444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The UAE data center construction market represents one of the most dynamic and rapidly evolving sectors within the Middle East’s technology infrastructure landscape. As the United Arab Emirates continues its transformation into a global digital hub, the demand for sophisticated data center facilities has reached unprecedented levels. Digital transformation initiatives across government and private sectors are driving substantial investments in data center infrastructure, positioning the UAE as a strategic gateway for cloud services, artificial intelligence, and digital commerce throughout the MENA region.

Market dynamics indicate robust growth driven by increasing cloud adoption rates of approximately 78% among enterprises, coupled with government initiatives supporting the UAE’s Vision 2071. The construction of hyperscale data centers, edge computing facilities, and colocation services has become a critical component of the nation’s economic diversification strategy. Dubai and Abu Dhabi lead the market expansion, with significant investments in sustainable construction technologies and energy-efficient cooling systems.

Regional positioning as a connectivity hub between Europe, Asia, and Africa has attracted major international cloud service providers and telecommunications companies to establish substantial data center footprints. The market encompasses various construction segments including hyperscale facilities, enterprise data centers, colocation services, and edge computing infrastructure, each requiring specialized construction expertise and advanced building technologies.

The UAE data center construction market refers to the comprehensive ecosystem of planning, designing, building, and commissioning specialized facilities that house critical IT infrastructure, servers, networking equipment, and storage systems. This market encompasses all construction activities related to creating secure, climate-controlled environments capable of supporting continuous digital operations with maximum uptime and reliability.

Data center construction involves complex engineering disciplines including structural design, mechanical systems, electrical infrastructure, fire suppression, security systems, and telecommunications connectivity. The construction process requires adherence to international standards such as Uptime Institute Tier classifications, ensuring facilities meet stringent requirements for power redundancy, cooling efficiency, and operational resilience.

Modern data center construction in the UAE incorporates advanced technologies including modular construction techniques, liquid cooling systems, renewable energy integration, and smart building automation. These facilities serve as the backbone for cloud computing services, artificial intelligence applications, Internet of Things deployments, and digital transformation initiatives across various industry sectors.

Strategic market positioning places the UAE data center construction sector at the forefront of regional digital infrastructure development. The market benefits from substantial government support through initiatives like the UAE Digital Government Strategy 2025 and smart city projects that require extensive data processing capabilities. Investment flows from both domestic and international sources continue to accelerate construction activities across multiple emirates.

Key growth drivers include the rapid adoption of cloud services, increasing data generation rates of approximately 35% annually, and the expansion of 5G networks requiring edge computing infrastructure. The construction market serves diverse client segments ranging from hyperscale cloud providers to local enterprises seeking colocation services and managed hosting solutions.

Technological advancement in construction methodologies has enabled faster deployment times and improved energy efficiency ratings. Sustainable construction practices have become increasingly important, with new facilities targeting 40% reduction in energy consumption compared to traditional designs. The market outlook remains highly positive, supported by continued digital transformation across government and private sectors.

Market segmentation reveals distinct construction categories serving different operational requirements and client needs:

Construction complexity varies significantly across these segments, with hyperscale facilities requiring the most sophisticated engineering solutions and highest construction investment levels. Each category demands specific expertise in areas such as power distribution, cooling systems, security implementation, and compliance with regulatory requirements.

Digital transformation acceleration across UAE industries serves as the primary catalyst for data center construction demand. Government initiatives including the UAE Strategy for Artificial Intelligence 2031 and blockchain strategy implementation require substantial computational infrastructure, driving construction of specialized facilities capable of supporting advanced technologies.

Cloud adoption rates continue expanding rapidly, with enterprise migration to cloud services reaching approximately 82% adoption levels across major industry sectors. This transition necessitates construction of hyperscale data centers and colocation facilities to support increased demand for cloud computing resources, storage capacity, and network connectivity services.

5G network deployment throughout the UAE creates unprecedented demand for edge computing infrastructure construction. The low-latency requirements of 5G applications require data processing capabilities positioned closer to end-users, driving construction of distributed edge data centers across urban and suburban areas.

Economic diversification strategies emphasizing technology sector growth attract international technology companies establishing regional headquarters and operational centers. These organizations require dedicated data center facilities, spurring construction of enterprise-grade infrastructure with customized specifications and enhanced security features.

Smart city initiatives across Dubai, Abu Dhabi, and other emirates generate massive data processing requirements for IoT sensors, traffic management systems, utility monitoring, and citizen services platforms. Construction of government data centers and public-private partnership facilities supports these comprehensive digital transformation projects.

High capital investment requirements present significant barriers for market entry, particularly for smaller construction companies lacking specialized expertise in data center development. The complex nature of data center construction demands substantial upfront investments in equipment, skilled personnel, and certification processes.

Skilled workforce shortages in specialized construction disciplines create project delays and increased labor costs. The demand for engineers, technicians, and project managers with data center construction experience exceeds current supply levels, particularly for advanced cooling systems and power infrastructure installation.

Regulatory compliance complexity requires navigation of multiple approval processes, building codes, and international standards. Construction projects must meet stringent requirements for fire safety, environmental impact, power consumption, and telecommunications connectivity, extending project timelines and increasing development costs.

Energy consumption concerns and sustainability requirements impose additional constraints on construction design and operational planning. Data centers typically consume significant electrical power for cooling and IT operations, requiring careful integration of renewable energy sources and energy-efficient technologies.

Land availability limitations in prime locations near fiber optic infrastructure and power substations create competition for suitable construction sites. The requirement for proximity to telecommunications networks and reliable power sources restricts development options in certain geographic areas.

Sustainable construction technologies present substantial opportunities for differentiation and market leadership. The growing emphasis on environmental responsibility creates demand for data centers incorporating renewable energy systems, advanced cooling technologies, and green building certifications, opening new market segments for specialized construction services.

Modular construction approaches offer significant potential for reducing deployment times and construction costs. Prefabricated data center modules enable faster project completion and provide scalability advantages, creating opportunities for construction companies to develop standardized solutions and manufacturing capabilities.

Edge computing expansion requires construction of numerous smaller facilities distributed across urban areas. This trend creates opportunities for construction companies to specialize in rapid deployment techniques and standardized edge data center designs serving 5G networks and IoT applications.

Government infrastructure projects related to smart city development and digital government services provide substantial construction opportunities. Public sector investments in data center infrastructure support long-term contracts and stable revenue streams for qualified construction providers.

International expansion of cloud service providers and technology companies into the UAE market creates demand for hyperscale data center construction. These projects typically involve substantial construction contracts and opportunities for ongoing maintenance and expansion services.

Supply chain integration has become increasingly sophisticated, with construction companies developing strategic partnerships with equipment manufacturers, cooling system providers, and power infrastructure specialists. These relationships enable more efficient project delivery and access to cutting-edge technologies for data center construction projects.

Construction methodologies continue evolving toward modular and prefabricated approaches, reducing on-site construction time by approximately 45% compared to traditional methods. This shift enables faster project delivery and improved quality control through factory-based manufacturing processes.

Technology integration during construction phases incorporates advanced building information modeling, IoT sensors for construction monitoring, and automated quality assurance systems. These technologies improve project management efficiency and ensure compliance with stringent data center performance requirements.

Market consolidation trends show larger construction companies acquiring specialized data center contractors to expand service capabilities and geographic coverage. This consolidation creates more comprehensive service offerings and improved project delivery capabilities for complex data center construction projects.

Competitive differentiation increasingly focuses on sustainability credentials, construction speed, and post-completion support services. Construction companies are developing specialized expertise in areas such as liquid cooling systems, renewable energy integration, and modular expansion capabilities to maintain competitive advantages.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into the UAE data center construction market. Primary research involves direct engagement with construction companies, data center operators, technology providers, and government agencies involved in infrastructure development projects.

Data collection processes include structured interviews with industry executives, construction project managers, and facility operators to gather insights on market trends, challenges, and growth opportunities. Survey methodologies capture quantitative data on construction volumes, project timelines, technology adoption rates, and investment patterns across different market segments.

Secondary research incorporates analysis of government publications, industry reports, construction permits, and project announcements to validate primary research findings. MarkWide Research utilizes proprietary databases and industry contacts to ensure comprehensive coverage of market developments and emerging trends.

Market modeling techniques apply statistical analysis and forecasting methodologies to project future market growth and identify key success factors. The research framework considers macroeconomic indicators, technology adoption curves, and regulatory developments affecting data center construction demand.

Quality assurance protocols ensure data accuracy through cross-validation of sources, expert review processes, and continuous monitoring of market developments. The research methodology maintains objectivity while providing actionable insights for industry participants and stakeholders.

Dubai emirate commands the largest share of data center construction activity, accounting for approximately 55% of total market volume. The emirate’s strategic location, advanced telecommunications infrastructure, and business-friendly environment attract major international data center operators and cloud service providers. Dubai Internet City and surrounding areas host numerous large-scale construction projects.

Abu Dhabi represents the second-largest construction market, driven by government initiatives and the presence of major telecommunications companies. The emirate focuses on sustainable data center construction and smart city infrastructure development, with several hyperscale facilities under construction to support artificial intelligence and blockchain initiatives.

Sharjah and Northern Emirates show growing construction activity, particularly for edge computing facilities and smaller enterprise data centers. These regions benefit from lower land costs and proximity to Dubai’s technology ecosystem while providing alternative locations for disaster recovery and backup facilities.

Free zone developments across multiple emirates create specialized environments for data center construction with streamlined regulatory processes and attractive investment incentives. These zones facilitate international investment and provide dedicated infrastructure for technology companies establishing regional operations.

Cross-emirate connectivity projects enhance the attractiveness of distributed data center construction strategies. Fiber optic networks and power grid interconnections enable construction of geographically dispersed facilities while maintaining high-performance connectivity and redundancy capabilities.

Market leadership includes both international construction giants and specialized regional contractors with data center expertise:

Competitive strategies emphasize specialization in data center construction, development of modular construction capabilities, and strategic partnerships with technology providers. Companies invest heavily in skilled workforce development and advanced construction methodologies to maintain market position.

Market differentiation focuses on construction speed, sustainability credentials, and post-completion support services. Leading contractors develop proprietary construction techniques and maintain strategic relationships with equipment suppliers to ensure competitive project delivery.

By Facility Type:

By Construction Type:

By End-User Sector:

Hyperscale data center construction represents the highest-value segment, requiring sophisticated engineering solutions and substantial capital investment. These projects typically involve construction of facilities exceeding 10,000 square meters with advanced cooling systems, redundant power infrastructure, and high-density server configurations. Construction timelines for hyperscale facilities range from 18 to 36 months depending on complexity and customization requirements.

Colocation facility construction focuses on multi-tenant environments with flexible space allocation and shared infrastructure services. These projects require careful planning for diverse client requirements, scalable power distribution, and secure access control systems. Modular design approaches enable phased construction and future expansion capabilities.

Edge data center construction emphasizes rapid deployment and standardized designs suitable for distributed deployment across urban areas. These smaller facilities typically require 6 to 12 months construction time and focus on automated operations with minimal on-site staffing requirements.

Enterprise data center construction involves customized solutions meeting specific organizational requirements for security, compliance, and operational procedures. These projects often incorporate specialized features such as enhanced physical security, regulatory compliance systems, and integration with existing corporate infrastructure.

Sustainable construction practices have become standard across all categories, with new facilities targeting LEED Gold certification and incorporating renewable energy systems, advanced cooling technologies, and energy-efficient building materials.

Construction companies benefit from substantial revenue opportunities in a growing market with high barriers to entry. Specialized data center construction expertise commands premium pricing and provides competitive differentiation. Long-term maintenance contracts and expansion projects create recurring revenue streams beyond initial construction phases.

Technology companies gain access to world-class data center infrastructure supporting their digital transformation and cloud service offerings. Purpose-built facilities provide optimal performance, reliability, and scalability for mission-critical applications and services.

Government entities achieve strategic objectives for digital government services, smart city initiatives, and economic diversification. Data center infrastructure supports public sector efficiency improvements and enables innovative citizen services through advanced technology platforms.

Investors access attractive returns in a growing infrastructure sector with stable demand drivers and long-term lease agreements. Data center construction projects typically provide predictable cash flows and appreciation potential in strategic locations.

Local communities benefit from job creation, skills development, and economic activity generated by data center construction projects. These facilities often provide ongoing employment opportunities and support development of technology sector expertise.

End-users gain access to reliable, secure, and high-performance data center services supporting their business operations and digital initiatives. Modern facilities provide enhanced uptime, security, and connectivity compared to traditional infrastructure alternatives.

Strengths:

Weaknesses:

Opportunities:

Threats:

Sustainable construction practices have become fundamental requirements rather than optional features. New data center construction projects increasingly incorporate renewable energy systems, advanced cooling technologies, and green building materials. Energy efficiency improvements of up to 50% compared to traditional designs are becoming standard expectations from clients and regulatory authorities.

Modular construction methodologies gain widespread adoption for their ability to reduce construction timelines and improve quality control. Prefabricated data center modules enable faster deployment and provide scalability advantages for future expansion requirements. This trend particularly benefits edge computing facility construction where rapid deployment is essential.

Liquid cooling systems emerge as preferred solutions for high-density server configurations and artificial intelligence applications. These advanced cooling technologies require specialized construction expertise and infrastructure modifications but provide significant energy efficiency improvements and space optimization benefits.

Automation integration during construction phases incorporates IoT sensors, building information modeling, and automated quality assurance systems. These technologies improve project management efficiency and ensure compliance with stringent data center performance requirements while reducing construction risks and delays.

Security enhancement becomes increasingly sophisticated with biometric access controls, advanced surveillance systems, and multi-layered physical security measures. Construction projects must accommodate these security requirements from initial design phases through final commissioning and operational handover.

Major construction projects announced recently include several hyperscale data center facilities in Dubai and Abu Dhabi, representing substantial investments in regional digital infrastructure. These projects incorporate cutting-edge construction technologies and sustainable design principles while providing significant capacity expansion for cloud services and digital applications.

Technology partnerships between construction companies and equipment manufacturers enable development of specialized construction capabilities and access to advanced data center technologies. These strategic relationships facilitate knowledge transfer and ensure construction teams remain current with evolving industry requirements and best practices.

Regulatory developments include updated building codes specifically addressing data center construction requirements, environmental impact assessments, and energy efficiency standards. MWR analysis indicates these regulatory changes will drive adoption of more sophisticated construction techniques and sustainable building practices.

Workforce development initiatives launched by construction companies and government agencies address skilled labor shortages through specialized training programs and certification processes. These programs focus on data center construction techniques, advanced cooling systems, and power infrastructure installation.

International expansion by regional construction companies includes establishment of specialized data center construction divisions and strategic partnerships with global technology providers. These developments enhance local construction capabilities and provide access to international best practices and advanced construction methodologies.

Strategic positioning recommendations emphasize development of specialized data center construction capabilities and strategic partnerships with technology providers. Construction companies should invest in workforce training, advanced construction methodologies, and sustainable building practices to maintain competitive advantages in this growing market segment.

Technology adoption priorities include implementation of modular construction techniques, building information modeling systems, and automated quality assurance processes. These technologies improve project delivery efficiency and ensure compliance with stringent data center performance requirements while reducing construction risks and timelines.

Sustainability integration should become a core competency rather than an optional service offering. Construction companies must develop expertise in renewable energy systems, advanced cooling technologies, and green building certification processes to meet evolving client expectations and regulatory requirements.

Market diversification strategies should consider expansion into edge computing facility construction, government infrastructure projects, and specialized applications such as artificial intelligence and blockchain data centers. These emerging segments provide growth opportunities and reduce dependence on traditional hyperscale construction projects.

Partnership development with equipment manufacturers, technology providers, and facility operators creates competitive advantages through access to advanced technologies, preferred supplier relationships, and ongoing maintenance contract opportunities. These strategic relationships enhance project delivery capabilities and provide recurring revenue streams.

Market expansion projections indicate continued robust growth driven by accelerating digital transformation, 5G network deployment, and artificial intelligence adoption across multiple industry sectors. The construction market is expected to maintain strong momentum with projected growth rates of approximately 12-15% annually over the next five years.

Technology evolution will drive demand for more sophisticated construction capabilities including liquid cooling systems, high-density power distribution, and advanced security infrastructure. Construction companies must continuously adapt to evolving technology requirements while maintaining expertise in traditional data center construction disciplines.

Sustainability requirements will become increasingly stringent, with new facilities expected to achieve carbon neutrality and incorporate renewable energy systems. MarkWide Research projects that sustainable construction practices will become mandatory rather than optional, driving innovation in building materials and construction methodologies.

Regional expansion opportunities include serving broader Middle East and Africa markets from UAE-based construction capabilities. The country’s strategic location and advanced infrastructure provide natural advantages for regional data center construction projects and cross-border technology initiatives.

Market consolidation trends may accelerate as larger construction companies acquire specialized contractors to expand service capabilities and geographic coverage. This consolidation will create more comprehensive service offerings while potentially reducing the number of independent specialized contractors in the market.

The UAE data center construction market represents a dynamic and rapidly expanding sector driven by digital transformation, government initiatives, and strategic geographic advantages. Strong growth fundamentals, supported by robust demand from cloud service providers, telecommunications companies, and government agencies, position this market for continued expansion over the coming years.

Construction companies that develop specialized expertise in data center construction, sustainable building practices, and advanced technologies will be well-positioned to capitalize on substantial growth opportunities. The market rewards innovation, quality, and reliability while providing attractive returns for companies capable of delivering complex infrastructure projects on time and within budget.

Future success in this market will depend on continuous adaptation to evolving technology requirements, sustainability mandates, and client expectations. Companies that invest in workforce development, strategic partnerships, and advanced construction methodologies will maintain competitive advantages in this sophisticated and growing market segment, contributing to the UAE’s transformation into a global digital hub.

What is Data Center Construction?

Data Center Construction refers to the process of building facilities that house computer systems and associated components, such as telecommunications and storage systems. These centers are crucial for managing data and supporting cloud computing, big data analytics, and various IT services.

What are the key players in the UAE Data Center Construction Market?

Key players in the UAE Data Center Construction Market include companies like Etisalat, du, and Gulf Data Hub. These companies are involved in the design, construction, and operation of data centers, catering to the growing demand for digital infrastructure in the region.

What are the main drivers of the UAE Data Center Construction Market?

The main drivers of the UAE Data Center Construction Market include the increasing demand for cloud services, the rise of digital transformation initiatives, and the growth of e-commerce. Additionally, government support for technology infrastructure is also a significant factor.

What challenges does the UAE Data Center Construction Market face?

The UAE Data Center Construction Market faces challenges such as high construction costs, regulatory hurdles, and the need for skilled labor. Additionally, the rapid pace of technological change can make it difficult for companies to keep up with the latest standards and requirements.

What opportunities exist in the UAE Data Center Construction Market?

Opportunities in the UAE Data Center Construction Market include the expansion of renewable energy sources for powering data centers, the increasing adoption of edge computing, and the potential for partnerships with tech firms. These trends can enhance operational efficiency and sustainability.

What trends are shaping the UAE Data Center Construction Market?

Trends shaping the UAE Data Center Construction Market include the shift towards modular data center designs, the integration of advanced cooling technologies, and the focus on sustainability practices. These innovations aim to improve energy efficiency and reduce the environmental impact of data centers.

UAE Data Center Construction Market

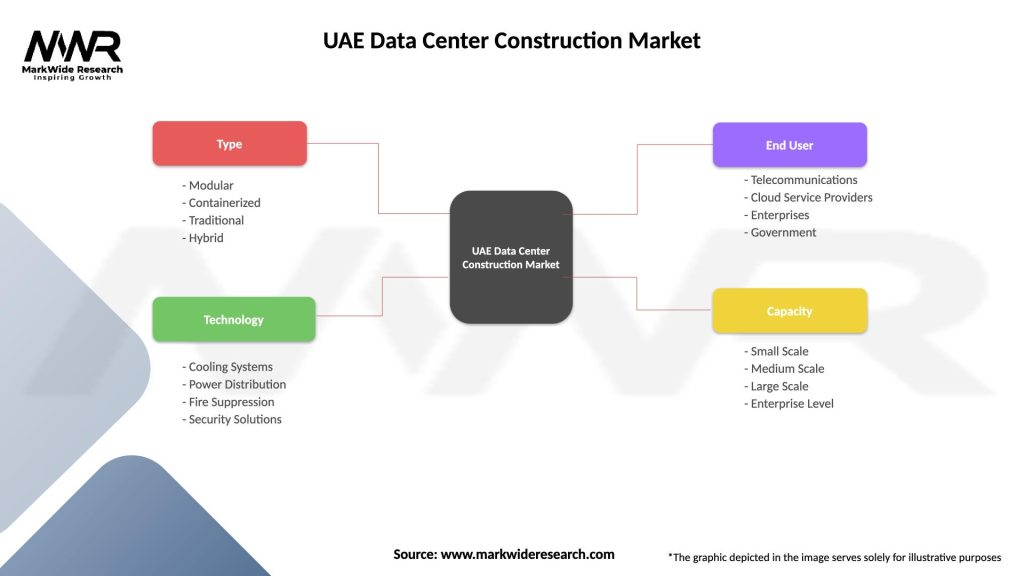

| Segmentation Details | Description |

|---|---|

| Type | Modular, Containerized, Traditional, Hybrid |

| Technology | Cooling Systems, Power Distribution, Fire Suppression, Security Solutions |

| End User | Telecommunications, Cloud Service Providers, Enterprises, Government |

| Capacity | Small Scale, Medium Scale, Large Scale, Enterprise Level |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the UAE Data Center Construction Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.