444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

China’s power transistor market represents one of the most dynamic and rapidly evolving segments within the global semiconductor industry. The market has experienced remarkable transformation driven by the country’s aggressive push toward electrification, renewable energy adoption, and advanced manufacturing capabilities. Power transistors serve as critical components in power conversion, motor control, and energy management systems across diverse applications including electric vehicles, industrial automation, consumer electronics, and renewable energy infrastructure.

Market dynamics in China reflect the nation’s strategic emphasis on semiconductor self-sufficiency and technological independence. The domestic power transistor ecosystem has witnessed substantial investments in research and development, manufacturing capacity expansion, and supply chain localization. Growth projections indicate the market is expanding at a robust CAGR of 8.2%, significantly outpacing global averages due to strong domestic demand and government policy support.

Regional concentration remains heavily focused in key manufacturing hubs including Guangdong, Jiangsu, and Shanghai, where established semiconductor clusters provide comprehensive infrastructure and talent pools. The market benefits from vertical integration opportunities as Chinese companies increasingly control entire value chains from raw materials to finished products, enhancing cost competitiveness and supply chain resilience.

The China power transistor market refers to the comprehensive ecosystem encompassing the design, manufacturing, distribution, and application of power semiconductor devices specifically within Chinese territory. Power transistors are semiconductor devices that control and amplify electrical power, enabling efficient energy conversion and management across various electronic systems and industrial applications.

Market scope includes multiple transistor technologies such as MOSFETs, IGBTs, bipolar junction transistors, and emerging wide-bandgap semiconductors like silicon carbide and gallium nitride devices. These components serve essential functions in power supplies, motor drives, inverters, converters, and switching applications across automotive, industrial, telecommunications, and consumer electronics sectors.

Strategic significance extends beyond commercial considerations to encompass national security and technological sovereignty objectives. The market represents China’s efforts to reduce dependency on foreign semiconductor suppliers while building indigenous capabilities in critical power electronics technologies that underpin modern infrastructure and industrial competitiveness.

China’s power transistor market demonstrates exceptional growth momentum supported by multiple converging factors including electrification trends, industrial modernization, and strategic government initiatives. The market landscape features a dynamic mix of established international players and rapidly emerging domestic competitors, creating an increasingly competitive environment that drives innovation and cost optimization.

Key market drivers include the accelerating adoption of electric vehicles, which accounts for approximately 35% of total power transistor demand, alongside robust growth in renewable energy installations and industrial automation systems. Domestic manufacturing capabilities have expanded significantly, with Chinese companies now controlling over 42% of local market share compared to just 28% five years ago.

Technology evolution toward wide-bandgap semiconductors presents both opportunities and challenges, as Chinese manufacturers invest heavily in silicon carbide and gallium nitride technologies to compete with established global leaders. Supply chain localization efforts have intensified following recent geopolitical tensions, driving increased investment in domestic production capacity and materials sourcing.

Market outlook remains highly positive despite global economic uncertainties, supported by China’s continued commitment to green energy transition, smart manufacturing initiatives, and 5G infrastructure deployment. The convergence of these trends creates sustained demand for advanced power transistor solutions across multiple application segments.

Market segmentation reveals distinct growth patterns across different application areas and technology categories. The following insights highlight critical market dynamics:

Technology trends indicate accelerating migration toward wide-bandgap semiconductors, with silicon carbide devices gaining significant market traction in high-power applications while gallium nitride solutions penetrate consumer and telecommunications segments.

Electric vehicle proliferation stands as the primary catalyst driving China’s power transistor market expansion. The government’s ambitious electrification targets and substantial subsidies have created unprecedented demand for power electronics components. EV sales growth of over 120% year-over-year directly translates to increased requirements for motor controllers, onboard chargers, and DC-DC converters, all of which rely heavily on advanced power transistor technologies.

Industrial automation initiatives under the “Made in China 2025” strategy significantly boost power transistor consumption across manufacturing sectors. Smart factory implementations require sophisticated motor drives, power supplies, and control systems that depend on high-performance semiconductor solutions. Factory automation investments have increased by 67% annually, creating sustained demand for industrial-grade power transistors.

Renewable energy expansion represents another crucial growth driver as China pursues carbon neutrality objectives. Solar photovoltaic installations and wind power projects require extensive power conversion equipment, including inverters, converters, and grid-tie systems. Clean energy capacity additions continue growing at double-digit rates, necessitating reliable and efficient power transistor solutions.

5G infrastructure deployment creates specialized demand for RF power transistors and high-frequency switching devices. Base station installations across urban and rural areas require advanced power amplifiers and efficient power management systems. Telecommunications infrastructure spending remains robust, supporting continued market growth in this segment.

Technology gaps in advanced power transistor manufacturing continue to challenge Chinese companies, particularly in wide-bandgap semiconductor production. While domestic capabilities have improved significantly, performance disparities compared to leading international suppliers remain evident in high-end applications requiring superior efficiency, reliability, and thermal management characteristics.

Supply chain vulnerabilities persist despite localization efforts, as critical raw materials and specialized manufacturing equipment still depend heavily on imports. Material sourcing constraints and equipment access limitations can disrupt production schedules and limit capacity expansion plans, particularly during periods of heightened geopolitical tensions.

Intense price competition pressures profit margins across the market as both domestic and international suppliers compete aggressively for market share. Commoditization trends in standard power transistor categories force manufacturers to continuously reduce costs while maintaining quality standards, creating challenges for sustainable business models.

Regulatory uncertainties surrounding international trade policies and technology transfer restrictions create planning difficulties for companies with global operations. Export control measures and changing compliance requirements can limit access to advanced technologies and international markets, constraining growth opportunities for Chinese manufacturers.

Wide-bandgap semiconductor adoption presents substantial opportunities for Chinese manufacturers to establish competitive positions in emerging technology segments. Silicon carbide and gallium nitride devices offer superior performance characteristics that enable new applications and higher value propositions, particularly in electric vehicles, renewable energy, and high-frequency switching applications.

Export market expansion offers significant growth potential as Chinese power transistor manufacturers develop competitive products and establish international distribution networks. Belt and Road Initiative countries represent particularly attractive markets for infrastructure-related power electronics applications, while established markets offer opportunities for cost-competitive solutions.

Vertical integration strategies enable Chinese companies to capture additional value chain segments while improving cost competitiveness and supply chain control. Integrated device manufacturers can optimize designs for specific applications while reducing dependency on external suppliers for critical components and materials.

Emerging applications in areas such as wireless power transfer, electric aircraft, and energy storage systems create new market segments with less established competition. Innovation opportunities in these developing markets allow Chinese companies to compete on technology leadership rather than just cost advantages.

Competitive intensity continues escalating as both established international suppliers and emerging Chinese manufacturers vie for market leadership across different segments. Market consolidation trends are evident as larger companies acquire smaller specialized firms to expand technology portfolios and manufacturing capabilities, creating more formidable competitive entities.

Technology evolution cycles are accelerating, requiring continuous investment in research and development to maintain competitive positions. Product lifecycles have shortened significantly, particularly in consumer electronics applications where rapid innovation and cost reduction pressures demand frequent product updates and manufacturing process improvements.

Customer requirements are becoming increasingly sophisticated, with emphasis on system-level optimization rather than individual component performance. Application-specific solutions gain preference over generic products, driving manufacturers to develop closer partnerships with end-users and provide comprehensive technical support services.

Supply chain dynamics reflect ongoing efforts to balance cost optimization with supply security considerations. Dual sourcing strategies and regional supplier diversification have become standard practices as companies seek to mitigate risks while maintaining competitive cost structures in an increasingly complex global environment.

Primary research activities encompass comprehensive interviews with industry executives, technology experts, and key stakeholders across the power transistor value chain. Data collection methods include structured surveys, in-depth discussions with manufacturing leaders, and technical consultations with research institutions and universities specializing in semiconductor technologies.

Secondary research sources comprise industry publications, government statistics, patent databases, and financial reports from publicly traded companies operating in the Chinese power transistor market. Market intelligence is gathered from trade associations, industry conferences, and specialized semiconductor research organizations to ensure comprehensive coverage of market trends and developments.

Quantitative analysis techniques employ statistical modeling and forecasting methodologies to project market growth trajectories and segment performance. Data validation processes include cross-referencing multiple sources, expert review panels, and sensitivity analysis to ensure accuracy and reliability of market projections and insights.

Qualitative assessment frameworks evaluate competitive positioning, technology roadmaps, and strategic initiatives through systematic analysis of company capabilities, market positioning, and growth strategies. Market dynamics evaluation considers regulatory impacts, technological disruptions, and macroeconomic factors affecting industry development patterns.

Eastern China dominates the power transistor market landscape, accounting for approximately 58% of total market activity. The region benefits from established semiconductor manufacturing clusters in Shanghai, Jiangsu, and Zhejiang provinces, where comprehensive ecosystems support design, manufacturing, and testing activities. Yangtze River Delta integration initiatives further strengthen regional competitiveness through improved infrastructure and resource sharing.

Southern China represents the second-largest regional market with 26% market share, driven primarily by Guangdong province’s electronics manufacturing base and proximity to Hong Kong’s financial and logistics networks. Pearl River Delta companies benefit from established supply chains, skilled workforce availability, and strong connections to international markets through established trading relationships.

Northern China contributes 12% of market activity, with Beijing and Tianjin serving as important research and development centers while supporting government and military applications. Technology innovation remains the region’s primary strength, with numerous universities and research institutes driving advanced semiconductor development programs.

Western and Central China account for the remaining 4% of market share but demonstrate rapid growth potential as government policies encourage inland development and manufacturing relocation. Emerging clusters in cities like Chengdu, Xi’an, and Wuhan offer cost advantages and growing technical capabilities that attract investment from established semiconductor companies.

Market leadership remains contested between international semiconductor giants and rapidly advancing Chinese manufacturers. The competitive environment reflects ongoing technology transfer, capacity building, and strategic positioning efforts across different market segments and application areas.

Competitive strategies increasingly focus on technology differentiation, application-specific solutions, and comprehensive customer support services rather than purely cost-based competition. Strategic partnerships and joint ventures enable technology transfer and market access while sharing development risks and costs.

By Technology:

By Application:

By Power Rating:

MOSFET segment maintains market leadership through widespread adoption across diverse applications requiring efficient switching performance. Technology advances in super junction and trench gate structures continue improving performance while reducing costs, supporting market expansion in both consumer and industrial applications. Chinese manufacturers have achieved significant competitiveness in standard MOSFET categories while investing in advanced technologies.

IGBT category demonstrates robust growth driven by electric vehicle adoption and industrial automation requirements. High-power applications benefit from IGBT’s superior performance characteristics in motor control and power conversion systems. Domestic production capabilities have expanded substantially, with Chinese companies now competing effectively in medium-power IGBT segments.

Wide-bandgap semiconductors represent the fastest-growing category despite smaller absolute volumes. Silicon carbide devices gain traction in electric vehicle onboard chargers and renewable energy inverters where efficiency advantages justify premium pricing. Gallium nitride solutions penetrate consumer electronics and telecommunications applications requiring high-frequency operation and compact form factors.

Automotive applications drive the highest growth rates across all transistor categories as electrification trends accelerate. Electric vehicle requirements span the entire power range from low-power auxiliary systems to high-power traction inverters, creating opportunities for diverse transistor technologies and suppliers.

Manufacturers benefit from China’s large domestic market providing scale advantages and opportunities for cost optimization through high-volume production. Local manufacturing presence enables closer customer relationships, faster response times, and reduced logistics costs while supporting supply chain localization objectives.

Technology companies gain access to China’s extensive research and development ecosystem including universities, research institutes, and government funding programs. Innovation partnerships facilitate technology transfer and collaborative development projects that accelerate product development cycles and market introduction timelines.

End-users benefit from increased supplier diversity, competitive pricing, and improved product availability through expanded local manufacturing capacity. Application-specific solutions developed for Chinese market requirements often provide superior performance and cost-effectiveness compared to generic international products.

Investors find attractive opportunities in China’s power transistor market through exposure to high-growth segments including electric vehicles, renewable energy, and industrial automation. Government policy support and strategic industry development initiatives provide additional confidence for long-term investment commitments.

Supply chain partners benefit from vertical integration opportunities and expanded business relationships as the market ecosystem develops greater depth and sophistication. Collaborative partnerships enable shared technology development, risk mitigation, and market expansion strategies.

Strengths:

Weaknesses:

Opportunities:

Threats:

Electrification acceleration across multiple industries drives fundamental shifts in power transistor requirements and applications. Electric vehicle adoption continues exceeding projections, creating sustained demand for high-performance power electronics while pushing technology boundaries for efficiency, reliability, and thermal management capabilities.

Wide-bandgap semiconductor migration gains momentum as performance advantages become more compelling and costs decrease through improved manufacturing processes. Silicon carbide adoption expands beyond premium applications into mainstream industrial and automotive segments, while gallium nitride penetration accelerates in consumer electronics and telecommunications equipment.

System-level optimization trends emphasize integrated solutions rather than discrete components, driving closer collaboration between semiconductor suppliers and equipment manufacturers. Application-specific designs become increasingly important as customers seek optimized performance for specific use cases rather than generic solutions.

Supply chain localization efforts intensify as companies seek greater control over critical components and materials. Domestic sourcing preferences create opportunities for Chinese suppliers while challenging international companies to establish local manufacturing presence and partnerships.

Sustainability considerations influence product development and manufacturing processes as environmental regulations tighten and customer preferences shift toward eco-friendly solutions. Energy efficiency improvements become key differentiators across all application segments, driving continuous innovation in transistor technologies and system designs.

Manufacturing capacity expansions continue across China as both domestic and international companies invest in production facilities to meet growing demand. MarkWide Research indicates that fab capacity additions have increased by 45% annually over the past three years, with particular emphasis on wide-bandgap semiconductor production capabilities.

Strategic partnerships and joint ventures proliferate as companies seek to combine complementary strengths and share development risks. Technology licensing agreements enable faster market entry and capability building while providing established companies with access to Chinese market opportunities and manufacturing cost advantages.

Research and development investments reach record levels as companies compete to develop next-generation technologies and maintain competitive positions. Government funding programs support advanced semiconductor development while private companies increase R&D spending to accelerate innovation cycles and product differentiation.

Acquisition activities reshape the competitive landscape as larger companies acquire specialized technology firms and manufacturing assets. Market consolidation creates more capable competitors while providing acquired companies with resources for accelerated growth and technology development.

Regulatory developments including environmental standards, safety requirements, and trade policies continue influencing market dynamics and competitive positioning. Policy changes create both challenges and opportunities for market participants depending on their strategic positioning and operational capabilities.

Technology investment priorities should focus on wide-bandgap semiconductors and advanced packaging technologies to maintain competitive relevance in evolving market segments. Companies must balance short-term profitability with long-term technology development to avoid obsolescence in rapidly changing market conditions.

Market positioning strategies should emphasize application-specific solutions and system-level optimization rather than generic component offerings. Customer partnerships become increasingly important for understanding evolving requirements and developing differentiated solutions that command premium pricing.

Supply chain diversification remains critical for managing risks associated with geopolitical tensions and material availability constraints. Dual sourcing strategies and regional supplier development help ensure business continuity while maintaining cost competitiveness in challenging market conditions.

International expansion opportunities should be evaluated carefully considering trade policy uncertainties and competitive dynamics in target markets. Export strategies must account for quality perceptions, certification requirements, and established competitor relationships while leveraging cost advantages and emerging technology capabilities.

Talent development investments are essential for supporting technology advancement and operational excellence as the industry becomes increasingly sophisticated. Skills shortages in advanced semiconductor design and manufacturing require proactive workforce development and retention strategies.

Market growth prospects remain highly positive supported by multiple structural trends including electrification, digitalization, and energy efficiency requirements. Long-term projections indicate sustained expansion at growth rates exceeding 7% annually through the next decade, driven primarily by electric vehicle adoption and industrial automation initiatives.

Technology evolution toward wide-bandgap semiconductors will accelerate as manufacturing costs decrease and performance advantages become more compelling across broader application ranges. Silicon carbide and gallium nitride devices are expected to capture over 25% market share within five years, fundamentally reshaping competitive dynamics and value propositions.

Competitive landscape transformation will continue as Chinese manufacturers strengthen technology capabilities and international companies establish deeper local presence. Market leadership positions may shift significantly as technology gaps narrow and domestic suppliers gain credibility in premium applications previously dominated by international players.

Application diversification will create new growth opportunities beyond traditional segments as emerging technologies like wireless power transfer, electric aircraft, and advanced energy storage systems mature. Innovation cycles are expected to accelerate, requiring continuous adaptation and investment from all market participants.

Regulatory environment evolution will continue influencing market development through environmental standards, safety requirements, and trade policies. MWR analysis suggests that regulatory compliance costs will increase but create opportunities for companies with advanced capabilities and comprehensive quality systems.

China’s power transistor market represents a dynamic and rapidly evolving ecosystem characterized by strong growth fundamentals, intense competition, and continuous technological advancement. The market benefits from multiple structural drivers including electric vehicle adoption, industrial automation, renewable energy expansion, and government policy support that create sustained demand across diverse application segments.

Competitive dynamics reflect the ongoing transformation as domestic manufacturers strengthen capabilities while international companies adapt strategies for the Chinese market environment. Technology evolution toward wide-bandgap semiconductors presents both opportunities and challenges, requiring significant investments in research, development, and manufacturing capabilities.

Future success in this market will depend on companies’ ability to balance cost competitiveness with technology leadership while navigating complex supply chain, regulatory, and geopolitical considerations. Strategic positioning must emphasize application-specific solutions, customer partnerships, and continuous innovation to maintain competitive relevance in this rapidly changing industry landscape.

What is Power Transistor?

Power transistors are semiconductor devices used to amplify or switch electronic signals and electrical power. They are essential components in various applications, including power supplies, motor drives, and audio amplifiers.

What are the key players in the China Power Transistor Market?

Key players in the China Power Transistor Market include companies like Infineon Technologies, ON Semiconductor, STMicroelectronics, and Nexperia, among others.

What are the main drivers of growth in the China Power Transistor Market?

The growth of the China Power Transistor Market is driven by the increasing demand for energy-efficient devices, the expansion of renewable energy sources, and the rising adoption of electric vehicles.

What challenges does the China Power Transistor Market face?

Challenges in the China Power Transistor Market include intense competition among manufacturers, rapid technological advancements, and supply chain disruptions that can affect production and delivery.

What opportunities exist in the China Power Transistor Market?

Opportunities in the China Power Transistor Market include the growing demand for smart grid technologies, advancements in electric vehicle infrastructure, and the increasing use of power transistors in consumer electronics.

What trends are shaping the China Power Transistor Market?

Trends in the China Power Transistor Market include the shift towards wide bandgap semiconductors, the integration of power transistors in IoT devices, and the focus on miniaturization and efficiency improvements in electronic components.

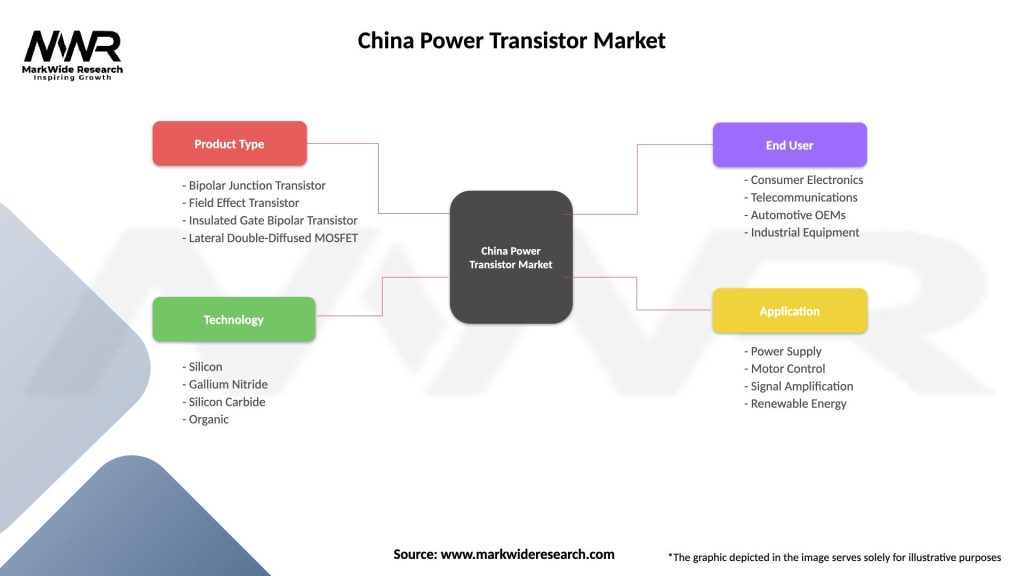

China Power Transistor Market

| Segmentation Details | Description |

|---|---|

| Product Type | Bipolar Junction Transistor, Field Effect Transistor, Insulated Gate Bipolar Transistor, Lateral Double-Diffused MOSFET |

| Technology | Silicon, Gallium Nitride, Silicon Carbide, Organic |

| End User | Consumer Electronics, Telecommunications, Automotive OEMs, Industrial Equipment |

| Application | Power Supply, Motor Control, Signal Amplification, Renewable Energy |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the China Power Transistor Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.