444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Switzerland data center power market represents a critical infrastructure segment experiencing unprecedented growth driven by digital transformation initiatives and increasing demand for cloud computing services. Switzerland’s strategic position as a European technology hub, combined with its stable political environment and robust energy infrastructure, has positioned the country as a preferred destination for data center investments. The market encompasses power distribution systems, uninterruptible power supplies (UPS), backup generators, and energy management solutions specifically designed for data center operations.

Market dynamics indicate that Switzerland’s data center power sector is expanding at a compound annual growth rate (CAGR) of 8.2%, reflecting the nation’s commitment to becoming a leading digital economy. The increasing adoption of artificial intelligence, Internet of Things (IoT), and edge computing technologies has significantly amplified power requirements for data centers across the country. Energy efficiency initiatives and sustainability mandates are reshaping power infrastructure investments, with operators prioritizing renewable energy integration and advanced cooling technologies.

Geographic distribution shows that approximately 45% of data center power infrastructure is concentrated in the Zurich metropolitan area, followed by Geneva and Basel regions. The market benefits from Switzerland’s abundant hydroelectric power resources, providing clean energy solutions that align with global sustainability objectives and corporate environmental commitments.

The Switzerland data center power market refers to the comprehensive ecosystem of electrical infrastructure, power management systems, and energy solutions specifically designed to support data center operations throughout Switzerland. This market encompasses all power-related components including primary power distribution, backup power systems, uninterruptible power supplies, power monitoring equipment, and energy efficiency technologies that ensure continuous, reliable operation of data processing facilities.

Power infrastructure components within this market include medium and high-voltage electrical systems, transformers, switchgear, generators, battery systems, and sophisticated power management software. The market also covers specialized cooling systems that consume significant portions of data center power budgets, representing integrated solutions that optimize both computational performance and energy consumption.

Operational scope extends beyond traditional hardware to include power purchase agreements, renewable energy certificates, grid integration services, and comprehensive maintenance contracts. This holistic approach ensures that data center operators can maintain 99.99% uptime reliability while meeting increasingly stringent environmental regulations and corporate sustainability targets.

Switzerland’s data center power market demonstrates remarkable resilience and growth potential, driven by the country’s position as a global financial and technology center. The market benefits from exceptional political stability, advanced telecommunications infrastructure, and abundant renewable energy resources that provide competitive advantages for data center operations. Digital transformation acceleration across industries has created sustained demand for reliable, scalable power solutions.

Key market characteristics include high adoption rates of energy-efficient technologies, with 72% of new installations incorporating advanced power management systems and renewable energy integration. The market shows strong preference for modular, scalable power solutions that can adapt to rapidly changing computational requirements. Sustainability initiatives have become primary drivers, with operators targeting carbon neutrality and implementing circular economy principles.

Competitive landscape features both international technology leaders and specialized Swiss engineering companies, creating a dynamic ecosystem that fosters innovation and customized solutions. The market demonstrates strong growth trajectory supported by favorable regulatory environment, strategic geographic location, and commitment to technological excellence that positions Switzerland as a preferred European data center destination.

Strategic market insights reveal several critical trends shaping Switzerland’s data center power landscape:

Digital transformation initiatives across Swiss enterprises represent the primary catalyst driving data center power market expansion. Organizations are migrating critical workloads to digital platforms, requiring robust, scalable power infrastructure capable of supporting increased computational demands. Cloud adoption rates have accelerated significantly, with businesses seeking reliable data center services that guarantee continuous availability and performance.

Regulatory environment strongly supports market growth through favorable data protection laws, including compliance with European GDPR requirements that encourage local data processing and storage. Switzerland’s political neutrality and stable legal framework provide additional confidence for international organizations establishing data center operations. Financial sector digitization particularly drives demand, as banking and insurance companies require secure, compliant infrastructure for sensitive data processing.

Sustainability mandates are increasingly influencing power infrastructure investments, with organizations prioritizing renewable energy sources and energy-efficient technologies. The Swiss government’s commitment to carbon neutrality by 2050 creates strong incentives for clean energy adoption in data center operations. Energy cost optimization remains a critical driver, as power represents approximately 30-40% of total data center operating expenses, making efficient power management essential for profitability.

Technological advancement in artificial intelligence, machine learning, and high-performance computing creates unprecedented power density requirements that drive infrastructure upgrades and specialized cooling solutions. The emergence of edge computing applications requires distributed power infrastructure capable of supporting localized data processing capabilities.

High capital investment requirements represent a significant barrier to market entry, particularly for smaller operators seeking to establish data center facilities. Power infrastructure represents substantial upfront costs, including electrical distribution systems, backup generators, UPS systems, and specialized cooling equipment. Complex regulatory compliance adds additional costs and timeline extensions for new facility development and existing infrastructure upgrades.

Grid capacity limitations in certain regions constrain market expansion, particularly in densely populated areas where electrical infrastructure may require significant upgrades to support high-density data center operations. Skilled workforce shortage affects both installation and maintenance of sophisticated power systems, creating operational challenges and increased labor costs for market participants.

Energy price volatility creates uncertainty for long-term operational planning, particularly as data centers require predictable power costs for financial modeling and customer pricing strategies. Environmental regulations while driving innovation, also impose additional compliance costs and operational constraints that may limit flexibility in power system design and operation.

Technology obsolescence risks require continuous investment in power infrastructure upgrades to maintain compatibility with evolving computing technologies and efficiency standards. The rapid pace of technological change creates challenges in balancing current operational needs with future scalability requirements.

Renewable energy integration presents substantial opportunities for market expansion, particularly given Switzerland’s abundant hydroelectric resources and growing solar power capacity. Data center operators can leverage power purchase agreements with renewable energy providers to achieve sustainability objectives while potentially reducing long-term energy costs. Energy storage technologies offer opportunities for grid stabilization services and peak demand management.

Edge computing deployment creates demand for distributed power infrastructure supporting localized data processing capabilities. This trend requires innovative power solutions that can operate efficiently in diverse environments while maintaining reliability standards. 5G network rollout drives additional edge computing requirements, expanding market opportunities for specialized power systems.

Artificial intelligence workloads require high-density power infrastructure and advanced cooling solutions, creating opportunities for specialized equipment manufacturers and service providers. Quantum computing research and development activities in Switzerland may generate future demand for ultra-specialized power and cooling systems.

Cross-border data flows and Switzerland’s strategic location between major European markets create opportunities for transit and interconnection services requiring robust power infrastructure. Disaster recovery services and business continuity planning drive demand for geographically distributed data center facilities with redundant power systems.

Supply chain dynamics within Switzerland’s data center power market reflect global technology trends while maintaining local customization capabilities. International equipment manufacturers collaborate with Swiss engineering firms to deliver solutions optimized for local conditions and regulatory requirements. The market demonstrates strong integration between power infrastructure providers, data center operators, and energy suppliers.

Competitive dynamics show increasing collaboration between traditional power equipment manufacturers and software companies developing intelligent power management systems. Innovation cycles are accelerating, with new technologies emerging regularly to address efficiency, reliability, and sustainability challenges. Market participants are investing heavily in research and development to maintain competitive advantages.

Customer dynamics reveal growing sophistication in power infrastructure requirements, with data center operators demanding comprehensive solutions that integrate seamlessly with existing systems. Service level expectations continue rising, with customers requiring 99.99% uptime guarantees and rapid response times for maintenance and support services.

Regulatory dynamics influence market development through evolving energy efficiency standards, environmental regulations, and grid integration requirements. Policy support for renewable energy adoption and digital infrastructure development creates favorable conditions for market expansion while establishing performance benchmarks that drive continuous improvement.

Comprehensive market analysis employed multiple research methodologies to ensure accurate and reliable insights into Switzerland’s data center power market. Primary research included structured interviews with key industry stakeholders, including data center operators, power equipment manufacturers, energy suppliers, and regulatory officials. Survey methodologies captured quantitative data on market trends, technology adoption rates, and investment priorities.

Secondary research incorporated analysis of industry reports, government publications, regulatory filings, and company financial statements to validate primary findings and identify market trends. Technical documentation review included power system specifications, energy efficiency standards, and environmental compliance requirements that influence market development.

Market modeling techniques utilized statistical analysis and forecasting methodologies to project future market trends and growth patterns. Comparative analysis examined Switzerland’s market characteristics relative to other European data center markets to identify unique competitive advantages and challenges.

Data validation processes ensured accuracy through triangulation of multiple information sources and expert review of findings. MarkWide Research methodology standards were applied throughout the research process to maintain consistency and reliability in market analysis and projections.

Zurich metropolitan region dominates Switzerland’s data center power market, accounting for approximately 45% of total infrastructure capacity. The region benefits from excellent connectivity to international fiber optic networks, proximity to major financial institutions, and robust electrical grid infrastructure. Power density requirements in Zurich are among the highest in Europe, driven by financial services and technology companies requiring high-performance computing capabilities.

Geneva region represents the second-largest market segment, with 28% market share driven by international organizations, multinational corporations, and research institutions. The region’s strategic location near CERN and other research facilities creates unique power requirements for scientific computing applications. Cross-border connectivity to France provides additional power supply options and redundancy capabilities.

Basel region accounts for approximately 15% of market capacity, with strong pharmaceutical and chemical industry presence driving specialized data center requirements. The region benefits from excellent transportation links and proximity to German and French markets. Industrial power infrastructure provides advantages for large-scale data center development.

Other regions including Bern, Lausanne, and smaller cities represent emerging opportunities for distributed data center deployment. Edge computing applications are driving power infrastructure development in these secondary markets, supported by 5G network expansion and local business digitization initiatives.

Market leadership in Switzerland’s data center power sector includes both international technology giants and specialized local providers:

Competitive strategies focus on technological innovation, energy efficiency improvements, and comprehensive service offerings. Companies are investing in local partnerships, research and development, and specialized solutions for Swiss market requirements.

By Technology:

By Data Center Type:

By Power Rating:

UPS Systems Category represents the largest segment within Switzerland’s data center power market, driven by critical reliability requirements and increasing power density demands. Modular UPS solutions are gaining popularity due to scalability advantages and improved efficiency ratings. Advanced lithium-ion battery technologies are replacing traditional lead-acid systems, offering longer lifespan and reduced maintenance requirements.

Power Distribution Category shows strong growth in intelligent PDU adoption, with smart monitoring capabilities becoming standard requirements. Remote management features and integration with data center infrastructure management (DCIM) systems drive market demand. High-density power distribution solutions address increasing rack power requirements from modern computing equipment.

Generator Systems Category benefits from reliability requirements and grid independence objectives. Natural gas generators are preferred over diesel systems due to environmental considerations and fuel availability. Advanced control systems and remote monitoring capabilities enhance operational efficiency and reduce maintenance costs.

Power Monitoring Category experiences rapid growth driven by energy efficiency initiatives and operational optimization requirements. Real-time analytics and predictive maintenance capabilities provide significant value for data center operators. Integration with artificial intelligence and machine learning systems enables automated power management and optimization.

Data Center Operators benefit from advanced power infrastructure through improved reliability, reduced operational costs, and enhanced energy efficiency. Predictive maintenance capabilities minimize unplanned downtime while optimizing equipment lifecycle costs. Comprehensive power monitoring enables precise capacity planning and resource allocation optimization.

Equipment Manufacturers gain access to a sophisticated market with high-quality requirements and willingness to invest in premium solutions. Innovation opportunities exist for developing specialized products addressing unique Swiss market needs. Long-term partnerships with local operators provide stable revenue streams and market intelligence.

Energy Suppliers benefit from stable, predictable demand from data center operations while supporting renewable energy integration objectives. Grid stabilization services from data center energy storage systems provide additional revenue opportunities. Power purchase agreements offer long-term revenue visibility and support renewable energy project financing.

Technology Companies leveraging Swiss data centers gain access to reliable, secure infrastructure supporting business continuity and regulatory compliance requirements. Sustainability benefits from renewable energy integration support corporate environmental objectives and stakeholder expectations.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainability Integration represents the most significant trend shaping Switzerland’s data center power market, with operators prioritizing renewable energy sources and carbon footprint reduction. Circular economy principles are being implemented through equipment lifecycle optimization and waste heat recovery systems. Advanced energy storage solutions enable grid stabilization services while supporting renewable energy integration.

Artificial Intelligence Optimization is transforming power management through predictive analytics, automated load balancing, and intelligent cooling control systems. Machine learning algorithms optimize power distribution and identify efficiency improvement opportunities in real-time. AI-driven maintenance scheduling reduces downtime while extending equipment lifecycles.

Edge Computing Expansion drives demand for distributed power infrastructure supporting localized data processing capabilities. Micro data centers require specialized power solutions optimized for space-constrained environments. 5G network deployment accelerates edge computing adoption across multiple industry sectors.

Modular Infrastructure Design enables rapid deployment and scalability while reducing capital investment risks. Prefabricated power modules accelerate construction timelines and improve quality control. Containerized solutions provide flexibility for temporary or specialized applications.

Grid Integration Innovation includes smart grid connectivity, demand response participation, and energy trading capabilities. Vehicle-to-grid integration may provide additional energy storage and grid stabilization services. Advanced power electronics enable bidirectional energy flows and grid support functions.

Recent technological advancement in power infrastructure includes deployment of silicon carbide semiconductors improving efficiency and reducing cooling requirements. Liquid cooling integration with power distribution systems addresses high-density computing requirements while improving overall energy efficiency. Advanced battery management systems extend energy storage lifecycles and improve safety performance.

Strategic partnerships between international technology providers and Swiss engineering companies are accelerating innovation and local market adaptation. Collaborative research initiatives with Swiss universities and research institutions drive development of next-generation power technologies. Industry consortiums are establishing standards for sustainable data center operations and renewable energy integration.

Regulatory developments include updated energy efficiency standards and environmental compliance requirements that influence power infrastructure design and operation. Grid modernization projects improve integration capabilities for renewable energy sources and energy storage systems. Government incentives support adoption of clean energy technologies and efficiency improvements.

Market consolidation activities include acquisitions and strategic alliances aimed at expanding service capabilities and geographic coverage. Vertical integration strategies combine power equipment manufacturing with comprehensive service offerings. International expansion by Swiss companies leverages local expertise in global markets.

MarkWide Research analysis indicates that market participants should prioritize sustainability initiatives and renewable energy integration to maintain competitive positioning. Investment in advanced monitoring and analytics capabilities will become essential for operational optimization and predictive maintenance. Companies should develop comprehensive service offerings combining equipment supply with ongoing support and optimization services.

Strategic recommendations include establishing local partnerships to navigate regulatory requirements and access specialized expertise. Technology roadmap development should anticipate future requirements including artificial intelligence workloads, edge computing applications, and quantum computing research. Modular, scalable solutions provide flexibility to address diverse customer requirements and market evolution.

Market positioning strategies should emphasize unique value propositions including reliability, efficiency, and sustainability benefits. Customer relationship management requires deep understanding of evolving requirements and proactive solution development. Long-term partnerships with key customers provide market stability and innovation opportunities.

Risk management approaches should address technology obsolescence, regulatory changes, and competitive pressures through diversified portfolios and flexible business models. Continuous innovation investment maintains technological leadership while addressing emerging market requirements and customer expectations.

Long-term market prospects for Switzerland’s data center power sector remain highly positive, supported by continued digital transformation, artificial intelligence adoption, and edge computing expansion. Growth projections indicate sustained expansion at compound annual growth rates exceeding 8% through the next decade. Increasing power density requirements and sustainability mandates will drive continuous infrastructure upgrades and technology adoption.

Technology evolution will focus on efficiency improvements, renewable energy integration, and intelligent automation capabilities. Next-generation power systems will incorporate advanced materials, artificial intelligence optimization, and seamless grid integration. Quantum computing applications may create specialized power requirements and market opportunities.

Market structure evolution may include increased consolidation among service providers and deeper integration between power infrastructure and data center operations. Service-based business models will become more prevalent, with customers preferring comprehensive solutions over individual equipment purchases. Subscription and performance-based pricing models may gain adoption.

Regulatory environment will likely become more stringent regarding environmental performance and energy efficiency, creating both challenges and opportunities for market participants. International coordination on sustainability standards may influence local requirements and competitive dynamics. Government support for digital infrastructure development will continue supporting market growth and innovation initiatives.

Switzerland’s data center power market represents a dynamic, high-growth sector positioned at the intersection of digital transformation, sustainability initiatives, and technological innovation. The market benefits from unique competitive advantages including political stability, abundant renewable energy resources, strategic geographic location, and strong engineering expertise that support continued expansion and innovation.

Market fundamentals remain strong, driven by accelerating digitization across industries, artificial intelligence adoption, edge computing deployment, and stringent reliability requirements. The integration of renewable energy sources and advanced power management technologies positions Switzerland as a leader in sustainable data center operations while maintaining operational excellence and competitive positioning.

Future success in this market will require continuous innovation, strategic partnerships, and adaptability to evolving customer requirements and regulatory environments. Companies that prioritize sustainability, invest in advanced technologies, and develop comprehensive service capabilities will be best positioned to capitalize on growth opportunities and maintain competitive advantages in Switzerland’s sophisticated data center power market.

What is Data Center Power?

Data Center Power refers to the electrical power supply and management systems that support the operation of data centers, including servers, storage, and networking equipment. It encompasses various aspects such as power distribution, backup systems, and energy efficiency measures.

What are the key players in the Switzerland Data Center Power Market?

Key players in the Switzerland Data Center Power Market include companies like ABB, Schneider Electric, and Siemens, which provide power management solutions and infrastructure for data centers. These companies focus on energy efficiency and reliability, among others.

What are the growth factors driving the Switzerland Data Center Power Market?

The growth of the Switzerland Data Center Power Market is driven by increasing data consumption, the rise of cloud computing, and the demand for energy-efficient solutions. Additionally, the expansion of digital services and the need for robust IT infrastructure contribute to this growth.

What challenges does the Switzerland Data Center Power Market face?

Challenges in the Switzerland Data Center Power Market include high energy costs, regulatory compliance related to energy consumption, and the need for sustainable practices. Additionally, the rapid pace of technological change can create difficulties in keeping infrastructure up to date.

What opportunities exist in the Switzerland Data Center Power Market?

Opportunities in the Switzerland Data Center Power Market include the adoption of renewable energy sources, advancements in energy storage technologies, and the development of smart grid solutions. These trends can enhance energy efficiency and reduce operational costs for data centers.

What trends are shaping the Switzerland Data Center Power Market?

Trends shaping the Switzerland Data Center Power Market include the increasing focus on sustainability, the integration of artificial intelligence for power management, and the shift towards modular data center designs. These innovations aim to improve efficiency and reduce environmental impact.

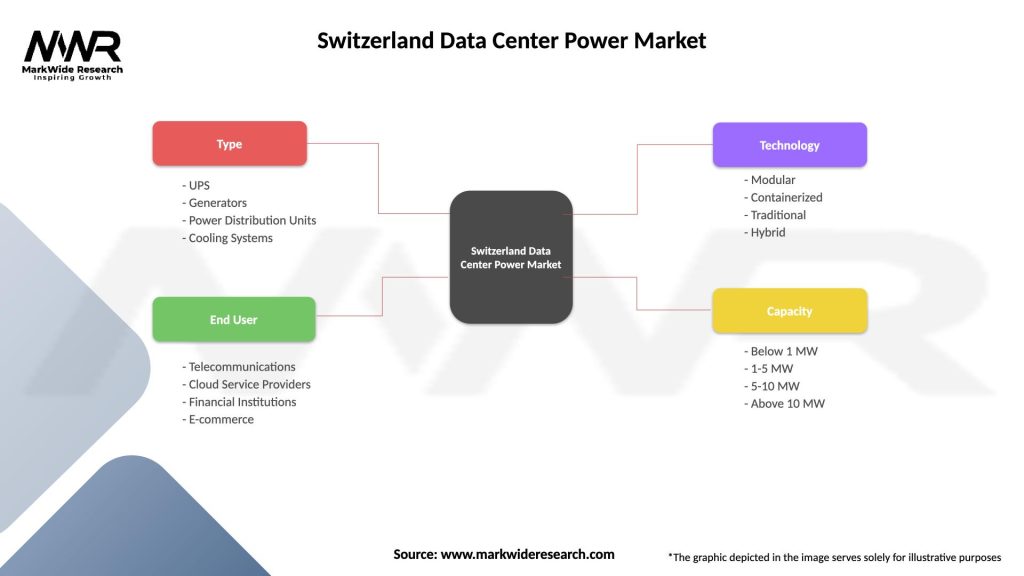

Switzerland Data Center Power Market

| Segmentation Details | Description |

|---|---|

| Type | UPS, Generators, Power Distribution Units, Cooling Systems |

| End User | Telecommunications, Cloud Service Providers, Financial Institutions, E-commerce |

| Technology | Modular, Containerized, Traditional, Hybrid |

| Capacity | Below 1 MW, 1-5 MW, 5-10 MW, Above 10 MW |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Switzerland Data Center Power Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.