444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The India electric vehicle battery anode market represents a critical component of the nation’s rapidly expanding electric mobility ecosystem. As India accelerates its transition toward sustainable transportation solutions, the demand for high-performance battery anodes has experienced unprecedented growth. The market encompasses various anode materials including graphite-based anodes, silicon-enhanced anodes, and emerging lithium titanate oxide technologies that power electric vehicles across multiple segments.

Market dynamics indicate robust expansion driven by government initiatives, increasing environmental consciousness, and technological advancements in battery chemistry. The sector is experiencing significant momentum with a projected CAGR of 28.5% through the forecast period, reflecting the accelerating adoption of electric vehicles nationwide. Manufacturing capabilities are rapidly scaling to meet domestic demand while positioning India as a potential global hub for battery component production.

Regional distribution shows concentrated development in key automotive manufacturing states, with Maharashtra, Tamil Nadu, and Gujarat leading in both production capacity and research initiatives. The market benefits from strategic government policies including the Production Linked Incentive scheme and FAME II program, which collectively support domestic manufacturing and technology development in the electric vehicle battery supply chain.

The India electric vehicle battery anode market refers to the domestic industry focused on manufacturing, developing, and supplying anode materials specifically designed for electric vehicle battery applications within the Indian automotive ecosystem, encompassing both traditional graphite-based solutions and advanced silicon-enhanced technologies.

Anode materials serve as the negative electrode in lithium-ion batteries, playing a crucial role in energy storage and release during charging and discharging cycles. In the context of electric vehicles, these materials must deliver exceptional performance characteristics including high energy density, rapid charging capabilities, and extended cycle life to meet the demanding requirements of modern electric mobility applications.

Market scope encompasses various anode technologies ranging from conventional natural graphite and synthetic graphite to innovative silicon nanowires and silicon-graphite composites. The industry also includes emerging technologies such as lithium metal anodes and solid-state anode solutions that promise to revolutionize electric vehicle battery performance and safety standards.

India’s electric vehicle battery anode market stands at a transformative juncture, driven by ambitious national electrification goals and substantial investments in domestic manufacturing capabilities. The sector demonstrates remarkable growth potential with increasing localization of battery component production and strategic partnerships between domestic manufacturers and international technology providers.

Key market drivers include government policy support, declining battery costs, and growing consumer acceptance of electric vehicles across passenger and commercial segments. The market benefits from India’s position as a major automotive manufacturing hub, with established supply chains and skilled workforce capabilities that facilitate rapid scaling of anode production facilities.

Technology trends indicate a shift toward silicon-enhanced anode materials that offer superior energy density compared to traditional graphite solutions. Domestic manufacturers are investing heavily in research and development to develop indigenous anode technologies that can compete with international standards while meeting the specific requirements of Indian electric vehicle applications.

Market challenges include raw material dependency, technology transfer complexities, and the need for substantial capital investments in manufacturing infrastructure. However, these challenges are being addressed through strategic government initiatives, international collaborations, and increasing private sector participation in the electric vehicle battery ecosystem.

Government policy initiatives serve as the primary catalyst driving India’s electric vehicle battery anode market expansion. The National Electric Mobility Mission Plan and associated policy frameworks create a supportive environment for domestic battery component manufacturing, including substantial financial incentives for anode material production facilities.

Environmental regulations and emission norms are accelerating the transition toward electric mobility, directly increasing demand for high-performance battery anodes. The implementation of BS-VI emission standards and future carbon neutrality commitments create sustained demand for electric vehicle technologies and their critical components.

Cost competitiveness of electric vehicles is improving rapidly, driven by declining battery costs and economies of scale in anode material production. Technological advancements in anode manufacturing processes are reducing production costs while improving performance characteristics, making electric vehicles more accessible to mainstream consumers.

Infrastructure development including charging networks and battery recycling facilities supports market growth by addressing key barriers to electric vehicle adoption. The expansion of charging infrastructure increases consumer confidence in electric vehicles, thereby driving demand for battery components including advanced anode materials.

Industry partnerships between domestic manufacturers and international technology providers are accelerating knowledge transfer and manufacturing capability development. These collaborations enable rapid scaling of anode production capacity while ensuring access to cutting-edge battery technologies and manufacturing processes.

Raw material dependency represents a significant constraint for India’s electric vehicle battery anode market, particularly regarding high-quality natural graphite and synthetic graphite sourcing. The limited domestic availability of these critical materials creates supply chain vulnerabilities and cost pressures that impact overall market competitiveness.

Technology gaps in advanced anode manufacturing processes pose challenges for domestic producers seeking to compete with established international suppliers. The complexity of silicon-enhanced anode production and quality control systems requires substantial investments in research and development capabilities and specialized manufacturing equipment.

Capital intensity of anode manufacturing facilities creates barriers to entry for smaller players and requires significant upfront investments that may deter potential market participants. The need for clean room facilities, precision manufacturing equipment, and quality testing systems increases the financial threshold for market entry.

Skilled workforce availability poses challenges as the specialized nature of anode manufacturing requires technical expertise in materials science, electrochemistry, and advanced manufacturing processes. The relatively nascent state of India’s battery manufacturing ecosystem means limited availability of experienced professionals in these critical areas.

Quality standards and certification requirements for electric vehicle battery components create additional compliance costs and technical challenges for domestic manufacturers. Meeting international safety standards and performance specifications requires substantial investments in testing facilities and quality assurance systems.

Domestic manufacturing localization presents substantial opportunities as India seeks to reduce dependence on imported battery components. The government’s emphasis on Atmanirbhar Bharat creates favorable conditions for establishing comprehensive anode manufacturing capabilities that can serve both domestic and export markets.

Technology innovation in next-generation anode materials offers opportunities for Indian companies to develop proprietary solutions tailored to local market requirements. Silicon nanowire technology and graphene-enhanced anodes represent emerging areas where domestic research institutions and manufacturers can establish competitive advantages.

Export market potential exists as India’s manufacturing capabilities mature and cost competitiveness improves. Regional markets in Southeast Asia and Africa present opportunities for Indian anode material suppliers to expand beyond domestic demand and achieve economies of scale.

Recycling and circular economy initiatives create opportunities for developing sustainable anode material recovery and reprocessing capabilities. As electric vehicle adoption increases, the potential for battery recycling and anode material recovery becomes increasingly attractive from both environmental and economic perspectives.

Research collaborations between industry and academic institutions offer opportunities to develop indigenous anode technologies and manufacturing processes. Strategic partnerships with Indian Institutes of Technology and national research laboratories can accelerate innovation while building domestic technical capabilities.

Supply chain evolution is fundamentally reshaping India’s electric vehicle battery anode market as manufacturers seek to establish resilient and cost-effective sourcing strategies. The integration of upstream raw material processing with downstream anode manufacturing is creating vertically integrated supply chains that enhance cost competitiveness and quality control.

Technology convergence between traditional automotive manufacturing and advanced battery technologies is driving innovation in anode material applications. The adoption of Industry 4.0 technologies including artificial intelligence and machine learning in anode manufacturing processes is improving production efficiency and quality consistency.

Market consolidation trends are emerging as larger players acquire smaller manufacturers to achieve economies of scale and expand technological capabilities. This consolidation is creating more robust market participants capable of meeting the demanding requirements of large-scale electric vehicle production.

Customer requirements are evolving toward more sophisticated anode specifications including fast-charging capabilities, extended cycle life, and enhanced safety characteristics. These changing requirements are driving continuous innovation in anode material composition and manufacturing processes.

Regulatory landscape continues to evolve with new standards for battery performance, safety, and environmental impact. These regulatory changes create both challenges and opportunities for anode manufacturers to differentiate their products through superior compliance and performance characteristics.

Primary research methodology encompasses comprehensive interviews with key stakeholders across India’s electric vehicle battery anode value chain, including raw material suppliers, anode manufacturers, battery producers, and electric vehicle OEMs. These interviews provide insights into market dynamics, technology trends, and future growth prospects.

Secondary research involves extensive analysis of industry reports, government publications, patent databases, and academic research papers related to anode technologies and electric vehicle battery markets. This research provides quantitative data on market size, growth rates, and technological developments.

Market modeling techniques incorporate both bottom-up and top-down approaches to validate market size estimates and growth projections. The methodology considers factors including electric vehicle adoption rates, battery capacity requirements, and anode material consumption patterns to develop accurate market forecasts.

Expert validation processes involve consultation with industry experts, technology specialists, and market analysts to ensure the accuracy and relevance of research findings. This validation helps identify emerging trends and potential market disruptions that may impact future growth trajectories.

Data triangulation methods are employed to cross-verify information from multiple sources and ensure the reliability of market insights. This approach helps eliminate potential biases and provides a comprehensive view of market conditions and future prospects.

Western India leads the electric vehicle battery anode market with Maharashtra and Gujarat accounting for approximately 45% of domestic production capacity. The region benefits from established automotive manufacturing infrastructure, proximity to major ports for raw material imports, and supportive state government policies for electric vehicle component manufacturing.

Southern India represents a rapidly growing market segment with Tamil Nadu and Karnataka emerging as key manufacturing hubs. The region’s strength in electronics manufacturing and research institutions provides advantages for advanced anode technology development and high-precision manufacturing processes.

Northern India shows increasing activity in anode manufacturing with Haryana and Uttar Pradesh attracting investments from both domestic and international players. The region’s proximity to the national capital and major automotive markets creates strategic advantages for market access and policy engagement.

Eastern India presents emerging opportunities particularly in West Bengal and Odisha, where mineral resources and industrial infrastructure support potential anode material processing capabilities. The region’s access to graphite deposits and port facilities creates advantages for raw material sourcing and export activities.

Regional specialization is developing with different areas focusing on specific aspects of the anode value chain. Research and development activities are concentrated in technology hubs, while large-scale manufacturing is gravitating toward regions with established industrial infrastructure and supportive policy environments.

Market leadership in India’s electric vehicle battery anode sector is characterized by a mix of domestic manufacturers, international technology providers, and emerging startups focused on innovative anode solutions. The competitive environment is rapidly evolving as new players enter the market and existing participants expand their capabilities.

Strategic partnerships between domestic and international players are reshaping the competitive landscape, enabling technology transfer and rapid capability development. These collaborations often involve joint ventures, licensing agreements, and technical cooperation arrangements that accelerate market development.

Innovation focus among competitors centers on developing cost-effective manufacturing processes, improved anode performance characteristics, and sustainable production methods. Companies are investing heavily in research and development to create differentiated products that meet evolving market requirements.

By Material Type: The market segments into natural graphite anodes, synthetic graphite anodes, silicon-based anodes, and lithium titanate oxide anodes. Natural graphite currently dominates with 60% market share due to cost advantages, while silicon-enhanced solutions are gaining traction in premium applications.

By Vehicle Type: Segmentation includes passenger electric vehicles, commercial electric vehicles, two-wheelers, and three-wheelers. The two-wheeler segment represents the largest application area, accounting for approximately 55% of total demand due to India’s significant electric scooter and motorcycle market.

By Battery Type: The market divides into lithium-ion batteries, lithium iron phosphate batteries, and solid-state batteries. Lithium-ion applications dominate current demand, while solid-state technologies represent emerging opportunities for next-generation anode materials.

By End-Use Application: Applications span automotive OEMs, battery manufacturers, aftermarket replacement, and energy storage systems. Automotive OEM applications drive the majority of demand, while energy storage represents a rapidly growing segment.

By Manufacturing Process: Segmentation includes traditional powder metallurgy, chemical vapor deposition, sol-gel processing, and mechanical milling. Advanced manufacturing processes are gaining adoption for high-performance anode applications requiring superior quality and consistency.

Natural Graphite Anodes maintain market leadership due to established supply chains and cost competitiveness. These materials offer reliable performance characteristics suitable for mainstream electric vehicle applications, with ongoing improvements in particle size optimization and surface treatment technologies enhancing their performance capabilities.

Synthetic Graphite Anodes are gaining market share in premium applications where superior performance justifies higher costs. These materials offer enhanced cycle life, improved fast-charging capabilities, and better temperature stability compared to natural graphite alternatives.

Silicon-Enhanced Anodes represent the fastest-growing category with significant potential for market disruption. These advanced materials offer substantially higher energy density but require sophisticated manufacturing processes and specialized handling techniques to achieve commercial viability.

Lithium Titanate Anodes serve niche applications requiring ultra-fast charging and exceptional safety characteristics. While currently representing a small market segment, these materials show promise for commercial vehicle applications and energy storage systems.

Composite Anode Materials combining multiple technologies are emerging as solutions that balance performance, cost, and manufacturing complexity. These hybrid approaches offer opportunities for domestic manufacturers to develop differentiated products tailored to specific market requirements.

Manufacturing Cost Reduction: Domestic anode production enables significant cost savings through reduced import dependencies, lower transportation costs, and optimized supply chain management. Local manufacturing also provides better inventory control and reduced working capital requirements.

Technology Access: Industry participants gain access to cutting-edge anode technologies through strategic partnerships, licensing agreements, and collaborative research initiatives. This access accelerates product development timelines and enhances competitive positioning in the market.

Market Proximity: Local manufacturing provides closer proximity to end customers, enabling better customer service, faster response times, and customized product development. This proximity also facilitates better understanding of local market requirements and preferences.

Policy Support: Industry participants benefit from government incentives, tax advantages, and policy support designed to promote domestic manufacturing. These benefits include production-linked incentives, capital subsidies, and preferential procurement policies.

Skill Development: The growing industry creates opportunities for workforce development and skill building in advanced manufacturing technologies. This human capital development benefits both individual participants and the broader industrial ecosystem.

Export Opportunities: Established domestic capabilities create platforms for export market development, enabling participants to achieve economies of scale and diversify revenue streams beyond the domestic market.

Strengths:

Weaknesses:

Opportunities:

Threats:

Silicon Integration represents a transformative trend as manufacturers increasingly incorporate silicon nanoparticles and silicon nanowires into traditional graphite anodes to achieve higher energy density. This trend is driven by the need for longer-range electric vehicles and more compact battery systems.

Sustainable Manufacturing is gaining prominence with companies focusing on environmentally friendly production processes and recyclable anode materials. This trend aligns with broader sustainability goals and regulatory requirements for reduced environmental impact in battery manufacturing.

Localization Acceleration shows domestic manufacturers rapidly expanding production capabilities to reduce import dependencies. According to MarkWide Research analysis, domestic production capacity is expected to increase significantly, supporting India’s goal of becoming self-reliant in battery component manufacturing.

Advanced Manufacturing Technologies including automated production systems, precision coating techniques, and real-time quality monitoring are being adopted to improve product consistency and reduce manufacturing costs. These technologies enable higher production volumes while maintaining stringent quality standards.

Customization Trends show increasing demand for application-specific anode materials tailored to different electric vehicle segments. Two-wheeler applications require different performance characteristics compared to passenger cars or commercial vehicles, driving product diversification.

Research Intensification in next-generation anode technologies including solid-state anodes, lithium metal anodes, and graphene-enhanced materials is accelerating as companies seek competitive advantages through technological innovation.

Manufacturing Expansion: Several major announcements of new anode manufacturing facilities across India, with combined capacity additions representing substantial increases in domestic production capability. These expansions are supported by both domestic and international investments.

Technology Partnerships: Strategic alliances between Indian companies and international technology providers are facilitating rapid technology transfer and capability development. These partnerships often include joint research initiatives and manufacturing collaboration agreements.

Government Initiatives: Launch of specialized schemes for battery component manufacturing, including dedicated funding for anode material production facilities and research and development activities. These initiatives provide both financial support and policy framework clarity.

Research Breakthroughs: Indian research institutions and companies are achieving significant milestones in indigenous anode technology development, including patents for novel materials and manufacturing processes that could provide competitive advantages.

Supply Chain Development: Establishment of comprehensive supply chains for anode materials, including upstream raw material processing capabilities and downstream integration with battery manufacturers and electric vehicle producers.

Quality Certifications: Achievement of international quality certifications by domestic manufacturers, enabling participation in global supply chains and export market opportunities. These certifications validate the quality and reliability of Indian-manufactured anode materials.

Technology Investment: Industry participants should prioritize investments in advanced anode technologies, particularly silicon-enhanced solutions that offer superior performance characteristics. Early adoption of these technologies will provide competitive advantages as market requirements evolve toward higher energy density applications.

Supply Chain Security: Companies should develop robust supply chain strategies that reduce dependence on single-source suppliers and geographical regions. Diversified sourcing strategies and strategic inventory management will help mitigate supply chain risks and cost volatility.

Quality Excellence: Establishing world-class quality control systems and obtaining international certifications should be immediate priorities for manufacturers seeking to compete in global markets. Quality consistency and reliability are critical success factors in the battery industry.

Research Collaboration: Strategic partnerships with academic institutions, research organizations, and technology companies will accelerate innovation and technology development. These collaborations can provide access to cutting-edge research while sharing development costs and risks.

Market Diversification: Companies should explore opportunities beyond traditional automotive applications, including energy storage systems, consumer electronics, and industrial applications. Market diversification reduces dependence on single market segments and provides growth opportunities.

Sustainability Focus: Incorporating sustainability considerations into product development and manufacturing processes will become increasingly important as environmental regulations strengthen and customer preferences shift toward eco-friendly solutions.

Market expansion prospects for India’s electric vehicle battery anode market remain exceptionally positive, driven by accelerating electric vehicle adoption and supportive government policies. MWR projects continued robust growth with expanding domestic manufacturing capabilities and increasing technology sophistication.

Technology evolution will see significant advancement in silicon-based anode materials and solid-state technologies that promise to revolutionize battery performance. These technological developments will create new market opportunities while potentially disrupting existing product categories.

Manufacturing scale is expected to increase dramatically with multiple gigafactory projects under development and existing facilities expanding capacity. This scaling will improve cost competitiveness and position India as a significant player in global anode material supply chains.

Export potential will materialize as domestic capabilities mature and cost competitiveness improves. Regional markets in Southeast Asia and Africa present attractive opportunities for Indian anode material suppliers to expand beyond domestic demand.

Innovation acceleration through increased research and development investments will drive the development of indigenous technologies and specialized products tailored to Indian market requirements. This innovation will reduce technology dependence and create competitive advantages.

Sustainability integration will become increasingly important with growing emphasis on circular economy principles, recycling capabilities, and environmentally responsible manufacturing processes. Companies that successfully integrate sustainability will gain competitive advantages in both domestic and export markets.

India’s electric vehicle battery anode market represents a dynamic and rapidly evolving sector with substantial growth potential driven by government support, technological advancement, and increasing electric vehicle adoption. The market demonstrates strong fundamentals with expanding domestic manufacturing capabilities, strategic international partnerships, and growing technological sophistication.

Key success factors for market participants include technology innovation, quality excellence, supply chain security, and strategic market positioning. Companies that successfully navigate these requirements while building sustainable competitive advantages will benefit from the market’s substantial growth opportunities.

Future prospects remain highly positive with continued policy support, accelerating electric vehicle adoption, and expanding export opportunities creating a favorable environment for sustained market growth. The sector’s evolution toward advanced technologies and sustainable manufacturing practices positions it as a critical component of India’s clean energy transition and industrial development strategy.

What is Electric Vehicle Battery Anode?

Electric Vehicle Battery Anode refers to the component in a battery that allows the flow of lithium ions during the charging and discharging process. It plays a crucial role in the performance and efficiency of electric vehicle batteries.

What are the key players in the India Electric Vehicle Battery Anode Market?

Key players in the India Electric Vehicle Battery Anode Market include companies like Amprius Energy, BASF, and LG Chem, which are involved in the development and production of advanced anode materials for electric vehicle batteries, among others.

What are the growth factors driving the India Electric Vehicle Battery Anode Market?

The growth of the India Electric Vehicle Battery Anode Market is driven by increasing demand for electric vehicles, advancements in battery technology, and government initiatives promoting sustainable transportation solutions.

What challenges does the India Electric Vehicle Battery Anode Market face?

Challenges in the India Electric Vehicle Battery Anode Market include high production costs, supply chain disruptions for raw materials, and the need for continuous innovation to improve battery performance and longevity.

What opportunities exist in the India Electric Vehicle Battery Anode Market?

Opportunities in the India Electric Vehicle Battery Anode Market include the potential for new material innovations, partnerships between automotive manufacturers and battery producers, and the expansion of charging infrastructure to support electric vehicle adoption.

What trends are shaping the India Electric Vehicle Battery Anode Market?

Trends in the India Electric Vehicle Battery Anode Market include the shift towards silicon-based anodes for higher energy density, the integration of recycling processes for battery materials, and the increasing focus on sustainability and environmental impact in battery production.

India Electric Vehicle Battery Anode Market

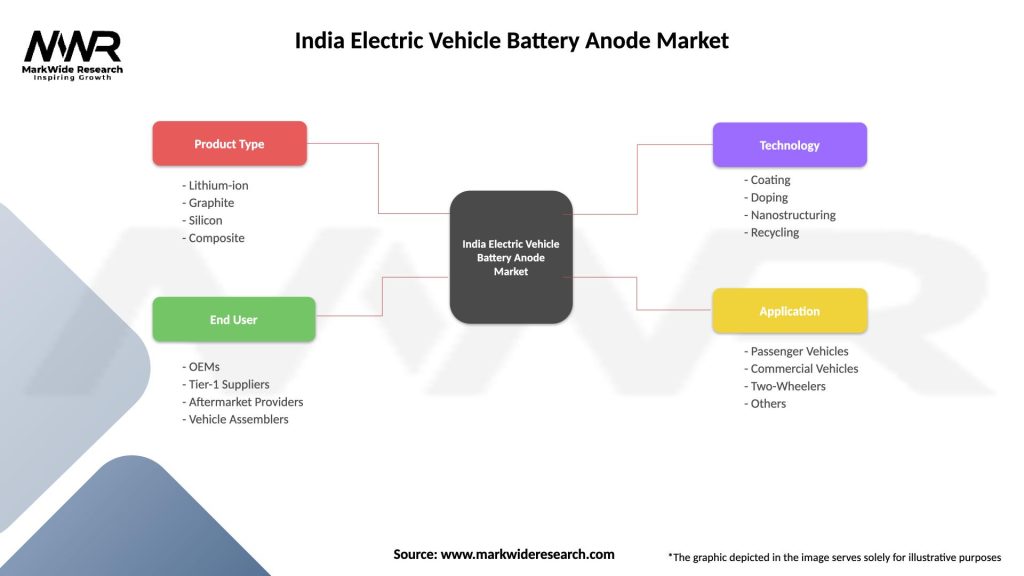

| Segmentation Details | Description |

|---|---|

| Product Type | Lithium-ion, Graphite, Silicon, Composite |

| End User | OEMs, Tier-1 Suppliers, Aftermarket Providers, Vehicle Assemblers |

| Technology | Coating, Doping, Nanostructuring, Recycling |

| Application | Passenger Vehicles, Commercial Vehicles, Two-Wheelers, Others |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the India Electric Vehicle Battery Anode Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.