444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The United States integrated circuits market represents one of the most dynamic and technologically advanced sectors in the global semiconductor industry. Integrated circuits, commonly known as microchips or chips, serve as the fundamental building blocks of modern electronic devices, powering everything from smartphones and computers to automotive systems and industrial equipment. The market demonstrates robust growth momentum driven by increasing digitalization, artificial intelligence adoption, and the proliferation of Internet of Things (IoT) devices across various industries.

Market dynamics indicate sustained expansion with the sector experiencing a compound annual growth rate (CAGR) of 8.2% over the recent forecast period. This growth trajectory reflects the critical role of integrated circuits in enabling technological innovation and supporting the digital transformation initiatives across multiple sectors. The United States maintains its position as a global leader in integrated circuit design and innovation, housing major semiconductor companies and research institutions that drive technological advancement.

Industry participants benefit from strong domestic demand coupled with significant export opportunities, as American-designed chips power devices worldwide. The market encompasses various segments including microprocessors, memory chips, analog circuits, and specialized application-specific integrated circuits (ASICs), each serving distinct technological requirements and market applications.

The United States integrated circuits market refers to the comprehensive ecosystem encompassing the design, development, manufacturing, and distribution of semiconductor devices within the American territory. Integrated circuits are miniaturized electronic circuits consisting of semiconductor devices and passive components fabricated on a single semiconductor substrate, typically silicon, enabling complex electronic functions in compact form factors.

Market scope includes various categories of integrated circuits such as digital circuits, analog circuits, mixed-signal circuits, and radio frequency (RF) circuits. These components serve as the technological foundation for modern electronic systems, enabling computational processing, data storage, signal amplification, and communication functions across diverse applications ranging from consumer electronics to aerospace and defense systems.

Industry definition encompasses both fabless semiconductor companies that focus on design and intellectual property development, as well as integrated device manufacturers (IDMs) that handle both design and fabrication processes. The market also includes foundry services, packaging and testing operations, and supporting ecosystem participants that contribute to the integrated circuit value chain.

Strategic analysis reveals the United States integrated circuits market as a cornerstone of technological innovation and economic competitiveness. The sector demonstrates exceptional resilience and adaptability, continuously evolving to meet emerging technological demands while maintaining leadership in critical areas such as microprocessor design, graphics processing units, and specialized semiconductor solutions.

Key performance indicators highlight the market’s strength with domestic companies capturing approximately 47% of global market share in semiconductor design and intellectual property. The industry benefits from substantial research and development investments, with leading companies allocating 15-20% of revenues to innovation initiatives that drive next-generation product development and technological breakthroughs.

Market positioning reflects strong competitive advantages including advanced design capabilities, robust intellectual property portfolios, and strategic partnerships with global technology leaders. The sector’s success stems from its ability to anticipate and respond to evolving market demands while maintaining technological leadership in high-performance computing, artificial intelligence, and emerging applications such as autonomous vehicles and edge computing.

Growth trajectory indicates continued expansion driven by digital transformation trends, increasing semiconductor content in traditional industries, and the emergence of new application areas requiring specialized integrated circuit solutions. The market benefits from supportive government policies and initiatives aimed at strengthening domestic semiconductor capabilities and reducing supply chain dependencies.

Market intelligence reveals several critical insights that shape the United States integrated circuits landscape:

Primary growth drivers propelling the United States integrated circuits market include the accelerating pace of digital transformation across industries and the increasing semiconductor content in traditional products. Artificial intelligence and machine learning applications create substantial demand for specialized processors and accelerators, while the expansion of cloud computing infrastructure drives requirements for high-performance server processors and memory solutions.

Automotive electrification represents a significant growth catalyst, with electric vehicles requiring sophisticated power management integrated circuits, battery management systems, and advanced driver assistance system (ADAS) components. The transition toward autonomous vehicles further amplifies semiconductor demand, requiring powerful processing capabilities and sensor interface circuits that enable real-time decision-making and environmental perception.

Internet of Things proliferation creates demand for low-power, cost-effective integrated circuits that enable connectivity and processing in edge devices. Smart home systems, industrial IoT applications, and wearable devices require specialized microcontrollers and wireless communication chips that balance performance requirements with power efficiency constraints.

5G network deployment drives demand for radio frequency integrated circuits, baseband processors, and infrastructure components that enable high-speed wireless communication. The technology transition creates opportunities for companies specializing in millimeter-wave circuits and advanced signal processing solutions that support next-generation wireless standards.

Significant challenges facing the United States integrated circuits market include the substantial capital requirements for advanced manufacturing facilities and the increasing complexity of semiconductor design processes. Fabrication costs for leading-edge process nodes require investments exceeding several billion dollars, creating barriers to entry and limiting the number of companies capable of manufacturing the most advanced integrated circuits.

Supply chain vulnerabilities have become increasingly apparent, with dependencies on overseas manufacturing and raw material suppliers creating potential disruptions to production and delivery schedules. Geopolitical tensions and trade restrictions further complicate global supply chain management, requiring companies to develop alternative sourcing strategies and consider reshoring manufacturing operations.

Talent shortages in specialized areas such as analog circuit design, verification engineering, and advanced packaging technologies constrain industry growth and innovation capabilities. The highly technical nature of semiconductor development requires extensive education and experience, creating challenges in rapidly scaling engineering teams to meet market demands.

Regulatory compliance requirements related to export controls, cybersecurity standards, and environmental regulations increase operational complexity and costs. Companies must navigate evolving regulatory landscapes while maintaining competitive positioning and market access in global markets.

Emerging opportunities in the United States integrated circuits market center around next-generation computing paradigms and specialized application requirements. Quantum computing represents a transformative opportunity, with companies developing quantum processors, control electronics, and supporting integrated circuits that enable quantum information processing and communication systems.

Edge computing applications create demand for specialized processors that balance computational performance with power efficiency, enabling artificial intelligence processing in distributed systems. Neuromorphic computing architectures offer potential for revolutionary advances in energy-efficient processing, mimicking biological neural networks to achieve superior performance in pattern recognition and learning applications.

Healthcare technology integration presents substantial growth opportunities as medical devices become increasingly sophisticated and connected. Biomedical sensors, implantable devices, and diagnostic equipment require specialized integrated circuits that meet stringent safety and reliability requirements while enabling advanced functionality.

Sustainable technology initiatives drive demand for power-efficient integrated circuits and renewable energy system components. Solar inverters, wind turbine controllers, and energy storage systems require specialized power management and control circuits that optimize energy conversion and system performance.

Market dynamics in the United States integrated circuits sector reflect the interplay between technological innovation, competitive pressures, and evolving customer requirements. Innovation cycles continue to accelerate, with companies investing heavily in research and development to maintain competitive advantages and address emerging application requirements.

Competitive landscape dynamics show increasing collaboration between traditional semiconductor companies and technology giants from adjacent industries. Strategic partnerships enable companies to leverage complementary capabilities and access new markets while sharing development costs and risks associated with advanced technology development.

Customer relationships have evolved toward deeper collaboration and co-development arrangements, with semiconductor companies working closely with system manufacturers to optimize integrated circuit designs for specific applications. This approach enables performance optimization and cost reduction while accelerating time-to-market for new products and solutions.

Technology convergence trends blur traditional boundaries between different types of integrated circuits, with system-on-chip (SoC) solutions integrating multiple functions on single devices. This convergence creates opportunities for companies with broad technology portfolios while challenging specialists to expand their capabilities or find strategic partners.

Comprehensive research approach employed in analyzing the United States integrated circuits market combines primary research methodologies with secondary data analysis to provide accurate and actionable market intelligence. Primary research includes extensive interviews with industry executives, technology leaders, and market participants across the semiconductor value chain to gather firsthand insights into market trends, competitive dynamics, and future opportunities.

Secondary research encompasses analysis of company financial reports, patent filings, industry publications, and government data sources to validate primary findings and provide quantitative market insights. Data triangulation techniques ensure accuracy and reliability of market assessments by cross-referencing multiple information sources and analytical approaches.

Market modeling utilizes advanced analytical frameworks to project market trends and quantify growth opportunities across different segments and applications. Scenario analysis considers various market conditions and external factors that could influence market development, providing stakeholders with comprehensive understanding of potential outcomes and strategic implications.

Expert validation processes involve review and verification of research findings by industry experts and technical specialists to ensure accuracy and relevance of market assessments. This collaborative approach enhances the quality and credibility of research outputs while providing valuable perspectives on market dynamics and future trends.

Geographic distribution of the United States integrated circuits market reveals distinct regional strengths and specializations that contribute to overall market leadership. Silicon Valley maintains its position as the global epicenter of semiconductor innovation, hosting major design companies, venture capital firms, and research institutions that drive technological advancement and market development.

West Coast dominance extends beyond California to include significant semiconductor activities in Oregon and Washington, with companies specializing in microprocessors, memory devices, and specialized integrated circuits. The region benefits from 62% concentration of major semiconductor design companies and maintains strong connections to Asian manufacturing partners and supply chains.

East Coast presence includes important semiconductor activities in Massachusetts, New York, and North Carolina, with focus areas including analog circuits, radio frequency devices, and specialized military and aerospace applications. Research triangle regions provide strong university partnerships and government research facilities that support advanced technology development.

Central regions contribute through specialized manufacturing facilities, testing operations, and emerging technology clusters that support the broader semiconductor ecosystem. Texas represents a significant hub for semiconductor manufacturing and assembly operations, with major facilities supporting both domestic and international markets.

Regional collaboration initiatives strengthen the overall market through shared research programs, talent development initiatives, and supply chain coordination efforts. State-level incentives and federal programs support continued investment in domestic semiconductor capabilities and maintain competitive positioning in global markets.

Market leadership in the United States integrated circuits sector is characterized by a diverse ecosystem of companies ranging from large multinational corporations to specialized startups focused on emerging technologies. Competitive dynamics reflect the industry’s innovation-driven nature, with companies competing on technological capabilities, intellectual property portfolios, and ability to anticipate and respond to market trends.

Leading market participants include:

Competitive strategies emphasize continuous innovation, strategic acquisitions, and partnerships that enhance technological capabilities and market reach. Companies invest heavily in research and development while building comprehensive intellectual property portfolios that provide competitive advantages and licensing opportunities.

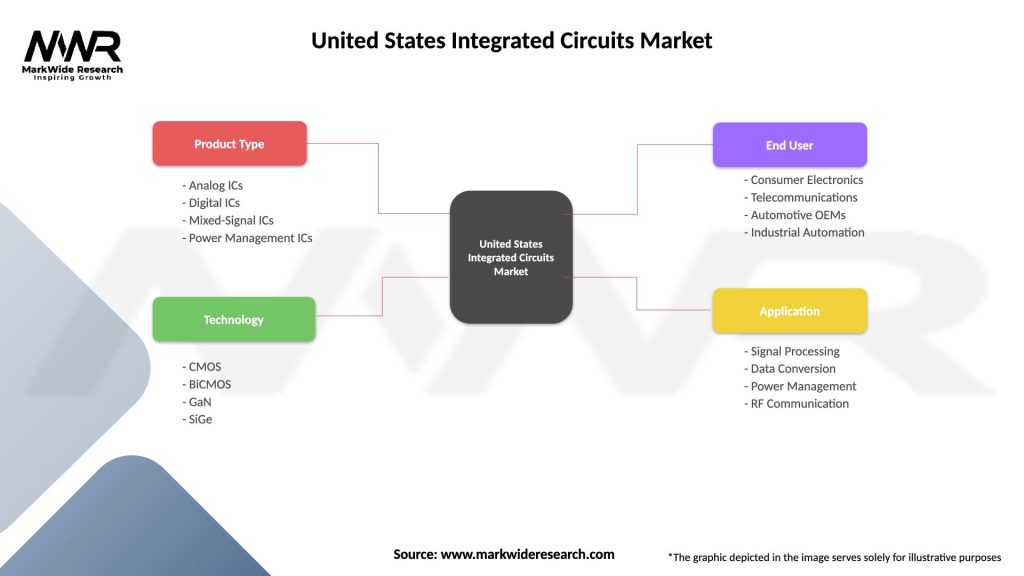

Market segmentation of the United States integrated circuits sector reveals diverse categories serving distinct applications and customer requirements. Product-based segmentation includes digital circuits, analog circuits, mixed-signal devices, and specialized application-specific integrated circuits (ASICs) that address specific market needs and performance requirements.

By Product Type:

By Application Sector:

Microprocessor segment maintains its position as the largest category within the United States integrated circuits market, driven by continuous demand for higher performance computing capabilities and energy-efficient designs. Innovation focus centers on advanced architectures, artificial intelligence acceleration, and specialized processing units that address emerging computational requirements across various applications.

Memory device category experiences strong growth driven by data center expansion, artificial intelligence applications, and increasing storage requirements in consumer and enterprise systems. Technology advancement includes development of next-generation memory technologies such as 3D NAND flash, high-bandwidth memory, and emerging non-volatile memory solutions that offer superior performance characteristics.

Analog circuit segment demonstrates steady growth supported by increasing electronic content in automotive systems, industrial automation, and Internet of Things applications. Market demand focuses on power management solutions, sensor interfaces, and signal conditioning circuits that enable efficient and reliable system operation across diverse environmental conditions.

Application-specific integrated circuits represent a rapidly growing category as companies seek optimized solutions for specific applications and performance requirements. Customization capabilities enable superior performance, reduced power consumption, and cost optimization compared to general-purpose solutions, driving adoption in specialized markets and emerging applications.

Radio frequency circuits experience significant growth driven by 5G network deployment, satellite communication systems, and wireless connectivity requirements in various applications. Technical challenges include managing signal integrity at higher frequencies while maintaining power efficiency and meeting stringent regulatory requirements for wireless communication systems.

Industry participants in the United States integrated circuits market benefit from numerous advantages that support business growth and competitive positioning. Technology leadership provides access to cutting-edge design tools, advanced manufacturing processes, and comprehensive intellectual property resources that enable development of innovative products and solutions.

Market access benefits include proximity to major technology companies, system manufacturers, and end-user markets that facilitate customer relationships and business development opportunities. Ecosystem advantages encompass access to specialized suppliers, service providers, and research institutions that support comprehensive product development and manufacturing capabilities.

Financial advantages include access to venture capital, private equity, and public markets that provide funding for research and development, capacity expansion, and strategic acquisitions. Talent availability from leading universities and experienced professionals supports innovation capabilities and technical expertise development across various specialization areas.

Stakeholder benefits extend to customers who gain access to advanced integrated circuit solutions that enable product differentiation and competitive advantages in their respective markets. Supply chain partners benefit from stable demand and long-term relationships that support business planning and investment decisions.

Regulatory support includes government initiatives that promote domestic semiconductor capabilities, research and development tax incentives, and export promotion programs that facilitate international market access and competitiveness.

Strengths:

Weaknesses:

Opportunities:

Threats:

Artificial intelligence integration represents the most significant trend shaping the United States integrated circuits market, with companies developing specialized processors and accelerators that enable machine learning and deep learning applications. AI-optimized architectures focus on parallel processing capabilities, memory bandwidth optimization, and energy efficiency to support demanding computational workloads across various applications.

Edge computing proliferation drives demand for integrated circuits that balance processing performance with power efficiency, enabling artificial intelligence and data processing capabilities in distributed systems. Edge AI processors incorporate specialized architectures that optimize inference performance while minimizing power consumption and heat generation in space-constrained applications.

Automotive electrification creates substantial opportunities for power management integrated circuits, battery management systems, and motor control solutions that enable efficient electric vehicle operation. Silicon carbide technology adoption increases for high-voltage applications, offering superior efficiency and thermal performance compared to traditional silicon-based solutions.

Heterogeneous integration trends involve combining different types of integrated circuits and technologies in single packages to achieve optimal performance and functionality. Chiplet architectures enable modular designs that reduce development costs while providing flexibility to optimize different functions using appropriate process technologies and design approaches.

Quantum computing development drives innovation in specialized integrated circuits that support quantum processors, control systems, and measurement equipment. Cryogenic electronics require unique design approaches and materials to operate reliably at extremely low temperatures while maintaining precise control and measurement capabilities.

Recent industry developments highlight the dynamic nature of the United States integrated circuits market and the continuous evolution of technology and business strategies. MarkWide Research analysis indicates that major companies have announced substantial investments in domestic manufacturing capabilities, with several new fabrication facilities planned to reduce supply chain dependencies and enhance production capacity.

Strategic acquisitions continue to reshape the competitive landscape as companies seek to acquire specialized technologies, intellectual property, and market access. Consolidation trends focus on combining complementary capabilities and achieving economies of scale in research and development, manufacturing, and market development activities.

Government initiatives include the CHIPS and Science Act, which provides substantial funding for domestic semiconductor manufacturing and research capabilities. Policy support aims to strengthen supply chain resilience, maintain technological leadership, and support innovation in critical semiconductor technologies and applications.

Partnership announcements between semiconductor companies and system manufacturers focus on co-development of optimized solutions for specific applications such as autonomous vehicles, data centers, and 5G infrastructure. Collaborative approaches enable faster time-to-market and better optimization of integrated circuit designs for target applications.

Technology breakthroughs include advances in process technology, packaging innovations, and new materials that enable improved performance and functionality. Research achievements in areas such as neuromorphic computing, quantum electronics, and advanced memory technologies demonstrate continued innovation and future market potential.

Strategic recommendations for United States integrated circuits market participants emphasize the importance of maintaining technological leadership while building resilient supply chains and expanding into emerging application areas. Investment priorities should focus on research and development capabilities, advanced manufacturing technologies, and strategic partnerships that enhance competitive positioning and market access.

Technology development recommendations include continued focus on artificial intelligence acceleration, edge computing solutions, and specialized integrated circuits for automotive and industrial applications. Innovation strategies should emphasize heterogeneous integration, advanced packaging technologies, and energy-efficient designs that address evolving market requirements and performance expectations.

Market expansion opportunities exist in emerging applications such as quantum computing, biomedical devices, and sustainable energy systems that require specialized integrated circuit solutions. Diversification strategies can reduce dependence on traditional markets while capturing growth opportunities in high-value segments with favorable competitive dynamics.

Supply chain optimization should include evaluation of domestic manufacturing options, strategic inventory management, and development of alternative supplier relationships that enhance resilience and reduce geopolitical risks. Risk mitigation strategies should address potential disruptions while maintaining cost competitiveness and operational efficiency.

Talent development initiatives should focus on building specialized capabilities in emerging technology areas while maintaining core competencies in traditional semiconductor design and development. Workforce planning should anticipate future skill requirements and support continuous learning and development programs that enhance technical capabilities and innovation potential.

Long-term prospects for the United States integrated circuits market remain highly positive, supported by continuous technological innovation, expanding application areas, and strong domestic demand across multiple sectors. Growth projections indicate sustained expansion with the market expected to maintain a compound annual growth rate of 7.5% over the next five years, driven by artificial intelligence adoption, automotive electrification, and infrastructure modernization initiatives.

Technology evolution will continue to drive market development with advances in process technology, architectural innovations, and new materials enabling improved performance and functionality. Emerging technologies such as quantum computing, neuromorphic processing, and advanced memory solutions represent significant long-term opportunities for companies with appropriate technical capabilities and market positioning.

Market dynamics will be influenced by increasing focus on supply chain resilience, sustainability requirements, and geopolitical considerations that affect global trade and technology transfer. Domestic manufacturing initiatives are expected to capture approximately 25% of advanced semiconductor production by 2030, reducing dependencies on overseas facilities while maintaining cost competitiveness.

Application diversification will continue as traditional industries integrate more sophisticated electronic systems and new applications emerge in areas such as healthcare technology, smart infrastructure, and environmental monitoring. MWR projections suggest that automotive and industrial applications will represent 35% of total market demand by 2028, reflecting the ongoing electrification and digitalization trends across these sectors.

Competitive landscape evolution will feature continued innovation, strategic partnerships, and potential new entrants from adjacent technology sectors. Success factors will include technological differentiation, customer relationships, intellectual property portfolios, and ability to anticipate and respond to changing market requirements and competitive dynamics.

The United States integrated circuits market stands as a testament to American technological leadership and innovation capabilities, maintaining its position as the global epicenter of semiconductor design and development. Market fundamentals remain strong with robust demand drivers, continuous technological advancement, and expanding application opportunities that support sustained growth and competitive positioning.

Strategic advantages including world-class research institutions, comprehensive talent ecosystems, and access to venture capital and investment funding provide a solid foundation for continued market leadership and innovation. Industry participants benefit from proximity to major technology companies, early adopter markets, and supportive government policies that facilitate business development and international competitiveness.

Future success will depend on maintaining technological leadership while addressing challenges related to supply chain resilience, talent development, and increasing global competition. Investment in domestic manufacturing capabilities, advanced research and development programs, and strategic partnerships will be critical for sustaining competitive advantages and capturing emerging market opportunities.

Market outlook remains highly optimistic with the United States integrated circuits market positioned to benefit from digital transformation trends, artificial intelligence adoption, and the increasing semiconductor content across diverse applications and industries. The sector’s continued evolution and adaptation to changing market requirements ensure its ongoing relevance and importance in the global technology landscape.

What is Integrated Circuits?

Integrated circuits (ICs) are semiconductor devices that combine multiple electronic components into a single chip, enabling complex functions in various applications such as computers, smartphones, and automotive systems.

What are the key players in the United States Integrated Circuits Market?

Key players in the United States Integrated Circuits Market include Intel Corporation, Texas Instruments, and Qualcomm, among others.

What are the main drivers of growth in the United States Integrated Circuits Market?

The growth of the United States Integrated Circuits Market is driven by the increasing demand for consumer electronics, advancements in automotive technology, and the rise of IoT applications.

What challenges does the United States Integrated Circuits Market face?

Challenges in the United States Integrated Circuits Market include supply chain disruptions, rapid technological changes, and increasing competition from global manufacturers.

What opportunities exist in the United States Integrated Circuits Market?

Opportunities in the United States Integrated Circuits Market include the expansion of AI and machine learning applications, growth in renewable energy technologies, and the development of next-generation communication networks.

What trends are shaping the United States Integrated Circuits Market?

Trends in the United States Integrated Circuits Market include the miniaturization of components, the shift towards more energy-efficient designs, and the increasing integration of AI capabilities into ICs.

United States Integrated Circuits Market

| Segmentation Details | Description |

|---|---|

| Product Type | Analog ICs, Digital ICs, Mixed-Signal ICs, Power Management ICs |

| Technology | CMOS, BiCMOS, GaN, SiGe |

| End User | Consumer Electronics, Telecommunications, Automotive OEMs, Industrial Automation |

| Application | Signal Processing, Data Conversion, Power Management, RF Communication |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the United States Integrated Circuits Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.