444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Estonia freight market represents a dynamic and strategically positioned logistics hub within the Baltic region, serving as a crucial gateway between Western Europe and Eastern markets. Estonia’s freight sector has experienced remarkable transformation over the past decade, driven by digital innovation, strategic geographic positioning, and robust infrastructure development. The market encompasses various transportation modes including road freight, rail transport, maritime shipping, and air cargo services, each contributing to the country’s comprehensive logistics ecosystem.

Market growth in Estonia’s freight sector has been consistently strong, with the industry experiencing a compound annual growth rate of 6.2% over recent years. This expansion reflects Estonia’s emergence as a key logistics center, benefiting from its membership in the European Union, advanced digital infrastructure, and strategic location along major trade routes connecting Scandinavia, Russia, and Central Europe. The country’s Port of Tallinn and other maritime facilities handle approximately 78% of regional cargo traffic, establishing Estonia as a dominant force in Baltic Sea logistics operations.

Digital transformation has become a defining characteristic of Estonia’s freight market, with the country leading European initiatives in e-logistics, automated customs processing, and smart transportation systems. Estonian freight companies have achieved 85% digitalization rates in core operations, significantly higher than the European average, contributing to enhanced efficiency and reduced operational costs across the supply chain network.

The Estonia freight market refers to the comprehensive ecosystem of transportation, logistics, and cargo handling services operating within Estonia’s borders and connecting to international trade networks. This market encompasses all commercial activities related to the movement of goods, including domestic distribution, international shipping, warehousing, and value-added logistics services that facilitate trade between businesses and consumers across multiple geographic regions.

Freight operations in Estonia include multiple transportation modalities working in integrated fashion to provide seamless cargo movement solutions. The market covers road transport companies, railway freight services, maritime shipping operations, air cargo facilities, and specialized logistics providers offering warehousing, distribution, and supply chain management services to domestic and international clients.

Estonia’s freight market stands as one of Europe’s most technologically advanced and efficiently operated logistics sectors, characterized by strong growth momentum and strategic positioning within global supply chains. The market has demonstrated resilience and adaptability, particularly during recent global disruptions, maintaining consistent service levels while expanding capacity and capabilities across all transportation modes.

Key performance indicators reveal the market’s robust health, with freight volumes increasing steadily and operational efficiency metrics exceeding regional benchmarks. Estonian freight companies have successfully leveraged the country’s digital infrastructure advantages, achieving 92% customer satisfaction rates through innovative service delivery models and transparent tracking systems that provide real-time visibility throughout the logistics process.

Strategic investments in infrastructure modernization, technology adoption, and capacity expansion have positioned Estonia’s freight market for continued growth. The sector benefits from government support for logistics development, EU funding for transportation infrastructure projects, and private sector investments in automation and digitalization initiatives that enhance competitiveness in international markets.

Market dynamics in Estonia’s freight sector reveal several critical insights that define current operations and future development trajectories:

Economic growth across the Baltic region serves as a primary driver for Estonia’s freight market expansion, with increasing trade volumes requiring enhanced logistics capabilities and capacity. Estonia’s membership in the European Union facilitates seamless cross-border operations, while the country’s stable political environment and business-friendly policies attract international logistics investments and partnerships.

Digital infrastructure excellence provides significant competitive advantages, enabling Estonian freight companies to offer superior service levels through advanced tracking, automated processing, and real-time communication systems. The country’s leadership in e-governance and digital services creates operational efficiencies that reduce costs and improve customer satisfaction across all freight market segments.

Infrastructure development continues driving market growth through strategic investments in port facilities, rail networks, and road systems that enhance capacity and connectivity. The Rail Baltica project represents a transformative infrastructure initiative that will significantly expand Estonia’s freight handling capabilities and strengthen connections to European markets.

E-commerce expansion generates increasing demand for last-mile delivery services and specialized logistics solutions, with online retail growth creating new opportunities for freight companies to develop innovative service offerings. Consumer expectations for fast, reliable delivery drive investments in distribution networks and technology systems that support efficient order fulfillment operations.

Labor shortages present ongoing challenges for Estonia’s freight market, with demographic trends and competition from other industries creating difficulties in recruiting and retaining qualified drivers, logistics specialists, and technical personnel. The aging workforce in transportation sectors requires strategic workforce development initiatives and immigration policies that support industry needs.

Regulatory complexity associated with international freight operations creates compliance burdens and operational challenges, particularly for smaller companies lacking resources to navigate complex customs procedures, environmental regulations, and safety requirements. Harmonization of regulations across different jurisdictions remains an ongoing challenge for cross-border operations.

Infrastructure limitations in certain areas constrain growth potential, with some rural regions lacking adequate road networks and logistics facilities to support comprehensive freight services. Investment requirements for infrastructure upgrades represent significant capital commitments that may limit expansion opportunities for some market participants.

Environmental pressures increasingly influence operational decisions and investment priorities, with stricter emissions standards and sustainability requirements creating compliance costs and necessitating investments in cleaner transportation technologies. Balancing environmental responsibilities with operational efficiency and cost competitiveness presents ongoing challenges for freight companies.

Green logistics initiatives present substantial opportunities for Estonian freight companies to differentiate services and capture environmentally conscious customers. Investment in electric vehicles, alternative fuels, and carbon-neutral operations can create competitive advantages while supporting Estonia’s sustainability commitments and EU environmental objectives.

Technology integration offers numerous opportunities for operational improvement and service enhancement, with artificial intelligence, machine learning, and automation technologies enabling more efficient route planning, predictive maintenance, and customer service delivery. Estonian companies’ digital expertise positions them well to capitalize on these technological opportunities.

Regional expansion into neighboring markets provides growth opportunities through strategic partnerships, acquisitions, and service extensions that leverage Estonia’s logistics capabilities across the broader Baltic and Nordic regions. Cross-border consolidation trends create opportunities for Estonian companies to expand their geographic footprint and service offerings.

Specialized services development in areas such as cold chain logistics, hazardous materials transport, and high-value cargo handling can generate premium revenue streams and strengthen customer relationships. Growing demand for specialized logistics solutions creates opportunities for service differentiation and market positioning.

Competitive dynamics in Estonia’s freight market reflect a healthy balance between established operators and innovative newcomers, with market leadership determined by service quality, technological capabilities, and customer relationships rather than size alone. This competitive environment drives continuous improvement and innovation across all market segments.

Customer expectations continue evolving toward greater transparency, reliability, and flexibility in freight services, with businesses demanding real-time tracking, predictable delivery schedules, and responsive customer support. Meeting these expectations requires ongoing investments in technology systems and operational capabilities that enhance service delivery quality.

Supply chain integration trends influence market dynamics as customers seek comprehensive logistics solutions rather than individual transportation services. Freight companies increasingly position themselves as strategic partners providing end-to-end supply chain management rather than simple cargo movement services.

Technology disruption creates both opportunities and challenges, with new technologies enabling operational improvements while requiring significant investments and organizational changes. Companies that successfully adapt to technological changes gain competitive advantages, while those that lag behind risk losing market position.

Comprehensive market analysis for Estonia’s freight sector employs multiple research methodologies to ensure accurate and reliable insights. Primary research includes structured interviews with industry executives, logistics managers, and government officials responsible for transportation policy and infrastructure development. These interviews provide qualitative insights into market trends, challenges, and opportunities from key stakeholder perspectives.

Secondary research incorporates analysis of government statistics, industry reports, trade publications, and academic studies related to Estonia’s transportation and logistics sectors. This research foundation provides quantitative data on freight volumes, economic impacts, and infrastructure utilization that supports market analysis and trend identification.

Data validation processes ensure research accuracy through cross-referencing multiple sources, statistical analysis of trends and patterns, and expert review of findings and conclusions. MarkWide Research employs rigorous quality control procedures to maintain research integrity and provide reliable market intelligence for decision-making purposes.

Market modeling techniques incorporate economic indicators, industry trends, and regulatory developments to project future market conditions and growth trajectories. These models consider multiple scenarios and variables that could influence market development, providing comprehensive insights for strategic planning and investment decisions.

Northern Estonia dominates the freight market landscape, with Tallinn serving as the primary logistics hub and accounting for approximately 58% of national freight operations. The region benefits from major port facilities, international airport cargo capabilities, and excellent road and rail connections that support both domestic and international freight movements. Industrial concentrations in electronics, machinery, and consumer goods generate substantial freight demand.

Southern Estonia represents a growing freight market segment, with Tartu and surrounding areas developing as secondary logistics centers serving regional manufacturing and agricultural sectors. The region’s 23% share of national freight activity reflects its importance in domestic distribution networks and cross-border trade with Latvia and other southern neighbors.

Western Estonia focuses primarily on maritime logistics and specialized cargo handling, with ports along the Baltic coast serving specific industry segments including timber, agricultural products, and manufactured goods. This region accounts for 19% of freight operations and plays a crucial role in Estonia’s maritime trade relationships with Scandinavian countries and Western Europe.

Cross-border operations represent a significant component of Estonia’s freight market, with international transit services connecting multiple regions and providing comprehensive logistics solutions for European trade routes. These operations benefit from Estonia’s EU membership and strategic geographic positioning between major economic centers.

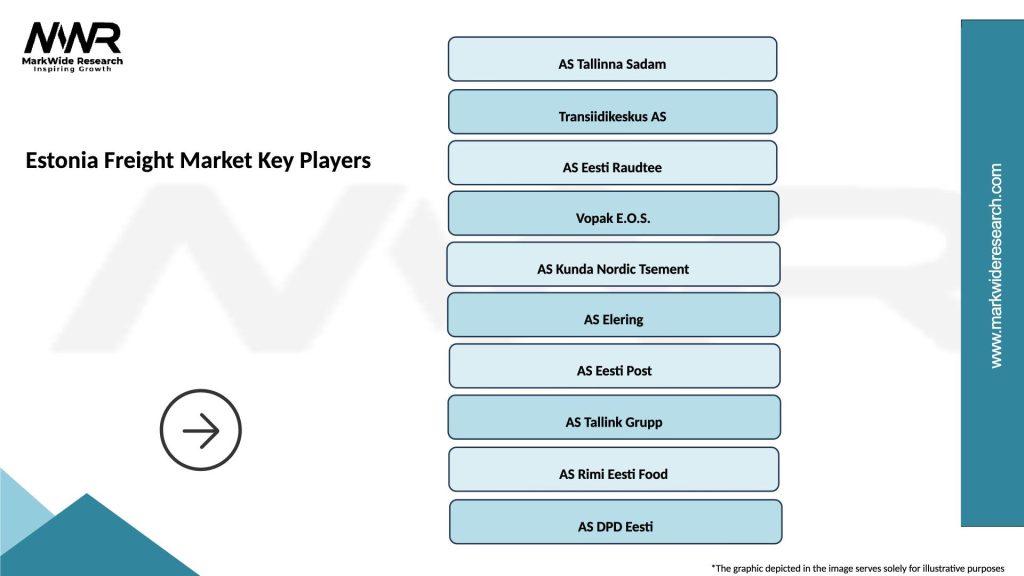

Market leadership in Estonia’s freight sector is distributed among several key players, each bringing unique strengths and capabilities to serve different market segments and customer requirements:

Competitive differentiation occurs through service quality, technological capabilities, geographic coverage, and specialized expertise in particular industry segments or transportation modes. Companies invest heavily in technology systems, fleet modernization, and staff training to maintain competitive advantages in this dynamic market environment.

By Transportation Mode:

By Service Type:

By End-User Industry:

Road freight operations maintain market dominance through flexibility, accessibility, and comprehensive coverage of domestic and regional routes. Estonian road freight companies have invested significantly in fleet modernization, with 72% of commercial vehicles meeting the latest European emission standards. Advanced fleet management systems enable real-time tracking, route optimization, and fuel efficiency improvements that enhance operational performance and customer service quality.

Maritime freight services capitalize on Estonia’s strategic coastal position and modern port infrastructure to serve as a gateway for Baltic Sea trade. The sector handles diverse cargo types including containers, bulk commodities, and specialized shipments, with port facilities continuously upgrading capabilities to accommodate larger vessels and increased cargo volumes. Integration with inland transportation networks creates seamless multimodal logistics solutions.

Rail freight development focuses on heavy cargo transportation and long-distance routes that complement road and maritime services. The upcoming Rail Baltica project will significantly enhance rail freight capabilities, providing direct connections to European markets and supporting sustainable transportation initiatives. Current rail operations emphasize bulk commodities, industrial goods, and intermodal container services.

Express and parcel services experience rapid growth driven by e-commerce expansion and changing consumer expectations for fast delivery. Companies in this segment invest heavily in sorting facilities, last-mile delivery networks, and technology systems that enable efficient package processing and tracking. Same-day and next-day delivery services become increasingly important for competitive positioning.

Operational efficiency gains result from Estonia’s advanced digital infrastructure and streamlined regulatory environment, enabling freight companies to reduce administrative burdens and focus resources on core transportation services. Automated customs processing, electronic documentation, and digital payment systems eliminate traditional bureaucratic delays and reduce operational costs across all freight market segments.

Strategic positioning advantages allow Estonian freight companies to serve as intermediaries for trade between Western Europe, Scandinavia, and Eastern markets. This geographic advantage creates opportunities for value-added services including consolidation, distribution, and supply chain management that generate higher margins than basic transportation services.

Technology leadership benefits enable Estonian freight companies to offer superior service levels through advanced tracking systems, predictive analytics, and automated operations. These technological capabilities attract international customers seeking reliable, transparent logistics solutions and create competitive advantages in global markets.

Market access opportunities through EU membership facilitate seamless cross-border operations and access to European markets without trade barriers or complex regulatory requirements. This access enables Estonian freight companies to expand their geographic reach and serve international customers with comprehensive logistics solutions.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digitalization acceleration continues transforming Estonia’s freight market, with companies implementing artificial intelligence, machine learning, and automation technologies to improve operational efficiency and customer service delivery. These digital initiatives enable predictive maintenance, dynamic route optimization, and enhanced supply chain visibility that create competitive advantages and operational cost reductions.

Sustainability initiatives gain prominence as environmental concerns influence customer decisions and regulatory requirements. Estonian freight companies increasingly invest in electric vehicles, alternative fuels, and carbon offset programs to reduce environmental impact while meeting customer sustainability expectations and regulatory compliance requirements.

Service integration trends drive freight companies to expand beyond basic transportation services, offering comprehensive supply chain solutions including warehousing, distribution, customs clearance, and inventory management. This integration creates stronger customer relationships and higher-value service offerings that improve profitability and market positioning.

Cross-border collaboration increases as Estonian freight companies form strategic partnerships with regional operators to provide seamless international services. These collaborations enable comprehensive coverage of Baltic and Nordic markets while sharing resources and expertise to enhance service capabilities and operational efficiency.

Infrastructure investments continue reshaping Estonia’s freight market landscape, with major projects including port expansions, road improvements, and the transformative Rail Baltica railway connection. These developments enhance capacity, improve connectivity, and position Estonia as a more attractive logistics destination for international businesses seeking efficient supply chain solutions.

Technology adoption accelerates across all freight market segments, with companies implementing advanced fleet management systems, automated warehousing solutions, and blockchain-based documentation systems. According to MWR analysis, these technological investments improve operational efficiency by an average of 28% while enhancing customer satisfaction through improved service reliability and transparency.

Regulatory harmonization efforts within the European Union create opportunities for streamlined cross-border operations and reduced administrative burdens. Estonian freight companies benefit from simplified customs procedures, standardized safety regulations, and harmonized environmental standards that facilitate international service expansion.

Market consolidation trends emerge as larger companies acquire smaller operators to expand geographic coverage, enhance service capabilities, and achieve operational synergies. This consolidation creates more comprehensive service providers while maintaining competitive market dynamics through new entrants and specialized service providers.

Strategic positioning recommendations emphasize leveraging Estonia’s digital infrastructure advantages and geographic positioning to capture growing international freight opportunities. Companies should focus on developing comprehensive multimodal services that integrate road, rail, and maritime transportation to provide seamless logistics solutions for complex supply chain requirements.

Technology investment priorities should focus on customer-facing systems that provide real-time tracking, transparent pricing, and responsive customer service. MarkWide Research analysis indicates that companies investing in customer experience technologies achieve 34% higher customer retention rates and generate premium pricing for their services.

Sustainability initiatives represent both competitive opportunities and regulatory necessities, requiring strategic investments in clean transportation technologies and carbon reduction programs. Companies that proactively address environmental concerns position themselves favorably for future regulatory requirements and environmentally conscious customers.

Workforce development strategies must address labor shortages through comprehensive training programs, competitive compensation packages, and technology systems that enhance job satisfaction and productivity. Successful companies invest in employee development and retention programs that build skilled, loyal workforces capable of delivering superior customer service.

Growth projections for Estonia’s freight market remain positive, with continued expansion expected across all transportation modes and service categories. The completion of major infrastructure projects, particularly Rail Baltica, will create new growth opportunities and enhance Estonia’s position as a regional logistics hub serving broader European markets.

Technology integration will continue driving operational improvements and service enhancements, with artificial intelligence, automation, and data analytics becoming standard components of freight operations. Companies that successfully implement these technologies will achieve competitive advantages through improved efficiency, reduced costs, and enhanced customer service capabilities.

Market evolution toward integrated logistics services will create opportunities for companies offering comprehensive supply chain solutions rather than simple transportation services. This evolution requires investments in warehousing facilities, technology systems, and specialized expertise that enable end-to-end logistics management for complex customer requirements.

Regional integration trends will strengthen Estonia’s role in Baltic and Nordic logistics networks, with cross-border partnerships and service coordination becoming increasingly important for market success. Companies that develop strong regional relationships and comprehensive service networks will be best positioned for future growth opportunities.

Estonia’s freight market represents a dynamic and strategically important sector within the country’s economy, characterized by strong growth momentum, technological leadership, and excellent positioning for future expansion. The market benefits from Estonia’s strategic geographic location, advanced digital infrastructure, and comprehensive transportation networks that support efficient domestic and international freight operations.

Key success factors include continued investment in technology systems, infrastructure development, and workforce capabilities that maintain Estonia’s competitive advantages in regional and international markets. Companies that leverage these advantages while addressing challenges such as labor shortages and regulatory complexity will be best positioned for sustained growth and market leadership.

Future opportunities in green logistics, technology integration, and regional market expansion provide substantial potential for continued market development and enhanced service capabilities. Estonia’s freight market is well-positioned to capitalize on these opportunities through strategic investments, innovative service development, and strong partnerships that create comprehensive logistics solutions for evolving customer requirements.

What is Freight?

Freight refers to the goods transported in bulk by truck, train, ship, or aircraft. In the context of the Estonia Freight Market, it encompasses various logistics services, including shipping, warehousing, and distribution across different sectors.

What are the key players in the Estonia Freight Market?

Key players in the Estonia Freight Market include companies like Tallink Grupp, AS Eesti Raudtee, and DSV Panalpina, which provide a range of logistics and transportation services. These companies are involved in both domestic and international freight operations, among others.

What are the growth factors driving the Estonia Freight Market?

The Estonia Freight Market is driven by factors such as the increasing demand for e-commerce logistics, the growth of the manufacturing sector, and the strategic location of Estonia as a transit hub in Northern Europe. Additionally, advancements in technology are enhancing operational efficiencies.

What challenges does the Estonia Freight Market face?

Challenges in the Estonia Freight Market include infrastructure limitations, regulatory compliance issues, and competition from other logistics hubs in the region. These factors can impact the efficiency and cost-effectiveness of freight operations.

What opportunities exist in the Estonia Freight Market?

Opportunities in the Estonia Freight Market include the potential for expanding digital logistics solutions, increasing investments in green transportation technologies, and the growth of cross-border trade with neighboring countries. These trends can enhance service offerings and operational capabilities.

What trends are shaping the Estonia Freight Market?

Trends in the Estonia Freight Market include the rise of automation in logistics, the adoption of sustainable practices, and the integration of advanced tracking technologies. These innovations are transforming how freight is managed and delivered.

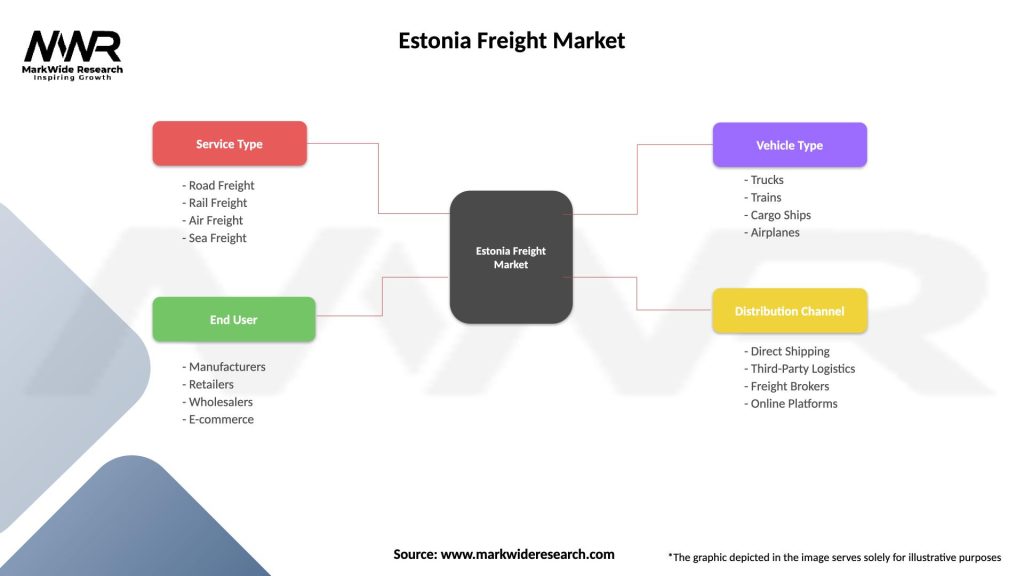

Estonia Freight Market

| Segmentation Details | Description |

|---|---|

| Service Type | Road Freight, Rail Freight, Air Freight, Sea Freight |

| End User | Manufacturers, Retailers, Wholesalers, E-commerce |

| Vehicle Type | Trucks, Trains, Cargo Ships, Airplanes |

| Distribution Channel | Direct Shipping, Third-Party Logistics, Freight Brokers, Online Platforms |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Estonia Freight Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.