444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Saudi Arabia data center rack market represents a critical infrastructure component driving the Kingdom’s digital transformation initiatives and Vision 2030 objectives. Data center racks serve as the fundamental backbone for housing servers, networking equipment, and storage systems across enterprise facilities, cloud service providers, and telecommunications infrastructure. The market demonstrates robust growth momentum with expanding digitalization efforts, increasing cloud adoption, and substantial investments in smart city projects throughout the region.

Market dynamics indicate accelerating demand driven by government-led digital initiatives, growing e-commerce activities, and expanding telecommunications infrastructure. The Kingdom’s strategic position as a regional technology hub continues attracting international cloud providers and data center operators, creating substantial opportunities for rack infrastructure providers. Growth projections suggest the market will experience a compound annual growth rate of 8.2% through the forecast period, supported by increasing data generation and storage requirements across various industry verticals.

Infrastructure development initiatives, including NEOM and other mega-projects, are significantly contributing to market expansion. The integration of advanced technologies such as artificial intelligence, Internet of Things, and 5G networks necessitates sophisticated data center infrastructure, positioning rack systems as essential components for supporting these technological advancements.

The Saudi Arabia data center rack market refers to the comprehensive ecosystem encompassing the design, manufacturing, distribution, and installation of specialized rack systems used to house and organize IT equipment within data center facilities across the Kingdom. Data center racks are standardized mounting structures that provide physical support, power distribution, cooling management, and cable organization for servers, switches, storage devices, and other critical IT infrastructure components.

These systems include various configurations such as open frame racks, enclosed server cabinets, wall-mounted racks, and specialized cooling-integrated solutions designed to optimize space utilization, enhance equipment accessibility, and ensure proper airflow management. The market encompasses both standard 19-inch and 23-inch rack formats, accommodating diverse equipment requirements across enterprise, colocation, hyperscale, and edge computing environments.

Market scope extends beyond basic rack hardware to include complementary accessories such as power distribution units, cable management systems, environmental monitoring solutions, and security features that collectively create comprehensive data center infrastructure solutions tailored to Saudi Arabia’s specific operational requirements and regulatory compliance standards.

The Saudi Arabia data center rack market exhibits exceptional growth potential driven by the Kingdom’s ambitious digital transformation agenda and substantial technology infrastructure investments. Market expansion is primarily fueled by increasing enterprise digitalization, cloud service adoption, and government initiatives promoting smart city development and Industry 4.0 implementation across various economic sectors.

Key market drivers include the establishment of hyperscale data centers by international cloud providers, growing demand for edge computing solutions, and expanding telecommunications infrastructure supporting 5G network deployment. The market benefits from favorable government policies encouraging foreign investment in technology infrastructure and the development of local manufacturing capabilities for IT equipment and components.

Competitive landscape features both international rack manufacturers and emerging local suppliers, creating a dynamic market environment with diverse product offerings and pricing strategies. Technology trends toward higher density computing, improved cooling efficiency, and modular rack designs are shaping product development and market positioning strategies among key industry participants.

Future outlook remains highly positive, with market growth expected to accelerate as Saudi Arabia continues implementing Vision 2030 initiatives and establishing itself as a regional technology and innovation hub, driving sustained demand for advanced data center infrastructure solutions.

Strategic market insights reveal several critical factors influencing the Saudi Arabia data center rack market development and competitive dynamics:

Digital transformation initiatives across Saudi Arabia’s public and private sectors represent the primary catalyst driving data center rack market expansion. Government digitalization programs encompassing e-government services, smart city projects, and digital identity systems require substantial IT infrastructure investments, creating consistent demand for rack systems and related components.

Cloud adoption acceleration among Saudi enterprises drives significant infrastructure requirements as organizations migrate from on-premises systems to hybrid and cloud-based architectures. This transition necessitates modern data center facilities equipped with standardized rack systems capable of supporting diverse workloads and scalable computing resources.

Vision 2030 implementation continues generating substantial technology infrastructure investments across various economic sectors, including healthcare, education, manufacturing, and financial services. These initiatives require robust data center capabilities supported by reliable rack infrastructure to ensure optimal equipment performance and operational efficiency.

5G network deployment throughout the Kingdom creates new infrastructure requirements for edge computing facilities and distributed data centers. Telecommunications expansion drives demand for specialized rack configurations optimized for network equipment and edge computing applications, contributing to market diversification and growth opportunities.

Foreign investment attraction in technology infrastructure brings international cloud providers and data center operators to Saudi Arabia, creating demand for standardized rack solutions meeting global operational requirements and compliance standards.

High initial investment requirements for comprehensive data center infrastructure, including rack systems and associated components, present significant barriers for smaller enterprises and organizations with limited capital budgets. Cost considerations often delay infrastructure upgrades and expansion projects, particularly among price-sensitive market segments.

Technical complexity associated with modern rack systems and their integration with cooling, power, and monitoring systems requires specialized expertise that may be limited in certain regions of Saudi Arabia. Skills shortages in data center design, installation, and maintenance can constrain market growth and increase project implementation costs.

Supply chain dependencies on international manufacturers for advanced rack components and specialized accessories create potential vulnerabilities related to delivery schedules, pricing fluctuations, and geopolitical factors affecting global trade relationships.

Regulatory compliance requirements for data center infrastructure, including environmental standards, safety regulations, and security specifications, may increase project complexity and costs while potentially limiting product selection options for certain applications.

Energy infrastructure limitations in some regions may constrain data center development and, consequently, demand for rack systems, particularly for high-density computing applications requiring substantial power and cooling resources.

NEOM and mega-project development present unprecedented opportunities for data center rack suppliers to participate in large-scale infrastructure projects requiring innovative and sustainable technology solutions. Smart city initiatives across multiple Saudi regions create diverse market segments with varying rack system requirements and specifications.

Local manufacturing development offers significant opportunities for establishing domestic production capabilities, reducing import costs, and creating value-added services for the regional market. Government incentives supporting local manufacturing and technology transfer create favorable conditions for international companies seeking market entry strategies.

Edge computing expansion driven by 5G deployment and IoT applications creates new market segments for compact, ruggedized, and specialized rack solutions designed for distributed computing environments. Industry 4.0 adoption across manufacturing and industrial sectors generates demand for edge data center infrastructure supporting real-time analytics and automation systems.

Sustainability focus creates opportunities for developing energy-efficient rack designs, integrated cooling solutions, and environmentally friendly materials that align with Saudi Arabia’s environmental goals and corporate sustainability initiatives.

Regional expansion potential allows successful suppliers to leverage Saudi Arabia as a base for serving broader Middle East and North Africa markets, capitalizing on the Kingdom’s strategic geographic position and growing regional influence in technology sectors.

Supply and demand dynamics in the Saudi Arabia data center rack market reflect the complex interplay between rapid infrastructure development, evolving technology requirements, and supply chain considerations. Demand patterns show strong correlation with government spending cycles, private sector digitalization initiatives, and international investment flows into the Kingdom’s technology sector.

Pricing dynamics demonstrate increasing pressure for cost optimization while maintaining quality and performance standards. Market competition intensifies as both international suppliers and emerging local manufacturers compete for market share, driving innovation and competitive pricing strategies across various product segments.

Technology evolution continues influencing market dynamics through the introduction of higher-density rack configurations, improved cooling integration, and enhanced monitoring capabilities. Customer preferences increasingly favor modular and scalable solutions that provide flexibility for future expansion and technology upgrades.

Regulatory influences shape market dynamics through evolving standards for data center infrastructure, environmental compliance, and security requirements. Policy changes related to local content requirements and import regulations create both challenges and opportunities for market participants.

Investment cycles in major infrastructure projects create periodic demand surges followed by consolidation periods, requiring suppliers to maintain flexible capacity and inventory management strategies to effectively serve market requirements.

Comprehensive market research for the Saudi Arabia data center rack market employs multiple methodological approaches to ensure accurate and reliable market intelligence. Primary research includes structured interviews with key industry stakeholders, including data center operators, IT infrastructure managers, government officials, and rack system suppliers operating within the Kingdom.

Secondary research encompasses analysis of government publications, industry reports, trade statistics, and regulatory documentation related to data center infrastructure development and technology investment initiatives. Market data collection utilizes both quantitative and qualitative research techniques to capture comprehensive market insights and trends.

Industry expert consultations provide valuable perspectives on market dynamics, competitive landscape, and future development trends affecting the data center rack market. Stakeholder surveys gather detailed information about purchasing decisions, technology preferences, and investment planning across various market segments.

Data validation processes ensure research accuracy through cross-referencing multiple sources, expert review, and statistical analysis of collected information. Market modeling techniques incorporate various economic and industry factors to develop reliable growth projections and market forecasts.

Continuous monitoring of market developments, policy changes, and technology trends ensures research findings remain current and relevant for strategic decision-making by industry participants and investors.

Riyadh region dominates the Saudi Arabia data center rack market, accounting for approximately 45% of total market demand, driven by its status as the political and economic center housing major government agencies, financial institutions, and corporate headquarters. Infrastructure concentration in the capital region creates substantial opportunities for rack suppliers serving both public and private sector clients.

Eastern Province represents the second-largest market segment with approximately 25% market share, supported by significant industrial activity, oil and gas operations, and growing technology sector investments. Dammam and Al Khobar serve as key commercial centers driving demand for enterprise data center infrastructure and rack systems.

Western Region, including Jeddah and Mecca, accounts for roughly 20% of market demand, benefiting from commercial activity, religious tourism infrastructure, and growing technology sector presence. Red Sea development projects and expanding logistics operations contribute to increasing data center infrastructure requirements.

Northern and Southern regions collectively represent approximately 10% of market demand, with growing potential driven by NEOM development, industrial diversification initiatives, and expanding telecommunications infrastructure. Regional development programs continue creating new opportunities for data center infrastructure investments.

According to MarkWide Research, regional market distribution is expected to become more balanced as government initiatives promote economic diversification and technology infrastructure development across all regions of the Kingdom.

The competitive landscape in the Saudi Arabia data center rack market features a diverse mix of international manufacturers, regional distributors, and emerging local suppliers competing across various market segments and price points.

Market competition intensifies through product innovation, pricing strategies, and service differentiation as suppliers seek to establish strong positions in the growing Saudi market. Local partnerships and distribution agreements play crucial roles in market access and customer relationship development.

By Rack Type:

By Application:

By End-User Industry:

Open frame racks represent the largest market segment, accounting for approximately 40% of total demand, driven by their cost-effectiveness and versatility across various applications. These systems provide excellent airflow management and easy equipment access, making them ideal for enterprise data centers and colocation facilities with standardized equipment configurations.

Enclosed server cabinets demonstrate strong growth momentum with approximately 35% market share, driven by increasing security requirements and environmental control needs. Advanced features including integrated cooling, power distribution, and monitoring systems make these solutions attractive for high-density computing applications and sensitive equipment protection.

Wall-mount racks serve specialized market segments with roughly 15% market share, primarily supporting edge computing deployments, small office installations, and distributed network infrastructure. Compact designs and space-saving configurations make these solutions ideal for locations with limited floor space and specific mounting requirements.

Portable and specialty racks account for the remaining 10% of market demand, serving niche applications including temporary installations, mobile data centers, and specialized equipment housing. Innovation focus in this segment emphasizes modularity, rapid deployment capabilities, and ruggedized construction for challenging environments.

Market trends indicate growing demand for integrated solutions combining rack systems with power distribution, cooling, and monitoring capabilities, reflecting customer preferences for comprehensive infrastructure packages rather than individual components.

Data center operators benefit from standardized rack systems that improve equipment organization, enhance cooling efficiency, and simplify maintenance procedures. Operational advantages include reduced installation time, improved cable management, and enhanced equipment accessibility for routine maintenance and upgrades.

IT infrastructure managers gain significant value through improved space utilization, better equipment protection, and enhanced monitoring capabilities. Management benefits include simplified inventory tracking, standardized configurations, and reduced complexity in equipment deployment and maintenance procedures.

Equipment manufacturers benefit from standardized mounting interfaces and consistent installation procedures that reduce product development costs and improve customer satisfaction. Design advantages include predictable thermal environments, reliable power distribution, and consistent mechanical interfaces across different installations.

System integrators realize improved project efficiency through standardized rack configurations, pre-configured accessories, and established installation procedures. Business benefits include reduced project risk, faster deployment schedules, and enhanced customer satisfaction through reliable infrastructure solutions.

End-user organizations achieve better total cost of ownership through improved equipment reliability, reduced maintenance requirements, and enhanced scalability for future expansion. Strategic advantages include improved business continuity, reduced operational complexity, and enhanced ability to adapt to changing technology requirements.

Strengths:

Weaknesses:

Opportunities:

Threats:

Hyperscale infrastructure adoption represents a dominant trend driving demand for standardized, high-density rack configurations optimized for cloud computing workloads. Major cloud providers establishing regional presence require consistent rack specifications and scalable deployment capabilities to support their global infrastructure standards.

Edge computing proliferation creates new market segments for compact, ruggedized rack solutions designed for distributed deployment scenarios. 5G network expansion and IoT applications drive demand for edge data center infrastructure supporting low-latency computing requirements across various industry verticals.

Sustainability integration becomes increasingly important as organizations focus on environmental responsibility and energy efficiency. Green data center initiatives drive demand for energy-efficient rack designs, integrated cooling solutions, and environmentally friendly materials that reduce overall facility environmental impact.

Modular design approaches gain popularity as organizations seek flexible infrastructure solutions that can adapt to changing requirements and technology evolution. Scalable architectures enable incremental capacity expansion and technology upgrades without major infrastructure overhauls.

Intelligent monitoring integration becomes standard as operators require real-time visibility into equipment performance, environmental conditions, and security status. IoT-enabled racks provide comprehensive monitoring capabilities supporting predictive maintenance and operational optimization.

Government initiatives continue driving market development through substantial investments in digital infrastructure and smart city projects. National Data Management Office establishment provides strategic direction for data center infrastructure development and regulatory framework evolution.

International partnerships between Saudi organizations and global technology providers create opportunities for knowledge transfer, local manufacturing development, and advanced technology deployment. Strategic alliances facilitate market entry for international suppliers while supporting local capability development.

Technology localization programs encourage domestic manufacturing and assembly capabilities for data center infrastructure components. Industrial development initiatives provide incentives for establishing local production facilities and technical expertise development.

Regulatory framework evolution includes updated standards for data center infrastructure, environmental compliance, and security requirements. Policy developments create clearer guidelines for infrastructure investment and operational requirements across various industry sectors.

Skills development programs address technical expertise shortages through training initiatives, certification programs, and educational partnerships. Workforce development efforts support market growth by ensuring adequate technical capabilities for infrastructure deployment and maintenance.

Market entry strategies should prioritize local partnership development and understanding of Saudi-specific requirements for successful market penetration. International suppliers benefit from establishing regional presence and developing relationships with local distributors and system integrators to effectively serve market demands.

Product development focus should emphasize energy efficiency, modular design, and integration capabilities that align with Saudi Arabia’s sustainability goals and infrastructure requirements. Innovation priorities include cooling integration, intelligent monitoring, and scalable architectures supporting diverse deployment scenarios.

Investment timing appears favorable given strong government support, increasing private sector demand, and expanding international presence in the Kingdom. MWR analysis suggests optimal market entry windows align with major infrastructure project timelines and government spending cycles.

Competitive differentiation requires focus on service capabilities, local support, and customization options rather than competing solely on price. Value proposition development should emphasize total cost of ownership, reliability, and long-term partnership potential with Saudi customers.

Supply chain optimization becomes critical for managing costs and ensuring reliable delivery schedules. Local sourcing and manufacturing capabilities provide competitive advantages while supporting government objectives for economic diversification and local content development.

Long-term market prospects remain highly positive, supported by sustained government investment in digital infrastructure and continued private sector digitalization initiatives. Growth trajectory is expected to accelerate as Vision 2030 projects advance and international technology companies expand their regional presence.

Technology evolution will continue driving market development through higher-density computing requirements, edge computing expansion, and advanced cooling integration needs. Innovation cycles in computing architecture and data center design will create ongoing opportunities for rack system suppliers offering advanced solutions.

Market maturation is anticipated to bring increased standardization, improved local manufacturing capabilities, and enhanced service ecosystems supporting comprehensive infrastructure solutions. Industry consolidation may occur as successful suppliers expand their market presence and capabilities.

Regional expansion potential positions Saudi Arabia as a strategic base for serving broader Middle East and North Africa markets. Export opportunities may develop as local manufacturing capabilities mature and regional demand for data center infrastructure continues growing.

MarkWide Research projections indicate sustained market growth with increasing emphasis on sustainability, efficiency, and intelligent infrastructure solutions that support Saudi Arabia’s transformation into a regional technology and innovation hub.

The Saudi Arabia data center rack market presents exceptional opportunities driven by the Kingdom’s ambitious digital transformation agenda, substantial government investments, and growing private sector demand for advanced IT infrastructure. Market fundamentals remain strong, supported by Vision 2030 initiatives, international technology investments, and expanding telecommunications infrastructure requirements.

Strategic positioning as a regional technology hub continues attracting global data center operators and cloud service providers, creating sustained demand for standardized rack solutions and comprehensive infrastructure support. Government policies favoring local manufacturing development and technology transfer provide additional growth catalysts for market participants.

Future success in this market requires understanding of local requirements, commitment to service excellence, and ability to provide integrated solutions supporting diverse customer needs across various industry sectors. The Saudi Arabia data center rack market represents a critical component of the Kingdom’s technology infrastructure development and offers substantial opportunities for suppliers capable of delivering innovative, efficient, and reliable solutions supporting the nation’s digital transformation objectives.

What is Data Center Rack?

Data Center Rack refers to a standardized frame or enclosure that houses servers, networking equipment, and other hardware in a data center environment. These racks are designed to optimize space, improve cooling efficiency, and facilitate organization within data centers.

What are the key players in the Saudi Arabia Data Center Rack Market?

Key players in the Saudi Arabia Data Center Rack Market include companies like Schneider Electric, Dell Technologies, and Huawei Technologies, which provide a range of data center solutions and infrastructure. These companies focus on innovation and efficiency in data center design and management, among others.

What are the growth factors driving the Saudi Arabia Data Center Rack Market?

The growth of the Saudi Arabia Data Center Rack Market is driven by the increasing demand for cloud computing, the rise of big data analytics, and the expansion of IT infrastructure across various sectors. Additionally, the government’s initiatives to promote digital transformation contribute to market growth.

What challenges does the Saudi Arabia Data Center Rack Market face?

Challenges in the Saudi Arabia Data Center Rack Market include high energy consumption, the need for advanced cooling solutions, and the rapid pace of technological change. These factors can complicate the management and operation of data centers, impacting overall efficiency.

What opportunities exist in the Saudi Arabia Data Center Rack Market?

Opportunities in the Saudi Arabia Data Center Rack Market include the growing adoption of edge computing, the increasing focus on sustainability, and the potential for smart data center technologies. These trends can lead to innovative solutions and improved operational efficiencies.

What trends are shaping the Saudi Arabia Data Center Rack Market?

Trends shaping the Saudi Arabia Data Center Rack Market include the integration of AI and machine learning for data center management, the shift towards modular data center designs, and the emphasis on energy-efficient solutions. These trends are influencing how data centers are built and operated.

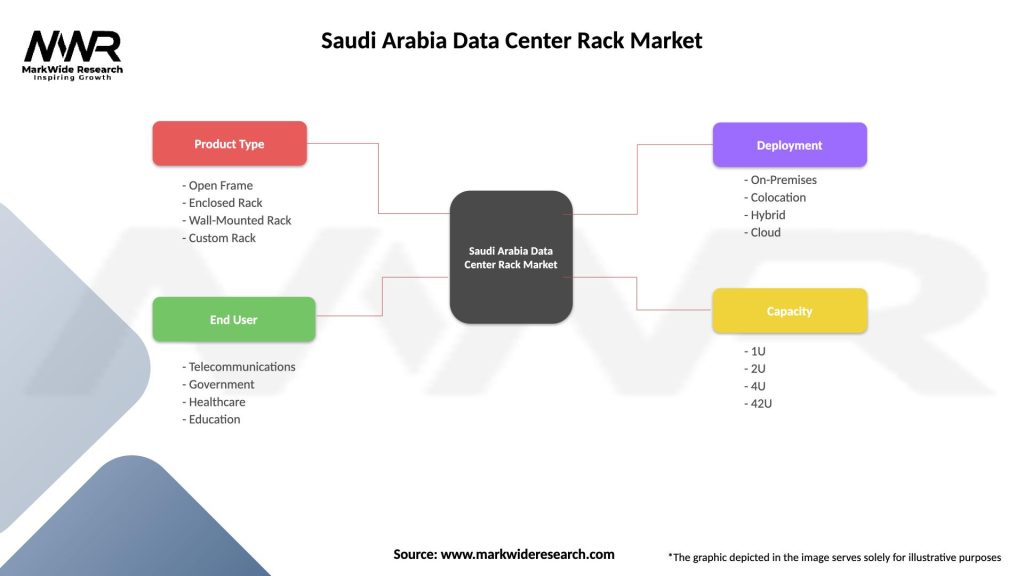

Saudi Arabia Data Center Rack Market

| Segmentation Details | Description |

|---|---|

| Product Type | Open Frame, Enclosed Rack, Wall-Mounted Rack, Custom Rack |

| End User | Telecommunications, Government, Healthcare, Education |

| Deployment | On-Premises, Colocation, Hybrid, Cloud |

| Capacity | 1U, 2U, 4U, 42U |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Saudi Arabia Data Center Rack Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.