444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Europe mHealth Apps Market represents one of the most dynamic and rapidly evolving segments within the broader digital healthcare ecosystem. Mobile health applications have fundamentally transformed how European consumers access healthcare services, manage chronic conditions, and maintain wellness routines. The market encompasses a diverse range of applications including fitness tracking, medication management, telemedicine platforms, mental health support, and chronic disease monitoring solutions.

Digital transformation across European healthcare systems has accelerated significantly, with mHealth apps experiencing unprecedented adoption rates of 78% among smartphone users aged 18-65. The integration of artificial intelligence, machine learning, and Internet of Things (IoT) technologies has enhanced the functionality and user experience of these applications, making them indispensable tools for both healthcare providers and patients.

Regulatory frameworks across European Union member states have evolved to support the safe deployment of medical applications while ensuring data privacy and security compliance. The General Data Protection Regulation (GDPR) has established robust standards for health data management, fostering consumer confidence in digital health solutions. This regulatory clarity has encouraged innovation while maintaining the highest standards of patient safety and data protection.

Market penetration varies significantly across different European regions, with Nordic countries leading adoption rates at 85% smartphone penetration for health apps, followed by Western European nations. The COVID-19 pandemic served as a catalyst for widespread acceptance of digital health solutions, permanently altering consumer behavior and healthcare delivery models across the continent.

The Europe mHealth Apps Market refers to the comprehensive ecosystem of mobile applications designed to support healthcare delivery, health monitoring, wellness management, and medical information access across European countries. These applications leverage smartphone capabilities, wearable device integration, and cloud-based technologies to provide users with convenient, accessible, and personalized healthcare solutions.

mHealth applications encompass various categories including diagnostic tools, treatment management platforms, fitness and wellness trackers, medication adherence systems, and telehealth consultation services. The market includes both consumer-facing applications available through app stores and enterprise solutions deployed by healthcare institutions, insurance companies, and pharmaceutical organizations.

Digital health solutions within this market segment utilize advanced technologies such as artificial intelligence for symptom assessment, machine learning for personalized recommendations, blockchain for secure data sharing, and augmented reality for medical training and patient education. These applications serve multiple stakeholders including individual consumers, healthcare professionals, medical institutions, and public health organizations.

Market dynamics in the European mHealth apps sector demonstrate robust growth driven by increasing smartphone penetration, aging population demographics, rising healthcare costs, and growing consumer awareness of preventive healthcare benefits. The market has experienced substantial expansion with adoption rates reaching 72% among European adults who regularly use at least one health-related mobile application.

Key growth drivers include the integration of wearable technologies, advancement in AI-powered diagnostic capabilities, and increasing support from healthcare systems for digital health initiatives. Government initiatives promoting digital health adoption have contributed to market expansion, with several European countries implementing national digital health strategies that specifically encourage mHealth app utilization.

Competitive landscape features a mix of established technology companies, specialized healthcare software developers, pharmaceutical companies, and innovative startups. Major players have invested heavily in research and development to create comprehensive health ecosystems that integrate multiple functionalities within single platforms.

Future prospects indicate continued growth with emerging technologies such as 5G connectivity, edge computing, and advanced biometric sensors expected to enhance application capabilities and user experiences. The market is projected to maintain strong momentum with increasing focus on personalized medicine and precision health approaches.

Consumer behavior analysis reveals significant shifts in how Europeans approach healthcare management, with increasing preference for self-monitoring and proactive health management. The following insights highlight critical market developments:

Demographic trends across Europe significantly influence mHealth app adoption, with an aging population increasingly seeking convenient healthcare solutions. The proportion of Europeans aged 65 and older continues to grow, creating substantial demand for applications that support independent living and chronic disease management.

Healthcare cost pressures drive both consumers and healthcare systems toward preventive care solutions that can reduce long-term treatment expenses. mHealth applications offer cost-effective alternatives to traditional healthcare delivery methods, enabling early intervention and continuous monitoring without requiring frequent clinical visits.

Technological advancement in smartphone capabilities, including improved sensors, processing power, and battery life, enables more sophisticated health monitoring applications. The proliferation of 5G networks across European markets enhances real-time data transmission and enables advanced telemedicine functionalities.

Regulatory support from European health authorities encourages digital health innovation while maintaining safety standards. The European Medicines Agency (EMA) and national regulatory bodies have established clear pathways for medical app approval, fostering innovation and market confidence.

COVID-19 impact permanently altered healthcare delivery preferences, with consumers becoming more comfortable with digital health solutions. The pandemic demonstrated the effectiveness of remote monitoring and telehealth services, leading to sustained adoption beyond crisis periods.

Insurance integration increasingly includes coverage for digital health solutions, with many European insurance providers offering premium discounts for users who actively engage with approved health apps. This financial incentive drives adoption and sustained usage among cost-conscious consumers.

Data privacy concerns remain significant barriers to widespread adoption, despite GDPR protections. Many potential users express hesitation about sharing sensitive health information through mobile applications, particularly regarding data storage, sharing practices, and potential security breaches.

Digital divide challenges persist across different demographic groups and geographic regions within Europe. Older adults and rural populations may lack the technical skills or reliable internet connectivity necessary to effectively utilize mHealth applications, limiting market penetration in these segments.

Regulatory complexity varies across European Union member states, creating challenges for app developers seeking to launch products across multiple markets. Different national requirements for medical device classification and data handling can increase development costs and time-to-market.

Healthcare system integration barriers include incompatible electronic health record systems, resistance from healthcare professionals, and lack of standardized data exchange protocols. These technical and organizational challenges limit the effectiveness of mHealth apps in clinical settings.

Quality and accuracy concerns regarding consumer-grade health monitoring devices and applications may limit clinical acceptance. Healthcare professionals often question the reliability of data collected through consumer applications, potentially reducing their willingness to incorporate such information into treatment decisions.

Reimbursement limitations in many European healthcare systems do not adequately cover digital health solutions, creating financial barriers for both consumers and healthcare providers. Limited insurance coverage reduces accessibility and may slow adoption rates among price-sensitive segments.

Artificial intelligence integration presents substantial opportunities for enhanced diagnostic capabilities, personalized treatment recommendations, and predictive health analytics. AI-powered applications can analyze vast amounts of health data to identify patterns and provide insights that support both individual health management and population health initiatives.

Chronic disease management represents a significant growth opportunity, with applications specifically designed for diabetes, cardiovascular disease, and respiratory conditions showing strong market potential. The increasing prevalence of chronic conditions across European populations creates sustained demand for comprehensive management solutions.

Mental health applications offer substantial growth potential, particularly following increased awareness of mental health issues during the COVID-19 pandemic. Digital therapy platforms, mood tracking applications, and stress management tools address growing demand for accessible mental health support.

Enterprise healthcare solutions provide opportunities for B2B market expansion, with hospitals, clinics, and healthcare systems seeking comprehensive digital health platforms. These solutions can improve operational efficiency, enhance patient engagement, and support clinical decision-making processes.

Wearable technology integration enables continuous health monitoring and real-time data collection, creating opportunities for more sophisticated health management applications. The growing popularity of smartwatches and fitness trackers provides platforms for advanced health monitoring capabilities.

Pharmaceutical partnerships offer opportunities for medication adherence applications, clinical trial support platforms, and patient engagement tools. Collaboration between app developers and pharmaceutical companies can create comprehensive solutions that support drug development and patient care.

Competitive intensity continues to increase as established technology companies, healthcare organizations, and innovative startups compete for market share. The market demonstrates characteristics of rapid innovation cycles, with new features and capabilities regularly introduced to maintain competitive advantages.

User expectations have evolved significantly, with consumers demanding seamless integration across multiple devices, intuitive user interfaces, and personalized experiences. Applications that fail to meet these elevated expectations face challenges in user acquisition and retention.

Healthcare digitization trends across European countries create favorable conditions for mHealth app adoption. Government initiatives promoting digital health infrastructure development support market growth and encourage innovation in healthcare technology solutions.

Partnership ecosystems have become increasingly important, with successful applications often requiring collaboration between technology developers, healthcare providers, device manufacturers, and regulatory bodies. These partnerships enable comprehensive solutions that address multiple aspects of health management.

Data interoperability challenges and opportunities shape market dynamics, with applications that can effectively integrate with existing healthcare systems gaining competitive advantages. Standardization efforts across European healthcare systems may create new opportunities for comprehensive health data management.

Investment flows into European mHealth startups and established companies indicate strong investor confidence in market growth potential. Venture capital and private equity investments support innovation and market expansion across various application categories.

Primary research methodologies employed in analyzing the European mHealth apps market include comprehensive surveys of healthcare professionals, patients, and technology developers across major European markets. In-depth interviews with key industry stakeholders provide qualitative insights into market trends, challenges, and opportunities.

Secondary research incorporates analysis of regulatory filings, company financial reports, industry publications, and academic studies related to digital health adoption in Europe. Government health statistics and demographic data provide foundational context for market analysis and forecasting.

Market segmentation analysis utilizes both quantitative and qualitative research approaches to identify distinct user groups, application categories, and regional variations. This segmentation enables detailed understanding of specific market dynamics and growth opportunities within different segments.

Technology assessment involves evaluation of emerging technologies, patent filings, and innovation trends that may impact future market development. This analysis helps identify potential disruptive technologies and their likely market impact timelines.

Regulatory analysis examines current and proposed regulations across European Union member states, assessing their potential impact on market development and competitive dynamics. This analysis includes evaluation of data protection requirements, medical device regulations, and reimbursement policies.

Competitive intelligence gathering involves monitoring competitor activities, product launches, partnership announcements, and strategic initiatives. This ongoing analysis provides insights into competitive positioning and market evolution trends.

Nordic countries lead European mHealth app adoption with 89% smartphone penetration for health applications, driven by advanced digital infrastructure, high technology literacy, and supportive government policies. Sweden, Denmark, and Finland demonstrate particularly strong adoption rates across all demographic segments.

Western Europe markets including Germany, France, and the United Kingdom show robust growth with 76% adoption rates among urban populations. These markets benefit from well-established healthcare systems, strong regulatory frameworks, and significant investment in digital health initiatives.

Southern European countries including Italy, Spain, and Portugal demonstrate growing adoption rates, particularly in urban areas and among younger demographics. Government digitization initiatives and EU funding support market development in these regions.

Central and Eastern Europe represent emerging markets with significant growth potential, showing rapid adoption increases of approximately 45% annually. Countries such as Poland, Czech Republic, and Hungary benefit from improving digital infrastructure and increasing smartphone penetration.

Market maturity varies significantly across regions, with Nordic and Western European markets showing characteristics of mature adoption while Eastern European markets demonstrate early-stage growth patterns. This variation creates opportunities for targeted market entry strategies and region-specific product development.

Regulatory harmonization across EU member states supports cross-border market expansion, though national variations in healthcare systems and reimbursement policies continue to influence regional market dynamics and competitive strategies.

Market leaders in the European mHealth apps sector include both global technology companies and specialized healthcare software developers. The competitive landscape demonstrates significant diversity in company sizes, market focus areas, and technological approaches.

Competitive strategies focus on differentiation through specialized functionality, superior user experience, healthcare provider integration, and comprehensive data analytics capabilities. Companies increasingly pursue partnership strategies to expand market reach and enhance service offerings.

Innovation focus areas include artificial intelligence integration, wearable device connectivity, clinical decision support, and personalized health recommendations. Companies that successfully integrate these technologies while maintaining user-friendly interfaces gain competitive advantages.

By Application Type:

By End User:

By Technology Platform:

Fitness and wellness applications represent the largest segment by user adoption, with 82% of mHealth app users engaging with fitness tracking functionality. These applications benefit from integration with wearable devices and social sharing features that enhance user engagement and retention.

Chronic disease management applications demonstrate the highest user engagement rates and clinical value, with users showing daily active usage rates significantly above industry averages. These applications often integrate with healthcare provider systems and support clinical decision-making processes.

Mental health applications have experienced rapid growth, particularly following increased awareness during the COVID-19 pandemic. User acceptance has improved significantly, with professional therapy integration becoming increasingly common and valued by users.

Telemedicine platforms have evolved from basic video consultation tools to comprehensive healthcare delivery platforms. Integration with electronic health records and prescription management systems enhances clinical utility and user satisfaction.

Medication management applications show strong potential for improving health outcomes through enhanced adherence monitoring and drug interaction checking. Integration with pharmacy systems and healthcare providers increases clinical relevance and user value.

Diagnostic support applications utilizing artificial intelligence for symptom assessment and health screening represent emerging high-growth segments. Regulatory approval processes and clinical validation requirements influence market development in this category.

Healthcare providers benefit from improved patient engagement, enhanced care coordination, and access to continuous health monitoring data. mHealth applications enable more efficient resource utilization and support value-based care delivery models.

Patients and consumers gain convenient access to healthcare services, personalized health insights, and tools for proactive health management. These applications empower individuals to take greater control over their health and wellness outcomes.

Healthcare systems can achieve cost reductions through preventive care emphasis, reduced hospital readmissions, and more efficient care delivery. Digital health solutions support population health management and chronic disease prevention initiatives.

Insurance companies benefit from improved risk assessment capabilities, enhanced member engagement, and potential cost savings through preventive care promotion. Wellness programs integrated with mHealth apps can reduce claims costs and improve member satisfaction.

Pharmaceutical companies gain opportunities for enhanced patient engagement, medication adherence improvement, and real-world evidence collection. Digital health partnerships support drug development and post-market surveillance activities.

Technology developers access growing market opportunities with potential for recurring revenue models, data monetization, and platform expansion. Successful applications can achieve significant scale and market valuation through user base growth.

Strengths:

Weaknesses:

Opportunities:

Threats:

Artificial intelligence integration continues to advance, with machine learning algorithms providing increasingly sophisticated health insights, predictive analytics, and personalized recommendations. AI-powered applications demonstrate superior user engagement and clinical outcomes compared to traditional approaches.

Wearable device connectivity has become standard functionality, with seamless integration between smartphones, smartwatches, fitness trackers, and medical devices. This connectivity enables continuous health monitoring and real-time data collection for comprehensive health management.

Telehealth integration transforms mHealth apps from standalone tools to comprehensive healthcare delivery platforms. Video consultations, remote monitoring, and digital prescription services create complete virtual care ecosystems within mobile applications.

Personalization advancement utilizes big data analytics and machine learning to provide highly customized health recommendations, treatment plans, and wellness programs. Users increasingly expect personalized experiences tailored to their specific health conditions and preferences.

Healthcare provider adoption accelerates as clinical evidence demonstrates improved patient outcomes and operational efficiency. Professional medical applications and enterprise solutions gain traction within healthcare institutions and clinical practices.

Mental health focus expands significantly, with applications addressing stress management, anxiety, depression, and overall mental wellness. Integration with professional therapy services and clinical support enhances credibility and effectiveness.

Regulatory approvals for medical-grade applications have increased significantly, with European regulatory bodies establishing clearer pathways for digital therapeutics and clinical decision support tools. These approvals enhance market credibility and enable healthcare system integration.

Partnership announcements between technology companies and healthcare organizations continue to reshape the competitive landscape. Strategic alliances enable comprehensive solution development and market expansion across different healthcare segments.

Investment activities in European mHealth startups have reached record levels, with venture capital and private equity firms recognizing the sector’s growth potential. Funding supports innovation, market expansion, and technology development initiatives.

Technology launches featuring advanced AI capabilities, enhanced security features, and improved user interfaces demonstrate ongoing innovation within the sector. Companies regularly introduce new functionalities to maintain competitive advantages and user engagement.

Clinical validation studies increasingly support the effectiveness of mHealth interventions, providing evidence-based support for healthcare provider adoption and insurance coverage decisions. Peer-reviewed research strengthens market credibility and user confidence.

Acquisition activities consolidate market players and create comprehensive digital health platforms. Larger technology companies acquire specialized healthcare applications to expand their health ecosystem offerings and market presence.

MarkWide Research recommends that companies focus on developing specialized applications addressing specific chronic conditions rather than broad-purpose health apps. Specialized solutions demonstrate higher user engagement rates and create stronger competitive moats through clinical expertise and targeted functionality.

Integration strategies should prioritize healthcare provider partnerships and electronic health record connectivity to enhance clinical utility and user value. Applications that successfully integrate with existing healthcare workflows gain significant competitive advantages and adoption rates.

Data security investments remain critical for building user trust and ensuring regulatory compliance. Companies should implement robust security measures, transparent privacy policies, and user control features to address ongoing privacy concerns and regulatory requirements.

User experience optimization should focus on simplicity, accessibility, and personalization to accommodate diverse user demographics and technical literacy levels. Applications that successfully balance functionality with ease of use achieve higher adoption and retention rates.

Clinical validation through peer-reviewed studies and real-world evidence collection strengthens market positioning and supports healthcare provider adoption. Companies should invest in clinical research and outcome measurement to demonstrate application effectiveness.

Geographic expansion strategies should consider regional variations in healthcare systems, regulatory requirements, and user preferences. Successful market entry requires localized approaches and partnerships with regional healthcare stakeholders.

Market evolution indicates continued strong growth driven by technological advancement, demographic trends, and healthcare system digitization. The integration of emerging technologies such as 5G connectivity, edge computing, and advanced biometric sensors will enhance application capabilities and user experiences.

Adoption patterns suggest mainstream acceptance across all demographic groups, with older adults representing a significant growth opportunity as digital literacy improves and applications become more user-friendly. Cross-generational usage is expected to reach 85% penetration within the next five years.

Technology integration will increasingly focus on comprehensive health ecosystems that combine multiple functionalities within unified platforms. Successful applications will offer seamless integration across devices, healthcare providers, and health management activities.

Regulatory evolution will likely establish clearer standards for digital therapeutics, clinical decision support tools, and health data management. These developments will create new opportunities for medical-grade applications while ensuring patient safety and data protection.

Healthcare system integration will become standard practice, with mHealth applications serving as essential components of digital health infrastructure. This integration will support value-based care models and population health management initiatives across European healthcare systems.

Innovation focus will shift toward precision medicine, predictive analytics, and preventive care solutions that can demonstrate measurable health outcomes and cost savings. Applications that successfully combine clinical effectiveness with user engagement will dominate future market growth.

The Europe mHealth Apps Market represents a transformative force in healthcare delivery, offering unprecedented opportunities for improved patient outcomes, cost reduction, and healthcare accessibility. The market demonstrates strong fundamentals with robust growth drivers, supportive regulatory frameworks, and increasing acceptance across all stakeholder groups.

Technological advancement continues to enhance application capabilities, with artificial intelligence, wearable integration, and telehealth functionality creating comprehensive digital health ecosystems. These developments position mHealth applications as essential tools for modern healthcare management and delivery.

Market challenges including data privacy concerns, digital divide issues, and integration complexities require ongoing attention and strategic solutions. Companies that successfully address these challenges while delivering superior user experiences and clinical value will achieve sustainable competitive advantages.

Future prospects remain highly positive, with demographic trends, healthcare cost pressures, and technology evolution supporting continued market expansion. The sector’s evolution toward specialized, clinically validated, and integrated solutions creates significant opportunities for stakeholders across the healthcare ecosystem. MWR analysis indicates that companies focusing on clinical effectiveness, user engagement, and healthcare system integration will be best positioned for long-term success in this dynamic and rapidly evolving market.

What is mHealth Apps?

mHealth Apps refer to mobile health applications that provide health-related services through mobile devices. These apps can assist users in managing their health, tracking fitness, and accessing medical information.

What are the key players in the Europe mHealth Apps Market?

Key players in the Europe mHealth Apps Market include companies like MyFitnessPal, HealthTap, and Fitbit, which offer various health tracking and management solutions, among others.

What are the main drivers of growth in the Europe mHealth Apps Market?

The growth of the Europe mHealth Apps Market is driven by increasing smartphone penetration, rising health awareness among consumers, and the demand for remote patient monitoring solutions.

What challenges does the Europe mHealth Apps Market face?

Challenges in the Europe mHealth Apps Market include data privacy concerns, regulatory compliance issues, and the need for user engagement to ensure app effectiveness.

What opportunities exist in the Europe mHealth Apps Market?

Opportunities in the Europe mHealth Apps Market include the integration of artificial intelligence for personalized health recommendations and the expansion of telehealth services to enhance patient care.

What trends are shaping the Europe mHealth Apps Market?

Trends in the Europe mHealth Apps Market include the rise of wearable technology, increased focus on mental health apps, and the growing popularity of gamification in health management.

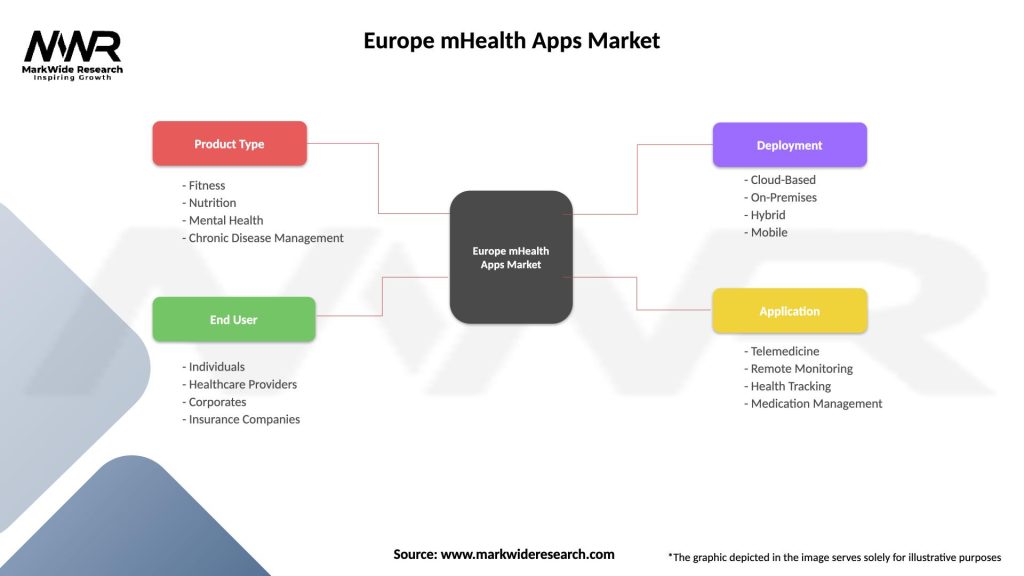

Europe mHealth Apps Market

| Segmentation Details | Description |

|---|---|

| Product Type | Fitness, Nutrition, Mental Health, Chronic Disease Management |

| End User | Individuals, Healthcare Providers, Corporates, Insurance Companies |

| Deployment | Cloud-Based, On-Premises, Hybrid, Mobile |

| Application | Telemedicine, Remote Monitoring, Health Tracking, Medication Management |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Europe mHealth Apps Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.