444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

for Fuel Cells Market")

Market Overview

The membrane electrode assemblies (MEA) for fuel cells market is poised for substantial growth, driven by increasing adoption of fuel cell technology across various applications such as transportation, stationary power generation, and portable devices. MEAs are critical components in fuel cells, facilitating the electrochemical reactions that convert hydrogen and oxygen into electricity and water. This comprehensive analysis explores the current market landscape, key drivers, challenges, opportunities, and future outlook for MEAs in fuel cell applications.

Meaning

Membrane electrode assemblies (MEA) are core components of fuel cells, comprising proton-conducting membranes, catalyst layers, and gas diffusion layers. MEAs enable efficient conversion of hydrogen and oxygen into electricity through electrochemical reactions, making them essential for fuel cell performance and durability. Advances in MEA design and materials contribute to improved fuel cell efficiency, power density, and operational reliability across diverse end-user industries.

Executive Summary

The MEA for fuel cells market is experiencing robust growth fueled by technological advancements, government initiatives promoting clean energy solutions, and increasing investments in hydrogen infrastructure. Key factors driving market expansion include the rising demand for zero-emission transportation solutions, advancements in fuel cell performance and durability, and growing awareness of environmental sustainability. Despite challenges such as high production costs and infrastructure limitations, the market outlook remains optimistic, driven by ongoing research and development efforts.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

The growth of the MEA for fuel cells market is driven by several key factors:

Market Restraints

Despite its growth potential, the MEA for fuel cells market faces challenges:

Market Opportunities

The MEA for fuel cells market presents opportunities for growth and innovation:

Market Dynamics

The dynamics of the MEA for fuel cells market are influenced by technological advancements, regulatory frameworks, investment trends, and consumer preferences towards sustainable energy solutions. The transition towards decarbonization, energy security, and electrification drives market dynamics and investment in fuel cell technology.

Regional Analysis

The MEA for fuel cells market exhibits regional variations based on economic development, government policies, and industrial applications:

Competitive Landscape

Leading Companies in the Membrane Electrode Assemblies (MEA) for Fuel Cells Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

The MEA for fuel cells market can be segmented based on several criteria:

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

The adoption of MEA for fuel cells offers several benefits for industry participants:

SWOT Analysis

A SWOT analysis of the MEA for fuel cells market highlights:

Market Key Trends

Covid-19 Impact

The Covid-19 pandemic disrupted global supply chains and temporarily affected market demand for MEA in fuel cells, particularly in automotive and industrial sectors. However, the crisis highlighted the resilience of fuel cell technology as a reliable and sustainable energy solution, driving continued investments in hydrogen infrastructure and clean energy transitions. As economies recover and prioritize green recovery initiatives, the MEA for fuel cells market is expected to rebound, supported by renewed policy support and accelerated adoption of zero-emission technologies.

Key Industry Developments

Analyst Suggestions

To capitalize on the opportunities in the MEA for fuel cells market, organizations should consider the following strategies:

Future Outlook

The future outlook for the MEA for fuel cells market is promising, driven by global commitments to decarbonization, advancements in hydrogen technology, and increasing adoption of clean energy solutions. As governments and industries accelerate efforts towards achieving net-zero emissions, fuel cell technology and MEAs are expected to play a pivotal role in the transition towards a sustainable energy future. Innovations in materials science, manufacturing processes, and system integration will shape the evolving landscape of the MEA for fuel cells market, offering opportunities for growth, investment, and environmental stewardship.

Conclusion

In conclusion, the MEA for fuel cells market represents a critical enabler of clean energy solutions, supporting global efforts to reduce carbon emissions, enhance energy security, and foster economic growth. Despite challenges such as high production costs and infrastructure limitations, the benefits of MEA technology in fuel cells outweigh its drawbacks, driving continued investment and innovation. By leveraging technological advancements, policy support, and market expansion strategies, stakeholders can seize opportunities in the dynamic and evolving MEA for fuel cells market, contributing to a sustainable and resilient energy ecosystem.

What is Membrane Electrode Assemblies (MEA) for Fuel Cells?

Membrane Electrode Assemblies (MEA) for Fuel Cells are critical components that facilitate the electrochemical reactions in fuel cells, converting chemical energy into electrical energy. They consist of a proton exchange membrane sandwiched between two electrodes, which are essential for the operation of various fuel cell types.

What are the key players in the Membrane Electrode Assemblies (MEA) for Fuel Cells Market?

Key players in the Membrane Electrode Assemblies (MEA) for Fuel Cells Market include companies like Ballard Power Systems, Proton OnSite, and 3M, which are known for their innovations in fuel cell technology and production. These companies focus on enhancing the efficiency and durability of MEAs, among others.

What are the growth factors driving the Membrane Electrode Assemblies (MEA) for Fuel Cells Market?

The growth of the Membrane Electrode Assemblies (MEA) for Fuel Cells Market is driven by increasing demand for clean energy solutions, advancements in fuel cell technology, and government initiatives promoting hydrogen fuel adoption. Additionally, the rising need for efficient energy storage systems contributes to market expansion.

What challenges does the Membrane Electrode Assemblies (MEA) for Fuel Cells Market face?

The Membrane Electrode Assemblies (MEA) for Fuel Cells Market faces challenges such as high production costs, limited durability of MEAs, and competition from alternative energy sources. These factors can hinder widespread adoption and commercialization of fuel cell technologies.

What opportunities exist in the Membrane Electrode Assemblies (MEA) for Fuel Cells Market?

Opportunities in the Membrane Electrode Assemblies (MEA) for Fuel Cells Market include the development of new materials that enhance performance, increasing investments in hydrogen infrastructure, and growing applications in transportation and stationary power generation. These factors are likely to drive innovation and market growth.

What trends are shaping the Membrane Electrode Assemblies (MEA) for Fuel Cells Market?

Trends shaping the Membrane Electrode Assemblies (MEA) for Fuel Cells Market include the integration of nanotechnology to improve efficiency, the shift towards sustainable manufacturing processes, and the increasing collaboration between automotive and energy sectors. These trends are pivotal in advancing fuel cell technologies.

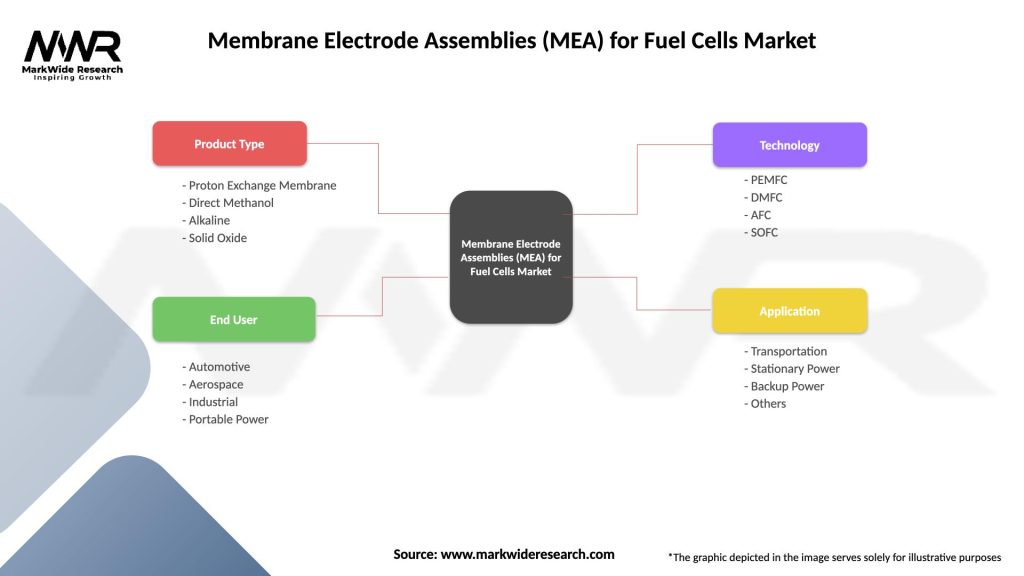

Membrane Electrode Assemblies (MEA) for Fuel Cells Market

| Segmentation Details | Description |

|---|---|

| Product Type | Proton Exchange Membrane, Direct Methanol, Alkaline, Solid Oxide |

| End User | Automotive, Aerospace, Industrial, Portable Power |

| Technology | PEMFC, DMFC, AFC, SOFC |

| Application | Transportation, Stationary Power, Backup Power, Others |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the Membrane Electrode Assemblies (MEA) for Fuel Cells Market

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA