444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The passive electronic components in the oil and gas industry market represents a critical segment that underpins the technological infrastructure of modern energy operations. Passive electronic components, including resistors, capacitors, inductors, and transformers, serve as fundamental building blocks in sophisticated control systems, monitoring equipment, and safety mechanisms throughout oil and gas facilities worldwide. These components operate without requiring external power sources, making them essential for reliable performance in harsh industrial environments.

Market dynamics indicate robust growth driven by increasing digitalization of oil and gas operations, with the sector experiencing a compound annual growth rate (CAGR) of 6.2% over recent years. The integration of advanced technologies such as Internet of Things (IoT), artificial intelligence, and predictive maintenance systems has significantly increased demand for high-performance passive components. Industry transformation toward smart oilfields and automated drilling operations continues to fuel market expansion, with upstream, midstream, and downstream segments all contributing to increased component consumption.

Regional distribution shows North America maintaining approximately 35% market share, followed by the Middle East and Asia-Pacific regions. The market’s resilience stems from the oil and gas industry’s continuous need for equipment upgrades, safety enhancements, and operational efficiency improvements. Technological advancement in component miniaturization and enhanced durability has enabled deployment in increasingly challenging environments, from deep-sea drilling platforms to extreme temperature processing facilities.

The passive electronic components in the oil and gas industry market refers to the specialized segment encompassing electronic components that do not require external power to function and are specifically designed for deployment in petroleum exploration, extraction, refining, and distribution operations. These components include resistors for current limiting, capacitors for energy storage and filtering, inductors for electromagnetic interference suppression, and transformers for voltage regulation across various oil and gas applications.

Market significance extends beyond simple component supply, encompassing the entire ecosystem of specialized manufacturing, testing, certification, and maintenance services required to ensure reliable operation in hazardous and demanding environments. The market includes components rated for explosive atmospheres, extreme temperatures, corrosive conditions, and high-vibration scenarios typical of oil and gas operations.

Strategic market positioning reveals the passive electronic components sector as an indispensable foundation for oil and gas industry modernization. The market demonstrates consistent growth patterns driven by increasing automation adoption, with digital transformation initiatives accounting for approximately 42% of new component demand. Key market participants focus on developing ruggedized components capable of withstanding harsh operational conditions while maintaining precise performance characteristics.

Investment trends show significant capital allocation toward research and development of next-generation passive components optimized for oil and gas applications. The market benefits from stringent safety regulations requiring advanced monitoring and control systems, creating sustained demand for high-reliability components. Technological convergence between traditional oil and gas operations and modern digital technologies continues to expand market opportunities across all industry segments.

Competitive landscape features established electronic component manufacturers alongside specialized suppliers focusing exclusively on oil and gas applications. Market consolidation trends indicate strategic partnerships between component suppliers and oil and gas equipment manufacturers to develop integrated solutions. Supply chain resilience has become a critical factor, with companies investing in diversified sourcing strategies to ensure continuous component availability.

Market intelligence reveals several critical insights shaping the passive electronic components landscape in oil and gas applications:

Primary market drivers propelling growth in passive electronic components for oil and gas applications stem from fundamental industry transformation and technological advancement. The increasing complexity of oil and gas operations necessitates sophisticated electronic systems that rely heavily on passive components for stable operation. Digitalization initiatives across the industry create substantial demand for components supporting advanced control systems, data acquisition networks, and communication infrastructure.

Regulatory compliance serves as a significant driver, with safety standards requiring redundant monitoring systems and fail-safe mechanisms that depend on reliable passive components. The push toward operational efficiency motivates investments in automation and optimization technologies, directly increasing component consumption. Infrastructure modernization in aging oil and gas facilities drives replacement and upgrade cycles, creating sustained market demand.

Environmental monitoring requirements mandate sophisticated sensing and control systems that utilize passive components for signal conditioning and data processing. The expansion of unconventional oil and gas extraction methods, including hydraulic fracturing and enhanced oil recovery, requires specialized electronic systems with ruggedized passive components. Remote operation capabilities increasingly important for offshore and remote locations, drive demand for reliable communication and control systems.

Market constraints affecting passive electronic components in oil and gas applications include cyclical industry spending patterns that create demand volatility. Economic downturns and commodity price fluctuations directly impact capital expenditure budgets, leading to delayed equipment upgrades and reduced component procurement. Technical challenges associated with developing components capable of operating reliably in extreme environments increase development costs and time-to-market.

Supply chain complexities present ongoing challenges, particularly for specialized components with limited supplier bases. Long lead times for custom or high-specification components can delay project implementations and increase inventory carrying costs. Certification requirements for hazardous area applications add complexity and cost to component development and procurement processes.

Competitive pressure from alternative technologies and solutions may limit growth in certain application areas. The conservative nature of the oil and gas industry can slow adoption of new component technologies, preferring proven solutions over innovative alternatives. Skills shortages in specialized engineering disciplines affect both component development and proper application in oil and gas systems.

Emerging opportunities in the passive electronic components market for oil and gas applications center on technological advancement and industry evolution. The transition toward renewable energy integration creates opportunities for components supporting hybrid energy systems and grid stabilization applications. Smart field development offers substantial growth potential as operators seek to optimize production through advanced monitoring and control systems.

Offshore expansion in deeper waters and harsher environments creates demand for ultra-reliable components capable of extended operation without maintenance access. The growing focus on environmental sustainability drives opportunities for components supporting emission monitoring, leak detection, and environmental compliance systems. Digital twin technology implementation requires sophisticated sensor networks and data acquisition systems utilizing passive components.

Emerging markets present significant growth opportunities as developing regions expand oil and gas infrastructure and adopt modern technologies. The increasing complexity of unconventional resource extraction methods creates demand for specialized components supporting advanced drilling and completion technologies. Cybersecurity concerns drive opportunities for components supporting secure communication and control systems in critical infrastructure applications.

Market dynamics in the passive electronic components sector reflect the complex interplay between technological advancement, regulatory requirements, and industry transformation. The oil and gas industry’s gradual shift toward digitalization creates sustained demand for components supporting advanced automation and monitoring systems. Component miniaturization trends enable deployment in space-constrained applications while maintaining performance specifications.

Supply-demand balance remains influenced by cyclical industry spending patterns and global economic conditions. According to MarkWide Research analysis, the market demonstrates resilience through diversification across upstream, midstream, and downstream applications. Technology convergence between traditional oil and gas operations and modern digital systems creates new application areas and component requirements.

Competitive dynamics feature established component manufacturers expanding into oil and gas applications alongside specialized suppliers developing niche solutions. The market benefits from increasing standardization of component specifications while maintaining flexibility for custom applications. Innovation cycles driven by industry needs for improved reliability, efficiency, and environmental compliance continue to shape market evolution.

Research approach for analyzing the passive electronic components in oil and gas industry market employs comprehensive primary and secondary research methodologies. Primary research includes structured interviews with industry executives, component manufacturers, oil and gas operators, and technology integrators to gather firsthand insights into market trends, challenges, and opportunities. Survey methodologies capture quantitative data on component usage patterns, procurement practices, and future investment intentions.

Secondary research encompasses analysis of industry reports, company financial statements, patent filings, and regulatory documentation to understand market structure and competitive dynamics. Technical literature review provides insights into component performance requirements and emerging technology trends. Market modeling techniques incorporate multiple data sources to develop comprehensive market size estimates and growth projections.

Data validation processes ensure accuracy through triangulation of multiple sources and expert review panels. Regional analysis incorporates local market conditions, regulatory environments, and industry development patterns. Trend analysis utilizes historical data patterns to identify market cycles and predict future developments in component demand and technology evolution.

North American market maintains leadership position with approximately 35% global market share, driven by extensive shale oil and gas development and advanced technology adoption. The region benefits from established supply chains, strong regulatory frameworks, and significant investment in digital oilfield technologies. United States dominates regional demand through large-scale unconventional resource development and infrastructure modernization programs.

Middle East region represents approximately 28% market share, supported by massive oil and gas reserves and ongoing infrastructure development projects. The region’s focus on production optimization and enhanced oil recovery drives demand for advanced monitoring and control systems. Gulf Cooperation Council countries lead regional investment in smart field technologies and operational efficiency improvements.

Asia-Pacific market shows rapid growth with 22% market share, driven by expanding energy infrastructure and increasing industrial automation adoption. China and India represent major growth markets through domestic energy development and refining capacity expansion. Offshore development in the region creates demand for specialized components capable of operating in marine environments.

European market accounts for 12% market share, characterized by mature infrastructure and focus on environmental compliance and efficiency improvements. The region’s emphasis on renewable energy integration creates opportunities for components supporting hybrid energy systems. North Sea operations drive demand for high-reliability components in challenging offshore environments.

Market competition features a diverse ecosystem of established electronic component manufacturers, specialized oil and gas suppliers, and emerging technology companies. Leading players focus on developing ruggedized components specifically designed for harsh oil and gas environments while maintaining competitive pricing and reliable supply chains.

Strategic partnerships between component manufacturers and oil and gas equipment suppliers create integrated solutions and preferred supplier relationships. Market consolidation trends indicate ongoing merger and acquisition activity as companies seek to expand product portfolios and geographic reach.

Component type segmentation reveals distinct market characteristics across different passive component categories:

By Component Type:

By Application Segment:

By Technology Platform:

Resistor category demonstrates steady growth driven by increasing automation and control system complexity. Precision resistors for sensor applications and high-power resistors for load testing represent key growth segments. Temperature coefficient and long-term stability requirements drive demand for specialized resistor technologies in critical measurement applications.

Capacitor segment shows robust expansion supported by power electronics applications and electromagnetic interference filtering requirements. Electrolytic capacitors for power supplies and ceramic capacitors for high-frequency applications represent major demand drivers. Reliability improvements in harsh environment applications continue to drive technology development and market growth.

Inductor applications benefit from increasing focus on power quality and electromagnetic compatibility in oil and gas facilities. Common-mode chokes and power inductors for switching power supplies represent growing application areas. Magnetic core materials optimized for high-temperature operation enable deployment in challenging environments.

Transformer category experiences growth through power distribution modernization and isolation requirements in hazardous areas. Current transformers for metering applications and isolation transformers for safety systems drive market demand. Custom transformer solutions for specialized applications create opportunities for value-added suppliers.

Oil and gas operators benefit from improved system reliability and reduced maintenance requirements through deployment of high-quality passive components. Enhanced operational efficiency and safety performance result from reliable electronic systems supporting critical operations. Cost optimization opportunities emerge through predictive maintenance capabilities and extended equipment lifecycles.

Component manufacturers gain access to a stable, high-value market with opportunities for long-term supplier relationships and custom product development. The oil and gas industry’s emphasis on reliability creates premium pricing opportunities for specialized components. Technology leadership in harsh environment applications provides competitive advantages and market differentiation.

System integrators benefit from comprehensive component portfolios enabling complete solution development for oil and gas applications. Partnerships with component suppliers provide access to technical expertise and application support. Value-added services including testing, certification, and lifecycle management create additional revenue opportunities.

End-user stakeholders experience improved operational performance through reliable electronic systems and reduced downtime. Enhanced safety performance and regulatory compliance result from properly specified and applied passive components. Investment protection through long-term component availability and support ensures sustainable operations.

Strengths:

Weaknesses:

Opportunities:

Threats:

Miniaturization trend continues driving development of smaller, more efficient passive components without compromising performance or reliability. Advanced materials and manufacturing techniques enable significant size reductions while maintaining or improving electrical characteristics. Integration opportunities with active components create system-level solutions optimized for specific oil and gas applications.

Smart component development incorporates sensing and communication capabilities into traditional passive components, enabling predictive maintenance and real-time monitoring. These intelligent components provide operational data and health status information, supporting proactive maintenance strategies. Wireless connectivity integration eliminates wiring requirements in challenging installation environments.

Environmental sustainability considerations drive development of components with reduced environmental impact throughout their lifecycle. Lead-free soldering, recyclable materials, and energy-efficient manufacturing processes address industry sustainability goals. Circular economy principles influence component design for repairability and end-of-life recycling.

Customization capabilities become increasingly important as oil and gas operators seek optimized solutions for specific applications. Flexible manufacturing processes and design tools enable rapid development of custom components meeting unique requirements. Application-specific component optimization provides performance advantages and competitive differentiation.

Recent industry developments highlight the dynamic nature of the passive electronic components market in oil and gas applications. Major component manufacturers have announced significant investments in research and development focused on harsh environment applications. Technology partnerships between component suppliers and oil and gas equipment manufacturers create integrated solutions addressing specific industry challenges.

Regulatory developments including updated safety standards and environmental requirements drive component specification changes and create opportunities for advanced solutions. New hazardous area certification processes streamline approval procedures while maintaining safety standards. Industry standardization efforts promote interoperability and reduce procurement complexity for end users.

Manufacturing innovations including advanced materials processing and automated production techniques improve component quality and reduce costs. Investment in regional manufacturing capabilities addresses supply chain resilience concerns and reduces lead times. Quality assurance improvements through advanced testing and validation procedures enhance component reliability in critical applications.

Market consolidation activities include strategic acquisitions and partnerships aimed at expanding product portfolios and geographic reach. Component manufacturers seek to strengthen positions in high-growth application areas and emerging markets. Vertical integration strategies enable better control over quality, costs, and supply chain reliability.

Strategic recommendations for market participants emphasize the importance of developing specialized expertise in oil and gas applications while maintaining cost competitiveness. Component manufacturers should invest in application engineering capabilities and customer support services to differentiate their offerings. Partnership strategies with system integrators and equipment manufacturers can provide access to new markets and application opportunities.

Technology investment priorities should focus on harsh environment performance, miniaturization, and smart component capabilities. Research and development efforts should address emerging application requirements including cybersecurity, environmental monitoring, and renewable energy integration. Manufacturing flexibility becomes critical for serving diverse customer requirements and rapid market changes.

Market expansion opportunities exist in emerging regions and new application areas driven by industry digitalization. Companies should develop local partnerships and distribution networks to effectively serve regional markets. Supply chain diversification strategies reduce risks and ensure component availability during disruptions.

Customer engagement strategies should emphasize technical support, application expertise, and long-term partnership development. Educational programs and technical resources help customers optimize component selection and application. Lifecycle support services including obsolescence management and upgrade planning create additional value for customers.

Market projections indicate continued growth in passive electronic components for oil and gas applications, driven by ongoing industry transformation and technology adoption. MWR analysis suggests the market will maintain a compound annual growth rate of 6.8% over the next five years, supported by digitalization initiatives and infrastructure modernization programs. Technology convergence between traditional oil and gas operations and advanced digital systems will create new component requirements and application opportunities.

Innovation trajectories point toward increased integration of sensing and communication capabilities in passive components, enabling predictive maintenance and real-time monitoring applications. Advanced materials and manufacturing techniques will enable further miniaturization while improving performance and reliability. Sustainability considerations will drive development of environmentally friendly components and manufacturing processes.

Regional growth patterns indicate strongest expansion in Asia-Pacific and Middle East markets, driven by infrastructure development and technology adoption. North American markets will continue to benefit from unconventional resource development and digitalization initiatives. Emerging applications in renewable energy integration and environmental monitoring will create additional growth opportunities.

Industry evolution toward autonomous operations and artificial intelligence integration will require more sophisticated electronic systems and specialized passive components. The increasing complexity of oil and gas operations will drive demand for high-performance, reliable components capable of operating in challenging environments. Long-term prospects remain positive despite cyclical industry challenges, supported by fundamental technology trends and operational requirements.

Market assessment reveals the passive electronic components sector in oil and gas applications as a resilient and growing market driven by fundamental industry transformation and technology advancement. The sector benefits from essential infrastructure requirements, regulatory compliance needs, and ongoing digitalization initiatives across all segments of the oil and gas industry. Strategic positioning of component manufacturers focusing on specialized applications and harsh environment performance creates sustainable competitive advantages.

Growth prospects remain favorable despite cyclical industry challenges, supported by increasing automation adoption, safety requirements, and operational efficiency initiatives. The market’s diversification across upstream, midstream, and downstream applications provides stability and reduces exposure to individual segment volatility. Technology trends including miniaturization, smart components, and environmental sustainability will shape future market development and create new opportunities for innovative suppliers.

Success factors for market participants include technical expertise, application knowledge, reliable supply chains, and strong customer relationships. Companies that invest in research and development, maintain quality standards, and provide comprehensive customer support will be best positioned to capitalize on market opportunities. The passive electronic components market in oil and gas applications represents a stable, growing sector with significant potential for companies that understand industry requirements and deliver specialized solutions meeting demanding operational conditions.

What is Passive Electronic Components?

Passive electronic components are devices that do not require an external power source to operate. They include resistors, capacitors, and inductors, which are essential in various applications within the oil and gas industry, such as signal processing and energy storage.

What are the key players in the Passive Electronic Components In the Oil and Gas Industry Market?

Key players in the Passive Electronic Components In the Oil and Gas Industry Market include companies like Vishay Intertechnology, Murata Manufacturing, and TDK Corporation, among others. These companies provide a range of components that support the operational efficiency of oil and gas exploration and production.

What are the growth factors for the Passive Electronic Components In the Oil and Gas Industry Market?

The growth of the Passive Electronic Components In the Oil and Gas Industry Market is driven by the increasing demand for automation and control systems in oil and gas operations. Additionally, the need for reliable and efficient electronic components to enhance safety and performance in harsh environments contributes to market expansion.

What challenges does the Passive Electronic Components In the Oil and Gas Industry Market face?

The Passive Electronic Components In the Oil and Gas Industry Market faces challenges such as the volatility of raw material prices and the stringent regulatory environment. These factors can impact production costs and the availability of components necessary for critical applications.

What opportunities exist in the Passive Electronic Components In the Oil and Gas Industry Market?

Opportunities in the Passive Electronic Components In the Oil and Gas Industry Market include the growing trend towards renewable energy integration and the development of smart technologies. These advancements create a demand for innovative passive components that can enhance system efficiency and reliability.

What trends are shaping the Passive Electronic Components In the Oil and Gas Industry Market?

Trends shaping the Passive Electronic Components In the Oil and Gas Industry Market include the increasing adoption of IoT technologies and the push for miniaturization of components. These trends are leading to the development of more compact and efficient electronic solutions tailored for the unique challenges of the oil and gas sector.

Passive Electronic Components In the Oil and Gas Industry Market

| Segmentation Details | Description |

|---|---|

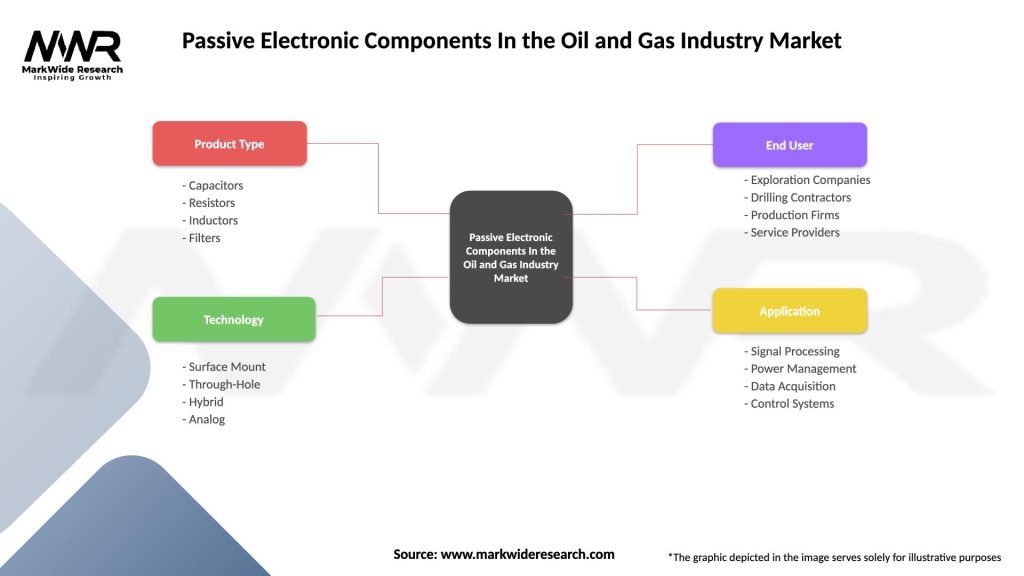

| Product Type | Capacitors, Resistors, Inductors, Filters |

| Technology | Surface Mount, Through-Hole, Hybrid, Analog |

| End User | Exploration Companies, Drilling Contractors, Production Firms, Service Providers |

| Application | Signal Processing, Power Management, Data Acquisition, Control Systems |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Passive Electronic Components In the Oil and Gas Industry Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA