444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

India’s oil and gas upstream market represents one of the most dynamic and rapidly evolving energy sectors in the Asia-Pacific region. The upstream segment encompasses exploration, development, and production activities across conventional and unconventional hydrocarbon resources. Market dynamics indicate substantial growth potential driven by increasing energy demand, government policy support, and technological advancements in exploration and production techniques.

The sector has witnessed significant transformation over the past decade, with enhanced focus on domestic production to reduce import dependency. Government initiatives including the Hydrocarbon Exploration and Licensing Policy (HELP) and Open Acreage Licensing Policy (OALP) have created favorable conditions for both domestic and international players. Production efficiency has improved by approximately 23% over the last five years through advanced drilling technologies and enhanced oil recovery methods.

Regional distribution shows concentrated activity in key basins including the Mumbai High offshore fields, Assam-Arakan Basin, and emerging shale gas prospects in the Cambay Basin. Technological adoption has accelerated with digital transformation initiatives accounting for nearly 18% of operational improvements in recent years. The market continues to attract substantial investment from major oil companies seeking to capitalize on India’s growing energy consumption patterns.

The India oil and gas upstream market refers to the comprehensive ecosystem of activities focused on the exploration, development, and production of crude oil and natural gas resources within Indian territory, including both onshore and offshore operations. This market encompasses all upstream value chain activities from initial geological surveys and seismic studies to drilling operations, field development, and hydrocarbon extraction processes.

Upstream operations specifically involve the search for underground or underwater crude oil and natural gas fields, drilling exploratory wells, and subsequently operating the wells that recover and bring the crude oil or raw natural gas to the surface. Market participants include national oil companies, international oil majors, independent exploration and production companies, and specialized service providers supporting various aspects of upstream operations.

India’s upstream oil and gas sector stands at a critical juncture of transformation, driven by ambitious energy security objectives and substantial policy reforms. The market demonstrates robust growth momentum supported by government initiatives aimed at reducing import dependency and enhancing domestic production capabilities. Strategic investments in exploration activities have increased significantly, with exploration spending growing by approximately 15% annually over the recent period.

Key market characteristics include diversified resource base spanning conventional oil and gas fields, coal bed methane, and emerging shale gas prospects. Technological integration has become a defining feature, with advanced seismic imaging, horizontal drilling, and enhanced oil recovery techniques driving operational efficiency improvements. Regulatory framework reforms have streamlined licensing processes and created more attractive investment conditions for both domestic and international players.

Market outlook remains positive with sustained government support, increasing private sector participation, and growing focus on unconventional resources. Production targets set by national energy policies indicate ambitious growth projections, supported by comprehensive infrastructure development and technology adoption initiatives across the upstream value chain.

Strategic market insights reveal several critical trends shaping India’s upstream oil and gas landscape:

Primary market drivers propelling growth in India’s upstream oil and gas sector encompass both demand-side and supply-side factors. Energy security concerns represent the fundamental driver, with India’s growing economy requiring substantial increases in energy supply to support industrial growth and rising living standards. Import dependency reduction initiatives have created strong policy support for domestic upstream development.

Government policy initiatives serve as crucial growth catalysts, including the implementation of production-sharing contracts, revenue-sharing models, and streamlined regulatory frameworks. Technological advancements in exploration and production techniques have made previously uneconomical resources viable, expanding the addressable resource base significantly. Digital transformation initiatives are driving operational efficiency improvements and cost reductions across upstream operations.

Investment climate improvements through policy reforms have attracted both domestic and international capital, providing necessary funding for large-scale exploration and development projects. Infrastructure development programs including pipeline networks and processing facilities have created enabling conditions for upstream expansion. Market liberalization measures have introduced competition and efficiency improvements throughout the value chain.

Significant market restraints continue to challenge the growth trajectory of India’s upstream oil and gas sector. High capital requirements for exploration and development activities create barriers to entry, particularly for smaller players and limit the pace of resource development. Geological complexity in many Indian basins requires advanced technologies and expertise, increasing operational risks and costs.

Regulatory challenges persist despite recent reforms, with complex approval processes and multiple regulatory authorities creating delays in project implementation. Environmental concerns and community resistance in certain regions have led to project delays and increased compliance costs. Land acquisition difficulties particularly affect onshore operations, creating bottlenecks in project development timelines.

Technical challenges include mature field management, declining production rates in existing fields, and the need for enhanced oil recovery techniques. Infrastructure limitations in remote areas increase development costs and complexity. Skilled workforce shortages in specialized technical areas constrain operational efficiency and expansion capabilities across the sector.

Substantial market opportunities exist across multiple dimensions of India’s upstream oil and gas sector. Unconventional resources represent the largest opportunity area, with significant shale gas, coal bed methane, and tight oil potential remaining largely untapped. Deep-water exploration offers promising prospects, particularly in the Krishna-Godavari and Cauvery basins where recent discoveries have demonstrated commercial viability.

Technology adoption opportunities span artificial intelligence applications, advanced seismic imaging, and enhanced oil recovery techniques that can significantly improve production efficiency and extend field life. Digital transformation initiatives offer potential for operational cost reductions and productivity improvements across exploration, drilling, and production operations.

Strategic partnerships with international oil companies provide opportunities for technology transfer, capital investment, and operational expertise sharing. Infrastructure development projects create opportunities for integrated upstream-midstream development approaches. Policy support measures including fiscal incentives and streamlined regulations continue to create favorable conditions for market expansion and investment attraction.

Market dynamics in India’s upstream oil and gas sector reflect complex interactions between supply-demand fundamentals, policy frameworks, and technological developments. Supply-side dynamics are influenced by production trends from existing fields, success rates in exploration activities, and the pace of new field development. Demand-side pressures continue to intensify with India’s growing energy consumption requirements and industrial expansion.

Competitive dynamics have evolved significantly with increased participation from private sector players and international oil companies. Technology dynamics are reshaping operational approaches, with digitalization initiatives improving efficiency by approximately 20% in recent implementations. Regulatory dynamics continue to evolve with ongoing policy reforms aimed at creating more attractive investment conditions.

Price dynamics in global oil markets significantly impact investment decisions and project economics in the upstream sector. Environmental dynamics are increasingly important, with sustainability considerations influencing operational practices and investment priorities. Geopolitical dynamics affect international partnerships and technology transfer arrangements, shaping the sector’s development trajectory.

Comprehensive research methodology employed for analyzing India’s upstream oil and gas market incorporates multiple data sources and analytical approaches. Primary research includes extensive interviews with industry executives, government officials, and technical experts across the upstream value chain. Secondary research encompasses analysis of government publications, industry reports, and regulatory filings from major market participants.

Data collection methods include structured surveys with upstream operators, service companies, and technology providers to gather insights on market trends, challenges, and opportunities. Quantitative analysis incorporates production data, investment figures, and operational metrics from reliable industry sources. Qualitative analysis focuses on policy developments, technological trends, and strategic initiatives shaping market evolution.

Market modeling approaches utilize statistical techniques to project future trends and assess various scenario outcomes. Validation processes ensure data accuracy through cross-referencing multiple sources and expert review. MarkWide Research analytical frameworks provide structured approaches for evaluating market dynamics and competitive positioning across different segments and geographical regions.

Regional analysis reveals distinct characteristics and opportunities across India’s diverse upstream oil and gas landscape. Western offshore regions, particularly the Mumbai High complex, continue to dominate production with approximately 40% of total crude oil output. Eastern offshore areas including the Krishna-Godavari basin show significant growth potential with recent major gas discoveries and ongoing exploration activities.

Northeastern states, particularly Assam, maintain historical importance in India’s upstream sector with mature oil fields and ongoing exploration in frontier areas. Rajasthan has emerged as a significant onshore production center with the Mangala, Bhagyam, and Aishwariya fields contributing substantially to domestic crude oil production. Gujarat demonstrates strong potential in both conventional and unconventional resources, including coal bed methane prospects.

Southern regions including Tamil Nadu and Andhra Pradesh offer opportunities in both onshore and offshore segments. Central Indian basins present emerging opportunities for unconventional resource development. Regional infrastructure development varies significantly, with western and southern regions having more developed supporting infrastructure compared to northeastern and central areas, influencing development economics and timelines.

Competitive landscape in India’s upstream oil and gas market features a diverse mix of national oil companies, international majors, and specialized service providers. Key market participants include:

Competitive strategies focus on technology adoption, operational efficiency improvements, and strategic partnerships for accessing new opportunities and sharing risks in exploration activities.

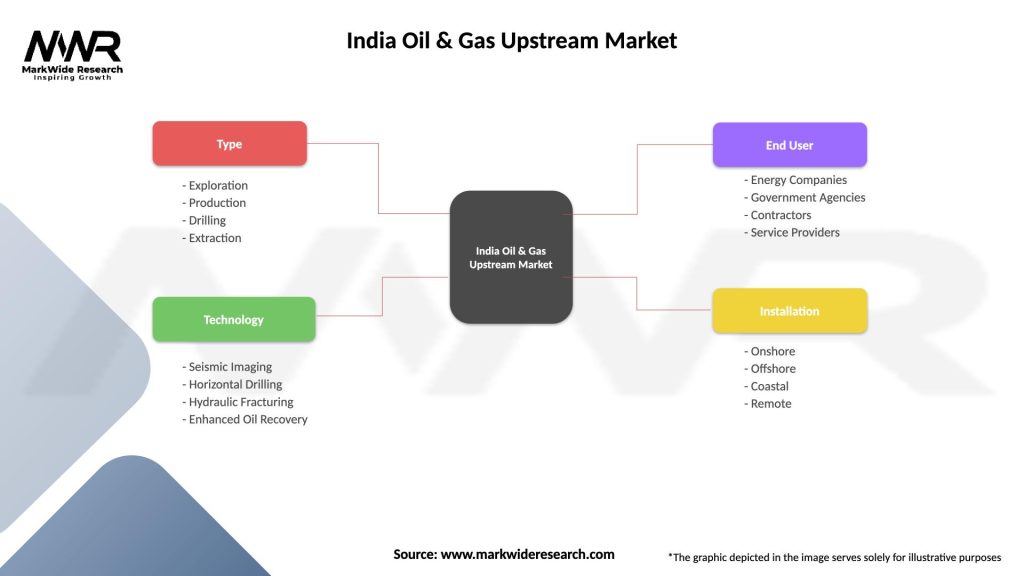

Market segmentation analysis reveals distinct characteristics across various dimensions of India’s upstream oil and gas sector:

By Resource Type:

By Operation Type:

By Geography:

Category-wise analysis provides detailed insights into specific segments of India’s upstream market:

Conventional Oil and Gas: This category continues to dominate current production with mature field management becoming increasingly important. Enhanced oil recovery techniques are being implemented to extend field life and improve recovery factors. Production optimization through advanced well management and reservoir monitoring systems shows promising results.

Unconventional Resources: Shale gas development represents a significant opportunity with pilot projects demonstrating technical feasibility. Coal bed methane production has shown steady growth with production increasing by approximately 12% annually in recent years. Tight oil prospects are being evaluated in several basins with encouraging preliminary results.

Deep-water Operations: Offshore deep-water exploration has gained momentum with several major discoveries in recent years. Technology requirements for deep-water operations necessitate partnerships with international companies possessing specialized expertise. Infrastructure investments in deep-water capabilities continue to expand operational possibilities in previously inaccessible areas.

Industry participants in India’s upstream oil and gas market realize multiple strategic benefits:

For Upstream Operators:

For Service Providers:

For Government and Society:

Strengths:

Weaknesses:

Opportunities:

Threats:

Key market trends shaping India’s upstream oil and gas sector demonstrate significant evolution in operational approaches and strategic priorities:

Digital Transformation: Accelerated adoption of digital technologies including artificial intelligence, machine learning, and IoT solutions for enhanced operational efficiency. Data analytics applications are improving exploration success rates and production optimization. Remote monitoring systems enable real-time operational management and predictive maintenance capabilities.

Sustainability Focus: Environmental sustainability has become a central consideration in upstream operations with increased emphasis on carbon footprint reduction and environmental protection measures. Clean technology adoption includes methane emission reduction systems and renewable energy integration in operations.

Unconventional Resource Development: Growing focus on unconventional resources with pilot projects demonstrating commercial viability. Technology improvements in hydraulic fracturing and horizontal drilling are making previously uneconomical resources viable. Regulatory support for unconventional development continues to strengthen.

International Collaboration: Strategic partnerships with international oil companies are increasing for technology transfer and capital investment. Joint venture structures are becoming more common for sharing risks and expertise in challenging projects.

Recent industry developments highlight the dynamic nature of India’s upstream oil and gas market:

Policy Initiatives: Implementation of the Hydrocarbon Exploration and Licensing Policy (HELP) has streamlined licensing procedures and introduced revenue-sharing models. Open Acreage Licensing Policy (OALP) allows companies to select exploration blocks throughout the year, improving operational flexibility.

Major Discoveries: Significant gas discoveries in the Krishna-Godavari basin have demonstrated the potential of deep-water exploration. Onshore discoveries in Rajasthan and Gujarat continue to add to domestic reserves. Unconventional resource assessments have identified substantial shale gas potential in multiple basins.

Technology Deployments: Advanced seismic imaging technologies are improving exploration success rates and reducing drilling risks. Enhanced oil recovery projects are extending field life and improving recovery factors in mature fields. Digital oilfield initiatives are optimizing production operations and reducing operational costs.

Infrastructure Investments: Pipeline network expansions are improving connectivity between producing areas and markets. Processing facility upgrades are enhancing production capacity and product quality. Port infrastructure developments are supporting offshore operations and equipment logistics.

Strategic recommendations for stakeholders in India’s upstream oil and gas market focus on leveraging emerging opportunities while addressing key challenges:

For Upstream Operators: Technology investment should prioritize digital transformation initiatives and advanced exploration techniques to improve operational efficiency. Portfolio diversification across conventional and unconventional resources can provide balanced risk-return profiles. Strategic partnerships with international companies can provide access to advanced technologies and capital resources.

For Service Providers: Capability development in specialized services for unconventional resources and deep-water operations presents significant growth opportunities. Technology innovation in digitalization and automation can create competitive advantages. Local partnerships can provide market access and regulatory navigation support.

For Investors: Long-term investment approaches are recommended given the capital-intensive nature of upstream operations and extended development timelines. Risk diversification across multiple projects and operators can provide balanced exposure. ESG considerations should be integrated into investment decision-making processes.

According to MarkWide Research analysis, successful market participation requires comprehensive understanding of regulatory frameworks, technological requirements, and local market dynamics. Stakeholder engagement with government agencies, local communities, and industry partners is essential for project success.

Future outlook for India’s upstream oil and gas market remains highly positive with multiple growth drivers supporting sustained expansion. Government policy support continues to strengthen with ongoing regulatory reforms and fiscal incentives designed to attract investment and accelerate development. Energy demand projections indicate substantial growth requirements that will drive continued upstream investment and development activities.

Technological advancement will play a crucial role in unlocking previously inaccessible resources and improving operational efficiency. Unconventional resource development is expected to gain momentum with production growth rates potentially reaching 25% annually as pilot projects transition to commercial development. Deep-water exploration will continue expanding with improved success rates from advanced seismic technologies.

Investment flows are projected to increase significantly as policy reforms create more attractive investment conditions and reduce regulatory uncertainties. International partnerships will expand as global oil companies seek growth opportunities in emerging markets. Infrastructure development will accelerate to support increased production and new field developments across diverse geographical regions.

MWR projections indicate sustained growth momentum with production efficiency improvements of approximately 30% expected over the next decade through technology adoption and operational optimization. Market maturation will create opportunities for specialized service providers and technology companies supporting upstream operations.

India’s upstream oil and gas market presents compelling opportunities for growth and investment driven by strong policy support, substantial resource potential, and increasing energy demand. Market transformation through regulatory reforms, technology adoption, and international collaboration is creating favorable conditions for sustained expansion across conventional and unconventional resources.

Strategic positioning in this dynamic market requires comprehensive understanding of regulatory frameworks, technological requirements, and operational challenges. Success factors include effective stakeholder engagement, technology innovation, and strategic partnership development with both domestic and international players. Long-term prospects remain highly positive with multiple growth drivers supporting continued market development and investment attraction.

The upstream oil and gas market will continue serving as a critical component of India’s energy security strategy while providing substantial opportunities for industry participants across the value chain. Sustained government support, combined with improving technology and operational capabilities, positions the market for continued growth and development in the years ahead.

What is Oil & Gas Upstream?

Oil & Gas Upstream refers to the exploration and production segment of the oil and gas industry, which involves locating oil and gas reserves and extracting them. This sector is crucial for meeting energy demands and includes activities such as drilling, well completion, and reservoir management.

What are the key players in the India Oil & Gas Upstream Market?

Key players in the India Oil & Gas Upstream Market include Oil and Natural Gas Corporation (ONGC), Reliance Industries Limited, and Cairn Oil & Gas. These companies are involved in exploration, production, and development of oil and gas resources, among others.

What are the growth factors driving the India Oil & Gas Upstream Market?

The growth of the India Oil & Gas Upstream Market is driven by increasing energy demand, government initiatives to enhance domestic production, and advancements in exploration technologies. Additionally, the push for energy security and reduced dependence on imports plays a significant role.

What challenges does the India Oil & Gas Upstream Market face?

The India Oil & Gas Upstream Market faces challenges such as regulatory hurdles, environmental concerns, and fluctuating global oil prices. These factors can impact investment decisions and operational efficiency in the sector.

What opportunities exist in the India Oil & Gas Upstream Market?

Opportunities in the India Oil & Gas Upstream Market include the potential for new discoveries in untapped regions, the adoption of digital technologies for enhanced operational efficiency, and partnerships with international firms for technology transfer. These factors can significantly boost production capabilities.

What trends are shaping the India Oil & Gas Upstream Market?

Trends shaping the India Oil & Gas Upstream Market include the increasing use of renewable energy sources, the implementation of advanced drilling techniques, and a focus on sustainability practices. These trends are influencing how companies operate and invest in the sector.

India Oil & Gas Upstream Market

| Segmentation Details | Description |

|---|---|

| Type | Exploration, Production, Drilling, Extraction |

| Technology | Seismic Imaging, Horizontal Drilling, Hydraulic Fracturing, Enhanced Oil Recovery |

| End User | Energy Companies, Government Agencies, Contractors, Service Providers |

| Installation | Onshore, Offshore, Coastal, Remote |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading companies in the India Oil & Gas Upstream Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.