444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

The Asia-Pacific data center storage market represents one of the most dynamic and rapidly expanding segments in the global technology infrastructure landscape. This region has emerged as a critical hub for digital transformation, cloud computing adoption, and enterprise data management solutions. Market dynamics indicate substantial growth driven by increasing digitalization across industries, rising cloud service adoption, and the proliferation of data-intensive applications including artificial intelligence, machine learning, and Internet of Things (IoT) implementations.

Regional growth patterns demonstrate remarkable expansion, with the market experiencing a robust compound annual growth rate (CAGR) of 12.8% over the forecast period. This growth trajectory reflects the region’s strategic importance in global data center operations and storage infrastructure development. Key contributing factors include massive investments in hyperscale data centers, government initiatives supporting digital infrastructure, and the increasing demand for edge computing solutions across diverse industry verticals.

Geographic distribution shows significant concentration in major economies including China, Japan, India, South Korea, and Australia, with emerging markets like Southeast Asian countries gaining substantial momentum. The region’s storage infrastructure encompasses traditional storage area networks (SAN), network-attached storage (NAS), direct-attached storage (DAS), and advanced software-defined storage solutions that are reshaping the technological landscape.

The Asia-Pacific data center storage market refers to the comprehensive ecosystem of storage hardware, software, and services deployed within data center facilities across the Asia-Pacific region to manage, store, and retrieve digital information efficiently. This market encompasses various storage technologies, architectures, and solutions designed to meet the growing data storage requirements of enterprises, cloud service providers, telecommunications companies, and government organizations operating in this dynamic region.

Storage technologies within this market include traditional magnetic disk drives, solid-state drives (SSDs), hybrid storage systems, and emerging technologies such as storage-class memory and DNA-based storage solutions. The market also covers storage management software, data protection solutions, backup and recovery systems, and cloud-integrated storage platforms that enable seamless data accessibility and management across distributed computing environments.

Market participants range from global technology giants to regional specialists, providing comprehensive storage solutions that address specific requirements of Asia-Pacific enterprises. These solutions support critical business operations, enable digital transformation initiatives, and facilitate compliance with regional data sovereignty and privacy regulations that are increasingly important in the Asia-Pacific business environment.

Strategic market positioning reveals the Asia-Pacific data center storage market as a cornerstone of the region’s digital infrastructure development. The market demonstrates exceptional resilience and growth potential, driven by accelerating digital transformation initiatives across both developed and emerging economies. Investment patterns show significant capital allocation toward next-generation storage technologies, with approximately 68% of enterprises planning substantial storage infrastructure upgrades within the next three years.

Technology adoption trends highlight the rapid migration from traditional storage architectures to software-defined and cloud-native solutions. This transformation is particularly pronounced in sectors such as financial services, healthcare, manufacturing, and telecommunications, where data-driven decision making has become essential for competitive advantage. Market segmentation reveals diverse application areas including enterprise data management, cloud storage services, content delivery networks, and emerging use cases in artificial intelligence and machine learning workloads.

Competitive dynamics showcase a healthy mix of established global vendors and innovative regional players, creating a vibrant ecosystem that drives technological advancement and competitive pricing. The market benefits from strong government support for digital infrastructure development, favorable regulatory frameworks, and increasing foreign direct investment in technology sectors across the Asia-Pacific region.

Fundamental market drivers demonstrate the critical role of data center storage in supporting the region’s digital economy growth. The following key insights provide comprehensive understanding of market dynamics:

Technology evolution patterns indicate significant shifts toward software-defined storage architectures, hybrid cloud deployments, and intelligent storage management systems that optimize performance while reducing operational costs.

Digital transformation initiatives across Asia-Pacific enterprises serve as the primary catalyst for data center storage market expansion. Organizations are increasingly recognizing data as a strategic asset, driving investments in advanced storage infrastructure that can support analytics, artificial intelligence, and real-time decision-making capabilities. Government digitalization programs in countries like India, China, and Singapore are accelerating the adoption of digital services, creating substantial demand for underlying storage infrastructure.

Cloud service proliferation represents another significant driver, with major cloud providers establishing extensive data center networks across the region. This expansion requires massive storage capacity to support growing customer workloads and data retention requirements. Hyperscale data center development has become particularly prominent, with these facilities requiring petabyte-scale storage systems that can scale efficiently while maintaining high performance and reliability standards.

Regulatory compliance requirements are increasingly driving storage infrastructure investments, as governments implement data sovereignty laws requiring local data storage. Industry-specific regulations in sectors such as banking, healthcare, and telecommunications mandate secure, auditable storage systems that meet strict compliance standards. Additionally, the growing emphasis on data privacy and protection is driving demand for advanced storage security features and encryption capabilities.

Emerging technology adoption including Internet of Things deployments, smart city initiatives, and Industry 4.0 implementations generate unprecedented data volumes that require sophisticated storage solutions. These applications often demand real-time data processing capabilities, driving adoption of high-performance storage technologies and edge computing architectures.

Capital investment requirements present significant challenges for many organizations considering data center storage infrastructure upgrades. The substantial upfront costs associated with enterprise-grade storage systems, particularly high-performance solutions, can strain budgets and delay implementation timelines. Total cost of ownership considerations including ongoing maintenance, power consumption, and skilled personnel requirements add complexity to investment decisions.

Technical complexity challenges associated with modern storage architectures require specialized expertise that may be scarce in certain markets. The integration of software-defined storage, hybrid cloud environments, and advanced data management tools demands skilled professionals who understand both traditional storage concepts and emerging technologies. Skills shortage in areas such as storage administration, data architecture, and cloud integration can limit deployment success and operational efficiency.

Data security concerns continue to influence storage infrastructure decisions, particularly in industries handling sensitive information. Organizations must balance accessibility requirements with security mandates, often resulting in complex storage architectures that can increase costs and operational complexity. Cybersecurity threats targeting storage infrastructure require continuous investment in security technologies and monitoring capabilities.

Vendor lock-in risks associated with proprietary storage solutions can limit flexibility and increase long-term costs. Organizations may hesitate to commit to specific storage platforms without clear migration paths or interoperability standards. Technology obsolescence concerns also influence purchasing decisions, as rapid technological evolution can render storage investments outdated more quickly than anticipated.

Artificial intelligence integration presents substantial opportunities for storage vendors to develop specialized solutions optimized for AI and machine learning workloads. These applications require storage systems that can handle massive datasets while providing high-speed access for training and inference operations. AI-driven storage management capabilities that automatically optimize performance, predict failures, and manage capacity allocation represent significant value propositions for enterprise customers.

Edge computing expansion creates demand for distributed storage architectures that can support low-latency applications across geographically dispersed locations. This trend is particularly relevant in the Asia-Pacific region, where diverse geographic conditions and varying infrastructure maturity levels require flexible storage deployment models. 5G network rollouts will further accelerate edge computing adoption, creating additional storage infrastructure requirements.

Sustainability initiatives are driving demand for energy-efficient storage solutions that can reduce data center power consumption and environmental impact. Organizations are increasingly prioritizing green technology investments, creating opportunities for vendors offering environmentally friendly storage systems. Circular economy principles are also influencing storage lifecycle management, with growing interest in refurbishment, recycling, and sustainable disposal programs.

Industry-specific solutions represent significant growth opportunities, as different sectors have unique storage requirements that generic solutions may not address effectively. Healthcare organizations need HIPAA-compliant storage systems, financial institutions require high-security solutions, and manufacturing companies need industrial-grade storage for operational technology environments. Vertical market specialization allows vendors to command premium pricing while providing superior value to customers.

Supply chain evolution within the Asia-Pacific data center storage market reflects broader technological and economic trends affecting the region. Manufacturing capabilities concentrated in countries like China, South Korea, and Taiwan provide cost advantages while enabling rapid scaling of production capacity. Regional supply chains are becoming increasingly important as organizations seek to reduce dependency on single-source suppliers and improve supply chain resilience.

Competitive intensity continues to drive innovation and pricing optimization across the market. Established global vendors compete with emerging regional players, creating a dynamic environment that benefits customers through improved technology offerings and competitive pricing structures. Partnership strategies between storage vendors, system integrators, and cloud service providers are reshaping market dynamics and creating new go-to-market approaches.

Technology convergence trends are blurring traditional boundaries between storage, compute, and networking infrastructure. Hyper-converged infrastructure solutions that integrate storage with other data center components are gaining traction, particularly among mid-market customers seeking simplified deployment and management. Software-defined approaches are enabling greater flexibility and cost optimization while reducing dependence on proprietary hardware platforms.

Customer buying patterns are evolving toward consumption-based models that align storage costs with actual usage patterns. This shift reflects broader trends toward operational expenditure models and cloud-like consumption of on-premises infrastructure. As-a-service delivery models are becoming increasingly popular, allowing organizations to access enterprise-grade storage capabilities without large capital investments.

Comprehensive market analysis employed multiple research methodologies to ensure accurate and reliable insights into the Asia-Pacific data center storage market. Primary research activities included extensive interviews with industry executives, technology vendors, system integrators, and end-user organizations across major Asia-Pacific markets. Survey methodologies captured quantitative data on market trends, technology adoption patterns, and investment priorities from a representative sample of market participants.

Secondary research activities involved analysis of industry reports, financial statements, regulatory filings, and technology specifications from leading storage vendors and data center operators. Market sizing and forecasting utilized multiple data sources to triangulate market estimates and validate growth projections. Industry expert consultations provided additional validation and insights into emerging trends and market dynamics.

Data validation processes ensured accuracy and reliability of market estimates through cross-referencing multiple sources and applying statistical analysis techniques. Regional market analysis incorporated country-specific economic indicators, technology adoption rates, and regulatory frameworks to provide granular insights into local market conditions. Forecast modeling utilized both bottom-up and top-down approaches to project market growth across different segments and geographic regions.

Quality assurance measures included peer review processes, expert validation sessions, and continuous monitoring of market developments to ensure research findings remain current and accurate. The methodology incorporated feedback from industry stakeholders to refine analysis and improve the relevance of insights for market participants.

China dominates the Asia-Pacific data center storage market with approximately 42% market share, driven by massive investments in digital infrastructure and the world’s largest internet user base. The country’s focus on technological self-sufficiency has accelerated domestic storage technology development while creating substantial demand for advanced storage solutions. Government initiatives including the Digital China strategy and New Infrastructure plan are driving significant investments in data center facilities and storage infrastructure.

Japan represents the second-largest market, characterized by high technology adoption rates and sophisticated enterprise requirements. Japanese organizations prioritize reliability and performance, driving demand for premium storage solutions and advanced data protection capabilities. Industry 4.0 initiatives in manufacturing and automotive sectors are creating substantial storage infrastructure requirements for operational technology applications.

India demonstrates the highest growth potential with rapid digitalization across sectors and government initiatives promoting digital services adoption. The country’s large population and growing internet penetration create substantial data generation and storage requirements. Data localization regulations are driving investments in domestic data center infrastructure and storage capabilities.

South Korea and Australia represent mature markets with high technology adoption rates and sophisticated storage infrastructure requirements. Both countries serve as regional hubs for multinational corporations and cloud service providers, driving demand for enterprise-grade storage solutions. Southeast Asian markets including Singapore, Thailand, and Malaysia are experiencing rapid growth driven by digital transformation initiatives and increasing foreign investment in technology infrastructure.

Market leadership in the Asia-Pacific data center storage sector is characterized by intense competition between global technology giants and innovative regional players. The competitive environment drives continuous innovation and competitive pricing while providing customers with diverse solution options.

Competitive strategies include technology innovation, strategic partnerships, regional market expansion, and development of industry-specific solutions. Vendors are increasingly focusing on software-defined capabilities, cloud integration, and artificial intelligence-driven management features to differentiate their offerings.

Technology-based segmentation reveals diverse storage architectures serving different performance and cost requirements across the Asia-Pacific market:

By Storage Type:

By Storage Medium:

By End-User Industry:

Enterprise storage solutions dominate the Asia-Pacific market, driven by large organizations’ requirements for high-performance, scalable storage infrastructure. These solutions typically feature advanced data protection capabilities, comprehensive management tools, and integration with existing enterprise IT environments. Performance optimization remains a critical consideration, with organizations increasingly adopting all-flash storage arrays to support demanding applications and reduce latency.

Cloud storage integration has become essential for modern storage architectures, with hybrid cloud deployments gaining significant traction across the region. Organizations are implementing storage solutions that seamlessly integrate with public cloud services while maintaining on-premises control over sensitive data. Multi-cloud strategies are driving demand for storage platforms that can operate across different cloud environments without vendor lock-in.

Software-defined storage adoption is accelerating as organizations seek greater flexibility and cost optimization. These solutions enable storage resource pooling, automated management, and policy-driven optimization that can significantly reduce operational overhead. Container-native storage is emerging as a critical requirement for organizations adopting microservices architectures and DevOps practices.

Edge storage requirements are creating new market categories as organizations deploy distributed computing architectures. These solutions must operate in challenging environments while providing reliable data storage and processing capabilities. Ruggedized storage systems designed for industrial and outdoor deployments represent a growing market segment with specialized requirements.

Technology vendors benefit from the expanding Asia-Pacific data center storage market through increased revenue opportunities and market share growth potential. The region’s diverse economic landscape provides multiple market entry strategies and customer segments, enabling vendors to optimize their go-to-market approaches. Innovation opportunities in emerging technologies such as artificial intelligence, edge computing, and 5G networks create competitive advantages for vendors investing in next-generation storage solutions.

System integrators and channel partners gain access to growing professional services opportunities as organizations require assistance with storage infrastructure design, implementation, and management. The complexity of modern storage architectures creates demand for specialized expertise and ongoing support services. Recurring revenue models through managed services and support contracts provide stable income streams and deeper customer relationships.

End-user organizations benefit from improved storage performance, reduced costs, and enhanced data management capabilities that enable digital transformation initiatives. Modern storage solutions provide better scalability, reliability, and security compared to legacy systems while offering cloud-like consumption models. Operational efficiency gains through automated management and intelligent optimization reduce IT overhead and improve resource utilization.

Cloud service providers can leverage advanced storage infrastructure to deliver superior services while optimizing operational costs. High-performance storage enables better customer experiences and supports premium service offerings that command higher margins. Competitive differentiation through storage performance and reliability helps providers attract and retain enterprise customers in competitive markets.

Strengths:

Weaknesses:

Opportunities:

Threats:

Artificial intelligence integration is transforming data center storage management through intelligent optimization, predictive maintenance, and automated capacity planning. AI-driven storage systems can analyze usage patterns, predict performance bottlenecks, and automatically optimize resource allocation to improve efficiency and reduce costs. Machine learning algorithms enable proactive problem identification and resolution, reducing downtime and improving overall system reliability.

Sustainability initiatives are driving adoption of energy-efficient storage technologies and environmentally responsible data center practices. Organizations are increasingly prioritizing green technology investments that reduce power consumption and environmental impact while maintaining performance requirements. Circular economy principles are influencing storage lifecycle management, with growing emphasis on equipment refurbishment, recycling, and sustainable disposal practices.

Edge computing proliferation is creating demand for distributed storage architectures that can support low-latency applications across geographically dispersed locations. This trend is particularly relevant for applications such as autonomous vehicles, industrial IoT, and real-time analytics that require immediate data processing capabilities. Micro data centers and edge storage solutions are becoming essential components of modern IT infrastructure.

Container and microservices adoption is driving demand for container-native storage solutions that can support dynamic, scalable application architectures. These storage systems must provide persistent data storage for containerized applications while supporting rapid scaling and deployment patterns. Kubernetes integration has become a critical requirement for enterprise storage solutions targeting modern application environments.

Strategic partnerships between storage vendors and cloud service providers are reshaping market dynamics and creating new hybrid deployment models. These collaborations enable seamless integration between on-premises storage infrastructure and public cloud services, providing customers with greater flexibility and choice. Technology alliances are also driving innovation in areas such as data protection, disaster recovery, and multi-cloud management.

Acquisition activities continue to consolidate the market as larger vendors acquire specialized technology companies and regional players to expand their capabilities and market reach. Recent acquisitions have focused on software-defined storage, data management, and artificial intelligence technologies that enhance storage platform capabilities. Market consolidation is creating stronger competitive positions while potentially reducing customer choice in certain segments.

Product innovation cycles are accelerating as vendors compete to deliver next-generation storage capabilities that address emerging customer requirements. Recent product launches have emphasized performance improvements, simplified management, and enhanced cloud integration capabilities. Technology roadmaps indicate continued focus on artificial intelligence, sustainability, and edge computing applications.

Regulatory developments across Asia-Pacific countries are influencing storage infrastructure requirements, particularly regarding data sovereignty and privacy protection. New regulations require organizations to implement specific data handling and storage practices, creating demand for compliant storage solutions. Compliance automation features are becoming essential capabilities for enterprise storage platforms operating in regulated industries.

MarkWide Research recommends that organizations prioritize storage infrastructure investments that align with long-term digital transformation strategies rather than focusing solely on immediate cost optimization. The rapid pace of technological change requires storage platforms that can adapt to evolving requirements while providing migration paths to future technologies. Strategic planning should incorporate emerging trends such as artificial intelligence, edge computing, and sustainability requirements.

Vendor selection criteria should emphasize software capabilities, cloud integration, and ecosystem partnerships rather than focusing primarily on hardware specifications. Modern storage environments require comprehensive management tools, automation capabilities, and seamless integration with existing IT infrastructure. Total cost of ownership analysis should include operational efficiency gains and productivity improvements enabled by advanced storage features.

Skills development initiatives are essential for organizations implementing advanced storage technologies, as the complexity of modern storage architectures requires specialized expertise. Investment in training programs, certification courses, and knowledge transfer activities can significantly improve deployment success and operational efficiency. Partnership strategies with experienced system integrators and managed service providers can help bridge skills gaps while accelerating implementation timelines.

Risk management strategies should address cybersecurity threats, vendor lock-in risks, and technology obsolescence concerns through diversified sourcing, comprehensive security measures, and flexible architecture designs. Organizations should also consider geographic and regulatory risks when planning storage infrastructure investments across different Asia-Pacific markets.

Market growth projections indicate continued expansion of the Asia-Pacific data center storage market, with particularly strong growth expected in emerging economies and edge computing applications. The market is projected to maintain a robust CAGR of 12.8% through the forecast period, driven by accelerating digital transformation initiatives and increasing data generation across industries. Technology evolution will continue to favor software-defined solutions, artificial intelligence integration, and sustainable storage architectures.

Emerging technologies including quantum computing, DNA storage, and advanced memory technologies may begin to influence market dynamics in the latter part of the forecast period. While these technologies remain largely experimental, early adoption in research and specialized applications could create new market segments and competitive dynamics. Innovation investments by leading vendors suggest continued focus on breakthrough technologies that could transform storage architectures.

Regional market development will likely see continued growth in China and India, while Southeast Asian markets emerge as significant growth drivers. Government initiatives supporting digital infrastructure development will continue to influence market expansion, particularly in countries implementing smart city and Industry 4.0 programs. Cross-border data flows and regional integration initiatives may create new opportunities for storage infrastructure providers.

Industry convergence trends will blur traditional boundaries between storage, compute, and networking infrastructure, creating integrated solutions that simplify deployment and management. The rise of composable infrastructure and disaggregated architectures will enable more flexible and efficient resource utilization. As-a-service delivery models will become increasingly prevalent, changing how organizations consume and pay for storage infrastructure.

The Asia-Pacific data center storage market represents a dynamic and rapidly evolving sector that plays a critical role in supporting the region’s digital transformation initiatives. With strong growth prospects driven by increasing digitalization, cloud adoption, and emerging technology implementations, the market offers substantial opportunities for vendors, service providers, and end-user organizations. Regional diversity creates multiple market entry strategies and customer segments, while government support for digital infrastructure development provides favorable conditions for market expansion.

Technology trends toward software-defined storage, artificial intelligence integration, and edge computing architectures are reshaping market dynamics and creating new competitive advantages for innovative vendors. Organizations that invest in modern storage infrastructure will be better positioned to capitalize on digital transformation opportunities while meeting evolving customer expectations and regulatory requirements. Strategic partnerships and ecosystem collaboration will become increasingly important for success in this complex and rapidly changing market environment.

The market’s future success will depend on addressing key challenges including skills shortages, cybersecurity threats, and regulatory complexity while capitalizing on opportunities in artificial intelligence, 5G networks, and sustainability initiatives. Market participants who can navigate these challenges while delivering innovative, cost-effective solutions will be well-positioned to capture significant value in this expanding market. The Asia-Pacific data center storage market will continue to serve as a cornerstone of the region’s digital infrastructure, enabling economic growth and technological advancement across diverse industries and applications.

What is Data Center Storage?

Data Center Storage refers to the systems and technologies used to store, manage, and protect data in data centers. This includes various storage solutions such as hard disk drives, solid-state drives, and cloud storage services that support enterprise applications and data management needs.

What are the key players in the Asia-Pacific Data Center Storage Market?

Key players in the Asia-Pacific Data Center Storage Market include Dell Technologies, Hewlett Packard Enterprise, IBM, and NetApp, among others. These companies provide a range of storage solutions tailored to meet the demands of data-intensive applications and cloud computing.

What are the main drivers of the Asia-Pacific Data Center Storage Market?

The main drivers of the Asia-Pacific Data Center Storage Market include the increasing demand for data storage due to the growth of cloud computing, the rise of big data analytics, and the need for enhanced data security. Additionally, the expansion of digital services across various industries fuels the need for robust storage solutions.

What challenges does the Asia-Pacific Data Center Storage Market face?

The Asia-Pacific Data Center Storage Market faces challenges such as the high costs associated with advanced storage technologies and the complexity of data management. Additionally, concerns regarding data privacy and compliance with regulations can hinder market growth.

What opportunities exist in the Asia-Pacific Data Center Storage Market?

Opportunities in the Asia-Pacific Data Center Storage Market include the growing adoption of artificial intelligence and machine learning for data management, as well as the increasing shift towards hybrid cloud solutions. These trends present avenues for innovation and expansion in storage technologies.

What trends are shaping the Asia-Pacific Data Center Storage Market?

Trends shaping the Asia-Pacific Data Center Storage Market include the rise of software-defined storage solutions, the integration of edge computing, and the increasing focus on sustainability in data center operations. These trends are driving advancements in storage efficiency and performance.

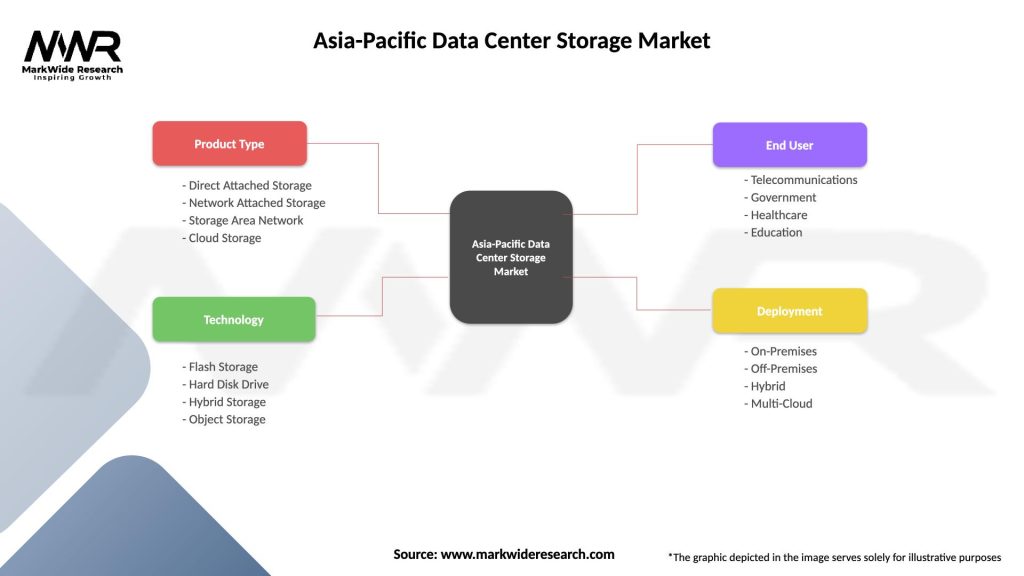

Asia-Pacific Data Center Storage Market

| Segmentation Details | Description |

|---|---|

| Product Type | Direct Attached Storage, Network Attached Storage, Storage Area Network, Cloud Storage |

| Technology | Flash Storage, Hard Disk Drive, Hybrid Storage, Object Storage |

| End User | Telecommunications, Government, Healthcare, Education |

| Deployment | On-Premises, Off-Premises, Hybrid, Multi-Cloud |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the Asia-Pacific Data Center Storage Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.