444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Europe metal caps and closures market represents a vital component of the continent’s packaging industry, serving diverse sectors including food and beverages, pharmaceuticals, cosmetics, and industrial applications. This market encompasses various types of metal closures such as crown caps, aluminum caps, twist-off caps, and specialty closures designed to preserve product integrity and enhance consumer convenience. European manufacturers have established themselves as global leaders in metal closure innovation, combining traditional craftsmanship with advanced manufacturing technologies.

Market dynamics in Europe are characterized by strong demand from the beverage industry, particularly for beer, wine, and premium spirits, where metal closures provide superior barrier properties and aesthetic appeal. The region’s commitment to sustainability has driven significant innovation in recyclable metal closure solutions, with recycling rates for aluminum caps reaching approximately 75% across major European markets. Germany, France, and Italy emerge as the largest consumers of metal caps and closures, collectively accounting for over 60% of regional demand.

Technological advancements continue to reshape the European metal caps and closures landscape, with manufacturers investing heavily in lightweight designs, enhanced barrier coatings, and smart closure technologies. The market demonstrates robust growth potential, driven by increasing consumption of packaged beverages, rising demand for premium packaging solutions, and growing emphasis on product authentication and tamper-evident features. Innovation cycles in the region typically span 18-24 months, reflecting the industry’s commitment to continuous improvement and market responsiveness.

The Europe metal caps and closures market refers to the comprehensive ecosystem of metal-based sealing solutions designed for various packaging applications across European countries. This market encompasses the manufacturing, distribution, and application of metal closures that provide secure sealing, product protection, and consumer convenience for packaged goods. Metal caps and closures serve as critical components in maintaining product freshness, preventing contamination, and ensuring regulatory compliance across multiple industries.

Primary applications include beverage containers, pharmaceutical vials, cosmetic jars, food containers, and industrial packaging solutions. The market includes various closure types such as crown caps for carbonated beverages, aluminum screw caps for wine and spirits, twist-off caps for beer bottles, and specialized closures for pharmaceutical and cosmetic applications. European standards for metal closures emphasize quality, safety, and environmental sustainability, driving continuous innovation in materials, design, and manufacturing processes.

Market participants range from large multinational corporations to specialized regional manufacturers, creating a diverse competitive landscape that fosters innovation and customer-focused solutions. The market’s significance extends beyond mere packaging functionality, encompassing brand differentiation, consumer experience enhancement, and supply chain optimization across the European economic region.

Strategic positioning of the Europe metal caps and closures market reflects strong fundamentals driven by robust demand from key end-use industries and continuous technological innovation. The market benefits from Europe’s position as a global leader in packaging technology and sustainable manufacturing practices. Growth trajectories indicate sustained expansion, with the market experiencing consistent demand growth of approximately 4.2% annually across major European economies.

Key market drivers include increasing consumption of packaged beverages, growing demand for premium packaging solutions, and rising emphasis on product safety and authenticity. The beverage industry represents the largest application segment, accounting for approximately 65% of total market demand, followed by pharmaceuticals and cosmetics. Sustainability initiatives have become central to market development, with European manufacturers leading global efforts in recyclable closure design and circular economy implementation.

Competitive dynamics feature a mix of established global players and innovative regional specialists, creating a balanced market structure that promotes both stability and innovation. Technology adoption rates remain high, with digital printing, smart closures, and advanced coating technologies gaining significant traction. The market demonstrates resilience against economic fluctuations, supported by essential product applications and strong regulatory frameworks that ensure consistent demand patterns.

Market intelligence reveals several critical insights that define the Europe metal caps and closures landscape. The following key insights provide strategic understanding of market dynamics:

Primary growth drivers propelling the Europe metal caps and closures market encompass diverse factors ranging from consumer behavior changes to technological innovations. The beverage industry’s expansion serves as the most significant driver, with increasing consumption of packaged drinks, craft beverages, and premium spirits creating sustained demand for high-quality metal closures. Consumer preferences for convenient, resealable packaging solutions continue to drive innovation in closure design and functionality.

Sustainability imperatives represent another crucial driver, as European regulations and consumer awareness push manufacturers toward environmentally responsible closure solutions. The region’s commitment to circular economy principles drives investment in recyclable materials, lightweight designs, and sustainable manufacturing processes. Regulatory compliance requirements, particularly in pharmaceutical and food applications, necessitate advanced closure technologies that ensure product integrity and consumer safety.

Premiumization trends across various industries create opportunities for value-added closure solutions that enhance brand differentiation and consumer experience. The growing craft beverage sector, luxury cosmetics market, and premium food packaging applications drive demand for specialized metal closures with unique designs, enhanced functionality, and superior aesthetic appeal. Technological advancement in manufacturing processes enables cost-effective production of complex closure designs, supporting market expansion across diverse application segments.

Significant challenges facing the Europe metal caps and closures market include raw material price volatility, particularly for aluminum and steel, which directly impacts manufacturing costs and profit margins. Supply chain disruptions experienced in recent years have highlighted vulnerabilities in global material sourcing, creating operational challenges for European manufacturers. Energy cost fluctuations, particularly relevant given Europe’s industrial energy requirements, add additional pressure on manufacturing economics.

Environmental regulations, while driving innovation, also create compliance costs and operational complexities for manufacturers. Stringent recycling targets and extended producer responsibility requirements necessitate significant investments in sustainable technologies and processes. Competition from alternative packaging solutions, including plastic closures and innovative sealing technologies, challenges traditional metal closure applications in certain market segments.

Technical limitations in certain applications, such as compatibility issues with specific product formulations or packaging formats, restrict market expansion opportunities. The complexity of achieving optimal barrier properties while maintaining cost-effectiveness presents ongoing challenges for manufacturers. Market saturation in mature application segments limits growth potential, requiring companies to focus on innovation and value-added solutions to maintain competitive positioning.

Emerging opportunities in the Europe metal caps and closures market span multiple dimensions, from technological innovation to market expansion. The growing craft beverage industry presents significant opportunities for specialized closure solutions that cater to unique branding and functionality requirements. Smart packaging integration offers substantial potential, with opportunities to incorporate NFC technology, tamper-evident features, and consumer engagement capabilities into metal closures.

Sustainability-driven innovation creates opportunities for manufacturers to develop next-generation recyclable closures, bio-based coatings, and circular economy solutions that align with European environmental objectives. The pharmaceutical industry’s expansion, particularly in biologics and specialty medications, drives demand for high-performance closures with enhanced barrier properties and regulatory compliance capabilities. Export market expansion presents opportunities for European manufacturers to leverage their technological leadership and quality reputation in emerging global markets.

Digital transformation opportunities include implementation of Industry 4.0 technologies, predictive maintenance systems, and data-driven quality control processes that enhance operational efficiency and product consistency. The growing e-commerce sector creates demand for closures optimized for shipping and handling requirements, opening new application segments. Customization capabilities enabled by advanced manufacturing technologies allow for cost-effective production of specialized closures for niche applications and premium market segments.

Complex market dynamics characterize the Europe metal caps and closures market, influenced by interconnected factors spanning supply chain management, technological innovation, and regulatory compliance. Demand patterns exhibit seasonal variations, particularly in beverage applications, with peak consumption periods driving production planning and inventory management strategies. The market demonstrates strong correlation with broader economic indicators, including consumer spending patterns and industrial production levels.

Competitive intensity varies across market segments, with commodity closure applications experiencing price-based competition while premium and specialized segments focus on innovation and value-added features. MarkWide Research analysis indicates that market consolidation trends continue, with larger players acquiring specialized manufacturers to expand technological capabilities and market reach. Supply chain optimization remains critical, with manufacturers investing in vertical integration and strategic partnerships to ensure material availability and cost control.

Innovation cycles accelerate as manufacturers respond to evolving customer requirements and regulatory changes. The integration of digital technologies into traditional manufacturing processes creates new competitive dynamics, with early adopters gaining significant advantages in operational efficiency and product quality. Customer relationship management becomes increasingly important as buyers seek comprehensive solutions rather than simple product supply, driving manufacturers toward service-oriented business models.

Comprehensive research methodology employed for analyzing the Europe metal caps and closures market incorporates multiple data sources and analytical approaches to ensure accuracy and reliability. Primary research includes extensive interviews with industry executives, manufacturing specialists, and key stakeholders across the value chain, providing firsthand insights into market trends, challenges, and opportunities. Survey methodologies capture quantitative data on market preferences, purchasing patterns, and technology adoption rates.

Secondary research encompasses analysis of industry reports, regulatory filings, patent databases, and trade publications to establish comprehensive market understanding. Data triangulation methods validate findings across multiple sources, ensuring consistency and reliability of market insights. Statistical analysis techniques, including regression analysis and trend forecasting, support quantitative market projections and growth rate calculations.

Market modeling approaches incorporate economic indicators, industry-specific factors, and regional variations to develop accurate market size estimates and growth projections. Expert validation processes involve review by industry specialists and academic researchers to ensure analytical rigor and practical relevance. Continuous monitoring of market developments through real-time data collection and analysis supports dynamic market assessment and timely insight generation.

Regional market distribution across Europe reveals distinct patterns reflecting economic development, industrial concentration, and consumer preferences. Germany leads regional consumption, accounting for approximately 25% of total market demand, driven by its robust beverage industry, advanced manufacturing sector, and strong export economy. The country’s emphasis on quality and innovation aligns well with premium closure applications, supporting sustained market growth.

France represents the second-largest market, with approximately 18% market share, benefiting from its world-renowned wine industry and luxury goods sector. French manufacturers excel in premium closure applications, particularly for wine and spirits, where aesthetic appeal and functional performance are paramount. Italy follows closely with 16% market share, supported by its diverse beverage industry, including wine, beer, and specialty drinks, along with a strong cosmetics sector.

United Kingdom maintains significant market presence despite Brexit-related challenges, with approximately 12% market share driven by its large beverage consumption market and pharmaceutical industry. Spain and Netherlands each contribute approximately 8% of regional demand, with Spain benefiting from its growing beverage industry and Netherlands from its strategic position as a European distribution hub. Eastern European markets, including Poland, Czech Republic, and Hungary, demonstrate rapid growth potential, collectively representing approximately 15% of regional market share with growth rates exceeding regional averages.

Competitive structure of the Europe metal caps and closures market features a diverse mix of global corporations, regional specialists, and innovative technology companies. The market demonstrates moderate concentration, with leading players maintaining significant market positions while numerous smaller companies serve niche applications and regional markets. Strategic positioning varies considerably, with some companies focusing on high-volume commodity applications while others specialize in premium and technically advanced closure solutions.

Major market participants include:

Competitive strategies emphasize innovation, sustainability, and customer service excellence, with leading companies investing heavily in research and development, manufacturing automation, and market expansion initiatives.

Market segmentation analysis reveals distinct categories based on product type, application, material composition, and end-use industry. By product type, the market divides into crown caps, aluminum screw caps, twist-off caps, and specialty closures, each serving specific application requirements and market segments. Crown caps dominate the beer and carbonated beverage segments, while aluminum screw caps lead in wine and spirits applications.

By application, the market segments into:

By material composition, segments include aluminum closures, steel closures, and composite metal closures, each offering distinct performance characteristics and cost profiles. By end-use industry, segmentation reflects the diverse application landscape, with beverage manufacturers representing the largest customer segment, followed by food processors, pharmaceutical companies, and cosmetics manufacturers.

Beverage category dominates the Europe metal caps and closures market, driven by high consumption rates of packaged drinks and the superior barrier properties of metal closures. Beer applications represent the largest sub-segment, with crown caps and twist-off caps providing essential carbonation retention and brand differentiation opportunities. The craft beer revolution across Europe creates demand for unique closure designs and premium materials that enhance product positioning and consumer appeal.

Wine and spirits applications demonstrate strong growth, particularly in premium segments where aluminum screw caps offer superior wine preservation compared to traditional cork closures. Market acceptance of screw caps for wine continues to grow, with adoption rates reaching approximately 40% in certain European markets. The spirits category benefits from increasing consumption of premium and craft spirits, driving demand for sophisticated closure solutions that enhance brand image and product integrity.

Pharmaceutical applications require the highest performance standards, with closures meeting stringent regulatory requirements for product safety, tamper evidence, and barrier properties. Cosmetics and personal care applications focus on aesthetic appeal and premium positioning, with metal closures providing luxury appearance and enhanced product protection. Food applications emphasize functionality and cost-effectiveness, with closures designed for easy opening, resealing capability, and extended shelf life preservation.

Manufacturers benefit from the Europe metal caps and closures market through diverse revenue opportunities, technological advancement potential, and sustainable business model development. The market’s stability and growth trajectory provide predictable demand patterns that support long-term investment planning and capacity expansion strategies. Innovation opportunities enable manufacturers to differentiate their offerings and capture premium pricing in specialized applications.

Brand owners and packaging buyers gain access to advanced closure solutions that enhance product protection, extend shelf life, and improve consumer convenience. Metal closures provide superior barrier properties compared to many alternative materials, ensuring product quality and reducing waste. The recyclability of metal closures supports corporate sustainability objectives and regulatory compliance requirements.

Consumers benefit from improved product quality, enhanced convenience features, and sustainable packaging options. Resealable closures provide portion control and product freshness maintenance, while tamper-evident features ensure product safety and authenticity. Supply chain participants including distributors and retailers benefit from the durability and handling characteristics of metal closures, which reduce product damage and improve operational efficiency throughout the distribution process.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability transformation represents the most significant trend shaping the Europe metal caps and closures market, with manufacturers investing heavily in recyclable materials, reduced environmental impact, and circular economy solutions. Lightweight design initiatives focus on material optimization while maintaining performance standards, reducing both costs and environmental footprint. Advanced coating technologies eliminate harmful substances while enhancing barrier properties and aesthetic appeal.

Smart packaging integration gains momentum as brands seek enhanced consumer engagement and product authentication capabilities. NFC-enabled closures provide interactive experiences, supply chain transparency, and anti-counterfeiting features that add significant value for premium applications. Digital printing technologies enable cost-effective customization and short-run production capabilities that support brand differentiation strategies.

Premiumization trends drive demand for sophisticated closure designs that enhance product positioning and consumer experience. Craft beverage growth creates opportunities for unique closure solutions that reflect artisanal quality and brand personality. MarkWide Research indicates that premium closure segments demonstrate growth rates significantly above market averages, reflecting consumer willingness to pay for enhanced packaging experiences. Automation advancement in manufacturing processes improves quality consistency, reduces costs, and enables flexible production capabilities that support market responsiveness.

Recent industry developments highlight the dynamic nature of the Europe metal caps and closures market, with significant investments in technology, sustainability, and market expansion. Manufacturing automation initiatives have transformed production capabilities, with leading companies implementing Industry 4.0 technologies that enhance efficiency, quality control, and operational flexibility. Advanced robotics and artificial intelligence applications optimize production planning and quality assurance processes.

Sustainability initiatives include major investments in recycling infrastructure, development of bio-based coating materials, and implementation of circular economy principles throughout the value chain. Strategic partnerships between closure manufacturers and recycling companies create closed-loop systems that maximize material recovery and reuse. Several European manufacturers have achieved carbon neutrality in their operations through renewable energy adoption and process optimization.

Market consolidation continues with strategic acquisitions that combine complementary technologies and expand geographic reach. Innovation investments focus on smart packaging capabilities, enhanced barrier properties, and cost-effective manufacturing processes. Regulatory compliance initiatives ensure adherence to evolving food safety, pharmaceutical, and environmental standards across European markets. Export expansion strategies leverage European quality reputation and technological leadership to capture opportunities in emerging global markets.

Strategic recommendations for Europe metal caps and closures market participants emphasize the importance of sustainability leadership, technological innovation, and market diversification. Manufacturers should prioritize investment in recyclable closure technologies and circular economy solutions to align with regulatory requirements and consumer expectations. Development of lightweight designs that maintain performance standards offers dual benefits of cost reduction and environmental impact minimization.

Innovation focus should emphasize smart packaging capabilities, enhanced barrier properties, and customization technologies that enable differentiation in competitive markets. Market expansion strategies should target high-growth segments including craft beverages, premium cosmetics, and pharmaceutical applications where value-added features command premium pricing. Supply chain optimization through vertical integration and strategic partnerships can mitigate raw material price volatility and ensure operational continuity.

Digital transformation initiatives should encompass manufacturing automation, predictive maintenance, and data-driven quality control systems that enhance operational efficiency and product consistency. Customer relationship management strategies should evolve toward comprehensive solution provision rather than simple product supply, creating stronger partnerships and competitive differentiation. Export market development leveraging European quality reputation and technological leadership can provide growth opportunities beyond regional markets.

Future prospects for the Europe metal caps and closures market appear robust, supported by fundamental demand drivers, technological advancement, and sustainability imperatives. Market growth is projected to continue at steady rates, with premium and specialized segments demonstrating above-average expansion potential. The beverage industry’s evolution toward craft and premium products creates sustained demand for innovative closure solutions that enhance brand differentiation and consumer experience.

Technological evolution will likely accelerate, with smart packaging capabilities becoming mainstream in premium applications within the next five years. Sustainability requirements will intensify, driving continued innovation in recyclable materials, bio-based coatings, and circular economy solutions. MWR projections indicate that sustainability-focused closure solutions will capture increasing market share as regulatory requirements and consumer preferences align toward environmental responsibility.

Market structure may experience further consolidation as companies seek scale advantages and technological capabilities to compete effectively in evolving market conditions. Regional dynamics will likely shift with Eastern European markets demonstrating accelerated growth as economic development drives increased consumption of packaged goods. Innovation cycles are expected to accelerate, with product development timelines shortening in response to rapidly evolving customer requirements and competitive pressures. The integration of digital technologies throughout the value chain will create new business models and competitive advantages for early adopters.

The Europe metal caps and closures market demonstrates strong fundamentals and promising growth prospects, driven by diverse application demands, technological innovation, and sustainability imperatives. Market resilience reflects the essential nature of closure applications across critical industries including beverages, pharmaceuticals, and food packaging. The region’s leadership in quality, innovation, and environmental responsibility positions European manufacturers advantageously in global markets.

Strategic success factors include sustainability leadership, technological innovation, and customer-centric solution development that addresses evolving market requirements. Growth opportunities span premium applications, smart packaging integration, and export market expansion, providing multiple avenues for market participants to achieve sustainable competitive advantages. The market’s evolution toward value-added solutions and comprehensive service provision creates opportunities for differentiation and premium positioning.

Future market development will likely emphasize sustainability, digitalization, and customization capabilities that enable manufacturers to serve diverse customer requirements effectively. The Europe metal caps and closures market remains well-positioned to capitalize on global packaging trends while maintaining its leadership in quality, innovation, and environmental responsibility. Continued investment in technology, sustainability, and market expansion will determine competitive success in this dynamic and evolving market landscape.

What is Metal Caps and Closures?

Metal caps and closures are packaging components made from metal that are used to seal containers, ensuring product integrity and safety. They are commonly used in industries such as food and beverage, pharmaceuticals, and cosmetics.

What are the key players in the Europe Metal Caps and Closures Market?

Key players in the Europe Metal Caps and Closures Market include Crown Holdings, Inc., Silgan Holdings Inc., and Ardagh Group, among others. These companies are known for their innovative packaging solutions and extensive product ranges.

What are the growth factors driving the Europe Metal Caps and Closures Market?

The Europe Metal Caps and Closures Market is driven by the increasing demand for sustainable packaging solutions, the growth of the beverage industry, and the rising consumer preference for metal packaging due to its recyclability and durability.

What challenges does the Europe Metal Caps and Closures Market face?

Challenges in the Europe Metal Caps and Closures Market include fluctuating raw material prices, competition from alternative packaging materials, and regulatory compliance regarding food safety and environmental standards.

What opportunities exist in the Europe Metal Caps and Closures Market?

Opportunities in the Europe Metal Caps and Closures Market include the development of innovative designs, the expansion of e-commerce packaging solutions, and the increasing focus on eco-friendly materials and production processes.

What trends are shaping the Europe Metal Caps and Closures Market?

Trends in the Europe Metal Caps and Closures Market include the rise of lightweight metal closures, advancements in tamper-evident technologies, and the growing popularity of customized packaging solutions to enhance brand identity.

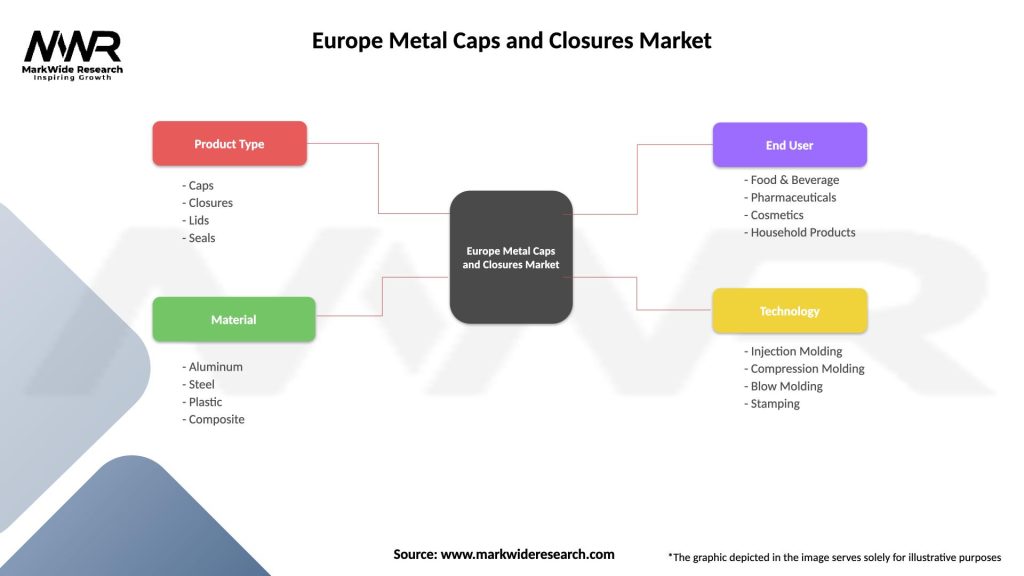

Europe Metal Caps and Closures Market

| Segmentation Details | Description |

|---|---|

| Product Type | Caps, Closures, Lids, Seals |

| Material | Aluminum, Steel, Plastic, Composite |

| End User | Food & Beverage, Pharmaceuticals, Cosmetics, Household Products |

| Technology | Injection Molding, Compression Molding, Blow Molding, Stamping |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Europe Metal Caps and Closures Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.