444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The China SLI battery market represents one of the most dynamic and rapidly evolving segments within the global automotive battery industry. Starting, Lighting, and Ignition (SLI) batteries serve as the fundamental power source for conventional vehicles, providing essential electrical energy for engine startup, lighting systems, and ignition processes. China’s position as the world’s largest automotive manufacturer and consumer has positioned its SLI battery market at the forefront of technological innovation and manufacturing excellence.

Market dynamics in China’s SLI battery sector are characterized by intense competition, technological advancement, and evolving consumer preferences. The market encompasses various battery technologies including traditional lead-acid batteries, enhanced flooded batteries (EFB), and absorbent glass mat (AGM) batteries. Manufacturing capabilities in China have reached unprecedented levels, with domestic producers achieving 78% market share in the regional automotive battery segment while maintaining competitive pricing strategies.

Growth trajectories indicate robust expansion driven by increasing vehicle production, replacement market demand, and technological upgrades. The market is experiencing a 6.2% compound annual growth rate, reflecting strong domestic demand and export opportunities. Regional distribution shows concentrated manufacturing in eastern provinces, with 45% of production capacity located in Jiangsu, Zhejiang, and Guangdong provinces.

Industry transformation is evident through the integration of advanced manufacturing processes, quality enhancement initiatives, and environmental compliance measures. Chinese SLI battery manufacturers are increasingly focusing on premium product segments, with AGM battery adoption growing at 12% annually as automotive manufacturers demand higher performance solutions for modern vehicles equipped with start-stop technology and advanced electrical systems.

The China SLI battery market refers to the comprehensive ecosystem encompassing the manufacturing, distribution, and consumption of starting, lighting, and ignition batteries within the Chinese automotive sector. SLI batteries are specialized automotive batteries designed to provide high current bursts for engine starting while maintaining steady power delivery for vehicle lighting and ignition systems throughout the operational lifecycle.

Market scope includes various battery technologies and applications across passenger vehicles, commercial vehicles, motorcycles, and specialty automotive applications. The market encompasses both original equipment manufacturer (OEM) supply chains and aftermarket replacement segments, representing the complete value chain from raw material processing to end-user consumption.

Technological diversity within the market includes conventional flooded lead-acid batteries, maintenance-free sealed batteries, enhanced flooded batteries (EFB), and absorbent glass mat (AGM) batteries. Each technology serves specific vehicle requirements and performance standards, with manufacturers continuously developing enhanced formulations to meet evolving automotive electrical demands.

Geographic coverage spans all Chinese provinces and autonomous regions, with manufacturing concentrated in industrial clusters that benefit from established supply chains, skilled workforce availability, and logistical advantages. The market serves both domestic consumption and international export requirements, positioning China as a global hub for SLI battery production and innovation.

China’s SLI battery market demonstrates exceptional growth potential and technological advancement, driven by the country’s position as the world’s largest automotive market. Market fundamentals remain strong with increasing vehicle production, growing replacement demand, and technological upgrades supporting sustained expansion across all market segments.

Key market drivers include rising vehicle ownership rates, increasing average vehicle age requiring battery replacements, and growing adoption of vehicles with start-stop technology demanding premium battery solutions. Domestic manufacturers have achieved significant market penetration with competitive cost structures enabling both domestic market leadership and international expansion opportunities.

Technology trends show accelerating adoption of advanced battery technologies, with AGM and EFB batteries gaining market share as automotive manufacturers integrate more sophisticated electrical systems. Manufacturing efficiency improvements have enabled Chinese producers to achieve 15% cost advantages compared to international competitors while maintaining quality standards.

Market challenges include raw material price volatility, environmental regulations requiring manufacturing process upgrades, and increasing competition from international brands seeking market share. However, strategic opportunities exist in premium product segments, export market expansion, and technology partnerships with automotive manufacturers developing next-generation vehicle platforms.

Strategic market insights reveal fundamental trends shaping the China SLI battery landscape, providing critical understanding for industry stakeholders and investment decision-making processes.

Primary market drivers propelling China’s SLI battery market expansion encompass automotive industry growth, technological advancement, and evolving consumer preferences that create sustained demand across all market segments.

Automotive production growth serves as the fundamental driver, with China maintaining its position as the world’s largest vehicle manufacturer. Annual vehicle production continues expanding, creating consistent demand for OEM battery supply while establishing the foundation for future replacement market opportunities. Commercial vehicle expansion particularly drives demand for heavy-duty SLI batteries designed for demanding operational environments.

Vehicle electrification trends paradoxically support SLI battery demand as hybrid vehicles require robust 12-volt systems alongside high-voltage traction batteries. Start-stop technology adoption is accelerating across passenger vehicle segments, requiring premium AGM and EFB batteries capable of handling frequent engine cycling without performance degradation.

Replacement market dynamics provide sustainable long-term growth as China’s vehicle fleet ages and requires battery replacement services. Average battery lifespan considerations combined with increasing vehicle ownership rates create predictable replacement cycles supporting aftermarket demand growth.

Export market opportunities are expanding as Chinese manufacturers achieve international quality certifications and establish global distribution networks. Cost competitiveness enables market penetration in price-sensitive international markets while maintaining acceptable profit margins for sustainable business growth.

Market restraints present challenges that could potentially limit growth trajectories and profitability within China’s SLI battery market, requiring strategic responses from industry participants.

Raw material price volatility represents a significant constraint, with lead prices experiencing periodic fluctuations that impact manufacturing costs and profit margins. Supply chain dependencies on global commodity markets create uncertainty in production planning and pricing strategies, particularly affecting smaller manufacturers with limited hedging capabilities.

Environmental regulations are becoming increasingly stringent, requiring substantial investments in manufacturing process upgrades, waste treatment systems, and recycling infrastructure. Compliance costs can be particularly challenging for smaller manufacturers lacking economies of scale to absorb regulatory compliance expenses efficiently.

Intense competition from both domestic and international manufacturers creates pricing pressure that can compress profit margins across all market segments. Market saturation in certain product categories limits opportunities for premium pricing strategies, requiring manufacturers to focus on operational efficiency and cost management.

Technology transition risks exist as automotive manufacturers increasingly adopt electric vehicle platforms that may reduce long-term demand for traditional SLI batteries. Market uncertainty regarding the pace of electrification creates challenges in long-term capacity planning and investment decision-making processes.

Strategic opportunities within China’s SLI battery market present significant potential for growth, innovation, and market expansion across multiple dimensions of the industry value chain.

Premium product segments offer substantial growth potential as automotive manufacturers increasingly specify advanced battery technologies for vehicles equipped with sophisticated electrical systems. AGM battery demand is expanding rapidly, providing opportunities for manufacturers capable of producing high-quality premium products with superior performance characteristics.

Export market expansion represents a major opportunity as Chinese manufacturers leverage cost advantages and quality improvements to penetrate international markets. Emerging market demand in Southeast Asia, Africa, and Latin America provides growth opportunities for manufacturers seeking geographic diversification and revenue expansion.

Technology partnerships with automotive manufacturers create opportunities for collaborative development of next-generation battery solutions tailored to specific vehicle platforms and performance requirements. Innovation collaboration can lead to exclusive supply agreements and premium pricing opportunities for advanced battery technologies.

Aftermarket service expansion offers opportunities to develop comprehensive battery service networks including installation, maintenance, and recycling services. Value-added services can enhance customer relationships while creating additional revenue streams beyond traditional battery manufacturing and distribution.

Market dynamics within China’s SLI battery sector reflect complex interactions between supply and demand factors, technological evolution, and competitive forces that shape industry development and strategic positioning.

Supply chain integration has become increasingly sophisticated, with leading manufacturers developing vertically integrated operations encompassing raw material processing, component manufacturing, and finished product assembly. Manufacturing efficiency improvements have enabled 20% productivity gains over recent years through automation, process optimization, and quality management system implementation.

Demand patterns show seasonal variations aligned with automotive production cycles and replacement market seasonality. Peak demand periods typically occur during spring and autumn months when vehicle maintenance activities increase and extreme weather conditions stress existing battery systems requiring replacement.

Competitive dynamics feature intense rivalry among domestic manufacturers while international brands seek to establish market presence through joint ventures, acquisitions, and direct investment strategies. Market consolidation trends are emerging as larger manufacturers acquire smaller competitors to achieve economies of scale and expand geographic coverage.

Innovation cycles are accelerating as manufacturers invest in research and development to create differentiated products meeting evolving automotive requirements. Technology advancement focuses on improving battery performance, extending service life, and enhancing environmental sustainability through advanced materials and manufacturing processes.

Research methodology employed in analyzing China’s SLI battery market incorporates comprehensive data collection, analysis techniques, and validation processes to ensure accuracy and reliability of market insights and projections.

Primary research involves extensive interviews with industry executives, manufacturing specialists, automotive engineers, and market participants across the entire value chain. Data collection encompasses production statistics, pricing information, technology trends, and competitive positioning analysis from direct industry sources.

Secondary research utilizes government statistics, industry association reports, trade publications, and academic research to supplement primary data collection efforts. Information validation processes ensure data accuracy through cross-referencing multiple sources and expert verification of key findings and market projections.

Analytical frameworks include quantitative modeling for market sizing, growth projections, and trend analysis combined with qualitative assessment of competitive dynamics, regulatory impacts, and technology evolution patterns. Market segmentation analysis provides detailed insights into product categories, application segments, and regional variations within the overall market structure.

Forecasting methodologies incorporate historical trend analysis, regression modeling, and scenario planning to develop robust market projections accounting for various growth drivers and potential constraints affecting future market development.

Regional analysis of China’s SLI battery market reveals significant geographic variations in manufacturing concentration, market demand, and competitive dynamics across different provinces and economic regions.

Eastern China dominates manufacturing activities with Jiangsu Province leading production capacity, hosting major manufacturing facilities from both domestic and international battery producers. Manufacturing clusters in this region benefit from established automotive supply chains, skilled workforce availability, and proximity to major automotive manufacturing centers.

Guangdong Province represents a significant market segment with strong demand from automotive assembly operations and robust aftermarket requirements. Export activities are concentrated in this region, leveraging established logistics infrastructure and international trade relationships to serve global markets.

Northern regions including Beijing, Tianjin, and surrounding areas demonstrate strong market demand driven by commercial vehicle operations and harsh winter conditions that increase battery replacement frequency. Seasonal demand patterns in these regions show pronounced peaks during autumn months as vehicle owners prepare for winter weather conditions.

Western regions present emerging opportunities as economic development and urbanization drive increasing vehicle ownership rates. Market penetration in these areas remains below national averages, providing growth potential for manufacturers developing appropriate distribution networks and service capabilities.

Central China serves as both a manufacturing base and consumption market, with Hubei and Hunan provinces hosting significant battery production facilities while maintaining strong local demand from automotive and commercial vehicle operations.

Competitive landscape analysis reveals a dynamic market structure characterized by strong domestic players, international brand presence, and emerging technology specialists competing across multiple market segments.

Market positioning strategies vary significantly among competitors, with domestic manufacturers typically competing on cost effectiveness and local market knowledge while international brands emphasize technology leadership and premium product quality. Strategic partnerships between manufacturers and automotive companies are becoming increasingly important for securing long-term supply agreements and collaborative technology development opportunities.

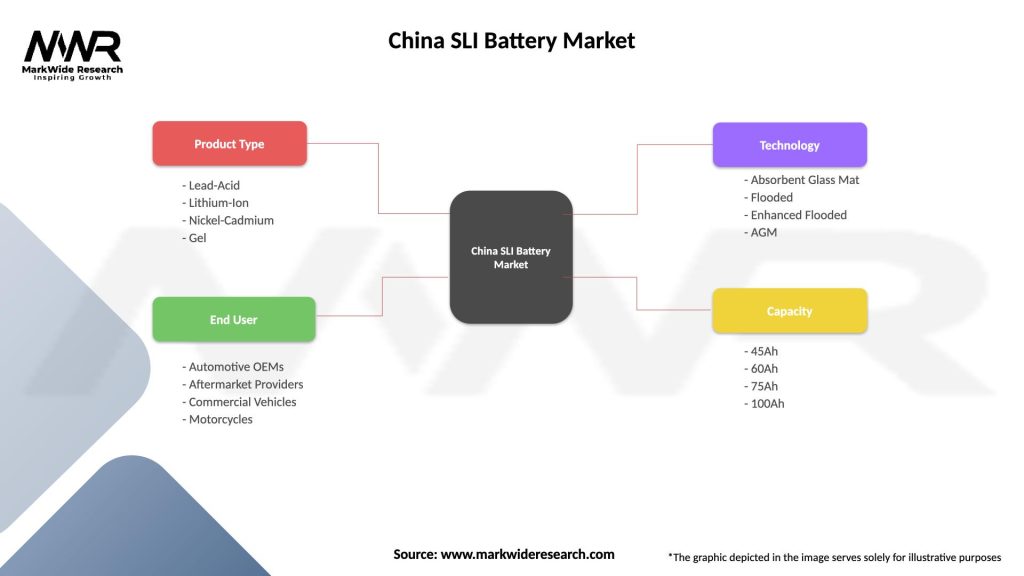

Market segmentation analysis provides detailed insights into the diverse product categories, application segments, and customer groups that comprise China’s comprehensive SLI battery market structure.

By Technology:

By Application:

By Sales Channel:

Category-wise analysis reveals distinct market characteristics, growth patterns, and competitive dynamics across different SLI battery product categories within the Chinese market.

Conventional flooded batteries maintain the largest market share due to cost effectiveness and widespread compatibility with existing vehicle fleets. Price sensitivity in this segment drives intense competition among manufacturers, with success depending on operational efficiency and distribution network effectiveness. Market maturity in this category limits growth potential but provides stable revenue streams for established manufacturers.

AGM battery segment demonstrates the highest growth rates as automotive manufacturers increasingly adopt start-stop technology and advanced electrical systems. Premium positioning enables higher profit margins while requiring significant investment in manufacturing technology and quality control systems. Market penetration is accelerating with luxury vehicle adoption driving demand growth.

EFB battery category represents an emerging opportunity as manufacturers seek cost-effective solutions for start-stop applications without the premium pricing of AGM technology. Technology development in this segment focuses on balancing performance requirements with manufacturing cost considerations to achieve market acceptance.

Commercial vehicle batteries require specialized designs capable of handling demanding operational conditions including extreme temperatures, vibration, and frequent deep discharge cycles. Product differentiation in this segment emphasizes durability, reliability, and service life rather than cost considerations alone.

Industry participants and stakeholders across China’s SLI battery market value chain can realize significant benefits through strategic positioning and market participation in this dynamic and growing sector.

Manufacturers benefit from robust domestic demand providing stable revenue streams while export opportunities enable geographic diversification and revenue growth. Economies of scale achieved through large-scale production enable competitive cost structures supporting both domestic market leadership and international expansion initiatives.

Automotive companies gain access to reliable, cost-effective battery supply chains supporting vehicle production requirements while benefiting from continuous technology advancement and quality improvements. Strategic partnerships with battery manufacturers enable collaborative development of customized solutions meeting specific vehicle platform requirements.

Distributors and retailers benefit from growing aftermarket demand providing sustainable business opportunities with predictable replacement cycles and seasonal demand patterns. Service integration opportunities enable value-added services including installation, testing, and recycling programs that enhance customer relationships and revenue potential.

Investors can participate in a growing market with strong fundamentals, technological advancement, and export growth potential. Market consolidation opportunities exist as the industry matures and smaller manufacturers seek strategic partnerships or acquisition opportunities with larger, well-capitalized competitors.

Technology providers benefit from increasing demand for advanced manufacturing equipment, quality control systems, and recycling technologies as manufacturers upgrade facilities and comply with environmental regulations.

SWOT analysis provides comprehensive evaluation of China’s SLI battery market strengths, weaknesses, opportunities, and threats affecting industry development and competitive positioning.

Strengths:

Weaknesses:

Opportunities:

Threats:

Key market trends shaping China’s SLI battery industry reflect technological evolution, changing consumer preferences, and regulatory developments that influence strategic planning and investment decisions.

Technology advancement trends show accelerating adoption of premium battery technologies as automotive manufacturers integrate more sophisticated electrical systems. AGM technology penetration is increasing rapidly, with market adoption rates growing 18% annually as start-stop technology becomes standard across passenger vehicle segments.

Manufacturing automation is transforming production processes as manufacturers invest in advanced equipment to improve quality consistency, reduce labor costs, and enhance production efficiency. Industry 4.0 integration enables real-time quality monitoring, predictive maintenance, and data-driven process optimization throughout manufacturing operations.

Sustainability initiatives are gaining prominence as manufacturers develop comprehensive recycling programs, implement cleaner production technologies, and pursue environmental certifications. Circular economy principles are being integrated into business models to address regulatory requirements and customer expectations for environmental responsibility.

Digital transformation trends include development of online sales channels, digital customer service platforms, and data analytics capabilities for market intelligence and customer relationship management. E-commerce integration is expanding rapidly in aftermarket segments, providing convenient purchasing options for consumers and service providers.

Quality enhancement remains a persistent trend as manufacturers implement advanced quality management systems, pursue international certifications, and invest in testing equipment to meet evolving customer expectations and regulatory requirements.

Industry developments within China’s SLI battery market demonstrate continuous evolution through technological advancement, strategic partnerships, and market expansion initiatives that reshape competitive dynamics and growth opportunities.

Manufacturing capacity expansion continues across major producers as companies invest in new production facilities and upgrade existing operations to meet growing demand and improve product quality. Automation investments are particularly significant, with leading manufacturers implementing advanced production lines capable of producing premium battery technologies at scale.

Strategic partnerships between battery manufacturers and automotive companies are increasing as both sectors recognize the benefits of collaborative technology development and long-term supply relationships. Joint ventures with international partners provide access to advanced technologies while enabling global market expansion opportunities.

Research and development investments are accelerating as manufacturers focus on next-generation battery technologies, improved materials, and enhanced manufacturing processes. Innovation centers established by major manufacturers are developing solutions for emerging automotive applications including mild hybrid systems and advanced start-stop technologies.

International expansion activities include establishment of overseas manufacturing facilities, distribution partnerships, and acquisition of foreign battery companies to gain market access and technology capabilities. Export growth strategies focus on emerging markets where Chinese manufacturers can leverage cost advantages while building brand recognition.

Environmental compliance initiatives include implementation of advanced recycling systems, cleaner production technologies, and comprehensive environmental management programs addressing regulatory requirements and sustainability objectives.

Strategic recommendations for China’s SLI battery market participants focus on leveraging market opportunities while addressing competitive challenges and positioning for long-term success in an evolving industry landscape.

Technology investment priorities should emphasize advanced battery technologies including AGM and EFB products to capture growing premium market segments. Manufacturing capability development in these technologies requires significant capital investment but offers superior profit margins and competitive differentiation opportunities.

Quality enhancement initiatives remain critical for building brand reputation and enabling international market expansion. Certification pursuit including international quality standards and automotive industry certifications provides credibility for export market penetration and premium customer acquisition.

Market diversification strategies should include both geographic expansion and application segment diversification to reduce dependence on domestic automotive markets. Export market development offers significant growth potential while providing hedge against domestic market fluctuations.

Partnership development with automotive manufacturers, technology providers, and international distributors can accelerate market access and technology advancement. Strategic alliances enable resource sharing, risk mitigation, and accelerated market penetration in competitive segments.

Sustainability integration should be prioritized as environmental regulations become more stringent and customers increasingly value environmental responsibility. Circular economy initiatives including comprehensive recycling programs can create competitive advantages while ensuring regulatory compliance.

Future outlook for China’s SLI battery market indicates continued growth opportunities despite evolving automotive industry dynamics and increasing competition from alternative technologies and international manufacturers.

Market growth projections suggest sustained expansion driven by replacement market demand, technology upgrades, and export opportunities. MarkWide Research analysis indicates the market will maintain robust growth trajectories with compound annual growth rates of 5.8% over the next five years, reflecting strong fundamentals and expanding applications.

Technology evolution will continue favoring advanced battery technologies as automotive electrical systems become more sophisticated. Premium product segments are expected to achieve market share growth of 25% as start-stop technology adoption accelerates and luxury vehicle sales increase across all market segments.

International expansion opportunities will grow as Chinese manufacturers achieve quality improvements and establish global distribution networks. Export market potential in emerging economies provides significant growth opportunities for manufacturers capable of balancing cost competitiveness with quality requirements.

Industry consolidation trends are expected to continue as smaller manufacturers face increasing competitive pressure and seek strategic partnerships or acquisition opportunities with larger, well-capitalized competitors. Market concentration may increase as leading manufacturers achieve greater economies of scale and market coverage.

Sustainability requirements will become increasingly important as environmental regulations evolve and customers demand responsible manufacturing practices. Innovation focus will shift toward developing environmentally sustainable products and manufacturing processes that meet evolving regulatory and customer expectations.

China’s SLI battery market represents a dynamic and rapidly evolving sector with substantial growth potential driven by robust automotive industry fundamentals, technological advancement, and expanding international opportunities. Market leadership by domestic manufacturers provides competitive advantages through cost effectiveness, manufacturing scale, and comprehensive distribution networks serving diverse customer segments.

Strategic opportunities exist across multiple dimensions including premium product development, international market expansion, and technology partnerships that can drive sustainable growth and profitability. Industry transformation toward advanced battery technologies creates opportunities for manufacturers capable of investing in technology development and quality enhancement initiatives.

Competitive dynamics will continue evolving as international manufacturers seek market share while domestic producers focus on quality improvement and global expansion. Success factors include technology leadership, manufacturing efficiency, quality consistency, and strategic partnership development across the automotive value chain.

Long-term outlook remains positive despite challenges from electric vehicle transition and increasing competition. Market fundamentals including replacement demand, export opportunities, and technology advancement provide sustainable growth drivers supporting continued industry development and investment attractiveness for stakeholders across the entire value chain.

What is SLI Battery?

SLI Battery refers to Starting, Lighting, and Ignition batteries, which are primarily used in automotive applications to start engines, power lights, and support ignition systems.

What are the key players in the China SLI Battery Market?

Key players in the China SLI Battery Market include companies like Johnson Controls, Exide Technologies, and Camel Group, among others.

What are the main drivers of growth in the China SLI Battery Market?

The growth of the China SLI Battery Market is driven by the increasing demand for electric vehicles, advancements in battery technology, and the rising automotive production rates.

What challenges does the China SLI Battery Market face?

Challenges in the China SLI Battery Market include intense competition among manufacturers, fluctuating raw material prices, and regulatory pressures regarding environmental standards.

What opportunities exist in the China SLI Battery Market?

Opportunities in the China SLI Battery Market include the expansion of renewable energy storage solutions, the growth of the electric vehicle sector, and innovations in battery recycling technologies.

What trends are shaping the China SLI Battery Market?

Trends in the China SLI Battery Market include the shift towards lithium-ion batteries, increased focus on sustainability, and the integration of smart battery management systems.

China SLI Battery Market

| Segmentation Details | Description |

|---|---|

| Product Type | Lead-Acid, Lithium-Ion, Nickel-Cadmium, Gel |

| End User | Automotive OEMs, Aftermarket Providers, Commercial Vehicles, Motorcycles |

| Technology | Absorbent Glass Mat, Flooded, Enhanced Flooded, AGM |

| Capacity | 45Ah, 60Ah, 75Ah, 100Ah |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the China SLI Battery Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.