444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The North America power transformer market represents a critical component of the region’s electrical infrastructure, encompassing the United States, Canada, and Mexico. This dynamic market serves as the backbone for electricity transmission and distribution networks, facilitating efficient power delivery across vast geographical areas. Power transformers play an essential role in stepping up or stepping down voltage levels to ensure safe and efficient electricity transmission from generation facilities to end consumers.

Market dynamics indicate robust growth driven by increasing electricity demand, aging infrastructure replacement needs, and the integration of renewable energy sources. The region’s commitment to grid modernization and smart grid initiatives has created substantial opportunities for advanced transformer technologies. MarkWide Research analysis reveals that the market is experiencing steady expansion, with growth rates of approximately 4.2% CAGR projected through the forecast period.

Regional distribution shows the United States commanding the largest market share at approximately 78%, followed by Canada at 15% and Mexico at 7%. This distribution reflects the varying levels of industrial development, population density, and infrastructure investment across the three countries. The market encompasses various transformer types, including distribution transformers, power transformers, and specialty transformers designed for specific applications.

The North America power transformer market refers to the comprehensive ecosystem of electrical equipment designed to transfer electrical energy between circuits through electromagnetic induction, operating within the geographical boundaries of the United States, Canada, and Mexico. These devices are fundamental to electrical power systems, enabling voltage transformation for efficient transmission and distribution.

Power transformers serve multiple critical functions within the electrical grid infrastructure. They step up voltage levels at generation facilities to minimize transmission losses over long distances, then step down voltages at distribution points to safe levels for consumer use. The market encompasses various transformer categories, including oil-filled transformers, dry-type transformers, and gas-insulated transformers, each designed for specific operational requirements and environmental conditions.

Market participants include manufacturers, distributors, utility companies, industrial end-users, and service providers who collectively contribute to the transformer value chain. The market’s significance extends beyond mere equipment sales, encompassing installation services, maintenance contracts, and technological innovations that enhance grid reliability and efficiency.

Strategic market positioning reveals the North America power transformer market as a mature yet evolving sector characterized by steady demand growth and technological advancement. The market benefits from substantial infrastructure investment, regulatory support for grid modernization, and increasing emphasis on renewable energy integration. Key growth drivers include aging infrastructure replacement, smart grid development, and industrial expansion across the region.

Technology trends are reshaping market dynamics, with digital transformers, condition monitoring systems, and eco-friendly insulation materials gaining prominence. The adoption rate of smart transformer technologies has increased by approximately 23% over recent years, reflecting utilities’ commitment to grid modernization. Market segmentation shows distribution transformers accounting for the largest share, followed by power transformers and specialty units.

Competitive landscape features established global manufacturers alongside regional players, creating a diverse supplier ecosystem. The market demonstrates resilience through economic cycles, supported by essential infrastructure requirements and regulatory mandates for grid reliability. Future prospects remain positive, driven by electrification trends, renewable energy integration, and ongoing infrastructure modernization initiatives.

Market intelligence reveals several critical insights shaping the North America power transformer landscape:

Primary growth catalysts propelling the North America power transformer market include several interconnected factors that create sustained demand across the region. Infrastructure aging represents the most significant driver, with many transformers installed during the 1960s-1980s reaching end-of-life status and requiring replacement. This replacement cycle creates predictable demand patterns for utilities and industrial customers.

Renewable energy expansion serves as another crucial driver, necessitating grid infrastructure upgrades to accommodate variable power sources. Solar and wind installations require specialized transformers for voltage regulation and grid synchronization. The renewable energy sector’s growth rate of approximately 12% annually creates corresponding demand for supporting transformer infrastructure.

Electrification trends across transportation, heating, and industrial processes increase overall electricity demand, requiring grid capacity expansion and transformer upgrades. Smart city initiatives and industrial automation further drive demand for reliable, efficient power distribution systems. Additionally, regulatory mandates for grid modernization and reliability improvements create mandatory replacement and upgrade cycles that support market growth.

Market challenges present obstacles to growth and profitability within the North America power transformer sector. High capital costs associated with transformer procurement and installation create budget constraints for utilities and industrial customers, particularly during economic downturns. The substantial investment required for large power transformers can delay project timelines and reduce market velocity.

Supply chain complexities pose significant challenges, with long lead times for specialized transformers and critical component shortages affecting delivery schedules. Raw material price volatility, particularly for copper, steel, and specialized insulation materials, creates cost pressures and margin compression for manufacturers. These factors contribute to project delays and increased total ownership costs.

Regulatory uncertainties regarding environmental standards, efficiency requirements, and grid interconnection rules create planning challenges for market participants. Technical complexity associated with modern transformer designs requires specialized expertise for installation and maintenance, potentially limiting market accessibility for smaller service providers. Additionally, environmental concerns related to transformer oil disposal and recycling create compliance costs and operational complexities.

Emerging opportunities within the North America power transformer market present significant potential for growth and innovation. Grid modernization initiatives across the region create substantial demand for advanced transformer technologies, including digital monitoring systems and smart grid integration capabilities. Government infrastructure investment programs provide funding support for utility upgrades and expansion projects.

Renewable energy integration offers extensive opportunities for specialized transformer applications, including offshore wind connections, solar farm substations, and energy storage system interfaces. The growing emphasis on grid resilience creates demand for redundant systems and rapid replacement capabilities, particularly in areas prone to natural disasters.

Industrial expansion in sectors such as data centers, electric vehicle manufacturing, and advanced manufacturing creates new market segments with specific transformer requirements. Cross-border trade opportunities between the United States, Canada, and Mexico under trade agreements facilitate market expansion and supply chain optimization. Technology partnerships between utilities and manufacturers enable innovative solutions that address specific regional challenges and requirements.

Market forces shaping the North America power transformer landscape reflect complex interactions between supply and demand factors, regulatory influences, and technological developments. Demand patterns demonstrate cyclical characteristics aligned with economic growth, infrastructure investment cycles, and regulatory mandates. Utility procurement strategies increasingly emphasize long-term partnerships and total cost of ownership considerations.

Supply dynamics show regional manufacturing capacity expansion, with several major manufacturers establishing or expanding North American production facilities. This trend toward regional manufacturing reduces supply chain risks and improves delivery times. Competitive intensity varies by market segment, with commodity transformers experiencing price pressure while specialized applications command premium pricing.

Technology evolution drives market transformation, with digitalization and smart grid capabilities becoming standard requirements rather than premium features. MWR analysis indicates that approximately 35% of new transformer installations now include digital monitoring capabilities. Market consolidation continues through strategic acquisitions and partnerships, creating larger, more capable organizations with enhanced research and development resources.

Comprehensive research approach employed for analyzing the North America power transformer market combines primary and secondary research methodologies to ensure accuracy and reliability. Primary research includes extensive interviews with industry executives, utility managers, procurement specialists, and technical experts across the United States, Canada, and Mexico. These interviews provide insights into market trends, purchasing decisions, and future requirements.

Secondary research encompasses analysis of industry reports, regulatory filings, company financial statements, and technical publications. Data validation processes ensure information accuracy through cross-referencing multiple sources and expert verification. Market sizing and forecasting utilize econometric models that consider historical trends, economic indicators, and industry-specific factors.

Regional analysis methodology accounts for varying market conditions, regulatory environments, and economic factors across North American countries. Segmentation analysis examines market dynamics by transformer type, application, voltage rating, and end-user category. Competitive intelligence gathering includes analysis of market share, product portfolios, pricing strategies, and strategic initiatives of key market participants.

United States market dominates the North American power transformer landscape, representing approximately 78% of regional demand. The market benefits from extensive electrical infrastructure, substantial industrial base, and ongoing grid modernization initiatives. Key growth areas include Texas, California, and the Northeast corridor, driven by population growth, renewable energy development, and infrastructure replacement needs.

Canadian market accounts for approximately 15% of regional demand, characterized by harsh operating conditions that require specialized transformer designs. The market focuses on reliability and cold-weather performance, with significant opportunities in oil sands operations, mining, and hydroelectric power transmission. Provincial variations create diverse market conditions, with Alberta and Ontario representing the largest markets.

Mexican market comprises approximately 7% of regional demand but demonstrates the highest growth potential. Infrastructure development programs, industrial expansion, and electrification initiatives drive market growth. The market benefits from manufacturing sector growth, particularly in automotive and electronics industries. Cross-border trade with the United States creates opportunities for integrated supply chain strategies and technology transfer.

Market leadership in the North America power transformer sector features a mix of global manufacturers and regional specialists, creating a diverse competitive environment. The competitive landscape demonstrates varying strategies, from broad product portfolios to specialized niche focus.

Competitive strategies include technology innovation, service expansion, regional manufacturing, and strategic partnerships with utilities and engineering firms.

Market segmentation reveals diverse applications and requirements across the North America power transformer market. By Product Type: Distribution transformers represent the largest segment, followed by power transformers and specialty transformers. Each segment demonstrates distinct growth patterns and competitive dynamics.

By Voltage Rating:

By Application:

Distribution transformers represent the largest market category, driven by continuous replacement needs and grid expansion requirements. These units typically operate at medium voltage levels and serve local distribution networks. Market characteristics include standardized designs, competitive pricing, and emphasis on reliability and efficiency. The adoption rate of smart distribution transformers has increased by approximately 28% in recent years.

Power transformers serve high-voltage transmission applications and represent a smaller but higher-value market segment. Key features include custom designs, long lead times, and specialized installation requirements. This category benefits from grid modernization projects and renewable energy integration initiatives. Technology trends focus on improved efficiency, reduced environmental impact, and enhanced monitoring capabilities.

Specialty transformers address specific applications such as furnace transformers, rectifier transformers, and mobile substations. Market dynamics include premium pricing, specialized expertise requirements, and close customer relationships. This segment demonstrates resilience through economic cycles due to essential application requirements and limited supplier alternatives.

Utility companies benefit from improved grid reliability, reduced maintenance costs, and enhanced operational efficiency through modern transformer technologies. Smart monitoring capabilities enable predictive maintenance strategies that reduce unplanned outages and extend equipment life. Advanced transformer designs offer improved efficiency ratings that reduce energy losses and operational costs.

Industrial customers gain advantages through customized transformer solutions that meet specific operational requirements. Energy efficiency improvements of up to 15% compared to older units reduce operating costs and support sustainability objectives. Reliable power supply ensures continuous operations and minimizes production disruptions.

Manufacturers benefit from steady demand patterns, long-term customer relationships, and opportunities for technology innovation. Service revenue streams provide recurring income through maintenance contracts and upgrade services. Regional manufacturing strategies reduce supply chain risks and improve customer responsiveness.

Environmental stakeholders benefit from improved transformer efficiency, reduced energy losses, and environmentally friendly insulation materials. Recycling programs for end-of-life transformers support circular economy principles and reduce environmental impact.

Strengths:

Weaknesses:

Opportunities:

Threats:

Digital transformation represents the most significant trend reshaping the North America power transformer market. Smart transformers equipped with sensors, communication capabilities, and data analytics are becoming standard requirements rather than premium options. This trend enables predictive maintenance, real-time monitoring, and improved grid management capabilities.

Sustainability focus drives demand for environmentally friendly transformer designs, including bio-based insulation fluids, recyclable materials, and improved energy efficiency. Circular economy principles influence product design and end-of-life management strategies. Manufacturers increasingly emphasize lifecycle environmental impact and sustainable manufacturing processes.

Modular designs gain popularity for their flexibility, reduced installation time, and improved maintainability. Prefabricated substations and mobile transformer solutions address rapid deployment requirements and temporary applications. Customization capabilities enable manufacturers to address specific customer requirements while maintaining production efficiency.

Service integration becomes increasingly important, with manufacturers expanding beyond equipment supply to comprehensive lifecycle services. Digital service platforms enable remote monitoring, predictive analytics, and optimized maintenance scheduling.

Recent industry developments demonstrate the dynamic nature of the North America power transformer market. Manufacturing capacity expansion by major players reflects confidence in long-term market growth and desire to reduce supply chain dependencies. Several companies have announced significant investments in North American production facilities.

Technology partnerships between transformer manufacturers and digital technology companies accelerate innovation in smart grid applications. Utility pilot projects test advanced transformer technologies and provide valuable operational data for product development. These collaborations drive market evolution and establish new performance standards.

Regulatory developments include updated efficiency standards, environmental requirements, and grid interconnection rules that influence product specifications and market dynamics. MarkWide Research indicates that regulatory compliance costs have increased by approximately 18% over recent years, affecting pricing strategies and product development priorities.

Acquisition activity continues as companies seek to expand capabilities, access new markets, and achieve operational synergies. Strategic alliances enable smaller companies to compete effectively while providing larger organizations with specialized expertise and market access.

Strategic recommendations for market participants focus on adapting to evolving market conditions and capitalizing on emerging opportunities. Technology investment should prioritize digital capabilities, sustainability features, and modular designs that address changing customer requirements. Companies should develop comprehensive digital strategies that integrate products and services.

Market positioning strategies should emphasize total cost of ownership value propositions rather than initial price competition. Service capabilities become increasingly important for competitive differentiation and customer retention. Organizations should invest in service infrastructure, digital platforms, and technical expertise to support comprehensive customer solutions.

Supply chain optimization requires balancing cost efficiency with resilience and responsiveness. Regional manufacturing strategies reduce risks while improving customer service. Companies should develop flexible supply chain models that can adapt to changing market conditions and customer requirements.

Partnership strategies should focus on complementary capabilities, market access, and technology development. Utility relationships require long-term commitment and demonstrated value delivery. Organizations should invest in customer relationship management and technical support capabilities.

Market prospects for the North America power transformer sector remain positive, supported by fundamental infrastructure requirements and evolving technology trends. Growth projections indicate continued expansion at approximately 4.5% CAGR through the next decade, driven by infrastructure modernization, renewable energy integration, and electrification trends.

Technology evolution will continue reshaping market dynamics, with digital capabilities becoming standard features across all transformer categories. Artificial intelligence and machine learning applications will enhance predictive maintenance, optimize performance, and reduce operational costs. Advanced materials will improve efficiency, reduce environmental impact, and extend equipment life.

Market structure evolution may include further consolidation among manufacturers and increased vertical integration by utilities seeking greater supply chain control. Regional manufacturing trends will likely accelerate, supported by government policies and supply chain resilience considerations.

Regulatory environment will continue evolving, with increasing emphasis on cybersecurity, environmental performance, and grid resilience. International cooperation on standards and best practices will facilitate technology transfer and market development across North America.

The North America power transformer market represents a critical component of regional electrical infrastructure, characterized by steady demand growth, technological innovation, and evolving customer requirements. Market fundamentals remain strong, supported by aging infrastructure replacement needs, renewable energy integration, and grid modernization initiatives across the United States, Canada, and Mexico.

Key success factors for market participants include technology leadership, comprehensive service capabilities, regional manufacturing presence, and strong utility relationships. Digital transformation and sustainability considerations are reshaping competitive dynamics and creating new value propositions. Organizations that successfully adapt to these trends while maintaining operational excellence will achieve sustainable competitive advantages.

Future market development will be influenced by regulatory evolution, technology advancement, and changing customer expectations. Strategic positioning should emphasize total value delivery, lifecycle services, and innovative solutions that address specific regional challenges and opportunities. The market’s essential role in electrical infrastructure ensures continued relevance and growth potential despite economic cycles and industry challenges.

What is Power Transformer?

Power transformers are electrical devices used to transfer electrical energy between two or more circuits through electromagnetic induction. They are essential in power distribution systems, enabling the transmission of electricity over long distances and ensuring voltage levels are suitable for various applications.

What are the key players in the North America Power Transformer Market?

Key players in the North America Power Transformer Market include Siemens AG, General Electric, Schneider Electric, and ABB Ltd. These companies are known for their innovative solutions and extensive product portfolios in the power transformer sector, among others.

What are the main drivers of the North America Power Transformer Market?

The main drivers of the North America Power Transformer Market include the increasing demand for electricity, the expansion of renewable energy sources, and the need for grid modernization. These factors are pushing utilities to invest in advanced transformer technologies to enhance efficiency and reliability.

What challenges does the North America Power Transformer Market face?

The North America Power Transformer Market faces challenges such as the high cost of advanced transformer technologies and the complexity of integrating renewable energy sources into existing grids. Additionally, regulatory compliance and environmental concerns can hinder market growth.

What opportunities exist in the North America Power Transformer Market?

Opportunities in the North America Power Transformer Market include the growing trend towards smart grid technologies and the increasing investment in infrastructure upgrades. These developments are expected to drive demand for more efficient and reliable power transformers.

What trends are shaping the North America Power Transformer Market?

Trends shaping the North America Power Transformer Market include the adoption of digital technologies for monitoring and maintenance, the shift towards eco-friendly transformer designs, and the integration of energy storage systems. These trends are enhancing operational efficiency and sustainability in power distribution.

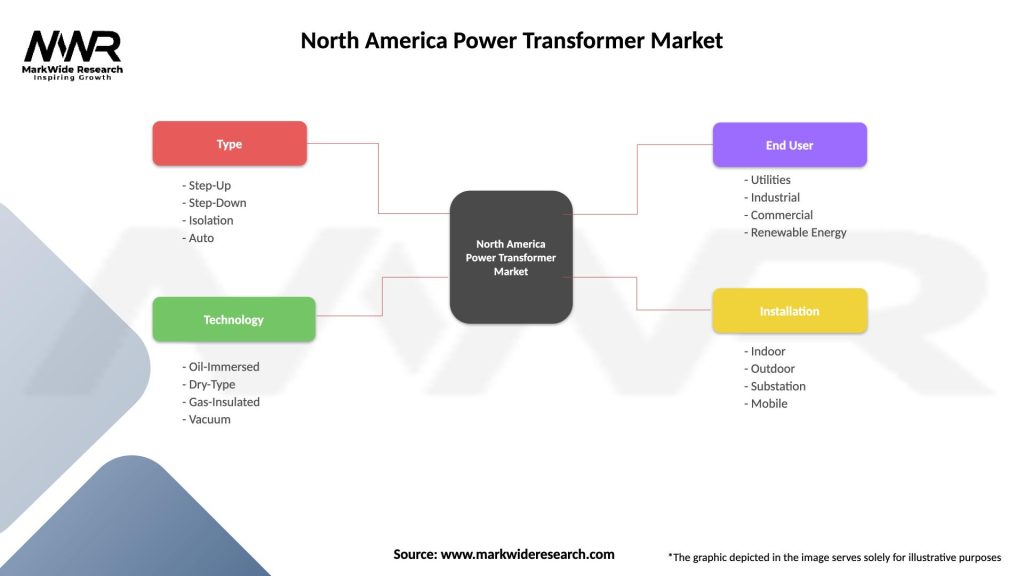

North America Power Transformer Market

| Segmentation Details | Description |

|---|---|

| Type | Step-Up, Step-Down, Isolation, Auto |

| Technology | Oil-Immersed, Dry-Type, Gas-Insulated, Vacuum |

| End User | Utilities, Industrial, Commercial, Renewable Energy |

| Installation | Indoor, Outdoor, Substation, Mobile |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the North America Power Transformer Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.