444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The SEA syngas market represents a rapidly expanding segment within Southeast Asia’s industrial landscape, driven by increasing demand for cleaner energy solutions and sustainable chemical production processes. Syngas, or synthesis gas, serves as a crucial intermediate in various industrial applications, including methanol production, ammonia synthesis, and Fischer-Tropsch processes. The region’s growing industrialization, coupled with stringent environmental regulations, has positioned the SEA syngas market as a key enabler of sustainable manufacturing practices.

Market dynamics in Southeast Asia reflect a significant shift toward cleaner production technologies, with syngas adoption growing at an impressive 8.2% CAGR across major industrial sectors. Countries including Thailand, Malaysia, Singapore, and Indonesia are leading this transformation, implementing advanced gasification technologies to meet both domestic energy needs and export requirements. The region’s abundant biomass resources and strategic location have created favorable conditions for syngas production and distribution networks.

Industrial applications continue to diversify, with petrochemical companies, power generation facilities, and chemical manufacturers increasingly adopting syngas-based processes. The technology’s versatility in utilizing various feedstocks, from natural gas to biomass and coal, has enhanced its appeal among regional manufacturers seeking operational flexibility and environmental compliance.

The SEA syngas market refers to the comprehensive ecosystem of synthesis gas production, distribution, and utilization across Southeast Asian countries, encompassing technologies, infrastructure, and applications that convert various feedstocks into valuable industrial intermediates. Syngas consists primarily of carbon monoxide and hydrogen, produced through gasification processes that transform carbonaceous materials into clean-burning fuel and chemical precursors.

Gasification technology forms the cornerstone of syngas production, utilizing high-temperature processes to convert feedstocks including natural gas, coal, biomass, and waste materials into synthesis gas. This process enables the transformation of diverse raw materials into standardized industrial inputs, supporting various downstream applications from fuel production to chemical synthesis.

Regional significance extends beyond traditional energy applications, as Southeast Asian countries leverage syngas technology to address multiple challenges simultaneously: energy security, environmental sustainability, and industrial competitiveness. The market encompasses upstream gasification facilities, midstream purification and conditioning systems, and downstream conversion processes that create value-added products for both domestic consumption and international export.

Strategic positioning of the SEA syngas market reflects the region’s commitment to sustainable industrial development and energy diversification. The market demonstrates robust growth potential, supported by favorable government policies, increasing environmental awareness, and technological advancements in gasification processes. Key growth drivers include rising demand for cleaner fuels, expanding petrochemical industries, and the need for efficient waste-to-energy solutions.

Technology adoption rates across the region show significant momentum, with 72% of major industrial facilities either implementing or planning syngas integration within their operations. This adoption pattern reflects the technology’s proven ability to enhance operational efficiency while reducing environmental impact. Investment flows into syngas infrastructure continue to accelerate, particularly in countries with established petrochemical sectors and supportive regulatory frameworks.

Market segmentation reveals diverse applications spanning power generation, chemical production, and fuel synthesis, with each segment contributing to overall market expansion. The region’s strategic advantages, including abundant feedstock availability, skilled workforce, and proximity to major export markets, position Southeast Asia as an emerging hub for syngas production and technology development.

Technological evolution within the SEA syngas market demonstrates several critical insights that shape industry development and investment decisions:

Investment patterns reveal strong confidence in long-term market growth, with major industrial players committing substantial resources to syngas infrastructure development. Technology partnerships between regional companies and international technology providers accelerate knowledge transfer and capability building throughout Southeast Asia.

Environmental regulations serve as primary catalysts for syngas market expansion, as governments across Southeast Asia implement increasingly stringent emission standards and carbon reduction targets. These regulatory frameworks create compelling economic incentives for industries to adopt cleaner production technologies, with syngas offering proven pathways to reduce greenhouse gas emissions while maintaining industrial competitiveness.

Energy security concerns drive strategic investments in syngas infrastructure, enabling countries to diversify their energy portfolios and reduce dependence on imported fuels. The technology’s ability to convert domestic resources, including biomass and waste materials, into valuable energy products aligns with national energy independence objectives. Feedstock flexibility provides additional security benefits, allowing producers to adapt to changing resource availability and market conditions.

Industrial growth across petrochemical, chemical, and manufacturing sectors creates sustained demand for syngas as a key industrial intermediate. The region’s expanding middle class and urbanization trends drive consumption of products derived from syngas-based processes, including plastics, fertilizers, and synthetic fuels. Export opportunities to developed markets seeking cleaner industrial products further enhance market attractiveness.

Technological maturation reduces implementation risks and operational costs, making syngas projects more financially viable for a broader range of applications. Improved gasification efficiency, enhanced gas cleaning technologies, and better process integration capabilities contribute to stronger project economics and faster payback periods.

Capital intensity represents a significant barrier to market entry, as syngas facilities require substantial upfront investments in gasification equipment, gas cleaning systems, and supporting infrastructure. These high initial costs can deter smaller companies and limit market participation to well-capitalized organizations with access to long-term financing solutions.

Technical complexity of gasification processes demands specialized expertise and operational knowledge that may be limited in certain regional markets. The need for skilled technicians, process engineers, and maintenance personnel creates workforce development challenges that can constrain project implementation timelines and operational efficiency.

Feedstock availability and pricing volatility introduce operational uncertainties that affect project economics and long-term viability. Competition for biomass resources from other applications, seasonal variations in agricultural waste availability, and fluctuating natural gas prices can impact production costs and profit margins.

Infrastructure limitations in some Southeast Asian countries may restrict syngas market development, particularly in areas lacking adequate transportation networks, utility connections, or industrial support services. These infrastructure gaps can increase project costs and limit site selection options for new facilities.

Regulatory uncertainty regarding future environmental standards, carbon pricing mechanisms, and technology incentives creates planning challenges for long-term investments. Changing policy landscapes may affect project economics and strategic decision-making processes.

Circular economy initiatives present substantial opportunities for syngas market expansion, as governments and industries seek innovative solutions for waste management and resource recovery. The technology’s ability to convert municipal solid waste, agricultural residues, and industrial byproducts into valuable synthesis gas aligns perfectly with circular economy principles and creates new revenue streams for waste management companies.

Carbon capture integration offers promising pathways for enhanced environmental performance and potential carbon credit generation. Advanced syngas facilities incorporating carbon capture, utilization, and storage technologies can achieve negative emissions profiles while producing valuable industrial products, creating competitive advantages in carbon-constrained markets.

Export market development provides significant growth potential, particularly for countries with abundant biomass resources and strategic geographic locations. Clean fuel exports to developed markets seeking low-carbon alternatives can generate substantial foreign exchange earnings while supporting domestic industrial development.

Technology partnerships with international leaders create opportunities for knowledge transfer, capability building, and market access. Joint ventures and licensing agreements can accelerate technology deployment while reducing development risks and costs for regional players.

Government incentives and support programs continue to evolve, offering financial assistance, tax benefits, and regulatory streamlining for qualifying syngas projects. These supportive policies create favorable investment climates and improve project economics across multiple market segments.

Supply chain evolution within the SEA syngas market reflects increasing sophistication and integration across value chain components. Upstream gasification technology providers are developing closer relationships with downstream users, creating integrated solutions that optimize overall system performance and economics. This vertical integration trend enhances operational efficiency and reduces transaction costs throughout the supply chain.

Competitive dynamics demonstrate a shift toward collaborative approaches, with traditional competitors forming strategic alliances to share development costs and technical risks. These partnerships enable faster technology deployment and market penetration while creating economies of scale that benefit all participants. Innovation cycles are accelerating as companies invest in research and development to maintain competitive advantages and address evolving market requirements.

Price mechanisms for syngas products are becoming more sophisticated, incorporating environmental attributes and quality specifications that reflect downstream application requirements. Long-term supply agreements with pricing formulas linked to feedstock costs and environmental benefits provide stability for both producers and consumers while encouraging continued investment in capacity expansion.

Regional integration efforts create opportunities for cross-border syngas trade and infrastructure sharing, potentially achieving 15-20% cost reductions through economies of scale and optimized logistics networks. These collaborative approaches enhance market liquidity and provide greater flexibility for supply and demand balancing across the region.

Primary research methodologies employed in analyzing the SEA syngas market encompass comprehensive stakeholder interviews, industry surveys, and direct engagement with key market participants including technology providers, project developers, end-users, and regulatory authorities. These primary sources provide real-time insights into market conditions, technology trends, and strategic decision-making processes that shape industry development.

Secondary research components integrate multiple data sources including government publications, industry reports, academic studies, and corporate disclosures to create comprehensive market intelligence. This multi-source approach ensures data accuracy and provides diverse perspectives on market dynamics and growth drivers.

Data validation processes involve cross-referencing information from multiple sources and conducting follow-up interviews to confirm key findings and resolve any inconsistencies. Statistical analysis techniques help identify trends and patterns while ensuring data reliability and analytical rigor.

Market modeling approaches utilize both bottom-up and top-down methodologies to project market growth and segment performance. These models incorporate various scenarios and sensitivity analyses to account for different market conditions and policy environments that may affect future development trajectories.

Thailand leads the SEA syngas market with approximately 35% regional market share, driven by its established petrochemical industry and supportive government policies for clean energy development. The country’s strategic location and well-developed industrial infrastructure create favorable conditions for syngas production and export activities. Major facilities in the Eastern Economic Corridor demonstrate successful integration of gasification technologies with downstream chemical production processes.

Malaysia represents the second-largest market segment, accounting for roughly 28% of regional capacity, with significant investments in palm oil waste gasification and natural gas-based syngas production. The country’s abundant biomass resources and established oil and gas sector provide strong foundations for market expansion. Government initiatives supporting renewable energy and waste management create additional growth opportunities.

Singapore focuses on high-value applications and technology development, leveraging its position as a regional hub for petrochemicals and specialty chemicals. Despite limited domestic feedstock resources, the country’s advanced technical capabilities and strategic location support import-based syngas operations and technology export activities.

Indonesia demonstrates substantial growth potential with vast biomass resources and expanding industrial base, though infrastructure limitations currently constrain market development. The country’s commitment to reducing greenhouse gas emissions and improving energy security drives interest in syngas technologies, particularly for remote area applications and industrial waste management.

Vietnam and Philippines represent emerging markets with growing industrial sectors and increasing environmental awareness, creating opportunities for syngas market entry and development. These countries benefit from technology transfer and investment from more established regional markets.

Market leadership in the SEA syngas sector reflects a diverse ecosystem of international technology providers, regional industrial companies, and specialized engineering firms that contribute to market development and growth:

Strategic partnerships between international technology providers and regional companies accelerate market development while building local capabilities and expertise. These collaborations often involve technology licensing, joint ventures, and long-term service agreements that support sustainable market growth.

Innovation focus among leading companies emphasizes improving gasification efficiency, reducing environmental impact, and expanding feedstock flexibility to address diverse regional market requirements and opportunities.

By Technology:

By Application:

By Feedstock:

Natural Gas-based Syngas maintains market leadership due to feedstock availability, process maturity, and consistent product quality. This category benefits from established supply chains and proven technology platforms that minimize operational risks. Investment preferences favor natural gas projects for their predictable economics and shorter development timelines, though environmental considerations increasingly influence technology selection.

Biomass Gasification represents the fastest-growing category, driven by sustainability objectives and abundant regional feedstock resources. Agricultural residues from palm oil, rice, and sugarcane production provide substantial feedstock potential, while dedicated energy crops offer additional supply security. This category faces challenges related to feedstock logistics and seasonal availability but benefits from strong policy support and carbon credit opportunities.

Waste-to-Syngas applications demonstrate significant potential for addressing multiple regional challenges simultaneously, including waste management, energy production, and environmental protection. Municipal solid waste gasification projects gain traction in urban areas facing waste disposal challenges, while industrial waste applications offer specialized solutions for specific industry sectors.

Power Generation applications show increasing adoption as utilities seek cleaner alternatives to conventional fossil fuels. Integrated gasification combined cycle plants demonstrate superior environmental performance compared to traditional coal-fired power generation, supporting regional decarbonization objectives while maintaining energy security.

Chemical Production remains the largest end-use category, with methanol and ammonia production driving sustained syngas demand. These applications benefit from established markets and proven economics, providing stable demand foundations for syngas producers throughout the region.

Environmental advantages position syngas technology as a key enabler of sustainable industrial development, offering significant reductions in greenhouse gas emissions compared to conventional production processes. Clean production capabilities help companies meet increasingly stringent environmental regulations while maintaining operational competitiveness and market access.

Economic benefits include improved resource utilization efficiency, reduced waste disposal costs, and potential revenue generation from byproduct sales. Operational flexibility allows producers to adapt to changing feedstock availability and market conditions, enhancing long-term business sustainability and profitability.

Strategic advantages for regional stakeholders include enhanced energy security, reduced import dependence, and improved industrial competitiveness. Technology development capabilities create opportunities for intellectual property creation and technology export to other emerging markets.

Social benefits encompass job creation in high-skilled technical positions, rural economic development through biomass supply chains, and improved waste management in urban areas. These positive impacts support broader sustainable development objectives while creating stakeholder value.

Risk mitigation benefits include diversified feedstock options, reduced exposure to volatile fossil fuel prices, and improved regulatory compliance capabilities. These advantages enhance project bankability and attract long-term investment capital for continued market expansion.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digitalization integration transforms syngas operations through advanced process control systems, predictive maintenance technologies, and real-time optimization platforms. These digital solutions enhance operational efficiency, reduce maintenance costs, and improve overall plant performance while enabling remote monitoring and control capabilities.

Modular design approaches gain popularity as they offer faster deployment, reduced capital requirements, and enhanced scalability for diverse market applications. Standardized modules enable cost reductions through manufacturing economies of scale while providing flexibility for site-specific requirements and phased capacity expansion.

Hybrid feedstock strategies become increasingly common as producers seek to optimize economics and ensure supply security through diversified input streams. Co-gasification of multiple feedstock types enables operational flexibility while maximizing resource utilization and minimizing waste generation.

Carbon utilization integration represents an emerging trend where syngas facilities incorporate carbon capture and utilization technologies to create additional value streams. These integrated approaches demonstrate 25-30% improvement in overall carbon efficiency while generating premium products for specialized markets.

Regional cooperation initiatives facilitate technology sharing, joint infrastructure development, and coordinated policy frameworks that support market expansion. Cross-border partnerships create opportunities for shared resources and risk mitigation while accelerating overall market development across Southeast Asia.

Technology partnerships between regional companies and international leaders accelerate capability building and market development throughout Southeast Asia. Recent collaborations focus on adapting proven technologies to local conditions while building domestic expertise and supply chain capabilities.

Policy framework evolution across multiple countries creates increasingly supportive environments for syngas investment and deployment. Regulatory streamlining initiatives reduce project development timelines while maintaining environmental protection standards and safety requirements.

Infrastructure investments in supporting systems including gas pipelines, storage facilities, and transportation networks enhance market accessibility and operational efficiency. These developments reduce project costs and enable broader market participation across diverse geographic areas.

Research and development initiatives focus on improving gasification efficiency, expanding feedstock compatibility, and reducing environmental impact. Innovation programs supported by government agencies and industry associations accelerate technology advancement and commercial deployment.

Market consolidation activities create stronger companies with enhanced technical capabilities and financial resources for large-scale project development. Strategic mergers and acquisitions enable technology integration and market expansion while improving overall industry competitiveness.

Investment strategies should prioritize projects with diversified feedstock options and strong downstream market linkages to ensure long-term viability and profitability. MarkWide Research analysis indicates that integrated facilities demonstrate superior financial performance compared to standalone gasification operations, suggesting the importance of value chain integration in project planning.

Technology selection decisions should consider local feedstock availability, environmental regulations, and market requirements to optimize project economics and operational performance. Flexible designs that accommodate multiple feedstock types provide strategic advantages in dynamic market conditions.

Partnership development with established technology providers and experienced operators can significantly reduce project risks while accelerating capability building and market entry. These relationships provide access to proven technologies, operational expertise, and established supply chains that support successful project implementation.

Policy engagement remains critical for project success, as supportive regulatory frameworks and government incentives significantly impact project economics and development timelines. Active participation in policy development processes helps ensure favorable conditions for market growth and investment.

Market timing considerations suggest that early market entry provides competitive advantages through preferred site selection, favorable supply agreements, and established customer relationships. However, careful evaluation of local market conditions and infrastructure readiness remains essential for successful project development.

Growth projections for the SEA syngas market indicate sustained expansion driven by increasing industrial demand, environmental regulations, and technology improvements. Market penetration is expected to accelerate as costs decline and operational experience increases across the region, with adoption rates potentially reaching 85% of suitable industrial applications within the next decade.

Technology evolution will continue improving efficiency and reducing costs, making syngas solutions more competitive across broader market segments. Advanced gasification technologies incorporating artificial intelligence and machine learning capabilities promise significant performance improvements and operational optimization opportunities.

Regional integration efforts will create larger, more liquid markets that support economies of scale and enhanced supply security. Cross-border infrastructure development enables resource sharing and market optimization while reducing overall system costs and risks.

Sustainability focus will drive continued innovation in clean production technologies and circular economy applications. Carbon neutrality objectives across multiple countries create strong policy support for syngas deployment while generating additional revenue opportunities through environmental attribute sales.

Export market development provides substantial growth potential as global demand for clean fuels and chemicals continues expanding. MWR projections suggest that Southeast Asian syngas exports could capture 12-15% of global clean fuel trade by 2030, supporting regional economic development and industrial competitiveness.

The SEA syngas market represents a transformative opportunity for sustainable industrial development across Southeast Asia, combining environmental benefits with economic growth potential. The region’s abundant feedstock resources, supportive policy frameworks, and growing industrial base create favorable conditions for continued market expansion and technology deployment.

Strategic advantages including geographic location, resource availability, and government support position Southeast Asia as an emerging global hub for syngas production and technology development. The market’s evolution from traditional applications toward innovative circular economy solutions demonstrates its adaptability and long-term growth potential.

Investment opportunities remain substantial for companies with appropriate technical capabilities and strategic vision, particularly in integrated facilities that maximize value creation across the entire supply chain. Success factors include technology selection, partnership development, and active engagement with evolving policy frameworks that support sustainable industrial development throughout the region.

What is Syngas?

Syngas, or synthesis gas, is a mixture of hydrogen, carbon monoxide, and sometimes carbon dioxide. It is primarily produced from natural gas, coal, or biomass and is used as a fuel or as an intermediate in the production of chemicals and fuels.

What are the key players in the SEA Syngas Market?

Key players in the SEA Syngas Market include Air Products and Chemicals, Inc., Linde plc, and Sasol Limited, among others. These companies are involved in the production and supply of syngas for various applications, including energy generation and chemical manufacturing.

What are the growth factors driving the SEA Syngas Market?

The SEA Syngas Market is driven by increasing demand for cleaner energy sources, the need for efficient fuel production, and the rising use of syngas in chemical synthesis. Additionally, government initiatives promoting renewable energy are also contributing to market growth.

What challenges does the SEA Syngas Market face?

The SEA Syngas Market faces challenges such as high production costs, environmental concerns related to carbon emissions, and competition from alternative energy sources. These factors can hinder the growth and adoption of syngas technologies.

What opportunities exist in the SEA Syngas Market?

Opportunities in the SEA Syngas Market include advancements in gasification technologies, increasing investments in renewable energy projects, and the potential for syngas to be used in hydrogen production. These factors can enhance the market’s growth prospects.

What trends are shaping the SEA Syngas Market?

Trends in the SEA Syngas Market include the integration of carbon capture and storage technologies, the development of more efficient gasification processes, and the growing interest in syngas for hydrogen production. These trends are expected to influence the market dynamics significantly.

SEA Syngas Market

| Segmentation Details | Description |

|---|---|

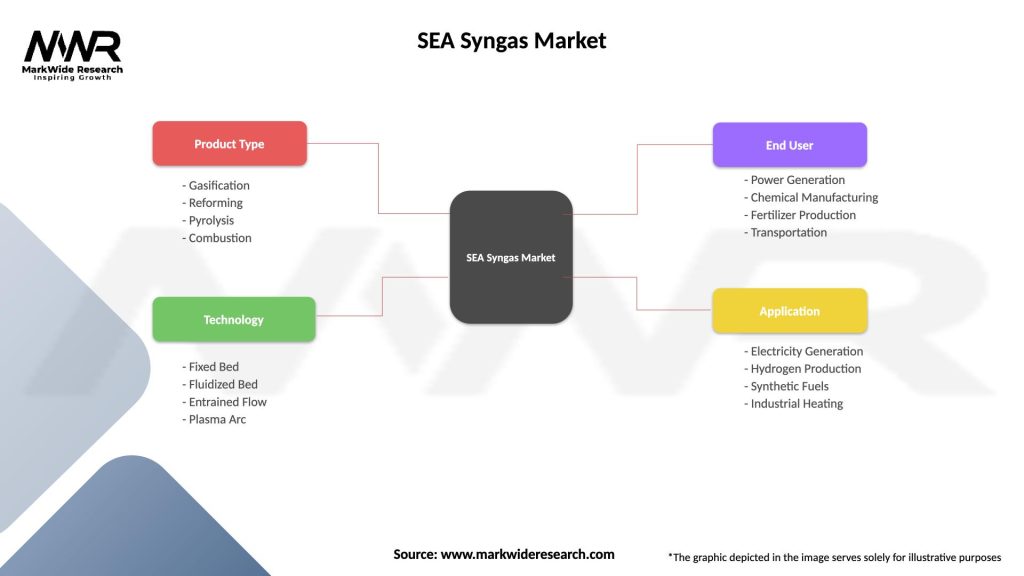

| Product Type | Gasification, Reforming, Pyrolysis, Combustion |

| Technology | Fixed Bed, Fluidized Bed, Entrained Flow, Plasma Arc |

| End User | Power Generation, Chemical Manufacturing, Fertilizer Production, Transportation |

| Application | Electricity Generation, Hydrogen Production, Synthetic Fuels, Industrial Heating |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the SEA Syngas Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.