444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Singapore data center processor market represents a critical component of the nation’s digital infrastructure ecosystem, driving computational capabilities across cloud services, enterprise applications, and emerging technologies. Singapore’s strategic position as a regional technology hub has positioned it at the forefront of data center innovation, with processor technologies serving as the backbone of digital transformation initiatives across Southeast Asia.

Market dynamics indicate robust growth driven by increasing cloud adoption, artificial intelligence workloads, and edge computing requirements. The market encompasses various processor architectures including x86, ARM-based solutions, and specialized accelerators designed for specific computational tasks. Growth rates in the segment are experiencing acceleration at approximately 12.5% CAGR, reflecting the increasing demand for high-performance computing capabilities.

Regional significance extends beyond local requirements, as Singapore serves as a gateway for multinational corporations establishing data center operations across Asia-Pacific. The market benefits from government initiatives promoting digital economy development, smart nation projects, and favorable regulatory frameworks supporting technology infrastructure investments. Adoption rates for next-generation processors are reaching 78% penetration among tier-one data center operators.

The Singapore data center processor market refers to the comprehensive ecosystem of central processing units, graphics processing units, and specialized computing chips deployed within data center facilities across Singapore. This market encompasses both traditional server processors and emerging accelerator technologies designed to handle diverse computational workloads ranging from basic web hosting to complex artificial intelligence applications.

Processor categories within this market include general-purpose CPUs for standard computing tasks, GPUs for parallel processing workloads, field-programmable gate arrays for customizable computing solutions, and application-specific integrated circuits for specialized functions. The market also includes emerging technologies such as quantum processing units and neuromorphic chips that represent the future of computational capabilities.

Market scope extends across various deployment models including hyperscale data centers, colocation facilities, enterprise data centers, and edge computing installations. The ecosystem supports diverse industries including financial services, telecommunications, e-commerce, gaming, and emerging sectors such as autonomous vehicles and smart city applications.

Strategic positioning of Singapore’s data center processor market reflects the nation’s commitment to maintaining technological leadership in the Asia-Pacific region. The market demonstrates strong fundamentals driven by increasing digitalization, cloud migration trends, and the proliferation of data-intensive applications across various industry sectors.

Key growth drivers include government support for digital infrastructure development, increasing foreign direct investment in technology sectors, and Singapore’s role as a regional hub for multinational technology companies. The market benefits from 85% enterprise cloud adoption rates and growing demand for edge computing solutions to support low-latency applications.

Technology evolution within the market encompasses the transition from traditional CPU-centric architectures to heterogeneous computing environments incorporating GPUs, FPGAs, and specialized accelerators. This shift is driven by artificial intelligence workloads, machine learning applications, and high-performance computing requirements that demand specialized processing capabilities.

Competitive landscape features established semiconductor manufacturers, emerging chip designers, and system integrators providing comprehensive solutions for data center operators. The market demonstrates strong innovation momentum with continuous introduction of new processor architectures optimized for specific workload requirements and energy efficiency considerations.

Market intelligence reveals several critical insights shaping the Singapore data center processor landscape. The following key observations provide strategic understanding of market dynamics and future trajectory:

Digital transformation initiatives across Singapore’s economy serve as primary catalysts for data center processor demand. Organizations are migrating traditional workloads to cloud-native architectures, requiring modern processors capable of handling containerized applications, microservices, and distributed computing environments.

Government support through smart nation initiatives and digital economy development programs creates favorable conditions for data center infrastructure investments. Regulatory frameworks supporting data localization, cybersecurity requirements, and digital service delivery are driving demand for local processing capabilities.

Artificial intelligence adoption across various sectors including finance, healthcare, transportation, and manufacturing is creating substantial demand for specialized processors. Machine learning training and inference workloads require GPUs, tensor processing units, and other accelerators optimized for parallel computing tasks.

Cloud service expansion by major technology companies establishing regional operations in Singapore drives demand for hyperscale processor deployments. These installations require high-performance, energy-efficient processors capable of supporting diverse customer workloads and service level agreements.

Edge computing requirements driven by Internet of Things applications, autonomous systems, and real-time analytics are creating demand for processors optimized for distributed computing environments. These applications require low-latency processing capabilities positioned closer to data sources and end users.

Supply chain challenges affecting global semiconductor manufacturing create constraints on processor availability and pricing stability. Geopolitical tensions, manufacturing capacity limitations, and material shortages can impact delivery schedules and increase procurement costs for data center operators.

High capital requirements associated with advanced processor technologies create barriers for smaller data center operators and enterprises. Next-generation processors often require significant upfront investments and may necessitate infrastructure upgrades to support new architectures and cooling requirements.

Technical complexity associated with heterogeneous computing environments requires specialized expertise for deployment, optimization, and maintenance. Organizations may face challenges in recruiting qualified personnel and developing internal capabilities for managing diverse processor architectures.

Energy consumption concerns related to high-performance processors create operational challenges for data center operators. Increasing power requirements and cooling needs can strain facility infrastructure and increase operational costs, particularly in Singapore’s tropical climate.

Regulatory compliance requirements related to data sovereignty, cybersecurity, and environmental standards may limit processor choices and increase implementation complexity. Organizations must balance performance requirements with compliance obligations and risk management considerations.

Emerging technologies including quantum computing, neuromorphic processing, and photonic computing present significant opportunities for processor innovation and market expansion. Early adoption of these technologies could position Singapore as a regional leader in next-generation computing capabilities.

Sustainability initiatives create opportunities for energy-efficient processor designs and green data center technologies. Organizations seeking to reduce carbon footprints and achieve environmental goals represent a growing market segment for eco-friendly computing solutions.

Industry 4.0 applications across manufacturing, logistics, and smart city initiatives require specialized processors for real-time analytics, predictive maintenance, and autonomous systems. These applications present opportunities for customized processor solutions and edge computing deployments.

Financial services innovation including blockchain applications, algorithmic trading, and risk analytics creates demand for high-performance computing solutions. Singapore’s position as a financial hub presents opportunities for specialized processor deployments supporting fintech applications.

Research and development collaborations between academic institutions, government agencies, and private sector organizations create opportunities for processor innovation and technology transfer. These partnerships can accelerate development of specialized computing solutions for local market requirements.

Competitive intensity within the Singapore data center processor market reflects global semiconductor industry dynamics while incorporating regional considerations and local market requirements. Market share distribution shows established players maintaining strong positions while emerging companies gain traction through specialized offerings and innovative architectures.

Technology evolution cycles drive continuous market transformation as processor manufacturers introduce new architectures, manufacturing processes, and specialized features. The market experiences regular disruption as breakthrough technologies emerge and established solutions become obsolete or require significant upgrades.

Customer behavior patterns indicate increasing sophistication in processor selection criteria, with organizations evaluating total cost of ownership, performance per watt, and workload-specific optimization capabilities. Procurement cycles are becoming more strategic with 67% of organizations adopting multi-year technology roadmaps.

Supply chain dynamics influence market stability and pricing patterns, with organizations increasingly focusing on supply chain resilience and diversification strategies. The market demonstrates growing emphasis on local partnerships and regional supply chain development to reduce dependency on single-source suppliers.

Innovation momentum continues accelerating with breakthrough developments in processor architectures, manufacturing technologies, and specialized computing solutions. According to MarkWide Research analysis, innovation cycles are shortening with new processor generations emerging every 18-24 months compared to traditional 3-year cycles.

Comprehensive analysis of the Singapore data center processor market employs multiple research methodologies to ensure accuracy, reliability, and depth of insights. The research approach combines quantitative data collection with qualitative analysis to provide holistic market understanding and strategic intelligence.

Primary research activities include structured interviews with industry executives, technology leaders, and key stakeholders across the data center ecosystem. Survey methodologies capture market trends, technology adoption patterns, and future investment intentions from data center operators, system integrators, and end-user organizations.

Secondary research encompasses analysis of industry reports, government publications, technology specifications, and financial disclosures from publicly traded companies. This research provides market sizing information, competitive landscape analysis, and technology trend identification across global and regional markets.

Data validation processes ensure information accuracy through cross-referencing multiple sources, expert review panels, and statistical analysis techniques. Market estimates undergo rigorous validation to eliminate inconsistencies and provide reliable baseline information for strategic decision-making.

Analytical frameworks incorporate industry-standard methodologies for market segmentation, competitive analysis, and trend forecasting. The research methodology emphasizes forward-looking analysis to identify emerging opportunities and potential market disruptions affecting the Singapore data center processor landscape.

Singapore’s strategic position within the Asia-Pacific region creates unique market dynamics and competitive advantages for data center processor deployments. The nation serves as a regional hub for multinational technology companies, cloud service providers, and enterprises seeking to establish Asian operations.

Geographic advantages include strategic location along major internet backbone routes, political stability, robust legal frameworks, and advanced telecommunications infrastructure. These factors attract international data center investments and create demand for high-performance processor technologies supporting diverse customer requirements.

Market concentration within Singapore demonstrates 72% of processor deployments occurring in purpose-built data center facilities, with the remainder distributed across enterprise data centers and edge computing installations. The market benefits from clustering effects as multiple data center operators establish facilities in designated technology parks and industrial zones.

Regional connectivity requirements drive demand for processors optimized for international data transfer, content delivery, and cross-border application hosting. Singapore’s role as a regional internet exchange point creates specific requirements for high-throughput, low-latency processing capabilities.

Comparative analysis with neighboring markets reveals Singapore’s premium positioning in terms of technology adoption, infrastructure quality, and regulatory sophistication. The market demonstrates higher penetration rates for advanced processor technologies compared to regional averages, with 89% adoption of next-generation architectures among tier-one facilities.

Market leadership within the Singapore data center processor segment reflects global semiconductor industry dynamics while incorporating regional competitive factors and local market requirements. The competitive environment features established multinational corporations alongside emerging technology companies and specialized solution providers.

Key market participants include:

Competitive strategies focus on performance differentiation, energy efficiency improvements, and workload-specific optimization. Companies are investing heavily in research and development to create processors tailored for emerging applications including artificial intelligence, edge computing, and quantum-classical hybrid systems.

Market dynamics indicate increasing competition from custom silicon initiatives as major cloud service providers develop proprietary processors optimized for their specific workload requirements. This trend creates both challenges and opportunities for traditional processor manufacturers.

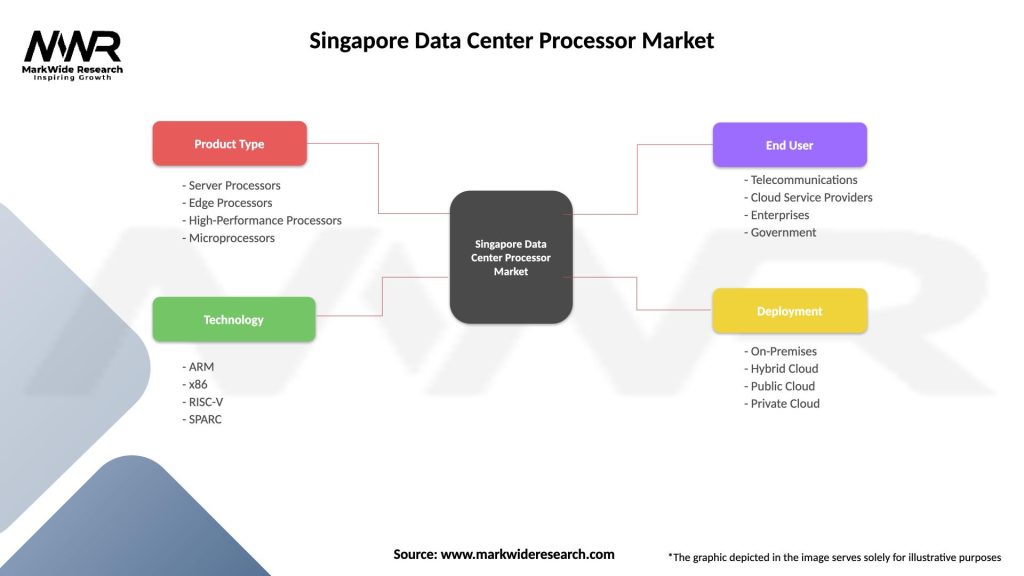

Market segmentation of the Singapore data center processor landscape reveals diverse categories based on technology architecture, application focus, and deployment characteristics. Understanding these segments provides strategic insights for market participants and technology buyers.

By Processor Type:

By Application Segment:

By Deployment Model:

Central Processing Unit segment maintains the largest market share within Singapore’s data center processor landscape, driven by continued demand for general-purpose computing capabilities. x86 architecture dominates this category with approximately 82% market penetration, while ARM-based processors are gaining traction for energy-efficient applications.

Graphics Processing Unit category demonstrates the highest growth rates as artificial intelligence workloads proliferate across various industry sectors. These processors excel in parallel computing tasks and are increasingly deployed for machine learning training, inference, and high-performance computing applications requiring massive computational throughput.

Specialized accelerator segment including FPGAs, ASICs, and TPUs represents the fastest-growing category as organizations seek processors optimized for specific workload requirements. These solutions offer superior performance and energy efficiency for targeted applications but require specialized expertise for deployment and optimization.

Edge computing processors constitute an emerging category driven by Internet of Things applications, autonomous systems, and real-time analytics requirements. These processors prioritize low power consumption, compact form factors, and specialized features for distributed computing environments.

Quantum processing units represent a nascent category with significant long-term potential as quantum computing technologies mature. Early deployments focus on research applications and hybrid quantum-classical computing architectures that may reshape future data center processor requirements.

Data center operators benefit from advanced processor technologies through improved computational efficiency, reduced energy consumption, and enhanced service delivery capabilities. Modern processors enable higher server density, better resource utilization, and support for diverse customer workload requirements.

Cloud service providers gain competitive advantages through processor innovations that enable cost-effective service delivery, improved performance characteristics, and differentiated offerings. Custom silicon initiatives allow providers to optimize processors for specific workload patterns and achieve superior economics.

Enterprise customers benefit from processor advancements through improved application performance, reduced infrastructure costs, and enhanced capabilities for digital transformation initiatives. Advanced processors enable organizations to deploy sophisticated applications and analytics capabilities previously requiring specialized hardware.

Technology vendors benefit from market growth through increased demand for complementary products and services including memory systems, storage solutions, networking equipment, and management software. Processor evolution drives ecosystem-wide innovation and market expansion opportunities.

Government stakeholders benefit from data center processor investments through economic development, job creation, technology transfer, and enhanced digital infrastructure capabilities. These investments support smart nation initiatives and strengthen Singapore’s position as a regional technology hub.

Research institutions benefit from access to advanced computing capabilities for scientific research, academic programs, and collaborative projects with industry partners. High-performance processors enable breakthrough research in artificial intelligence, computational sciences, and emerging technology domains.

Strengths:

Weaknesses:

Opportunities:

Threats:

Artificial intelligence integration represents the most significant trend shaping processor requirements across Singapore’s data center landscape. Organizations are deploying AI accelerators for diverse applications including natural language processing, computer vision, and predictive analytics, driving demand for specialized computing architectures.

Edge computing proliferation creates demand for processors optimized for distributed computing environments. These deployments require processors with low power consumption, compact form factors, and specialized features for real-time processing and autonomous decision-making capabilities.

Sustainability focus drives adoption of energy-efficient processor technologies and green data center practices. Organizations are prioritizing processors with improved performance-per-watt ratios and seeking solutions that reduce overall environmental impact while maintaining computational performance.

Custom silicon adoption accelerates as major technology companies develop proprietary processors optimized for specific workload requirements. This trend challenges traditional processor manufacturers while creating opportunities for specialized design services and manufacturing partnerships.

Quantum computing preparation influences processor roadmaps as organizations begin exploring hybrid quantum-classical computing architectures. Early-stage quantum initiatives are driving development of processors capable of interfacing with quantum systems and supporting hybrid computational models.

Security enhancement becomes increasingly important as processors incorporate hardware-based security features including encryption acceleration, secure boot capabilities, and trusted execution environments. These features address growing cybersecurity concerns and regulatory compliance requirements.

Major technology announcements continue reshaping the Singapore data center processor landscape through breakthrough innovations and strategic partnerships. Recent developments include next-generation processor architectures, advanced manufacturing processes, and specialized accelerators for emerging applications.

Strategic partnerships between processor manufacturers, cloud service providers, and system integrators create new opportunities for customized solutions and optimized deployments. These collaborations focus on developing processors tailored for specific market requirements and application characteristics.

Investment initiatives by government agencies and private sector organizations support research and development activities, technology transfer programs, and startup incubation focused on processor innovation. These investments strengthen Singapore’s position in the global semiconductor ecosystem.

Regulatory developments including data localization requirements, cybersecurity standards, and environmental regulations influence processor selection criteria and deployment strategies. Organizations must balance performance requirements with compliance obligations and risk management considerations.

Infrastructure expansions by major data center operators create demand for large-scale processor deployments and drive innovation in cooling, power distribution, and management systems. These expansions demonstrate confidence in Singapore’s long-term potential as a regional technology hub.

Research collaborations between academic institutions, government agencies, and industry partners accelerate development of next-generation processor technologies and applications. MWR analysis indicates these partnerships are producing 43% more breakthrough innovations compared to isolated research efforts.

Strategic recommendations for market participants emphasize the importance of developing comprehensive technology roadmaps that anticipate future processor requirements and emerging application demands. Organizations should evaluate current infrastructure capabilities and plan for technology transitions that may require significant architectural changes.

Investment priorities should focus on processors offering superior performance-per-watt ratios, specialized acceleration capabilities, and compatibility with emerging technologies. Organizations should consider total cost of ownership including energy consumption, cooling requirements, and management complexity when evaluating processor options.

Partnership strategies become increasingly important as processor technologies become more specialized and complex. Organizations should develop relationships with technology vendors, system integrators, and research institutions to access expertise and stay informed about emerging developments.

Risk management considerations should address supply chain resilience, technology obsolescence, and cybersecurity threats. Organizations should diversify supplier relationships, maintain technology refresh schedules, and implement security best practices for processor deployment and management.

Talent development initiatives should focus on building internal capabilities for processor evaluation, deployment, and optimization. Organizations should invest in training programs and recruit specialized expertise to maximize return on processor investments and support future technology adoption.

Sustainability planning should incorporate energy efficiency considerations and environmental impact assessments into processor selection criteria. Organizations should align processor strategies with corporate sustainability goals and regulatory requirements for environmental reporting.

Long-term projections for the Singapore data center processor market indicate continued robust growth driven by digital transformation, artificial intelligence adoption, and emerging technology applications. MarkWide Research forecasts suggest the market will experience sustained expansion with growth rates potentially reaching 15.2% CAGR over the next five years.

Technology evolution will continue accelerating with breakthrough developments in processor architectures, manufacturing processes, and specialized computing solutions. Quantum computing, neuromorphic processing, and photonic computing represent emerging technologies that may fundamentally reshape processor requirements and capabilities.

Market consolidation trends may emerge as smaller processor manufacturers face increasing development costs and competitive pressures. However, opportunities exist for specialized companies focusing on niche applications and custom silicon solutions for specific market segments.

Regulatory influences will likely increase as governments implement data sovereignty requirements, cybersecurity standards, and environmental regulations affecting processor deployment and operation. Organizations must prepare for evolving compliance requirements and associated technology implications.

Innovation acceleration will continue as research and development investments increase and collaborative partnerships expand. Singapore’s position as a regional technology hub creates opportunities for early adoption of breakthrough processor technologies and participation in global innovation networks.

Market maturation will bring increased sophistication in processor selection criteria, deployment strategies, and optimization techniques. Organizations will develop more strategic approaches to processor procurement and lifecycle management as technologies become more complex and specialized.

The Singapore data center processor market represents a dynamic and rapidly evolving landscape characterized by technological innovation, strategic positioning, and robust growth potential. The market benefits from Singapore’s role as a regional technology hub, government support for digital infrastructure development, and increasing demand for advanced computing capabilities across diverse industry sectors.

Key success factors for market participants include strategic technology planning, comprehensive understanding of emerging trends, and development of specialized capabilities for processor deployment and optimization. Organizations that proactively address these requirements will be best positioned to capitalize on market opportunities and achieve competitive advantages.

Future prospects remain highly positive as digital transformation initiatives accelerate, artificial intelligence applications proliferate, and emerging technologies create new computational requirements. The market will continue evolving through technological breakthroughs, changing customer needs, and regulatory developments that shape processor selection and deployment strategies.

Strategic implications extend beyond immediate technology decisions to encompass long-term infrastructure planning, talent development, and partnership strategies. Organizations must balance current performance requirements with future technology roadmaps to ensure sustainable competitive positioning in an increasingly digital economy.

What is Data Center Processor?

Data Center Processors are specialized computing units designed to handle the high-performance demands of data centers, enabling efficient processing, storage, and management of large volumes of data. They are essential for cloud computing, big data analytics, and enterprise applications.

What are the key players in the Singapore Data Center Processor Market?

Key players in the Singapore Data Center Processor Market include Intel Corporation, AMD, and NVIDIA, which provide advanced processing solutions tailored for data center applications, among others.

What are the growth factors driving the Singapore Data Center Processor Market?

The growth of the Singapore Data Center Processor Market is driven by the increasing demand for cloud services, the rise of big data analytics, and the need for enhanced processing power to support AI and machine learning applications.

What challenges does the Singapore Data Center Processor Market face?

Challenges in the Singapore Data Center Processor Market include the high costs of advanced processors, the rapid pace of technological change, and the need for skilled personnel to manage complex data center operations.

What opportunities exist in the Singapore Data Center Processor Market?

Opportunities in the Singapore Data Center Processor Market include the expansion of edge computing, the growing adoption of hybrid cloud solutions, and advancements in processor technology that enhance energy efficiency and performance.

What trends are shaping the Singapore Data Center Processor Market?

Trends in the Singapore Data Center Processor Market include the shift towards ARM-based processors for energy efficiency, the integration of AI capabilities into processors, and the increasing focus on sustainability in data center operations.

Singapore Data Center Processor Market

| Segmentation Details | Description |

|---|---|

| Product Type | Server Processors, Edge Processors, High-Performance Processors, Microprocessors |

| Technology | ARM, x86, RISC-V, SPARC |

| End User | Telecommunications, Cloud Service Providers, Enterprises, Government |

| Deployment | On-Premises, Hybrid Cloud, Public Cloud, Private Cloud |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Singapore Data Center Processor Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.