444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The US digital lending market represents a transformative shift in the financial services landscape, fundamentally changing how consumers and businesses access credit. This rapidly evolving sector encompasses online lending platforms, peer-to-peer lending networks, and technology-driven financial institutions that leverage advanced algorithms and data analytics to streamline the lending process. Digital lending platforms have revolutionized traditional banking by offering faster approval times, reduced paperwork, and enhanced accessibility for borrowers across diverse demographic segments.

Market dynamics indicate substantial growth momentum driven by increasing consumer demand for convenient financial services and the widespread adoption of mobile banking technologies. The sector has experienced remarkable expansion, with digital loan originations growing at approximately 15.2% annually over recent years. Fintech companies and established financial institutions are increasingly investing in digital infrastructure to capture market share in this competitive landscape.

Technological innovation serves as the primary catalyst for market expansion, with artificial intelligence, machine learning, and blockchain technologies enabling more sophisticated risk assessment models and automated underwriting processes. The integration of alternative data sources has expanded credit access to previously underserved populations, while regulatory frameworks continue evolving to accommodate these innovative lending models.

The US digital lending market refers to the comprehensive ecosystem of technology-enabled financial services that facilitate loan origination, processing, and servicing through digital channels. This market encompasses various lending models including peer-to-peer platforms, online direct lenders, marketplace lending, and digital-first banking institutions that utilize advanced technology to deliver credit products to consumers and businesses.

Digital lending platforms differentiate themselves from traditional banking through streamlined application processes, rapid decision-making capabilities, and enhanced user experiences delivered through web and mobile applications. These platforms leverage big data analytics, artificial intelligence, and automated underwriting systems to assess creditworthiness and determine loan terms more efficiently than conventional lending institutions.

The market includes various loan categories such as personal loans, small business financing, student loans, auto loans, and mortgage products delivered through digital channels. Alternative lending models have emerged to serve specific market segments, including borrowers with limited credit history or those seeking faster approval processes than traditional banks typically provide.

Market leadership in the US digital lending sector is characterized by intense competition between established fintech pioneers and traditional financial institutions adapting to digital transformation. The landscape features diverse players ranging from specialized online lenders to comprehensive financial technology platforms offering multiple credit products through integrated digital ecosystems.

Consumer adoption rates have accelerated significantly, with approximately 42% of borrowers now considering digital-first lenders as their primary option for personal credit needs. This shift reflects changing consumer preferences toward convenience, transparency, and speed in financial transactions. Mobile lending applications have become increasingly sophisticated, offering features such as instant pre-qualification, document upload capabilities, and real-time loan tracking.

Regulatory developments continue shaping market dynamics as federal and state authorities work to establish comprehensive frameworks governing digital lending practices. The sector benefits from supportive regulatory trends that encourage innovation while maintaining consumer protection standards. Risk management technologies have evolved to address the unique challenges of digital lending, including fraud prevention, identity verification, and automated compliance monitoring systems.

Technological advancement drives competitive differentiation in the digital lending market, with leading platforms investing heavily in artificial intelligence and machine learning capabilities. The following key insights characterize current market dynamics:

Consumer demand for convenient and accessible financial services represents the primary driver of digital lending market expansion. Modern borrowers increasingly expect streamlined application processes, transparent pricing, and rapid funding capabilities that traditional banking institutions often struggle to deliver efficiently. Digital-native consumers particularly favor online lending platforms that offer intuitive user interfaces and mobile-responsive designs.

Technological infrastructure improvements have enabled sophisticated risk assessment models that leverage alternative data sources beyond traditional credit scores. These innovations allow lenders to serve previously underbanked populations while maintaining acceptable risk profiles. Cloud computing platforms provide scalable infrastructure that supports rapid business growth and geographic expansion for digital lending companies.

Competitive pressure from fintech startups has forced traditional financial institutions to accelerate their digital transformation initiatives. Banks are increasingly partnering with technology providers or developing internal capabilities to compete effectively in the digital lending space. Regulatory support for financial innovation has created favorable conditions for new market entrants while encouraging established institutions to modernize their lending operations.

Economic factors including low interest rates and increased demand for credit have created favorable market conditions for lending growth. Small business financing needs, particularly following economic disruptions, have driven demand for alternative lending solutions that offer faster approval and funding processes than traditional bank loans.

Regulatory uncertainty poses significant challenges for digital lending platforms as federal and state authorities continue developing comprehensive oversight frameworks. Compliance costs and the complexity of navigating multiple regulatory jurisdictions can strain resources, particularly for smaller fintech companies seeking to scale their operations across different states.

Credit risk management remains a fundamental challenge as digital lenders must balance accessibility with prudent underwriting standards. The reliance on automated decision-making systems can lead to unexpected losses if risk models fail to account for changing economic conditions or borrower behavior patterns. Data quality issues and the integration of alternative credit data sources present ongoing challenges for accurate risk assessment.

Cybersecurity threats represent critical concerns for digital lending platforms that handle sensitive financial and personal information. The increasing sophistication of cyber attacks requires continuous investment in security infrastructure and monitoring systems. Data privacy regulations add complexity to customer data management and require robust compliance frameworks.

Market saturation in certain lending segments has intensified competition and compressed profit margins. The proliferation of digital lending platforms has created challenges in customer acquisition and retention, leading to increased marketing costs and the need for differentiated value propositions. Economic volatility can rapidly impact loan performance and funding availability for digital lenders.

Underserved market segments present substantial growth opportunities for digital lending platforms willing to develop specialized products and risk assessment models. Small businesses, gig economy workers, and consumers with limited credit history represent significant addressable markets that traditional lenders often overlook. Embedded finance solutions offer opportunities to integrate lending capabilities directly into e-commerce platforms, business software, and mobile applications.

Geographic expansion opportunities exist as digital lending platforms can leverage their technology infrastructure to enter new markets with relatively low incremental costs. Rural and suburban markets often lack adequate access to traditional banking services, creating opportunities for digital-first lenders to capture market share. International expansion represents longer-term growth potential as regulatory frameworks mature in global markets.

Product diversification enables digital lending platforms to expand beyond their initial focus areas into complementary financial services. Opportunities include wealth management, insurance products, and business banking services that leverage existing customer relationships and data insights. Partnership strategies with traditional financial institutions can provide access to larger customer bases and regulatory expertise.

Technological innovation continues creating new opportunities for market differentiation and operational efficiency. Artificial intelligence applications in fraud detection, customer service, and personalized product recommendations offer competitive advantages. Blockchain technology presents opportunities for enhanced security, transparency, and automated contract execution in lending operations.

Competitive intensity in the US digital lending market continues escalating as both fintech startups and traditional financial institutions vie for market share. The sector demonstrates classic network effects where platforms with larger customer bases can achieve better risk diversification and operational efficiencies. Customer acquisition costs have increased significantly as marketing channels become more competitive and expensive.

Funding dynamics play a crucial role in digital lending market evolution, with platforms requiring access to capital markets or institutional investors to support loan origination. Interest rate fluctuations directly impact profitability and lending capacity for many digital platforms. Institutional partnerships with banks, credit unions, and investment funds provide stable funding sources while enabling regulatory compliance through established banking relationships.

Technology evolution drives continuous innovation in lending processes, with approximately 78% of digital lenders investing in artificial intelligence capabilities to improve underwriting accuracy and operational efficiency. Data analytics sophistication enables more precise risk pricing and personalized customer experiences, creating competitive advantages for technology-forward platforms.

Regulatory adaptation influences market structure as authorities balance innovation encouragement with consumer protection requirements. State-level licensing requirements and federal oversight create compliance complexities that favor larger, well-capitalized platforms. Open banking initiatives may reshape competitive dynamics by enabling greater data sharing and interoperability between financial service providers.

Comprehensive market analysis for the US digital lending sector employs multiple research methodologies to ensure accuracy and depth of insights. Primary research includes extensive interviews with industry executives, technology leaders, and regulatory experts to understand current market dynamics and future trends. Survey data from borrowers and lenders provides quantitative insights into user behavior, satisfaction levels, and adoption patterns across different demographic segments.

Secondary research encompasses analysis of public company financial reports, regulatory filings, and industry publications to track market performance and competitive positioning. MarkWide Research utilizes proprietary databases and analytical frameworks to identify emerging trends and quantify market opportunities across various lending categories and geographic regions.

Data validation processes include cross-referencing multiple sources and conducting expert interviews to verify key findings and assumptions. Quantitative analysis incorporates statistical modeling to project market trends and validate growth projections. Regulatory analysis examines current and proposed legislation that may impact market development and competitive dynamics.

Technology assessment evaluates the impact of emerging technologies on lending processes and market structure. This includes analysis of artificial intelligence applications, blockchain implementations, and mobile platform capabilities. Competitive intelligence gathering provides insights into strategic initiatives, partnership developments, and product innovations across the digital lending ecosystem.

Geographic distribution of digital lending activity across the United States reveals significant variations in market penetration and growth patterns. California leads in digital lending adoption with approximately 23% market share, driven by the concentration of technology companies and venture capital funding in Silicon Valley. The state’s regulatory environment and consumer acceptance of financial technology innovations create favorable conditions for digital lending growth.

New York represents the second-largest regional market, accounting for roughly 18% of digital lending activity. The state’s dense population, high income levels, and sophisticated financial services infrastructure support robust demand for alternative lending solutions. Regulatory frameworks in New York have evolved to accommodate fintech innovation while maintaining consumer protection standards.

Texas and Florida demonstrate strong growth potential with rapidly expanding populations and increasing small business formation rates. These states collectively represent approximately 22% of the digital lending market, with particular strength in small business and real estate lending segments. Regulatory environments in these states generally support financial innovation and entrepreneurship.

Midwest and Southeast regions show increasing adoption of digital lending platforms, particularly in underbanked rural and suburban areas where traditional banking services may be limited. These markets present opportunities for digital lenders to capture market share from traditional institutions. Regional banks in these areas are increasingly partnering with fintech companies to enhance their digital capabilities and compete more effectively.

Market leadership in the US digital lending sector is distributed among several categories of players, each with distinct competitive advantages and strategic approaches. The competitive landscape includes established fintech pioneers, traditional banks with digital initiatives, and specialized lending platforms focused on specific market segments.

Strategic differentiation among competitors focuses on technology capabilities, customer experience, risk management sophistication, and regulatory compliance. Many platforms are expanding beyond their original lending focus to offer comprehensive financial services ecosystems.

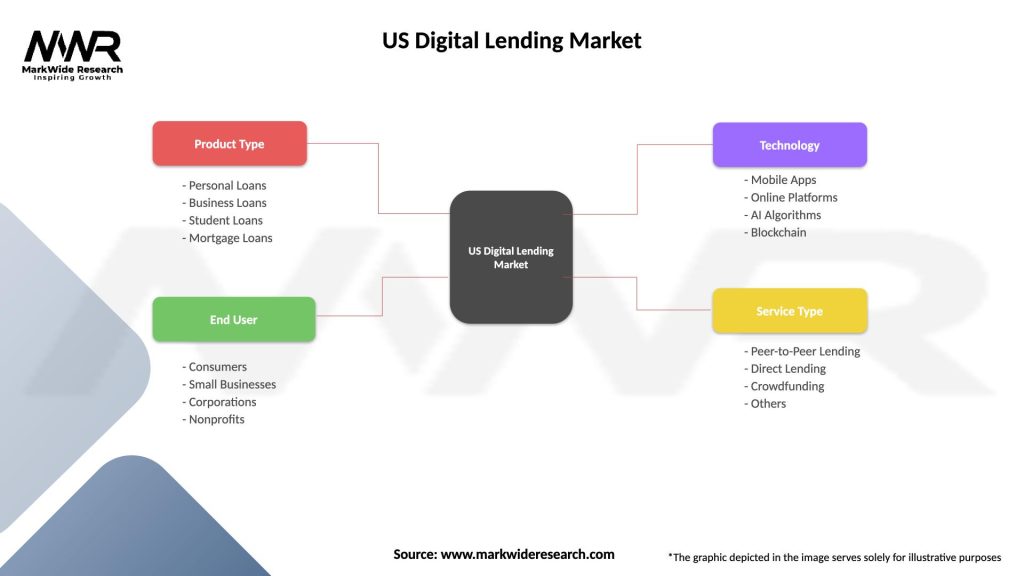

Market segmentation in the US digital lending sector reflects diverse borrower needs, loan purposes, and risk profiles. Understanding these segments enables lenders to develop targeted products and marketing strategies that address specific customer requirements and market opportunities.

By Loan Type:

By Borrower Segment:

By Platform Type:

Personal lending represents the largest segment within the digital lending market, driven by consumer demand for debt consolidation and major purchase financing. This category benefits from standardized underwriting processes and relatively predictable risk profiles. Competition intensity remains high as multiple platforms target similar borrower demographics with comparable product offerings.

Small business lending demonstrates strong growth potential as traditional banks often struggle to serve this market efficiently. Digital platforms leverage alternative data sources and automated underwriting to serve businesses that may not qualify for conventional bank loans. Revenue-based financing and merchant cash advance products have gained popularity among businesses seeking flexible repayment terms.

Student loan refinancing has emerged as a significant category, particularly as borrowers seek to reduce interest rates and modify repayment terms. Digital platforms offer streamlined application processes and competitive rates for qualified borrowers. Regulatory changes in federal student loan programs may impact this segment’s growth trajectory.

Mortgage lending through digital channels has experienced rapid adoption, accelerated by pandemic-related changes in home buying patterns. Online mortgage platforms offer faster processing times and enhanced customer experiences compared to traditional mortgage brokers. Integration capabilities with real estate platforms and mobile applications provide competitive advantages.

Auto lending through digital platforms continues expanding as consumers increasingly research and apply for vehicle financing online. Partnerships with automotive dealers and direct-to-consumer models both show growth potential. Electric vehicle financing represents an emerging opportunity as the automotive market transitions toward sustainable transportation.

Borrower advantages in the digital lending ecosystem include significantly improved accessibility, convenience, and transparency compared to traditional banking relationships. Digital platforms typically offer faster application processing, with many providing instant pre-qualification and same-day funding capabilities. Competitive pricing often results from reduced operational overhead and automated processing systems.

Lender benefits include enhanced operational efficiency through automated underwriting and loan servicing systems. Digital platforms can serve larger customer bases with relatively small staff requirements compared to traditional branch-based banking. Data analytics capabilities enable more sophisticated risk assessment and personalized product offerings that improve customer satisfaction and retention rates.

Investor opportunities in digital lending platforms provide access to diversified loan portfolios with attractive risk-adjusted returns. Institutional investors can participate in lending markets that were previously accessible only to traditional banks. Technology platforms offer transparency and real-time portfolio monitoring capabilities that enhance investment decision-making.

Economic benefits include increased credit access for underserved populations and small businesses that drive economic growth and job creation. Digital lending platforms can serve rural and suburban markets where traditional banking services may be limited. Financial inclusion improvements result from alternative credit scoring models that consider non-traditional data sources.

Regulatory advantages include enhanced monitoring and compliance capabilities through automated systems that track lending activities and ensure adherence to consumer protection requirements. Digital platforms can implement policy changes more rapidly than traditional institutions. Data availability supports regulatory oversight and market stability monitoring efforts.

Strengths:

Weaknesses:

Opportunities:

Threats:

Artificial intelligence integration represents the most significant technological trend reshaping digital lending operations. Machine learning algorithms increasingly sophisticated in analyzing borrower behavior patterns, predicting default risks, and personalizing loan offers. Natural language processing enhances customer service capabilities through chatbots and automated document analysis systems.

Embedded finance solutions are gaining momentum as lending capabilities become integrated directly into e-commerce platforms, business software, and mobile applications. This trend enables seamless credit access at the point of sale or within existing customer workflows. API-first architectures facilitate these integrations while maintaining security and compliance standards.

Alternative credit scoring continues evolving with the incorporation of non-traditional data sources including social media activity, utility payments, and mobile phone usage patterns. These models enable credit access for borrowers with limited traditional credit history. Real-time credit decisions based on comprehensive data analysis are becoming standard expectations among consumers.

Regulatory technology adoption helps digital lenders manage compliance requirements more efficiently through automated monitoring and reporting systems. RegTech solutions enable real-time compliance checking and reduce the risk of regulatory violations. MWR analysis indicates that approximately 67% of digital lenders are investing in regulatory technology capabilities.

Sustainability focus is emerging as lenders develop products supporting environmental and social objectives. Green lending products for energy-efficient home improvements and electric vehicle purchases are gaining popularity. ESG considerations increasingly influence lending decisions and investor preferences in the digital lending sector.

Strategic partnerships between traditional banks and fintech companies have accelerated as established institutions seek to enhance their digital capabilities while fintech platforms gain access to regulatory expertise and funding sources. These collaborations often involve technology licensing agreements or joint venture structures that combine complementary strengths.

Acquisition activity in the digital lending sector reflects market consolidation trends as larger platforms acquire specialized competitors or technology providers. Notable transactions include traditional banks purchasing fintech lending platforms to accelerate their digital transformation initiatives. Private equity investment continues flowing into promising digital lending companies with proven business models.

Regulatory developments include the implementation of new oversight frameworks for digital lending activities and consumer protection measures. Federal agencies are developing comprehensive guidelines for fintech lending while state regulators adapt licensing requirements. Open banking initiatives may reshape competitive dynamics by enabling greater data sharing between financial service providers.

Technology innovations include the deployment of blockchain technology for loan documentation and smart contract execution. Biometric authentication systems enhance security while improving user experience. Cloud infrastructure investments enable scalable operations and enhanced data analytics capabilities across digital lending platforms.

Product innovations reflect evolving consumer needs and market opportunities. Income-share agreements for education financing, revenue-based lending for businesses, and flexible repayment options demonstrate industry adaptation to diverse borrower requirements. Cryptocurrency lending represents an emerging category as digital asset adoption increases.

Technology investment should remain a top priority for digital lending platforms seeking to maintain competitive advantages. Companies should focus on artificial intelligence capabilities, cybersecurity infrastructure, and mobile platform optimization to meet evolving customer expectations. Data analytics sophistication will increasingly determine success in risk assessment and customer acquisition efficiency.

Regulatory compliance capabilities require continuous attention as oversight frameworks evolve and expand. Digital lenders should invest in regulatory technology solutions and maintain strong legal expertise to navigate complex compliance requirements. Proactive engagement with regulatory authorities can help shape policy development and ensure business model sustainability.

Partnership strategies offer opportunities for growth and risk mitigation through collaborations with traditional financial institutions, technology providers, and distribution partners. Strategic alliances can provide access to new customer segments, funding sources, and regulatory expertise. Embedded finance partnerships represent particularly attractive opportunities for market expansion.

Market diversification across loan types, borrower segments, and geographic regions can reduce concentration risks and capture growth opportunities. Companies should carefully evaluate expansion strategies based on their core competencies and available resources. International expansion may offer long-term growth potential as global regulatory frameworks mature.

Customer experience optimization remains critical for differentiation in an increasingly competitive market. Digital lenders should focus on streamlining application processes, improving transparency, and enhancing customer service capabilities. Personalization technologies can improve customer satisfaction and retention rates while supporting premium pricing strategies.

Market evolution in the US digital lending sector points toward continued growth and innovation over the next decade. MarkWide Research projects that digital lending adoption will expand significantly as younger demographics become primary borrowers and technology capabilities continue advancing. The integration of artificial intelligence and machine learning will enable more sophisticated risk assessment and personalized lending experiences.

Regulatory maturation is expected to provide greater clarity and stability for digital lending operations while maintaining appropriate consumer protection standards. Federal and state authorities will likely develop comprehensive frameworks that balance innovation encouragement with prudent oversight. Regulatory harmonization across states may reduce compliance complexity and enable more efficient market operations.

Technology convergence will blur traditional boundaries between lending, banking, and financial services as platforms expand their product offerings and capabilities. Embedded finance solutions will become increasingly prevalent, with lending capabilities integrated into diverse business and consumer applications. Blockchain technology may revolutionize loan documentation and servicing processes.

Market consolidation trends are likely to continue as successful platforms acquire competitors and traditional banks purchase fintech companies to accelerate digital transformation. This consolidation may result in fewer but larger digital lending platforms with comprehensive service offerings. Niche specialization will remain viable for companies focusing on specific borrower segments or loan types.

Global expansion opportunities will emerge as international regulatory frameworks mature and consumer acceptance of digital financial services increases worldwide. US digital lending companies with proven business models and technology capabilities are well-positioned to capture international market opportunities. Cross-border lending may become feasible as regulatory cooperation increases between countries.

The US digital lending market represents a dynamic and rapidly evolving sector that has fundamentally transformed how consumers and businesses access credit. Through technological innovation, enhanced customer experiences, and improved operational efficiency, digital lending platforms have captured significant market share while expanding credit access to previously underserved populations. The sector’s growth trajectory reflects broader trends toward digitalization in financial services and changing consumer preferences for convenient, transparent lending solutions.

Competitive dynamics continue intensifying as both fintech startups and traditional financial institutions invest heavily in digital capabilities and customer acquisition. Success in this market requires continuous innovation, regulatory compliance expertise, and the ability to adapt quickly to changing market conditions. Technology leadership in areas such as artificial intelligence, data analytics, and mobile platform optimization will increasingly determine competitive positioning and market share.

Future prospects for the digital lending market remain positive despite challenges related to regulatory complexity, credit risk management, and competitive intensity. The ongoing digital transformation of financial services, combined with evolving consumer expectations and technological capabilities, supports continued growth and innovation. Strategic partnerships, market diversification, and international expansion opportunities provide multiple pathways for sustained development in this transformative sector of the financial services industry.

What is Digital Lending?

Digital lending refers to the process of providing loans through online platforms, utilizing technology to streamline the application and approval process. This includes personal loans, business loans, and peer-to-peer lending, among others.

What are the key players in the US Digital Lending Market?

Key players in the US Digital Lending Market include companies like LendingClub, SoFi, and Upstart, which offer various loan products and services. These companies leverage technology to enhance user experience and improve lending efficiency, among others.

What are the main drivers of growth in the US Digital Lending Market?

The main drivers of growth in the US Digital Lending Market include the increasing adoption of mobile banking, the demand for faster loan processing, and the rise of alternative credit scoring models. Additionally, consumer preferences for online services are contributing to market expansion.

What challenges does the US Digital Lending Market face?

The US Digital Lending Market faces challenges such as regulatory compliance, data security concerns, and competition from traditional banks. These factors can impact the operational efficiency and customer trust in digital lending platforms.

What opportunities exist in the US Digital Lending Market?

Opportunities in the US Digital Lending Market include the potential for expanding into underserved demographics, the integration of artificial intelligence for better risk assessment, and the development of new financial products tailored to consumer needs. These factors can drive innovation and growth.

What trends are shaping the US Digital Lending Market?

Trends shaping the US Digital Lending Market include the rise of embedded finance, increased use of blockchain technology for secure transactions, and a focus on personalized lending experiences. These trends are influencing how consumers interact with lending services.

US Digital Lending Market

| Segmentation Details | Description |

|---|---|

| Product Type | Personal Loans, Business Loans, Student Loans, Mortgage Loans |

| End User | Consumers, Small Businesses, Corporations, Nonprofits |

| Technology | Mobile Apps, Online Platforms, AI Algorithms, Blockchain |

| Service Type | Peer-to-Peer Lending, Direct Lending, Crowdfunding, Others |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the US Digital Lending Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.