digital transformation across all sectors of the economy.

Investment patterns in Japan’s data center market reflect strong confidence in the country’s digital future, with both domestic and international operators committing substantial resources to capacity expansion and technology upgrades. The market is projected to maintain robust growth trajectory, supported by increasing data generation, cloud adoption rates exceeding 40% among enterprises, and the ongoing digital transformation of traditional industries.

Strategic insights into Japan’s data center market reveal several critical trends shaping the industry’s future direction:

Digital transformation initiatives across Japan’s corporate landscape serve as the primary catalyst for data center market expansion. Organizations are increasingly migrating their operations to digital platforms, requiring robust and scalable infrastructure to support their evolving technological needs. Cloud adoption has accelerated significantly, with enterprises recognizing the benefits of flexible, scalable computing resources that data centers provide.

Government policies promoting digital society transformation, including the Society 5.0 initiative and Digital Transformation (DX) programs, are creating substantial demand for data center services. These initiatives encourage businesses to adopt advanced technologies such as artificial intelligence, Internet of Things, and big data analytics, all of which require substantial computing and storage capacity that modern data centers can efficiently provide.

5G network deployment represents another significant driver, as telecommunications operators and service providers require extensive edge computing infrastructure to deliver low-latency services. The rollout of 5G technology is creating demand for distributed data center architecture, with edge computing facilities becoming increasingly important for supporting real-time applications and services.

E-commerce growth and digital content consumption are driving demand for content delivery networks and cloud services, requiring substantial data center capacity to ensure optimal user experiences. The increasing popularity of streaming services, online gaming, and digital entertainment platforms necessitates robust infrastructure capable of handling high-bandwidth applications and large-scale data processing requirements.

High capital requirements for data center development and operation present significant barriers to market entry, particularly for smaller operators. The substantial investments required for land acquisition, facility construction, power infrastructure, and cooling systems create challenges for new entrants seeking to establish competitive positions in Japan’s data center market.

Energy costs and power availability constraints pose ongoing challenges for data center operators in Japan. The country’s relatively high electricity costs, combined with increasing energy consumption requirements of modern data centers, create operational cost pressures that operators must carefully manage through efficiency improvements and renewable energy adoption strategies.

Skilled workforce shortages in specialized technical areas including data center engineering, cybersecurity, and cloud technologies limit the industry’s ability to rapidly scale operations. The competition for qualified professionals is intensifying as demand for data center services grows, potentially constraining expansion plans and operational efficiency improvements.

Regulatory complexity and compliance requirements, while providing important protections, can create operational challenges and increase costs for data center operators. Navigating Japan’s regulatory landscape requires significant expertise and resources, particularly for international operators seeking to establish or expand their Japanese operations.

Edge computing expansion presents substantial opportunities for data center operators as 5G networks enable new applications requiring ultra-low latency processing. The development of distributed data center networks to support edge computing applications creates opportunities for operators to establish smaller, strategically located facilities that complement existing hyperscale infrastructure.

Sustainability initiatives offer opportunities for operators to differentiate their services through renewable energy integration, energy-efficient technologies, and carbon-neutral operations. Organizations increasingly prioritize environmental considerations in their infrastructure decisions, creating market opportunities for green data center solutions and sustainable hosting services.

Hybrid cloud services represent a growing opportunity as enterprises seek to balance the benefits of public cloud services with the control and security of private infrastructure. Data center operators can capitalize on this trend by offering integrated hybrid solutions that seamlessly connect on-premises infrastructure with public cloud services.

Disaster recovery services present significant opportunities given Japan’s geographical challenges and the critical importance of business continuity. Operators can develop specialized disaster-resilient infrastructure and comprehensive backup solutions that address the unique requirements of Japanese businesses operating in earthquake-prone regions.

Competitive dynamics in Japan’s data center market are characterized by intense competition between domestic operators, international hyperscale providers, and specialized service companies. The market is witnessing consolidation trends as larger operators acquire smaller facilities to expand their geographic coverage and service capabilities, while new entrants focus on niche markets and specialized services.

Technology evolution continues to reshape market dynamics, with operators investing heavily in advanced cooling systems, automation technologies, and energy-efficient infrastructure. The adoption of artificial intelligence for data center management and predictive maintenance is improving operational efficiency and reducing costs, creating competitive advantages for technologically advanced operators.

Customer expectations are evolving rapidly, with organizations demanding higher levels of service reliability, security, and performance from their data center providers. This trend is driving operators to invest in premium service offerings and advanced monitoring capabilities to meet increasingly sophisticated customer requirements.

Supply chain considerations have become increasingly important, particularly following global disruptions that highlighted the importance of resilient infrastructure supply chains. Data center operators are focusing on supply chain diversification and local sourcing strategies to ensure reliable equipment availability and reduce dependency on single suppliers or regions.

Comprehensive market analysis of Japan’s data center sector employs multiple research methodologies to ensure accuracy and reliability of findings. Primary research involves extensive interviews with industry executives, data center operators, technology vendors, and enterprise customers to gather firsthand insights into market trends, challenges, and opportunities.

Secondary research encompasses analysis of industry reports, government publications, regulatory filings, and company financial statements to validate primary research findings and provide comprehensive market context. MarkWide Research utilizes proprietary databases and analytical frameworks to process and analyze large volumes of market data from multiple sources.

Quantitative analysis involves statistical modeling and trend analysis to identify growth patterns, market correlations, and predictive indicators. This approach enables the development of robust market forecasts and identification of key performance metrics that drive data center market dynamics in Japan.

Qualitative assessment focuses on understanding market nuances, competitive positioning, and strategic implications that quantitative data alone cannot capture. This methodology provides deeper insights into customer behavior, technology adoption patterns, and market evolution trends that shape the Japanese data center landscape.

Tokyo metropolitan area dominates Japan’s data center market, accounting for approximately 65% of total capacity and serving as the primary hub for international connectivity and financial services infrastructure. The region benefits from excellent telecommunications infrastructure, proximity to major enterprises, and access to skilled technical workforce, making it the preferred location for hyperscale operators and enterprise data centers.

Osaka region represents the second-largest data center market in Japan, capturing approximately 20% market share and serving as an important backup location for Tokyo-based operations. The region’s strategic position in western Japan, combined with lower real estate costs and government incentives, is attracting increased investment from both domestic and international data center operators.

Nagoya area is emerging as a significant data center hub, particularly for manufacturing and automotive industry applications. The region’s industrial base and strategic location between Tokyo and Osaka create opportunities for specialized data center services supporting Industry 4.0 initiatives and manufacturing digitalization efforts.

Regional markets including Fukuoka, Sendai, and Sapporo are experiencing growing demand for data center services, driven by local economic development and the need for distributed infrastructure to support edge computing applications. These markets offer opportunities for operators to establish regional presence and serve local enterprise customers with specialized requirements.

Market leadership in Japan’s data center sector is shared among several key categories of operators, each bringing unique strengths and capabilities to the market:

Competitive strategies focus on geographic expansion, service diversification, and technology innovation to capture market share and differentiate service offerings. Operators are investing heavily in sustainability initiatives, edge computing capabilities, and hybrid cloud solutions to meet evolving customer demands and maintain competitive positioning.

By Facility Type:

By Service Type:

By End-User Industry:

Colocation services continue to dominate Japan’s data center market, with enterprises increasingly preferring shared infrastructure solutions over building proprietary facilities. This segment benefits from cost optimization advantages, professional management capabilities, and access to advanced technologies that individual organizations might find difficult to implement independently.

Hyperscale facilities are experiencing rapid growth driven by cloud service adoption and digital transformation initiatives. These large-scale operations offer economies of scale and advanced automation capabilities that enable efficient service delivery and competitive pricing for cloud-based applications and services.

Edge computing infrastructure represents the fastest-growing segment, with deployment rates increasing approximately 30% annually as 5G networks enable new applications requiring ultra-low latency processing. This category is particularly important for autonomous vehicles, smart city applications, and industrial IoT implementations.

Managed services are gaining traction as organizations seek to focus on core business activities while outsourcing IT infrastructure management to specialized providers. This segment offers opportunities for data center operators to provide value-added services and develop long-term customer relationships beyond basic infrastructure provision.

Enterprise customers benefit from access to world-class infrastructure without the substantial capital investments required for building and maintaining proprietary data centers. Organizations can leverage professional expertise, advanced security measures, and scalable resources that enable them to focus on core business activities while ensuring reliable IT operations.

Data center operators benefit from strong market demand, recurring revenue models, and opportunities for service expansion and geographic growth. The market offers stable cash flows from long-term customer contracts and opportunities to develop specialized services that command premium pricing.

Technology vendors benefit from substantial demand for advanced data center equipment, software solutions, and professional services. The market’s focus on energy efficiency and automation creates opportunities for innovative technology providers to develop and deploy cutting-edge solutions.

Government stakeholders benefit from enhanced digital infrastructure that supports economic development, innovation, and competitiveness. Robust data center infrastructure enables digital government initiatives and supports the broader digital transformation of Japanese society and economy.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability transformation is becoming a defining trend in Japan’s data center market, with operators increasingly adopting renewable energy sources, implementing advanced cooling technologies, and pursuing carbon neutrality goals. This trend is driven by both regulatory requirements and customer demands for environmentally responsible infrastructure solutions.

Edge computing proliferation represents a fundamental shift in data center architecture, with operators developing distributed networks of smaller facilities positioned closer to end users. This trend is accelerating with 5G deployment and the growth of applications requiring ultra-low latency processing capabilities.

Artificial intelligence integration is transforming data center operations through predictive maintenance, automated resource management, and intelligent cooling optimization. AI-powered systems are enabling operators to achieve efficiency improvements of up to 15% while reducing operational costs and improving service reliability.

Hybrid cloud adoption is driving demand for data center services that seamlessly integrate with public cloud platforms. Organizations are seeking flexible infrastructure solutions that enable them to optimize workload placement between on-premises and cloud environments based on performance, cost, and compliance requirements.

Major capacity expansions by hyperscale operators are reshaping Japan’s data center landscape, with significant investments in new facilities and infrastructure upgrades. These developments are enhancing Japan’s position as a regional hub for cloud services and digital infrastructure.

Strategic partnerships between telecommunications operators and data center providers are creating integrated service offerings that combine connectivity, infrastructure, and managed services. These collaborations are enabling more comprehensive solutions for enterprise customers seeking end-to-end digital infrastructure support.

Technology innovations in cooling systems, power management, and automation are improving data center efficiency and reducing environmental impact. MarkWide Research analysis indicates that these technological advances are enabling operators to achieve significant improvements in power usage effectiveness and operational efficiency.

Regulatory developments including updated data protection requirements and cybersecurity standards are influencing data center design and operations. These changes are creating opportunities for operators to differentiate their services through enhanced security and compliance capabilities.

Investment prioritization should focus on sustainable technologies and edge computing infrastructure to capitalize on emerging market opportunities. Operators should consider renewable energy integration and energy-efficient technologies as essential components of long-term competitive strategy rather than optional enhancements.

Geographic diversification beyond the Tokyo metropolitan area presents opportunities for growth and risk mitigation. Operators should evaluate secondary markets in Osaka, Nagoya, and other regional centers as potential locations for expansion and customer base diversification.

Service portfolio expansion into managed services, hybrid cloud solutions, and specialized industry applications can create additional revenue streams and strengthen customer relationships. Organizations should focus on developing value-added services that differentiate their offerings in an increasingly competitive market.

Partnership strategies with technology vendors, telecommunications providers, and cloud service companies can enhance service capabilities and market reach. Strategic alliances can provide access to complementary technologies and customer bases that support growth and competitive positioning.

Long-term growth prospects for Japan’s data center market remain highly positive, supported by continued digital transformation, 5G deployment, and the increasing importance of data-driven business operations. MWR projects that the market will maintain robust growth trajectory over the next decade, driven by both domestic demand and Japan’s role as a regional digital hub.

Technology evolution will continue to shape market dynamics, with edge computing, artificial intelligence, and quantum computing creating new requirements for specialized data center infrastructure. Operators that successfully adapt to these technological changes will be best positioned to capture emerging market opportunities and maintain competitive advantages.

Sustainability requirements will become increasingly important, with carbon neutrality and environmental responsibility becoming essential criteria for customer selection of data center providers. The market will likely see continued investment in renewable energy solutions and energy-efficient technologies as standard operational requirements.

Market consolidation trends may accelerate as operators seek to achieve economies of scale and expand service capabilities through acquisitions and strategic partnerships. This consolidation could create opportunities for specialized operators while potentially reducing the number of independent facilities in certain market segments.

Japan’s data center market stands at the forefront of global digital infrastructure development, characterized by technological sophistication, robust demand growth, and strategic importance for the broader digital economy. The market’s evolution reflects Japan’s commitment to digital transformation and its position as a technology leader in the Asia-Pacific region.

Market fundamentals remain strong, supported by continued enterprise digitalization, government initiatives promoting digital society development, and the increasing adoption of cloud computing and advanced technologies. The combination of domestic demand growth and Japan’s role as a regional hub for international operations creates a compelling investment environment for data center operators and technology providers.

Future success in Japan’s data center market will depend on operators’ ability to adapt to evolving customer requirements, embrace sustainable technologies, and develop innovative service offerings that address the unique needs of Japanese businesses and international organizations operating in the region. The market’s continued growth and evolution position it as a critical component of Japan’s digital infrastructure and economic competitiveness in the global marketplace.

What is Data Center in Japan?

A Data Center in Japan refers to a facility used to house computer systems and associated components, such as telecommunications and storage systems. These centers are critical for managing data and applications for various industries, including finance, healthcare, and technology.

What are the key players in the Data Center in Japan Market?

Key players in the Data Center in Japan Market include NTT Communications, KDDI Corporation, and Equinix, which provide a range of services from colocation to cloud solutions. These companies are pivotal in supporting the growing demand for data storage and processing capabilities in Japan, among others.

What are the growth factors driving the Data Center in Japan Market?

The Data Center in Japan Market is driven by factors such as the increasing demand for cloud computing services, the rise of big data analytics, and the expansion of IoT applications. Additionally, the need for enhanced data security and compliance with regulations is propelling market growth.

What challenges does the Data Center in Japan Market face?

Challenges in the Data Center in Japan Market include high operational costs, limited space in urban areas, and the need for advanced cooling technologies. Additionally, regulatory compliance and the rapid pace of technological change pose significant hurdles for operators.

What opportunities exist in the Data Center in Japan Market?

Opportunities in the Data Center in Japan Market include the growing demand for hybrid cloud solutions and the potential for green data centers that focus on sustainability. Furthermore, advancements in AI and machine learning can enhance operational efficiency and service offerings.

What trends are shaping the Data Center in Japan Market?

Trends shaping the Data Center in Japan Market include the shift towards edge computing, increased investment in renewable energy sources, and the adoption of advanced cooling technologies. Additionally, the integration of AI for data management and operational efficiency is becoming more prevalent.

Data Center in Japan Market

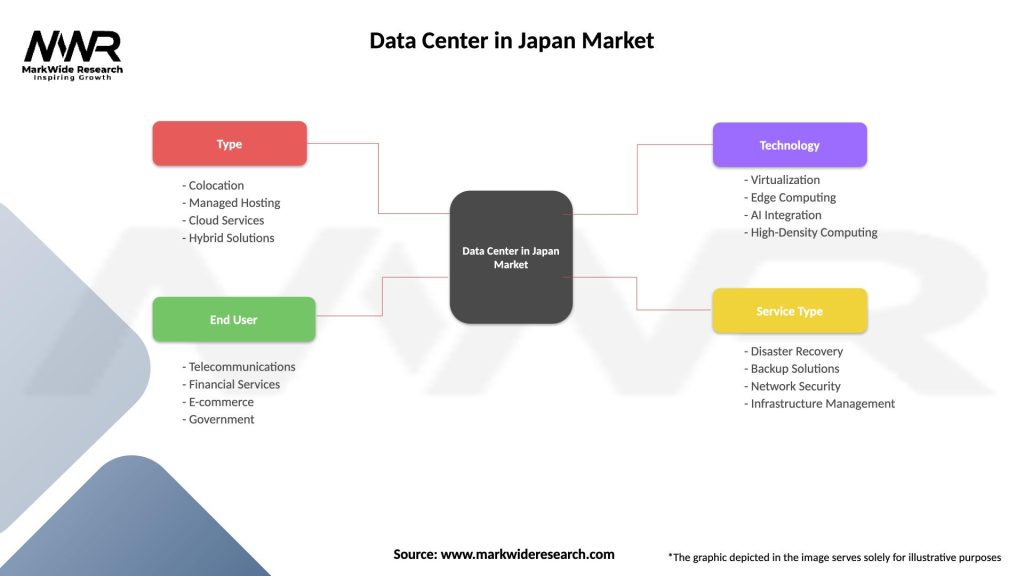

| Segmentation Details | Description |

|---|---|

| Type | Colocation, Managed Hosting, Cloud Services, Hybrid Solutions |

| End User | Telecommunications, Financial Services, E-commerce, Government |

| Technology | Virtualization, Edge Computing, AI Integration, High-Density Computing |

| Service Type | Disaster Recovery, Backup Solutions, Network Security, Infrastructure Management |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Data Center in Japan Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.