444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Brazil continuous glucose monitoring market represents a rapidly expanding segment within the country’s healthcare technology landscape, driven by increasing diabetes prevalence and growing awareness of advanced glucose management solutions. Continuous glucose monitoring (CGM) systems have emerged as revolutionary devices that provide real-time glucose readings, enabling diabetic patients to make informed decisions about their treatment and lifestyle choices. The Brazilian market demonstrates significant potential for growth, with healthcare providers and patients increasingly recognizing the benefits of continuous monitoring over traditional fingerstick methods.

Market dynamics in Brazil reflect a combination of rising healthcare investments, expanding insurance coverage, and technological advancements that make CGM devices more accessible to diverse patient populations. The market experiences robust growth driven by an aging population, lifestyle changes contributing to diabetes incidence, and government initiatives promoting diabetes management. Healthcare infrastructure improvements across Brazil’s major metropolitan areas have facilitated better distribution and support for advanced medical devices, creating favorable conditions for CGM adoption.

Regional distribution shows concentrated demand in São Paulo, Rio de Janeiro, and other major urban centers, where healthcare facilities possess the necessary infrastructure to support CGM technology implementation. The market exhibits strong growth potential with 12.5% CAGR projected over the forecast period, reflecting increasing patient awareness and healthcare provider adoption of continuous monitoring solutions.

The Brazil continuous glucose monitoring market refers to the comprehensive ecosystem of medical devices, technologies, and services that enable real-time glucose level monitoring for diabetic patients throughout the Brazilian healthcare system. Continuous glucose monitoring represents a paradigm shift from traditional glucose testing methods, offering patients and healthcare providers continuous insights into glucose fluctuations, trends, and patterns that inform treatment decisions and lifestyle modifications.

CGM systems consist of small sensors inserted under the skin that measure glucose levels in interstitial fluid, transmitting data wirelessly to receivers, smartphones, or insulin pumps. This technology eliminates the need for frequent fingerstick tests while providing comprehensive glucose data that helps patients and healthcare providers optimize diabetes management strategies. The Brazilian market encompasses various CGM technologies, from basic real-time monitoring systems to advanced integrated platforms that connect with insulin delivery systems.

Market scope includes sensor technologies, data management software, mobile applications, and associated healthcare services that support continuous glucose monitoring implementation across Brazil’s diverse healthcare landscape. The definition extends to encompass both prescription-based medical devices and emerging over-the-counter monitoring solutions that serve different patient segments and clinical requirements.

Brazil’s continuous glucose monitoring market demonstrates exceptional growth momentum, driven by increasing diabetes prevalence, technological innovations, and expanding healthcare access across the country. The market benefits from strong government support for diabetes management initiatives, growing insurance coverage for advanced medical devices, and rising patient awareness of continuous monitoring benefits. Key market drivers include the country’s aging population, lifestyle-related diabetes increases, and healthcare digitization trends that favor connected medical devices.

Technological advancement plays a crucial role in market expansion, with manufacturers introducing more accurate, user-friendly, and cost-effective CGM solutions tailored to Brazilian market needs. The integration of artificial intelligence, mobile connectivity, and cloud-based data analytics enhances the value proposition of CGM systems, making them attractive to both patients and healthcare providers. Market penetration remains relatively low compared to developed markets, indicating substantial growth opportunities as awareness and accessibility improve.

Competitive landscape features both international medical device companies and emerging local players developing solutions specifically for the Brazilian market. The market shows strong potential for sustained growth, with healthcare expenditure increases and government diabetes prevention programs creating favorable conditions for CGM adoption across diverse patient populations.

Market insights reveal several critical factors shaping Brazil’s continuous glucose monitoring landscape, providing valuable perspectives for stakeholders across the healthcare ecosystem. Understanding these insights enables better strategic decision-making and market positioning for companies operating in this dynamic sector.

Primary market drivers propelling Brazil’s continuous glucose monitoring market growth stem from demographic, technological, and healthcare system factors that create favorable conditions for CGM adoption. These drivers work synergistically to expand market opportunities and accelerate technology penetration across diverse patient populations.

Demographic trends represent fundamental growth drivers, with Brazil’s aging population experiencing higher diabetes incidence rates and requiring more sophisticated glucose management solutions. The country’s urbanization patterns contribute to lifestyle changes that increase diabetes risk, creating expanding patient populations that benefit from continuous monitoring technology. Healthcare awareness campaigns and diabetes education programs increase patient understanding of CGM benefits, driving demand for advanced monitoring solutions.

Technological advancement serves as a critical driver, with manufacturers developing more accurate, comfortable, and user-friendly CGM systems that appeal to Brazilian patients. Integration with smartphones and digital health platforms enhances the value proposition, making CGM systems more attractive to tech-savvy patients and healthcare providers. Cost reduction trends in sensor manufacturing and device production make CGM technology increasingly accessible to broader patient segments.

Healthcare system evolution supports market growth through improved diabetes care protocols, expanded specialist networks, and enhanced medical device distribution infrastructure. Government initiatives promoting diabetes prevention and management create supportive policy environments for CGM adoption, while insurance coverage expansion reduces financial barriers for patients seeking continuous monitoring solutions.

Market restraints present challenges that may limit the pace of continuous glucose monitoring adoption in Brazil, requiring strategic approaches from manufacturers and healthcare providers to address these barriers effectively. Understanding these constraints enables better market entry strategies and product development decisions.

Cost considerations remain significant restraints, as CGM systems require ongoing sensor replacements and associated expenses that may burden patients with limited financial resources. Despite improving insurance coverage, many patients still face out-of-pocket costs that influence their ability to maintain continuous monitoring regimens. Economic disparities across Brazil’s regions create uneven market access, with rural and lower-income populations having limited access to advanced diabetes management technologies.

Healthcare infrastructure limitations in certain regions restrict CGM implementation, as these systems require technical support, patient education, and healthcare provider training that may not be readily available in all areas. Regulatory complexity and approval processes, while improving, can still create delays in bringing new CGM technologies to market, limiting patient access to the latest innovations.

Patient education challenges represent ongoing restraints, as effective CGM use requires understanding of glucose patterns, data interpretation, and device maintenance that may overwhelm some patients. Healthcare provider training needs also create implementation barriers, as successful CGM programs require knowledgeable medical professionals who can guide patients through technology adoption and ongoing management.

Market opportunities in Brazil’s continuous glucose monitoring sector present substantial potential for growth and innovation, driven by unmet medical needs, technological possibilities, and evolving healthcare delivery models. These opportunities create pathways for market expansion and value creation across the diabetes care ecosystem.

Underserved patient populations represent significant opportunities, as current CGM penetration rates remain low compared to the total diabetic population in Brazil. Expanding access to rural areas, developing cost-effective solutions for lower-income patients, and creating culturally appropriate education programs can unlock substantial market potential. Pediatric diabetes management presents growing opportunities as parents and healthcare providers recognize CGM benefits for children with Type 1 diabetes.

Technology integration opportunities include developing CGM systems that connect with telemedicine platforms, electronic health records, and artificial intelligence-powered diabetes management applications. Partnership opportunities with local healthcare providers, insurance companies, and government health programs can accelerate market penetration and improve patient access to continuous monitoring technology.

Product innovation opportunities focus on developing CGM solutions specifically tailored to Brazilian market needs, including Portuguese-language interfaces, local customer support, and pricing models that accommodate diverse economic circumstances. Healthcare digitization trends create opportunities for integrated diabetes management platforms that combine CGM data with other health metrics and lifestyle factors.

Market dynamics in Brazil’s continuous glucose monitoring sector reflect complex interactions between technological innovation, healthcare policy changes, patient needs, and competitive forces that shape market evolution and growth trajectories. These dynamics create both challenges and opportunities for market participants.

Supply chain dynamics influence market development through manufacturing capabilities, distribution networks, and technical support infrastructure that determine how effectively CGM products reach Brazilian patients. International manufacturers must navigate import regulations, local partnership requirements, and currency fluctuations that affect product pricing and availability. Demand dynamics reflect changing patient preferences, healthcare provider recommendations, and insurance coverage decisions that influence CGM adoption rates.

Competitive dynamics intensify as more companies enter the Brazilian market, driving innovation, improving product features, and potentially reducing costs for patients. Regulatory dynamics continue evolving as Brazilian health authorities adapt policies to accommodate new CGM technologies while ensuring patient safety and product efficacy. These regulatory changes can significantly impact market access and competitive positioning.

Healthcare delivery dynamics shift toward more personalized, data-driven diabetes management approaches that favor CGM adoption. The integration of continuous monitoring data with broader healthcare systems creates new possibilities for population health management and improved clinical outcomes. Economic dynamics including healthcare spending patterns, insurance coverage evolution, and government health program funding influence market growth potential and accessibility.

Research methodology employed for analyzing Brazil’s continuous glucose monitoring market incorporates comprehensive primary and secondary research approaches designed to provide accurate, reliable, and actionable market intelligence. The methodology ensures thorough coverage of market dynamics, competitive landscape, and growth opportunities while maintaining analytical rigor and objectivity.

Primary research components include extensive interviews with healthcare providers, diabetes specialists, medical device distributors, and patient advocacy groups throughout Brazil. These interviews provide firsthand insights into market challenges, adoption patterns, and future growth prospects from diverse stakeholder perspectives. Patient surveys and focus groups offer valuable insights into CGM user experiences, preferences, and barriers to adoption that inform market analysis and strategic recommendations.

Secondary research methodology encompasses analysis of government health statistics, medical device registration data, healthcare expenditure reports, and diabetes prevalence studies from authoritative Brazilian health organizations. Market intelligence gathering includes monitoring competitor activities, product launches, pricing strategies, and partnership announcements that influence market dynamics and competitive positioning.

Data validation processes ensure accuracy through cross-referencing multiple sources, expert review panels, and statistical analysis techniques that identify trends and patterns in market development. MarkWide Research employs rigorous quality control measures throughout the research process to maintain high standards of analytical accuracy and reliability in market assessments.

Regional analysis of Brazil’s continuous glucose monitoring market reveals significant variations in adoption patterns, healthcare infrastructure, and growth potential across different geographic areas. Understanding these regional differences enables more targeted market strategies and resource allocation decisions for companies operating in the Brazilian CGM sector.

Southeast Region dominates the Brazilian CGM market, with São Paulo and Rio de Janeiro metropolitan areas accounting for approximately 45% of total market share. This region benefits from advanced healthcare infrastructure, higher concentrations of diabetes specialists, and greater insurance coverage for medical devices. Patient awareness and technology adoption rates remain highest in these urban centers, supported by better access to medical education and digital health resources.

South Region demonstrates strong growth potential, with cities like Porto Alegre and Curitiba showing increasing CGM adoption rates of approximately 18% market share. The region’s relatively high income levels and well-developed healthcare systems create favorable conditions for advanced diabetes management technologies. Healthcare provider engagement in the South Region shows positive trends toward recommending CGM systems for appropriate patients.

Northeast and Central-West Regions represent emerging opportunities with combined market share of approximately 25%, driven by expanding healthcare infrastructure and growing diabetes awareness programs. These regions face challenges related to healthcare access and economic constraints but demonstrate increasing interest in digital health solutions. Government health initiatives in these regions focus on improving diabetes care access and may accelerate CGM adoption in the coming years.

Competitive landscape in Brazil’s continuous glucose monitoring market features a mix of established international medical device companies and emerging local players, creating a dynamic environment characterized by innovation, strategic partnerships, and evolving market positioning strategies.

Market competition intensifies through product innovation, pricing strategies, and patient support program development. Companies invest heavily in clinical studies, regulatory approvals, and healthcare provider education to establish market presence and build patient loyalty. Strategic partnerships with local distributors, healthcare systems, and insurance providers play crucial roles in market penetration and sustainable growth.

Market segmentation analysis provides detailed insights into different CGM market segments, enabling better understanding of customer needs, growth opportunities, and competitive dynamics across various product categories and patient populations in Brazil.

By Technology:

By Patient Type:

By End User:

Category-wise analysis reveals distinct patterns and opportunities within different segments of Brazil’s continuous glucose monitoring market, providing valuable insights for strategic planning and product development initiatives.

Real-Time CGM Category demonstrates the highest growth potential, driven by patients seeking immediate glucose information and healthcare providers recommending advanced monitoring for complex diabetes cases. This category benefits from technological innovations including smartphone integration, cloud-based data storage, and artificial intelligence-powered insights. Market penetration in this category reaches approximately 35% of total CGM users, with strong growth expected as prices become more accessible.

Flash Glucose Monitoring Category shows broad market appeal due to its balance of functionality and affordability, making it accessible to larger patient populations. This category experiences steady growth as patients transition from traditional fingerstick testing to continuous monitoring solutions. User satisfaction rates remain high, with approximately 78% of users reporting improved diabetes management and quality of life.

Pediatric CGM Category represents a specialized but growing segment, with parents and healthcare providers increasingly recognizing the benefits of continuous monitoring for children with diabetes. This category requires specialized features including parental monitoring capabilities, school-friendly designs, and age-appropriate user interfaces. Adoption rates in pediatric populations show 22% annual growth, driven by improved clinical outcomes and family peace of mind.

Industry participants and stakeholders in Brazil’s continuous glucose monitoring market realize substantial benefits through participation in this growing healthcare technology sector, creating value for patients, healthcare providers, and business organizations.

For Patients:

For Healthcare Providers:

For Industry Companies:

SWOT analysis provides comprehensive evaluation of Brazil’s continuous glucose monitoring market, identifying internal strengths and weaknesses alongside external opportunities and threats that influence market development and strategic planning.

Strengths:

Weaknesses:

Opportunities:

Threats:

Key market trends shaping Brazil’s continuous glucose monitoring landscape reflect technological advancement, changing patient preferences, and evolving healthcare delivery models that influence market development and competitive dynamics.

Digital Health Integration represents a dominant trend, with CGM systems increasingly connecting to smartphone applications, cloud platforms, and electronic health records. This integration enables comprehensive diabetes management ecosystems that combine glucose monitoring with medication tracking, lifestyle logging, and healthcare provider communication. Artificial intelligence and machine learning capabilities enhance CGM value by providing predictive insights and personalized recommendations for glucose management.

Personalized Medicine Approaches drive demand for CGM systems that adapt to individual patient needs, preferences, and clinical requirements. Manufacturers develop customizable monitoring solutions with adjustable alert settings, personalized target ranges, and individualized data presentation formats. Patient-centric design focuses on user experience improvements that make CGM technology more accessible and engaging for diverse patient populations.

Telemedicine Integration accelerates as healthcare providers adopt remote monitoring capabilities that leverage CGM data for virtual consultations and care management. This trend particularly benefits patients in rural areas or those with mobility limitations, expanding access to specialized diabetes care. Remote patient monitoring programs demonstrate improved clinical outcomes and cost-effectiveness, encouraging broader adoption across healthcare systems.

Cost Reduction Initiatives focus on making CGM technology more affordable through manufacturing innovations, economies of scale, and alternative pricing models. Subscription-based services, insurance coverage expansion, and government subsidy programs work to reduce financial barriers for patients. Value-based care models emphasize clinical outcomes and cost-effectiveness, supporting CGM adoption through demonstrated health improvements.

Industry developments in Brazil’s continuous glucose monitoring market reflect rapid innovation, strategic partnerships, and regulatory evolution that shape market dynamics and competitive positioning for industry participants.

Product Innovation Developments include the introduction of next-generation CGM sensors with improved accuracy, extended wear time, and enhanced user comfort. Manufacturers invest heavily in research and development to create sensors that require less calibration, provide more reliable data, and integrate seamlessly with digital health platforms. Miniaturization trends result in smaller, more discreet devices that appeal to patients concerned about device visibility and lifestyle impact.

Regulatory Developments show Brazilian health authorities streamlining approval processes for innovative CGM technologies while maintaining safety and efficacy standards. Recent regulatory changes facilitate faster market entry for new products and expand access to over-the-counter monitoring solutions. ANVISA initiatives support digital health innovation through updated guidelines that accommodate connected medical devices and data sharing platforms.

Partnership Developments demonstrate increasing collaboration between international CGM manufacturers and Brazilian healthcare organizations, distributors, and technology companies. These partnerships focus on improving market access, developing local support capabilities, and creating culturally appropriate patient education programs. Strategic alliances with insurance companies and government health programs expand coverage and reduce patient costs.

Market Access Developments include expanded insurance coverage for CGM devices, government pilot programs for diabetes management, and healthcare system initiatives that integrate continuous monitoring into standard care protocols. MarkWide Research analysis indicates these developments significantly improve market accessibility and accelerate adoption rates across diverse patient populations.

Analyst recommendations for stakeholders in Brazil’s continuous glucose monitoring market focus on strategic approaches that maximize growth opportunities while addressing market challenges and competitive dynamics effectively.

For Market Entrants:

For Healthcare Providers:

For Investors:

Future outlook for Brazil’s continuous glucose monitoring market indicates sustained growth driven by demographic trends, technological advancement, and healthcare system evolution that create favorable conditions for market expansion and innovation.

Market growth projections suggest continued expansion with anticipated 15.2% annual growth over the next five years, driven by increasing diabetes prevalence, improving healthcare access, and technological innovations that make CGM systems more attractive to patients and healthcare providers. Patient adoption rates are expected to accelerate as awareness increases and costs decrease through manufacturing improvements and competitive pressures.

Technology evolution will likely focus on enhanced accuracy, extended sensor life, and improved integration with digital health ecosystems. Artificial intelligence applications will become more sophisticated, providing predictive analytics and personalized recommendations that enhance clinical outcomes and patient engagement. Non-invasive monitoring technologies may emerge as game-changing innovations that eliminate the need for sensor insertion.

Healthcare integration will deepen as CGM data becomes standard components of diabetes care protocols, population health management programs, and value-based care initiatives. Telemedicine expansion will leverage CGM data for remote patient monitoring and virtual care delivery, particularly benefiting underserved populations in rural areas.

Market accessibility improvements through expanded insurance coverage, government health programs, and innovative financing models will broaden CGM access to diverse patient populations. MWR analysis suggests that market penetration rates could reach 25% of eligible patients within the forecast period, representing substantial growth from current adoption levels.

Brazil’s continuous glucose monitoring market represents a dynamic and rapidly evolving healthcare technology sector with substantial growth potential driven by increasing diabetes prevalence, technological innovation, and improving healthcare infrastructure. The market demonstrates strong fundamentals including a large patient population, supportive regulatory environment, and growing awareness of continuous monitoring benefits among patients and healthcare providers.

Key success factors for market participants include developing cost-effective solutions tailored to Brazilian market needs, establishing strong local partnerships, and investing in comprehensive patient and provider education programs. The competitive landscape continues evolving as international companies expand their presence while local players develop innovative solutions for specific market segments.

Strategic opportunities abound for companies that can effectively address market challenges including cost barriers, regional access disparities, and education needs while leveraging technological advancement and healthcare digitization trends. The integration of CGM technology with broader digital health ecosystems creates new value propositions and competitive advantages for forward-thinking market participants.

Long-term market prospects remain highly positive, supported by demographic trends, healthcare policy evolution, and continuous technological improvement that enhance CGM value propositions. Success in this market requires sustained commitment, cultural sensitivity, and strategic focus on patient outcomes and healthcare provider needs. Companies that effectively navigate these requirements will be well-positioned to capitalize on Brazil’s substantial continuous glucose monitoring market opportunities and contribute to improved diabetes care outcomes across the country.

What is Continuous Glucose Monitoring?

Continuous Glucose Monitoring (CGM) refers to a method of tracking glucose levels in real-time using a small sensor placed under the skin. This technology is primarily used by individuals with diabetes to manage their blood sugar levels more effectively.

What are the key players in the Brazil Continuous Glucose Monitoring Market?

Key players in the Brazil Continuous Glucose Monitoring Market include Abbott Laboratories, Dexcom, and Medtronic, which are known for their innovative CGM systems and technologies. These companies focus on enhancing user experience and accuracy in glucose monitoring, among others.

What are the growth factors driving the Brazil Continuous Glucose Monitoring Market?

The growth of the Brazil Continuous Glucose Monitoring Market is driven by the increasing prevalence of diabetes, rising awareness about diabetes management, and advancements in CGM technology. Additionally, the demand for real-time monitoring solutions is contributing to market expansion.

What challenges does the Brazil Continuous Glucose Monitoring Market face?

The Brazil Continuous Glucose Monitoring Market faces challenges such as high costs of CGM devices, limited reimbursement policies, and the need for user training. These factors can hinder widespread adoption among patients and healthcare providers.

What opportunities exist in the Brazil Continuous Glucose Monitoring Market?

Opportunities in the Brazil Continuous Glucose Monitoring Market include the potential for technological advancements, such as integration with mobile health applications and artificial intelligence. Additionally, increasing government initiatives to support diabetes care can further enhance market growth.

What trends are shaping the Brazil Continuous Glucose Monitoring Market?

Trends shaping the Brazil Continuous Glucose Monitoring Market include the development of more user-friendly devices, the rise of telehealth services, and the growing emphasis on personalized medicine. These trends are influencing how patients manage their diabetes and interact with healthcare providers.

Brazil Continuous Glucose Monitoring Market

| Segmentation Details | Description |

|---|---|

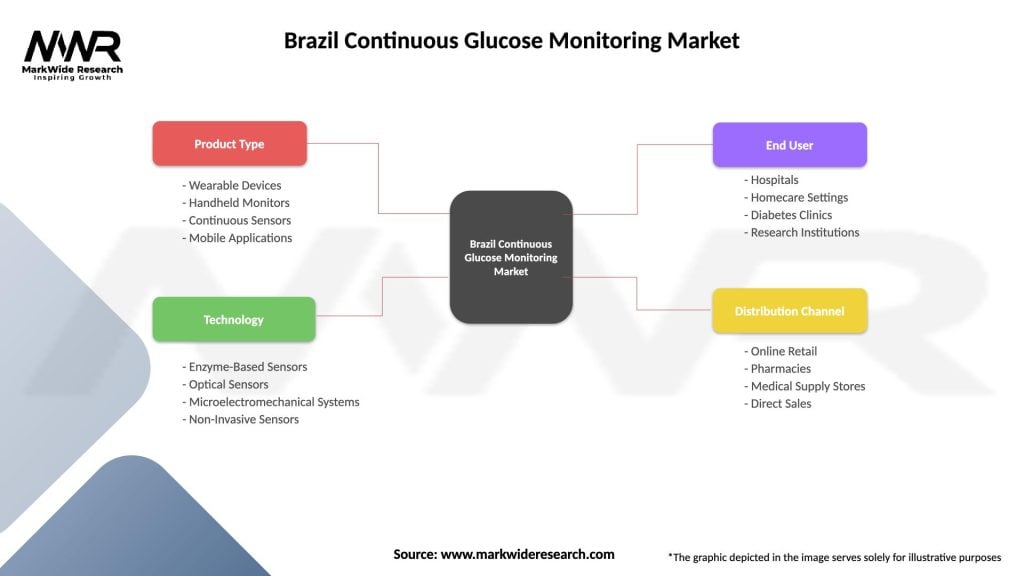

| Product Type | Wearable Devices, Handheld Monitors, Continuous Sensors, Mobile Applications |

| Technology | Enzyme-Based Sensors, Optical Sensors, Microelectromechanical Systems, Non-Invasive Sensors |

| End User | Hospitals, Homecare Settings, Diabetes Clinics, Research Institutions |

| Distribution Channel | Online Retail, Pharmacies, Medical Supply Stores, Direct Sales |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Brazil Continuous Glucose Monitoring Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.