444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Japan data center rack market represents a critical component of the nation’s rapidly expanding digital infrastructure ecosystem. As Japan continues its digital transformation journey, the demand for sophisticated data center solutions has reached unprecedented levels, driving significant growth in the rack infrastructure segment. The market encompasses various rack types, including server racks, network racks, and storage racks, each designed to meet specific operational requirements of modern data centers.

Market dynamics indicate robust expansion driven by increasing cloud adoption, edge computing deployment, and the proliferation of IoT devices across Japanese enterprises. The market is experiencing a compound annual growth rate (CAGR) of 8.2%, reflecting the strong demand for reliable and efficient data center infrastructure. Tokyo and Osaka emerge as primary growth centers, accounting for approximately 65% of total market activity, while regional data centers contribute to the remaining market share.

Technological advancement plays a pivotal role in shaping market trends, with manufacturers focusing on developing energy-efficient, high-density rack solutions that align with Japan’s sustainability goals. The integration of intelligent rack management systems and advanced cooling technologies has become increasingly important as organizations seek to optimize their data center operations while reducing environmental impact.

The Japan data center rack market refers to the comprehensive ecosystem of physical infrastructure solutions designed to house, organize, and protect critical IT equipment within data center facilities across Japan. These specialized mounting structures serve as the backbone of modern data centers, providing standardized frameworks for servers, networking equipment, storage systems, and associated hardware components.

Data center racks encompass various configurations including open frame racks, enclosed server cabinets, wall-mount racks, and custom-designed solutions tailored to specific operational requirements. The market includes both the physical rack hardware and complementary accessories such as power distribution units, cable management systems, and environmental monitoring equipment that ensure optimal performance and reliability.

Furthermore, the market extends beyond traditional hardware to include intelligent rack solutions featuring integrated monitoring capabilities, remote management functionality, and advanced security features. These sophisticated systems enable data center operators to maintain optimal environmental conditions, monitor equipment health, and ensure maximum uptime for critical business applications.

Japan’s data center rack market demonstrates exceptional growth momentum, driven by the nation’s commitment to digital innovation and technological leadership. The market benefits from strong government support for digital infrastructure development, substantial corporate investments in cloud computing, and the increasing adoption of edge computing solutions across various industry sectors.

Key market drivers include the rapid expansion of hyperscale data centers, growing demand for colocation services, and the need for modernized IT infrastructure to support emerging technologies such as artificial intelligence and machine learning. The market shows particular strength in the 42U rack segment, which represents approximately 45% of total market share due to its optimal balance of capacity and space efficiency.

Competitive landscape features both international technology leaders and domestic manufacturers, creating a dynamic environment that fosters innovation and competitive pricing. The market is characterized by increasing consolidation among service providers and growing emphasis on sustainable, energy-efficient solutions that align with Japan’s environmental objectives.

Regional distribution shows concentration in major metropolitan areas, with Tokyo metropolitan region accounting for the largest market share, followed by Osaka, Nagoya, and other key industrial centers. The market outlook remains highly positive, with continued growth expected across all major segments and geographic regions.

Market intelligence reveals several critical insights that define the current landscape and future trajectory of Japan’s data center rack market:

Digital transformation initiatives across Japanese enterprises serve as the primary catalyst for data center rack market expansion. Organizations increasingly recognize the strategic importance of robust IT infrastructure in maintaining competitive advantage, driving substantial investments in modern data center facilities and supporting equipment.

Cloud adoption acceleration represents another significant growth driver, with Japanese companies migrating workloads to cloud platforms at unprecedented rates. This trend necessitates expanded data center capacity and more sophisticated rack infrastructure to support diverse computing requirements and ensure optimal performance levels.

Government initiatives promoting digital innovation and smart city development create favorable conditions for market growth. Japan’s commitment to becoming a leading digital economy drives public and private sector investments in advanced IT infrastructure, including state-of-the-art data center facilities equipped with modern rack solutions.

Emerging technologies such as artificial intelligence, machine learning, and Internet of Things applications require specialized computing environments that demand high-performance rack infrastructure. The growing adoption of these technologies across various industry sectors creates sustained demand for advanced data center solutions.

Disaster recovery planning has become increasingly important following natural disasters, driving organizations to invest in redundant data center infrastructure and geographically distributed facilities. This trend supports market growth as companies establish multiple data center locations with comprehensive rack infrastructure.

High initial investment requirements pose significant challenges for organizations considering data center infrastructure upgrades. The substantial capital expenditure associated with modern rack solutions, including supporting systems and installation costs, can limit market growth among smaller enterprises and budget-conscious organizations.

Space constraints in major metropolitan areas create limitations for data center expansion, particularly in Tokyo and other densely populated regions. Limited availability of suitable real estate for data center development restricts market growth potential and increases operational costs for facility operators.

Skilled workforce shortage represents a critical challenge affecting market development. The complexity of modern data center operations requires specialized technical expertise, and the limited availability of qualified professionals can constrain market growth and increase operational costs.

Regulatory compliance requirements add complexity and cost to data center operations, particularly regarding environmental standards, safety regulations, and data protection laws. These compliance obligations can slow market adoption and increase the total cost of ownership for data center infrastructure.

Technology obsolescence concerns influence purchasing decisions, as organizations worry about investing in solutions that may become outdated quickly. The rapid pace of technological change creates uncertainty about long-term infrastructure investments and can delay purchasing decisions.

Edge computing expansion presents substantial growth opportunities as organizations deploy distributed computing resources closer to end users. This trend creates demand for smaller, specialized data center facilities equipped with appropriate rack infrastructure to support edge applications and reduce latency.

5G network deployment across Japan opens new market segments for data center rack solutions. The infrastructure requirements for 5G networks include numerous edge data centers and distributed computing facilities, creating significant opportunities for rack manufacturers and service providers.

Sustainability initiatives drive demand for energy-efficient, environmentally friendly rack solutions. Organizations increasingly prioritize green technology solutions, creating opportunities for manufacturers developing innovative, sustainable data center infrastructure products.

Artificial intelligence adoption requires specialized computing environments with high-density rack configurations and advanced cooling systems. The growing implementation of AI applications across various industries creates opportunities for specialized rack solutions designed to support intensive computing workloads.

Hybrid cloud strategies adopted by Japanese enterprises create demand for flexible, scalable data center infrastructure. Organizations implementing hybrid cloud approaches require versatile rack solutions that can accommodate diverse computing requirements and support seamless integration between on-premises and cloud resources.

Supply chain evolution significantly impacts market dynamics, with manufacturers adapting to global component shortages and logistics challenges. The industry has demonstrated resilience by diversifying supplier networks and implementing more flexible manufacturing processes to maintain product availability and competitive pricing.

Technological convergence between traditional IT infrastructure and emerging technologies creates new market dynamics. The integration of edge computing, IoT, and AI technologies requires rack solutions that can accommodate diverse equipment types and support varying power and cooling requirements.

Customer expectations continue to evolve, with organizations demanding more sophisticated, intelligent rack solutions that provide enhanced monitoring, management, and security capabilities. This shift drives innovation among manufacturers and creates opportunities for value-added services and solutions.

Competitive pressure intensifies as both domestic and international players compete for market share. This dynamic environment fosters innovation, drives down costs, and accelerates the development of advanced rack technologies that benefit end users.

Partnership strategies become increasingly important as companies seek to offer comprehensive solutions that combine hardware, software, and services. Strategic alliances between rack manufacturers, data center operators, and technology providers create new market opportunities and enhance customer value propositions.

Comprehensive market analysis employs multiple research methodologies to ensure accurate and reliable insights into Japan’s data center rack market. The research approach combines quantitative and qualitative analysis techniques to provide a complete understanding of market dynamics, trends, and growth opportunities.

Primary research activities include extensive interviews with industry executives, data center operators, equipment manufacturers, and technology vendors. These discussions provide valuable insights into market trends, customer requirements, competitive dynamics, and future growth prospects from key stakeholders across the value chain.

Secondary research encompasses analysis of industry reports, company financial statements, government publications, and trade association data. This comprehensive review of existing information sources ensures thorough coverage of market developments and provides context for primary research findings.

Market sizing methodology utilizes bottom-up and top-down approaches to validate market estimates and growth projections. The analysis considers various factors including data center capacity expansion, rack replacement cycles, and new facility construction to develop accurate market forecasts.

Data validation processes ensure research accuracy through triangulation of multiple information sources and verification with industry experts. This rigorous approach maintains the highest standards of research quality and provides reliable insights for strategic decision-making.

Tokyo Metropolitan Area dominates Japan’s data center rack market, accounting for approximately 42% of total market activity. The region benefits from high concentration of enterprises, government agencies, and financial institutions that require sophisticated data center infrastructure. Major hyperscale data centers and colocation facilities in the area drive substantial demand for advanced rack solutions.

Osaka Region represents the second-largest market segment, contributing approximately 23% of national market share. The area serves as a critical hub for manufacturing and logistics operations, creating strong demand for data center infrastructure to support industrial automation and supply chain management applications.

Nagoya and surrounding areas account for roughly 12% of market activity, driven primarily by automotive industry requirements and manufacturing operations. The region’s focus on industrial IoT and smart manufacturing creates specific demand for edge computing infrastructure and specialized rack solutions.

Regional data centers in smaller metropolitan areas contribute the remaining 23% of market share, reflecting the growing trend toward distributed computing and edge infrastructure deployment. These facilities typically require smaller-scale but highly reliable rack solutions to support local business operations and government services.

Geographic distribution trends show increasing investment in disaster recovery facilities and geographically distributed data centers. This development pattern creates opportunities for rack manufacturers to expand their presence beyond traditional metropolitan concentrations and serve emerging regional markets.

Market leadership is shared among several key players, each bringing unique strengths and capabilities to Japan’s data center rack market:

Competitive strategies focus on product innovation, customer service excellence, and strategic partnerships with data center operators and system integrators. Companies increasingly emphasize sustainability, energy efficiency, and intelligent management capabilities to differentiate their offerings in the competitive marketplace.

By Rack Type:

By Rack Unit Size:

By End-User Industry:

Server Racks Category represents the largest market segment, driven by continuous server hardware upgrades and capacity expansion requirements. Modern server racks incorporate advanced features such as integrated power distribution, intelligent monitoring systems, and optimized airflow management to support high-density computing environments.

Network Racks Segment shows strong growth due to increasing network infrastructure complexity and the deployment of advanced networking equipment. These specialized racks accommodate switches, routers, and other networking hardware while providing optimal cable management and accessibility for maintenance operations.

Storage Racks Category benefits from growing data storage requirements and the adoption of high-capacity storage systems. Modern storage racks feature enhanced structural support, vibration dampening, and specialized cooling systems to ensure optimal performance of sensitive storage equipment.

Specialty Racks Segment includes custom solutions designed for specific applications such as edge computing, industrial environments, and outdoor installations. This category shows rapid growth as organizations deploy computing resources in diverse locations and challenging environments.

Intelligent Racks Category represents the fastest-growing segment, featuring integrated monitoring, management, and security capabilities. These advanced solutions provide real-time visibility into rack conditions, equipment status, and environmental parameters, enabling proactive maintenance and optimization.

Data Center Operators benefit from improved operational efficiency, reduced maintenance costs, and enhanced equipment reliability through modern rack solutions. Advanced rack systems provide better organization, easier maintenance access, and integrated monitoring capabilities that streamline data center operations.

Equipment Manufacturers gain access to standardized mounting platforms that simplify product design and installation processes. Rack standardization enables manufacturers to develop equipment that integrates seamlessly with various data center environments, reducing complexity and costs.

System Integrators benefit from comprehensive rack solutions that simplify installation processes and reduce project timelines. Integrated rack systems with pre-configured components enable faster deployment and more predictable project outcomes for complex data center implementations.

End-User Organizations achieve improved IT infrastructure reliability, better space utilization, and enhanced security through professional rack solutions. Modern rack systems provide organized, secure environments that protect critical equipment while enabling efficient operations and maintenance.

Service Providers can offer enhanced value propositions through advanced rack infrastructure that supports diverse customer requirements. Flexible, scalable rack solutions enable service providers to accommodate various equipment types and configurations while maintaining operational efficiency.

Strengths:

Weaknesses:

Opportunities:

Threats:

Intelligent Infrastructure Integration emerges as a dominant trend, with rack manufacturers incorporating advanced monitoring, management, and automation capabilities into their solutions. These intelligent systems provide real-time visibility into rack conditions, equipment status, and environmental parameters, enabling proactive maintenance and optimization.

Sustainability and Energy Efficiency become increasingly important considerations in rack design and selection. Manufacturers focus on developing solutions that minimize environmental impact through efficient materials usage, recyclable components, and energy-saving features that align with corporate sustainability goals.

Modular and Scalable Designs gain popularity as organizations seek flexible infrastructure solutions that can adapt to changing requirements. Modular rack systems enable easy expansion, reconfiguration, and upgrade capabilities without major infrastructure overhauls.

Edge Computing Optimization drives development of specialized rack solutions designed for distributed computing environments. These solutions emphasize compact form factors, enhanced security features, and remote management capabilities suitable for unmanned edge locations.

Liquid Cooling Integration becomes more prevalent as high-density computing requirements exceed traditional air cooling capabilities. Rack manufacturers develop solutions that accommodate liquid cooling systems while maintaining accessibility and serviceability.

Strategic partnerships between rack manufacturers and cloud service providers accelerate product development and market adoption. These collaborations result in customized solutions that meet specific hyperscale requirements while driving innovation across the broader market.

Technology acquisitions enable companies to expand their capabilities and market reach through complementary technologies and expertise. Recent acquisitions focus on intelligent management systems, cooling technologies, and edge computing solutions.

Product launches featuring advanced capabilities such as integrated power management, intelligent monitoring, and enhanced security features demonstrate continued innovation in the rack market. These new solutions address evolving customer requirements and emerging technology trends.

Manufacturing expansion in Japan and other Asian markets reflects growing regional demand and the need for local production capabilities. Companies invest in new facilities and production capacity to serve the expanding Japanese market more effectively.

Sustainability initiatives across the industry focus on developing environmentally friendly products and manufacturing processes. Companies implement circular economy principles, reduce material waste, and develop recyclable products to meet growing environmental requirements.

MarkWide Research recommends that market participants focus on developing comprehensive solutions that combine hardware, software, and services to address evolving customer requirements. The integration of intelligent management capabilities and sustainability features will become increasingly important for competitive differentiation.

Investment priorities should emphasize research and development activities focused on edge computing solutions, liquid cooling integration, and intelligent infrastructure management. These areas represent the highest growth potential and align with major technology trends affecting the data center industry.

Partnership strategies should target system integrators, cloud service providers, and colocation operators to expand market reach and develop specialized solutions. Strategic alliances enable companies to leverage complementary expertise and accelerate market penetration.

Geographic expansion into regional markets outside major metropolitan areas presents opportunities for growth as edge computing and distributed infrastructure deployment increases. Companies should develop solutions and support capabilities tailored to these emerging market segments.

Customer engagement initiatives should focus on understanding evolving requirements and providing consultative support throughout the solution lifecycle. Companies that demonstrate deep understanding of customer challenges and provide comprehensive support will achieve competitive advantage.

Market growth trajectory remains highly positive, with continued expansion expected across all major segments and geographic regions. The increasing digitization of business processes, adoption of cloud computing, and deployment of emerging technologies will sustain demand for advanced data center rack solutions.

Technology evolution will drive development of more sophisticated, intelligent rack solutions that provide enhanced monitoring, management, and automation capabilities. The integration of artificial intelligence and machine learning technologies will enable predictive maintenance and optimization features that improve operational efficiency.

Edge computing expansion will create substantial new market opportunities as organizations deploy distributed computing resources closer to end users. This trend will drive demand for specialized rack solutions designed for edge environments and remote locations.

Sustainability requirements will become increasingly important, with organizations prioritizing energy-efficient, environmentally friendly solutions. Manufacturers that successfully develop sustainable products and manufacturing processes will gain competitive advantage in the evolving market.

Market consolidation may occur as companies seek to achieve scale advantages and expand their capabilities through strategic acquisitions. This trend could result in fewer but larger players with comprehensive solution portfolios and global reach.

Japan’s data center rack market demonstrates exceptional growth potential driven by digital transformation initiatives, cloud adoption, and emerging technology deployment. The market benefits from strong fundamentals including substantial infrastructure investment, technological innovation, and growing demand for sophisticated data center solutions.

Key success factors for market participants include focus on product innovation, customer service excellence, and strategic partnerships that enable comprehensive solution delivery. Companies that successfully integrate intelligent management capabilities, sustainability features, and edge computing optimization will achieve competitive advantage in the evolving marketplace.

MWR analysis indicates that the market will continue expanding across all major segments, with particular strength in intelligent rack solutions, edge computing applications, and sustainability-focused products. Organizations that align their strategies with these trends and invest in appropriate capabilities will be well-positioned for long-term success in Japan’s dynamic data center rack market.

What is Data Center Rack?

Data Center Rack refers to a standardized frame or enclosure used to house servers, networking equipment, and other hardware in a data center environment. These racks are designed to optimize space, improve cooling efficiency, and facilitate organization within data centers.

What are the key players in the Japan Data Center Rack Market?

Key players in the Japan Data Center Rack Market include companies like Fujitsu, NEC Corporation, and Hitachi, which provide a range of data center solutions and infrastructure. These companies are known for their innovative technologies and robust product offerings, among others.

What are the growth factors driving the Japan Data Center Rack Market?

The Japan Data Center Rack Market is driven by the increasing demand for cloud computing services, the rise in data generation, and the need for efficient data management solutions. Additionally, the expansion of IT infrastructure and the adoption of advanced technologies contribute to market growth.

What challenges does the Japan Data Center Rack Market face?

Challenges in the Japan Data Center Rack Market include the high costs associated with advanced data center technologies and the complexity of integrating new systems with existing infrastructure. Additionally, the rapid pace of technological change can make it difficult for companies to keep up.

What opportunities exist in the Japan Data Center Rack Market?

Opportunities in the Japan Data Center Rack Market include the growing trend of edge computing and the increasing focus on energy-efficient solutions. As businesses seek to enhance their data processing capabilities, there is potential for innovative rack designs and smart technologies.

What trends are shaping the Japan Data Center Rack Market?

Trends in the Japan Data Center Rack Market include the shift towards modular data center designs and the integration of IoT technologies for better monitoring and management. Additionally, sustainability initiatives are prompting companies to adopt greener practices in their data center operations.

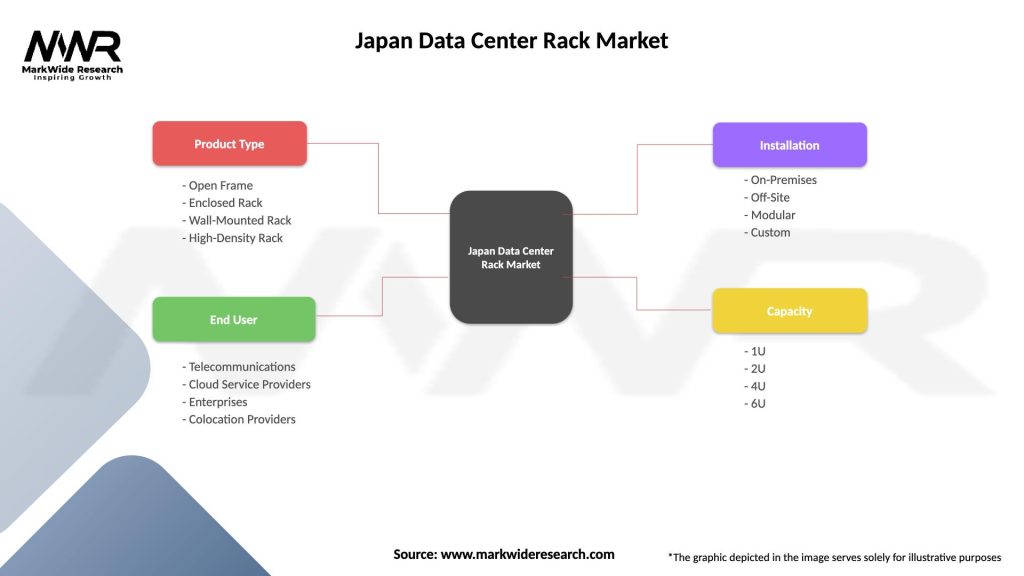

Japan Data Center Rack Market

| Segmentation Details | Description |

|---|---|

| Product Type | Open Frame, Enclosed Rack, Wall-Mounted Rack, High-Density Rack |

| End User | Telecommunications, Cloud Service Providers, Enterprises, Colocation Providers |

| Installation | On-Premises, Off-Site, Modular, Custom |

| Capacity | 1U, 2U, 4U, 6U |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Japan Data Center Rack Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.