444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Mexico cold chain logistics market represents a rapidly expanding sector driven by increasing demand for temperature-controlled transportation and storage solutions across various industries. Mexico’s strategic location as a bridge between North and South America, combined with its growing agricultural exports and pharmaceutical manufacturing capabilities, has positioned the country as a critical hub for cold chain operations in Latin America.

Market dynamics indicate robust growth potential, with the sector experiencing a compound annual growth rate (CAGR) of 8.2% over the forecast period. This expansion is primarily fueled by rising consumer awareness regarding food safety, stringent regulatory requirements for pharmaceutical products, and the increasing penetration of organized retail chains across Mexico. Temperature-sensitive goods including fresh produce, dairy products, frozen foods, vaccines, and biotechnology products require sophisticated cold chain infrastructure to maintain product integrity throughout the supply chain.

Infrastructure development across Mexico has significantly enhanced the cold chain logistics landscape, with major investments in refrigerated warehouses, cold storage facilities, and temperature-controlled transportation fleets. The market encompasses various stakeholders including logistics service providers, cold storage operators, transportation companies, and technology solution providers who collectively ensure the seamless movement of temperature-sensitive products from origin to destination.

The Mexico cold chain logistics market refers to the comprehensive network of temperature-controlled supply chain services that maintain specific temperature ranges for perishable and temperature-sensitive products throughout storage, handling, and transportation processes within Mexico’s borders and international trade corridors.

Cold chain logistics encompasses multiple integrated components working in harmony to preserve product quality and safety. These components include refrigerated storage facilities, temperature-controlled transportation vehicles, monitoring and tracking systems, packaging solutions, and specialized handling equipment. The market serves diverse industries including agriculture, food and beverage, pharmaceuticals, chemicals, and biotechnology sectors.

Temperature management throughout the cold chain is critical for maintaining product efficacy, extending shelf life, and ensuring compliance with regulatory standards. The market involves sophisticated logistics operations that require precise temperature control, real-time monitoring, and rapid response capabilities to address any temperature excursions that could compromise product integrity.

Mexico’s cold chain logistics sector demonstrates exceptional growth momentum driven by expanding agricultural exports, pharmaceutical manufacturing growth, and increasing consumer demand for fresh and frozen products. The market benefits from Mexico’s advantageous geographic position, enabling efficient distribution to both domestic and international markets while serving as a strategic logistics hub for North American trade.

Key growth drivers include the rapid expansion of modern retail formats, increasing health consciousness among consumers, and stringent food safety regulations. The pharmaceutical segment particularly shows strong growth potential, with biotechnology products accounting for 23% of temperature-controlled shipments. Additionally, the fresh produce export sector continues to expand, with Mexico serving as a major supplier to the United States and Canadian markets.

Technology adoption plays a crucial role in market evolution, with advanced monitoring systems, IoT sensors, and blockchain technology enhancing supply chain visibility and traceability. These technological advancements enable real-time temperature monitoring, predictive analytics, and improved inventory management, resulting in reduced product losses and enhanced operational efficiency across the cold chain network.

Strategic market positioning reveals several critical insights that define Mexico’s cold chain logistics landscape:

Market penetration varies significantly across different regions, with northern border states and major metropolitan areas showing higher adoption rates of advanced cold chain solutions. The integration of traditional supply chains with modern cold chain infrastructure continues to present both opportunities and challenges for market participants.

Export growth serves as the primary catalyst for Mexico’s cold chain logistics expansion, with agricultural exports requiring sophisticated temperature-controlled transportation and storage solutions. Mexico’s position as a leading exporter of fresh produce, including avocados, berries, and vegetables, necessitates robust cold chain infrastructure to maintain product quality during international shipments.

Pharmaceutical manufacturing expansion significantly contributes to market growth, with Mexico emerging as a major production hub for generic drugs, vaccines, and biotechnology products. The pharmaceutical sector requires stringent temperature control throughout the supply chain, with temperature deviations potentially causing 35% of pharmaceutical product losses without proper cold chain management.

Consumer behavior changes drive increased demand for fresh and frozen products, with Mexican consumers showing growing preference for high-quality perishable goods. The expansion of modern retail formats, including supermarket chains and convenience stores, creates sustained demand for reliable cold chain logistics services to maintain product freshness and safety standards.

Regulatory requirements continue to strengthen across food safety and pharmaceutical sectors, mandating compliance with international standards for temperature-controlled logistics. These regulations drive investments in advanced monitoring systems, certified facilities, and trained personnel, ultimately expanding the addressable market for professional cold chain service providers.

Infrastructure limitations present significant challenges in certain regions of Mexico, where inadequate cold storage facilities and limited refrigerated transportation capacity constrain market growth. Rural areas particularly face connectivity issues and insufficient cold chain infrastructure, creating bottlenecks in the supply chain for agricultural products.

High operational costs associated with maintaining temperature-controlled environments throughout the supply chain pose financial challenges for smaller operators and emerging market participants. Energy costs for refrigeration systems, specialized equipment investments, and skilled workforce requirements create substantial barriers to entry for new players in the cold chain logistics market.

Technology adoption barriers include limited technical expertise and resistance to change among traditional logistics providers. The integration of advanced monitoring systems, IoT devices, and data analytics platforms requires significant training investments and operational adjustments that some companies find challenging to implement effectively.

Seasonal demand fluctuations create capacity utilization challenges, with peak agricultural seasons requiring substantial infrastructure that may remain underutilized during off-peak periods. This seasonality affects profitability and complicates long-term planning for cold chain logistics providers operating in Mexico’s agricultural corridors.

E-commerce expansion presents substantial growth opportunities for cold chain logistics providers, with online grocery shopping and direct-to-consumer pharmaceutical deliveries requiring sophisticated last-mile cold chain solutions. The growing preference for home delivery of fresh and frozen products creates new market segments for specialized cold chain services.

Cross-border trade opportunities continue expanding as Mexico strengthens trade relationships with various countries beyond North America. The USMCA agreement and other trade partnerships create favorable conditions for cold chain logistics providers to expand their international service offerings and capture growing export volumes.

Technology innovation opportunities include the development of more efficient refrigeration systems, advanced packaging solutions, and automated cold storage facilities. Companies investing in cutting-edge technologies can achieve competitive advantages through improved operational efficiency, reduced energy consumption, and enhanced service quality.

Market consolidation opportunities exist for well-capitalized logistics providers to acquire smaller operators and expand their geographic coverage and service capabilities. Strategic acquisitions can help companies achieve economies of scale, improve network density, and enhance their competitive positioning in key market segments.

Supply chain integration trends are reshaping Mexico’s cold chain logistics landscape, with companies seeking end-to-end solutions that encompass storage, transportation, and value-added services. This integration drives consolidation among service providers and creates opportunities for comprehensive logistics solutions that address multiple customer requirements within a single service framework.

Competitive pressures intensify as international logistics companies enter the Mexican market, bringing advanced technologies and operational expertise that raise industry standards. Local providers must adapt by investing in infrastructure upgrades, technology adoption, and workforce development to maintain their competitive positions against well-funded international competitors.

Customer expectations continue evolving toward greater transparency, reliability, and sustainability in cold chain operations. Shippers increasingly demand real-time visibility, temperature monitoring, and environmental responsibility from their logistics partners, driving service providers to enhance their capabilities and reporting systems.

Regulatory evolution influences market dynamics through changing compliance requirements and quality standards. According to MarkWide Research analysis, regulatory compliance costs represent approximately 12% of total operational expenses for cold chain logistics providers, highlighting the significant impact of regulatory requirements on market dynamics and competitive positioning.

Primary research methodologies employed in analyzing Mexico’s cold chain logistics market include comprehensive interviews with industry executives, logistics service providers, cold storage operators, and key customers across various sectors. These interviews provide valuable insights into market trends, operational challenges, and growth opportunities from multiple stakeholder perspectives.

Secondary research encompasses extensive analysis of industry reports, government statistics, trade association data, and company financial statements to establish market baselines and identify growth patterns. This research approach ensures comprehensive coverage of market dynamics and provides quantitative foundations for market analysis and projections.

Market validation processes involve cross-referencing multiple data sources and conducting follow-up interviews to verify key findings and ensure accuracy of market insights. The validation methodology includes consultation with industry experts and comparison of findings with established market benchmarks to maintain research integrity and reliability.

Data collection spans multiple geographic regions within Mexico, ensuring representative coverage of different market conditions and operational environments. The research methodology incorporates both quantitative metrics and qualitative assessments to provide a balanced perspective on market opportunities and challenges facing cold chain logistics providers.

Northern Mexico dominates the cold chain logistics market, accounting for approximately 42% of total market activity due to its proximity to the United States border and concentration of agricultural export operations. States including Sonora, Sinaloa, and Nuevo León host major cold storage facilities and serve as primary distribution hubs for cross-border trade in temperature-sensitive products.

Central Mexico represents a significant market segment centered around Mexico City and surrounding metropolitan areas, where large consumer populations drive demand for fresh and frozen products. The region benefits from established transportation networks and serves as a distribution hub for domestic market supply chains, with cold storage capacity growing at 15% annually to meet increasing demand.

Western Mexico shows strong growth potential driven by agricultural production in states like Jalisco and Michoacán, which are major producers of avocados, berries, and other export crops. The region’s Pacific coast ports provide strategic advantages for international shipments to Asian markets, creating opportunities for specialized cold chain logistics services.

Southern and Eastern Mexico present emerging opportunities as infrastructure development expands cold chain capabilities in previously underserved regions. These areas benefit from agricultural diversification and growing pharmaceutical manufacturing activities, though they currently represent smaller market shares compared to northern and central regions.

Market leadership in Mexico’s cold chain logistics sector is characterized by a mix of international logistics giants and specialized local providers, each bringing distinct competitive advantages and market positioning strategies.

Competitive strategies focus on technology differentiation, geographic expansion, and vertical integration to capture larger market shares and improve service offerings. Companies are investing heavily in automation, IoT monitoring systems, and sustainable refrigeration technologies to differentiate their services and improve operational efficiency.

By Temperature Range:

By Application:

By Service Type:

Fresh Produce Segment dominates Mexico’s cold chain logistics market, driven by the country’s position as a major agricultural exporter. This category requires sophisticated temperature and humidity control throughout the supply chain, with post-harvest losses reduced by 28% through proper cold chain management. The segment benefits from year-round production cycles and growing international demand for Mexican agricultural products.

Pharmaceutical Cold Chain represents the fastest-growing segment, with increasing domestic pharmaceutical manufacturing and growing demand for temperature-sensitive medications. This category requires the most stringent temperature control and monitoring, with regulatory compliance driving investments in advanced tracking systems and validated storage facilities.

Dairy and Frozen Foods segment shows steady growth supported by changing consumer preferences and expanding retail distribution networks. This category benefits from the growth of modern retail formats and increasing consumer awareness of food safety and quality standards.

Export-Oriented Services category focuses on cross-border transportation and storage services supporting Mexico’s international trade relationships. This segment requires specialized documentation, customs clearance capabilities, and compliance with international quality standards, creating opportunities for full-service logistics providers.

Logistics Service Providers benefit from expanding market opportunities driven by growing demand across multiple industry segments. The cold chain logistics market offers higher margins compared to ambient logistics services, with specialized expertise creating competitive barriers and customer loyalty. Technology investments enable service differentiation and operational efficiency improvements that enhance profitability.

Agricultural Producers gain access to broader markets and improved product quality through professional cold chain services. Proper temperature management extends shelf life, reduces post-harvest losses, and enables premium pricing for high-quality products. Cold chain logistics support enables Mexican agricultural producers to compete effectively in international markets.

Pharmaceutical Companies achieve regulatory compliance and product integrity through specialized cold chain services. Professional logistics providers offer validated storage and transportation solutions that ensure product efficacy and reduce regulatory risks. The cold chain infrastructure supports Mexico’s growing pharmaceutical manufacturing sector and enables efficient distribution of temperature-sensitive medications.

Retailers and Distributors benefit from reliable supply chains that ensure product availability and quality for their customers. Cold chain logistics enable retailers to expand their fresh and frozen product offerings while reducing inventory losses and improving customer satisfaction through consistent product quality.

Strengths:

Weaknesses:

Opportunities:

Threats:

Automation Integration emerges as a dominant trend, with cold chain logistics providers investing in automated storage and retrieval systems, robotic handling equipment, and AI-powered inventory management. These technologies improve operational efficiency, reduce labor costs, and enhance accuracy in temperature-controlled environments.

Sustainability Focus drives adoption of environmentally friendly refrigeration systems, energy-efficient facilities, and sustainable packaging solutions. Companies are implementing natural refrigerants, solar-powered cooling systems, and carbon footprint reduction programs to meet environmental regulations and customer expectations.

Real-time Monitoring becomes standard practice through IoT sensors, blockchain technology, and cloud-based tracking systems. These technologies provide end-to-end visibility, enable predictive maintenance, and support regulatory compliance through detailed temperature and handling records.

Last-mile Innovation addresses growing e-commerce demands through specialized delivery vehicles, neighborhood cold storage hubs, and flexible delivery options. MWR data indicates that last-mile cold chain services are growing at 22% annually, reflecting changing consumer purchasing patterns and delivery expectations.

Infrastructure Expansion projects include major cold storage facility developments in key agricultural and manufacturing regions. Recent investments exceed previous capacity additions, with new facilities incorporating advanced automation and energy-efficient technologies to serve growing market demand.

Technology Partnerships between logistics providers and technology companies accelerate innovation in monitoring systems, predictive analytics, and supply chain optimization. These collaborations enable faster deployment of advanced solutions and improve competitive positioning for participating companies.

Regulatory Updates strengthen food safety and pharmaceutical handling requirements, driving investments in compliance systems and validated processes. New regulations create opportunities for specialized service providers while raising barriers for non-compliant operators.

Strategic Acquisitions reshape the competitive landscape as larger logistics companies acquire specialized cold chain operators to expand their service capabilities and geographic coverage. These transactions accelerate market consolidation and create integrated service platforms.

Investment Priorities should focus on technology infrastructure, automation systems, and geographic expansion in high-growth regions. Companies should prioritize investments that improve operational efficiency, enhance service quality, and support scalable growth strategies.

Partnership Strategies can accelerate market penetration through collaborations with agricultural producers, pharmaceutical manufacturers, and retail chains. Strategic partnerships enable companies to secure long-term contracts and develop specialized service offerings for key market segments.

Technology Adoption recommendations include implementing comprehensive monitoring systems, automation technologies, and data analytics platforms. These investments improve operational efficiency, reduce costs, and enable service differentiation in competitive market conditions.

Market Entry Strategies for new participants should emphasize niche specialization, regional focus, and technology differentiation. Successful market entry requires understanding local market conditions, regulatory requirements, and customer preferences while building operational capabilities that support sustainable growth.

Growth Projections indicate continued expansion of Mexico’s cold chain logistics market, with projected growth rates of 9.1% CAGR over the next five years. This growth is supported by increasing agricultural exports, pharmaceutical manufacturing expansion, and growing domestic demand for temperature-controlled products.

Technology Evolution will transform cold chain operations through advanced automation, artificial intelligence, and sustainable refrigeration systems. These technological advances will improve operational efficiency, reduce environmental impact, and enable new service capabilities that meet evolving customer requirements.

Market Maturation trends suggest increasing consolidation among service providers, with larger companies acquiring specialized operators to create comprehensive service platforms. This consolidation will improve service quality, expand geographic coverage, and create economies of scale that benefit customers and shareholders.

International Integration will strengthen Mexico’s position as a regional cold chain logistics hub, with improved connectivity to North and South American markets. Enhanced trade relationships and infrastructure investments will create new opportunities for cross-border cold chain services and expand the addressable market for Mexican logistics providers.

Mexico’s cold chain logistics market presents exceptional growth opportunities driven by agricultural export strength, pharmaceutical manufacturing expansion, and increasing consumer demand for temperature-controlled products. The market benefits from strategic geographic advantages, growing infrastructure investments, and supportive trade relationships that create favorable conditions for sustained expansion.

Key success factors for market participants include technology adoption, operational excellence, and strategic positioning in high-growth segments. Companies that invest in advanced monitoring systems, automation technologies, and sustainable practices will achieve competitive advantages and capture larger market shares in this dynamic sector.

Future market development will be characterized by continued consolidation, technology innovation, and international integration. The combination of growing demand, infrastructure improvements, and regulatory support creates a positive outlook for Mexico’s cold chain logistics market, positioning it as a critical component of the country’s economic development and international trade competitiveness.

What is Cold Chain Logistics?

Cold Chain Logistics refers to the temperature-controlled supply chain that is essential for transporting perishable goods such as food, pharmaceuticals, and chemicals. It ensures that products are kept within specific temperature ranges to maintain their quality and safety throughout the distribution process.

What are the key players in the Mexico Cold Chain Logistics Market?

Key players in the Mexico Cold Chain Logistics Market include companies like Grupo Bimbo, DHL Supply Chain, and Kuehne + Nagel, which provide specialized services for temperature-sensitive products. These companies focus on maintaining the integrity of the cold chain through advanced logistics solutions, among others.

What are the main drivers of the Mexico Cold Chain Logistics Market?

The main drivers of the Mexico Cold Chain Logistics Market include the increasing demand for fresh food products, the growth of the pharmaceutical industry, and the rising consumer awareness regarding food safety. These factors contribute to the expansion of temperature-controlled logistics solutions.

What challenges does the Mexico Cold Chain Logistics Market face?

The Mexico Cold Chain Logistics Market faces challenges such as inadequate infrastructure, high operational costs, and regulatory compliance issues. These challenges can hinder the efficiency and effectiveness of cold chain operations.

What opportunities exist in the Mexico Cold Chain Logistics Market?

Opportunities in the Mexico Cold Chain Logistics Market include the adoption of advanced technologies like IoT and blockchain for better tracking and monitoring of shipments. Additionally, the growing e-commerce sector presents new avenues for cold chain logistics services.

What trends are shaping the Mexico Cold Chain Logistics Market?

Trends shaping the Mexico Cold Chain Logistics Market include the increasing use of automation in warehousing and transportation, as well as a focus on sustainability practices. Companies are also investing in energy-efficient refrigeration technologies to reduce their carbon footprint.

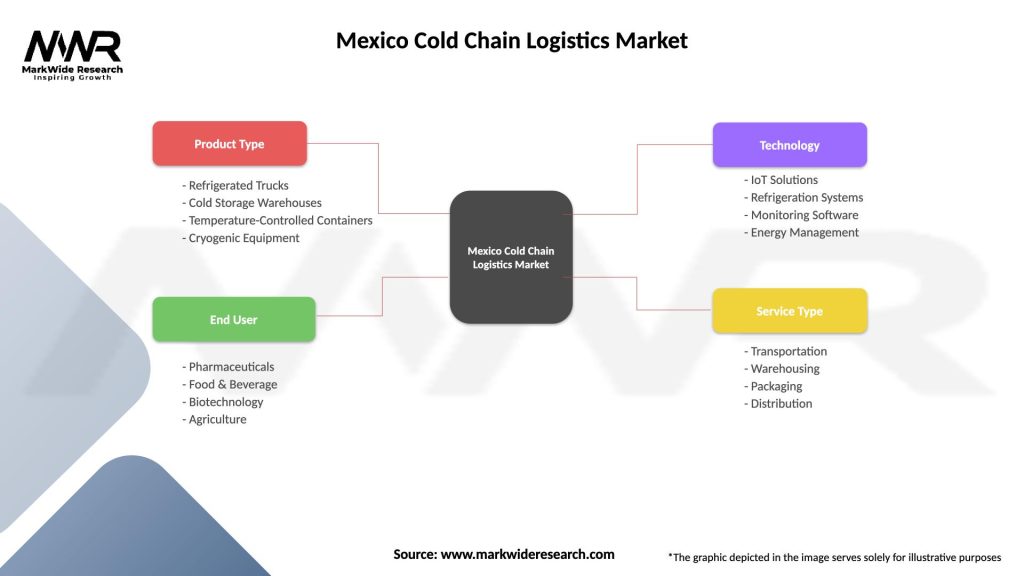

Mexico Cold Chain Logistics Market

| Segmentation Details | Description |

|---|---|

| Product Type | Refrigerated Trucks, Cold Storage Warehouses, Temperature-Controlled Containers, Cryogenic Equipment |

| End User | Pharmaceuticals, Food & Beverage, Biotechnology, Agriculture |

| Technology | IoT Solutions, Refrigeration Systems, Monitoring Software, Energy Management |

| Service Type | Transportation, Warehousing, Packaging, Distribution |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Mexico Cold Chain Logistics Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.