444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Taiwan data center rack market represents a critical component of the island nation’s rapidly expanding digital infrastructure ecosystem. As Taiwan continues to strengthen its position as a global technology hub, the demand for sophisticated data center solutions has experienced unprecedented growth. The market encompasses various rack configurations, including open frame racks, enclosed server racks, wall-mounted racks, and specialized cooling-integrated systems designed to support high-density computing environments.

Taiwan’s strategic location in the Asia-Pacific region, combined with its advanced manufacturing capabilities and robust telecommunications infrastructure, has positioned the country as a preferred destination for hyperscale data centers and edge computing facilities. The market is experiencing substantial growth driven by increasing cloud adoption, digital transformation initiatives, and the proliferation of IoT devices across various industries. Current market dynamics indicate a compound annual growth rate of 8.2% through the forecast period, reflecting the strong demand for reliable and efficient data center infrastructure.

Government initiatives supporting digital economy development and foreign investment in technology infrastructure have further accelerated market expansion. The Taiwan data center rack market benefits from the country’s stable political environment, reliable power supply, and proximity to major Asian markets, making it an attractive location for international technology companies seeking to establish regional data center operations.

The Taiwan data center rack market refers to the comprehensive ecosystem of physical infrastructure solutions designed to house, organize, and support IT equipment within data center facilities across Taiwan. These specialized mounting systems provide the structural foundation for servers, networking equipment, storage devices, and power distribution units while ensuring optimal airflow management and accessibility for maintenance operations.

Data center racks in Taiwan’s market context encompass a wide range of standardized and customized solutions, including 19-inch server racks, 23-inch telecommunications racks, open frame configurations, and enclosed cabinets with integrated cooling and power management systems. The market includes both domestic manufacturing and international sourcing of rack solutions to meet the diverse requirements of local enterprises, cloud service providers, and multinational corporations operating in Taiwan.

Market participants include rack manufacturers, system integrators, data center operators, and end-users across various sectors such as telecommunications, financial services, government, healthcare, and manufacturing. The Taiwan data center rack market serves as a crucial enabler of the country’s digital transformation journey and its ambitions to become a regional technology leader.

Taiwan’s data center rack market is experiencing robust growth fueled by accelerating digitalization trends and increasing demand for cloud-based services. The market landscape is characterized by strong competition among international and domestic players, with emphasis on innovation, energy efficiency, and scalability. Key growth drivers include the expansion of hyperscale data centers, edge computing deployments, and government support for digital infrastructure development.

Market segmentation reveals diverse applications across enterprise data centers, colocation facilities, and cloud service provider installations. The telecommunications sector represents the largest end-user segment, accounting for approximately 35% of total market demand, followed by financial services and government sectors. Geographically, the Taipei metropolitan area dominates market activity, though significant growth is observed in Taichung and Kaohsiung regions.

Technological advancements in rack design, including improved cooling efficiency, higher power density support, and modular configurations, are driving market evolution. The integration of smart monitoring systems and IoT-enabled rack management solutions is becoming increasingly important for operators seeking to optimize data center performance and reduce operational costs.

Future market prospects remain highly positive, with projected growth driven by 5G network deployments, artificial intelligence applications, and increasing data generation from connected devices. The market is expected to benefit from Taiwan’s strategic position in global supply chains and its commitment to sustainable technology development.

Strategic market analysis reveals several critical insights shaping the Taiwan data center rack market landscape:

Digital transformation initiatives across Taiwan’s economy serve as the primary catalyst for data center rack market growth. Organizations are increasingly migrating to cloud-based infrastructures, requiring substantial expansion of data center capacity and corresponding rack installations. The acceleration of digital services adoption, particularly following the global pandemic, has created sustained demand for reliable and scalable data center solutions.

Government policy support plays a crucial role in market expansion through initiatives such as the Digital Nation and Innovative Economic Development Program. These policies encourage foreign investment in technology infrastructure while promoting domestic innovation in data center technologies. Regulatory frameworks supporting data localization and cybersecurity requirements are driving demand for local data center facilities equipped with advanced rack systems.

5G network deployment represents a significant growth driver, requiring extensive edge computing infrastructure to support low-latency applications. Telecommunications operators are investing heavily in distributed data center networks, creating substantial demand for compact and efficient rack solutions. The rollout of 5G services is expected to generate approximately 25% additional rack demand over the next three years.

Artificial intelligence and machine learning applications are driving requirements for high-performance computing infrastructure, necessitating specialized rack configurations capable of supporting GPU-intensive workloads. The growing adoption of AI across industries is creating demand for racks with enhanced cooling capabilities and higher power density support.

High initial capital requirements present significant barriers for smaller organizations seeking to establish or expand data center operations. The substantial investment needed for quality rack infrastructure, including associated cooling and power systems, can limit market participation and slow adoption rates among cost-sensitive segments.

Space constraints in Taiwan’s densely populated urban areas create challenges for data center development and expansion. Limited availability of suitable real estate for large-scale data center facilities constrains market growth and increases operational costs. Land scarcity particularly affects the Taipei metropolitan area, where demand for data center services is highest.

Skilled workforce shortages in data center design, installation, and maintenance create operational challenges and increase project timelines. The specialized nature of modern data center rack systems requires technical expertise that may be limited in the local market, potentially constraining growth rates and increasing implementation costs.

Environmental regulations and sustainability requirements are becoming increasingly stringent, requiring investments in energy-efficient cooling systems and environmentally friendly materials. Compliance with evolving environmental standards may increase costs and complexity for rack manufacturers and data center operators.

Supply chain vulnerabilities exposed during recent global disruptions have highlighted dependencies on international component suppliers. Potential disruptions to critical component availability could impact project timelines and increase costs for data center rack deployments.

Edge computing expansion presents substantial opportunities for innovative rack solutions designed for distributed computing environments. The growing need for low-latency processing capabilities is driving demand for compact, efficient rack systems suitable for deployment in non-traditional data center locations such as retail stores, manufacturing facilities, and telecommunications infrastructure.

Green data center initiatives are creating opportunities for manufacturers developing energy-efficient and sustainable rack solutions. Organizations seeking to reduce their environmental footprint are increasingly prioritizing racks with advanced cooling technologies, renewable energy integration capabilities, and recyclable materials. This trend is expected to drive 40% of new rack purchases toward environmentally optimized solutions.

Smart rack technologies incorporating IoT sensors, automated monitoring, and predictive maintenance capabilities represent emerging opportunities. These intelligent systems can optimize power usage, monitor environmental conditions, and predict equipment failures, providing significant value to data center operators seeking to improve efficiency and reduce operational costs.

Regional expansion beyond traditional metropolitan areas offers growth opportunities as businesses and government agencies in secondary cities invest in local data center infrastructure. The development of regional data centers creates demand for rack solutions tailored to smaller-scale deployments while maintaining enterprise-grade reliability and performance.

Industry-specific solutions present opportunities for specialized rack configurations designed for unique sector requirements. Healthcare, financial services, and manufacturing industries have specific compliance, security, and performance needs that can be addressed through customized rack solutions.

Competitive dynamics in the Taiwan data center rack market are characterized by intense rivalry among international and domestic players. Global manufacturers leverage advanced technologies and economies of scale, while local companies compete on customization capabilities, rapid response times, and deep understanding of regional requirements. This competition drives continuous innovation and competitive pricing strategies.

Technology evolution is rapidly transforming market dynamics through the introduction of higher-density configurations, improved cooling efficiency, and intelligent management systems. Rack manufacturers are investing heavily in research and development to address evolving customer needs for greater computing density, energy efficiency, and operational simplicity. According to MarkWide Research analysis, technology innovation cycles are accelerating, with new product introductions occurring at 18-month intervals.

Customer requirements are becoming increasingly sophisticated, with emphasis on total cost of ownership, scalability, and future-proofing capabilities. Data center operators are seeking rack solutions that can adapt to changing technology requirements while maintaining optimal performance and efficiency. This trend is driving demand for modular and flexible rack architectures.

Supply chain dynamics are evolving as manufacturers seek to balance cost efficiency with supply security. The trend toward regional supply chain diversification is creating opportunities for local component suppliers and assembly operations while reducing dependence on single-source suppliers.

Primary research methodology employed comprehensive interviews with key market participants including rack manufacturers, data center operators, system integrators, and end-users across various industry sectors. Structured questionnaires were designed to gather insights on market trends, technology preferences, purchasing criteria, and future requirements. Face-to-face interviews and virtual consultations were conducted with over 150 industry professionals to ensure representative market coverage.

Secondary research involved extensive analysis of industry reports, company financial statements, government publications, and trade association data. Market sizing and forecasting models were developed using historical data analysis, trend extrapolation, and comparative market studies. Regulatory filings, patent databases, and technical specifications were reviewed to understand technology trends and competitive positioning.

Data validation processes included cross-referencing multiple sources, conducting follow-up interviews for clarification, and employing statistical analysis techniques to ensure data accuracy and reliability. Market estimates were validated through triangulation methods comparing primary research findings with secondary data sources and expert opinions.

Analytical framework incorporated both quantitative and qualitative research methodologies to provide comprehensive market insights. Statistical modeling techniques were used for market sizing and forecasting, while qualitative analysis provided context for market dynamics, competitive landscape, and future trends. The research methodology ensured robust and actionable insights for market participants.

Northern Taiwan dominates the data center rack market, accounting for approximately 55% of total demand, driven by the concentration of technology companies, financial institutions, and government agencies in the Taipei metropolitan area. The region benefits from excellent telecommunications infrastructure, reliable power supply, and proximity to international submarine cable landing points. Major hyperscale data centers and colocation facilities in this region drive significant rack demand.

Central Taiwan represents a growing market segment, with Taichung emerging as an important secondary data center hub. The region’s strategic location, lower real estate costs, and government incentives for technology investments are attracting data center developments. Manufacturing companies in the region are also investing in private data center facilities, contributing to steady rack demand growth of approximately 12% annually.

Southern Taiwan is experiencing increased data center activity, particularly in Kaohsiung, driven by port logistics, petrochemical industries, and emerging technology sectors. The region’s development as a smart city initiative is creating demand for edge computing infrastructure and corresponding rack solutions. Government support for regional development is encouraging data center investments in this area.

Eastern Taiwan represents a smaller but emerging market segment, with opportunities related to disaster recovery facilities and regional government data centers. The region’s natural advantages for cooling and renewable energy integration are attracting interest from environmentally conscious data center operators seeking sustainable infrastructure solutions.

Market leadership is distributed among several key players, each bringing distinct competitive advantages to the Taiwan data center rack market:

Competitive strategies focus on technological innovation, local partnerships, and customization capabilities. International players leverage global expertise and economies of scale, while regional companies compete on responsiveness, local support, and specialized solutions for specific market segments.

By Rack Type:

By End-User Industry:

By Deployment Type:

Enterprise Segment demonstrates strong preference for enclosed rack solutions with integrated security features and environmental monitoring capabilities. Organizations prioritize reliability, scalability, and compliance with industry standards. The segment shows increasing adoption of intelligent rack management systems for improved operational efficiency, with approximately 60% of enterprises planning smart rack upgrades within the next two years.

Telecommunications Sector requires specialized rack configurations designed for network equipment with unique form factors and cooling requirements. The segment is experiencing rapid growth due to 5G deployment, with emphasis on compact, high-density solutions suitable for cell tower installations and central office environments. Telecommunications racks typically feature enhanced cable management and rapid deployment capabilities.

Hyperscale Segment focuses on cost-effective, standardized rack solutions optimized for massive scale deployments. Open frame racks dominate this category due to superior cooling efficiency and cost advantages. Hyperscale operators prioritize automation-friendly designs and rapid deployment capabilities to support their aggressive expansion timelines.

Edge Computing Category represents the fastest-growing segment, requiring compact, ruggedized rack solutions suitable for deployment in non-traditional data center environments. These applications demand racks with enhanced environmental protection, remote monitoring capabilities, and simplified maintenance procedures. The segment is expected to achieve growth rates exceeding 15% annually.

Data Center Operators benefit from improved operational efficiency through advanced rack designs that optimize airflow management, reduce cooling costs, and simplify maintenance procedures. Modern rack solutions enable higher equipment density while maintaining optimal operating conditions, resulting in improved space utilization and reduced operational expenses. Intelligent monitoring capabilities provide real-time visibility into environmental conditions and equipment status.

IT Equipment Manufacturers gain from standardized rack interfaces that ensure compatibility across diverse data center environments. Rack standardization reduces design complexity and enables economies of scale in equipment production. Collaboration with rack manufacturers facilitates optimization of cooling and power delivery for specific equipment configurations.

System Integrators benefit from comprehensive rack solutions that simplify project implementation and reduce installation complexity. Pre-configured rack systems with integrated power and cooling components accelerate deployment timelines and reduce integration risks. Standardized designs enable more predictable project outcomes and improved profitability.

End-User Organizations realize significant benefits through improved IT infrastructure reliability, reduced operational costs, and enhanced scalability. Modern rack solutions provide better protection for critical IT equipment while enabling more efficient space utilization. Energy-efficient designs contribute to reduced power consumption and lower environmental impact.

Government Agencies benefit from enhanced cybersecurity through secure rack designs and improved disaster recovery capabilities. Standardized solutions facilitate procurement processes and ensure compliance with government regulations and standards.

Strengths:

Weaknesses:

Opportunities:

Threats:

Hyperconverged Infrastructure adoption is driving demand for rack solutions optimized for software-defined data centers. Organizations are seeking racks that can accommodate diverse hardware configurations while providing flexibility for future technology evolution. This trend is influencing rack design toward more modular and adaptable architectures.

Liquid Cooling Integration is becoming increasingly important as computing densities continue to increase. Rack manufacturers are developing solutions that seamlessly integrate liquid cooling systems to address thermal management challenges in high-performance computing environments. Approximately 30% of new hyperscale installations are incorporating some form of liquid cooling technology.

Micro Data Centers represent an emerging trend driven by edge computing requirements and space constraints. These compact, self-contained solutions combine racks, cooling, power, and monitoring systems in standardized configurations suitable for deployment in diverse environments. The micro data center segment is experiencing rapid growth in retail, healthcare, and industrial applications.

Sustainability Focus is driving innovation in rack materials, manufacturing processes, and end-of-life recycling programs. Manufacturers are developing racks using recycled materials and implementing circular economy principles. Energy efficiency improvements in rack design are contributing to overall data center sustainability goals.

Artificial Intelligence Integration is enabling predictive maintenance, automated optimization, and intelligent capacity planning in rack management systems. AI-powered analytics provide insights into equipment performance, environmental conditions, and potential failure modes, enabling proactive maintenance strategies.

Major Infrastructure Investments by international cloud service providers are transforming the Taiwan data center landscape. Recent announcements of significant data center investments by global technology companies are driving substantial demand for rack infrastructure and associated systems. These investments are expected to increase rack demand by approximately 45% over the next three years.

5G Network Rollout by major telecommunications operators is creating unprecedented demand for edge computing infrastructure and specialized rack solutions. The deployment of thousands of small cell sites and edge data centers requires compact, ruggedized rack systems designed for distributed deployment scenarios.

Government Digital Transformation initiatives are driving public sector investments in data center infrastructure. Smart city projects, digital government services, and cybersecurity enhancements are creating steady demand for secure, compliant rack solutions designed for government applications.

Manufacturing Sector Digitalization is generating demand for industrial-grade rack solutions suitable for harsh manufacturing environments. Industry 4.0 initiatives and IoT implementations require robust data center infrastructure capable of supporting real-time analytics and automated control systems.

Sustainability Regulations are influencing rack design and selection criteria, with increasing emphasis on energy efficiency, recyclable materials, and environmental impact reduction. New environmental standards are driving innovation in cooling efficiency and power management systems.

Market participants should focus on developing comprehensive solutions that address the evolving needs of Taiwan’s diverse data center market. MWR analysis suggests that success requires balancing standardization for cost efficiency with customization capabilities for specific market segments. Companies should invest in local partnerships and support capabilities to compete effectively against established international players.

Technology innovation should prioritize energy efficiency, intelligent monitoring, and modular design principles. The integration of IoT sensors, predictive analytics, and automated management systems will become increasingly important for competitive differentiation. Manufacturers should also focus on developing solutions that support both traditional data center applications and emerging edge computing requirements.

Supply chain resilience requires diversification of component sources and development of local supplier relationships. Companies should evaluate opportunities for regional manufacturing and assembly operations to reduce dependency on international supply chains while improving responsiveness to local market needs.

Sustainability initiatives should be integrated into product development and marketing strategies. Organizations that can demonstrate measurable environmental benefits through improved energy efficiency and sustainable materials will gain competitive advantages as environmental consciousness increases among customers.

Market expansion strategies should consider opportunities in secondary cities and emerging application areas such as edge computing, industrial IoT, and smart city infrastructure. Developing specialized solutions for these segments can provide growth opportunities beyond traditional enterprise data center markets.

Long-term market prospects for Taiwan’s data center rack market remain highly positive, driven by continued digital transformation, 5G deployment, and the country’s strategic position in the global technology ecosystem. The market is expected to benefit from Taiwan’s commitment to becoming a regional technology hub and its investments in advanced manufacturing capabilities.

Technology evolution will continue to drive market growth through the introduction of higher-density configurations, improved cooling efficiency, and intelligent management systems. The integration of artificial intelligence and machine learning capabilities into rack management systems will enable new levels of operational optimization and predictive maintenance.

Edge computing expansion represents the most significant growth opportunity, with distributed computing requirements driving demand for innovative rack solutions designed for non-traditional data center environments. This trend is expected to account for approximately 25% of total market growth over the next five years.

Sustainability requirements will increasingly influence purchasing decisions, with organizations prioritizing energy-efficient and environmentally responsible solutions. Manufacturers that can demonstrate measurable environmental benefits will gain competitive advantages in an increasingly environmentally conscious market.

Regional market development beyond the Taipei metropolitan area will create new opportunities for growth and market expansion. Government initiatives supporting regional development and smart city projects will drive demand for data center infrastructure in secondary markets throughout Taiwan.

The Taiwan data center rack market stands at the forefront of the Asia-Pacific region’s digital infrastructure evolution, driven by robust demand from diverse industry sectors and supported by favorable government policies. The market’s strong fundamentals, including Taiwan’s strategic location, advanced manufacturing capabilities, and stable infrastructure, position it for continued growth and expansion.

Key success factors for market participants include technological innovation, local market understanding, and the ability to provide comprehensive solutions addressing diverse customer requirements. The integration of intelligent monitoring systems, energy-efficient designs, and modular architectures will be critical for maintaining competitive advantages in an increasingly sophisticated market.

Future growth prospects remain highly attractive, with emerging opportunities in edge computing, 5G infrastructure, and sustainable technology solutions. Organizations that can effectively balance standardization with customization while maintaining focus on innovation and customer service will be best positioned to capitalize on the market’s continued expansion and evolution.

What is Data Center Rack?

Data Center Rack refers to a standardized frame or enclosure used to house servers, networking equipment, and other hardware in a data center environment. These racks are designed to optimize space, improve cooling efficiency, and facilitate organization within data centers.

What are the key players in the Taiwan Data Center Rack Market?

Key players in the Taiwan Data Center Rack Market include companies like Schneider Electric, Vertiv, and Rittal, which provide a range of solutions for data center infrastructure. These companies focus on innovation and efficiency in their product offerings, among others.

What are the growth factors driving the Taiwan Data Center Rack Market?

The Taiwan Data Center Rack Market is driven by the increasing demand for cloud computing services, the rise of big data analytics, and the need for efficient data storage solutions. Additionally, the expansion of IT infrastructure in various sectors contributes to market growth.

What challenges does the Taiwan Data Center Rack Market face?

Challenges in the Taiwan Data Center Rack Market include the high costs associated with advanced rack systems and the complexity of integrating new technologies into existing infrastructures. Additionally, the rapid pace of technological change can make it difficult for companies to keep up.

What opportunities exist in the Taiwan Data Center Rack Market?

Opportunities in the Taiwan Data Center Rack Market include the growing trend of edge computing and the increasing focus on energy-efficient solutions. As businesses seek to optimize their data management, innovative rack designs and smart technologies are likely to gain traction.

What trends are shaping the Taiwan Data Center Rack Market?

Trends in the Taiwan Data Center Rack Market include the adoption of modular rack systems and the integration of IoT technologies for better monitoring and management. Additionally, sustainability initiatives are prompting companies to develop eco-friendly rack solutions.

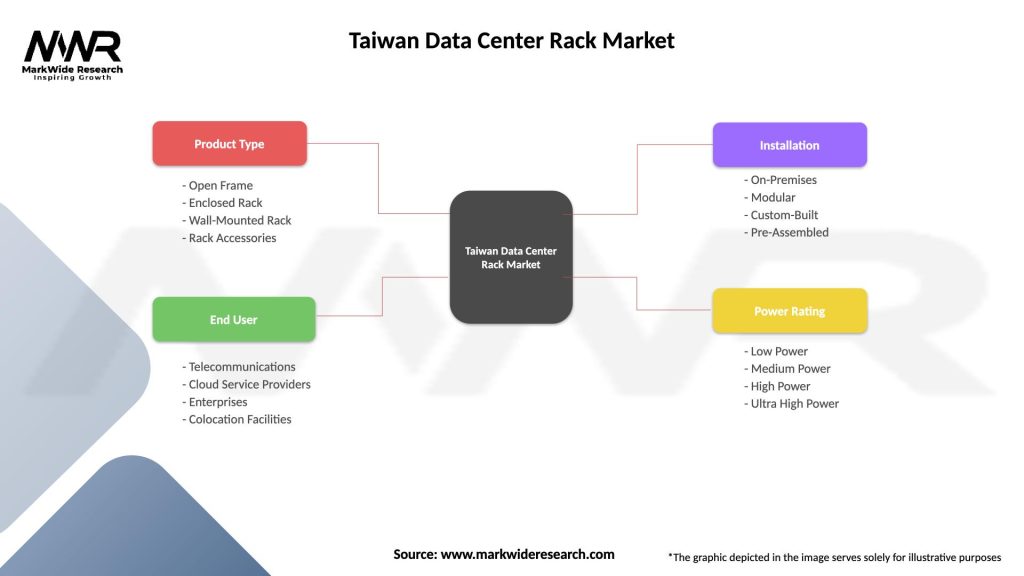

Taiwan Data Center Rack Market

| Segmentation Details | Description |

|---|---|

| Product Type | Open Frame, Enclosed Rack, Wall-Mounted Rack, Rack Accessories |

| End User | Telecommunications, Cloud Service Providers, Enterprises, Colocation Facilities |

| Installation | On-Premises, Modular, Custom-Built, Pre-Assembled |

| Power Rating | Low Power, Medium Power, High Power, Ultra High Power |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Taiwan Data Center Rack Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.