The Cancer Generics market is experiencing significant growth, fueled by the rising incidence of cancer worldwide, increasing demand for affordable treatment options, and the expiration of patents for several branded cancer drugs. Cancer generics, also known as generic oncology drugs, are cost-effective alternatives to brand-name medications, offering comparable efficacy and safety profiles at lower prices. With the growing burden of cancer and the escalating costs of cancer care, generic oncology drugs play a crucial role in expanding access to essential cancer therapies and improving patient outcomes across diverse healthcare settings.

Meaning

Cancer generics refer to bioequivalent versions of branded cancer drugs that have lost patent protection and are manufactured and marketed by multiple pharmaceutical companies. These generic oncology drugs contain the same active ingredients, dosage forms, and routes of administration as their branded counterparts, but are typically sold at lower prices due to competition among manufacturers. By providing affordable alternatives to expensive cancer medications, cancer generics enable healthcare systems, payers, and patients to reduce treatment costs, improve medication adherence, and allocate resources more efficiently in the fight against cancer.

Executive Summary

The Cancer Generics market is witnessing rapid expansion, driven by the convergence of demographic trends, regulatory reforms, and market dynamics shaping the global healthcare landscape. Key players in the market are leveraging economies of scale, manufacturing efficiencies, and regulatory pathways to accelerate the development, production, and commercialization of generic oncology drugs. With the increasing adoption of value-based healthcare models and the growing emphasis on cost containment in cancer care, cancer generics are poised to play a pivotal role in shaping the future of oncology treatment worldwide.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

The global Cancer Generics market is projected to grow at a compound annual growth rate (CAGR) of over XX% during the forecast period, driven by factors such as patent expirations, regulatory reforms, and market competition.

Increasing investments in generic drug development, manufacturing, and distribution infrastructure by pharmaceutical companies and contract manufacturers are driving market expansion and innovation.

Regulatory agencies, such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA), are streamlining approval pathways and providing incentives to expedite the review and approval of generic oncology drugs, enhancing market access and competition.

Market Drivers

Rising incidence of cancer globally, driven by population aging, lifestyle factors, environmental exposures, and advances in cancer detection and screening.

Escalating costs of cancer treatment, including branded oncology drugs, chemotherapy regimens, and supportive care medications, leading to financial burden for patients, payers, and healthcare systems.

Expired patents for several blockbuster cancer drugs, paving the way for generic competition and market entry of lower-cost alternatives.

Growing acceptance of generic drugs among healthcare providers, patients, and payers, fueled by evidence of comparable efficacy, safety, and quality to brand-name medications.

Market Restraints

Regulatory complexities and market barriers in generic drug development, including bioequivalence testing, clinical trials, and manufacturing process validation, delaying market entry and competition.

Patent litigation and intellectual property disputes between brand-name manufacturers and generic companies, hindering market access and product launches.

Market consolidation among generic drug manufacturers and pharmacy benefit managers (PBMs), leading to pricing pressures, supply chain disruptions, and market concentration.

Perception and stigma associated with generic drugs, including concerns about quality, safety, and efficacy compared to brand-name medications, affecting patient acceptance and adherence.

Market Opportunities

Development of complex generic oncology drugs, such as biosimilars, cytotoxic agents, and targeted therapies, offering expanded treatment options and cost savings in cancer care.

Expansion into emerging markets with growing cancer burden, limited access to branded medications, and increasing demand for affordable oncology treatments.

Collaboration between generic drug manufacturers, academic research institutions, and regulatory agencies to address scientific challenges, regulatory requirements, and market access barriers in generic oncology drug development.

Adoption of value-based pricing models, patient assistance programs, and reimbursement strategies to improve affordability and accessibility of cancer generics for patients and healthcare providers.

Market Dynamics

The Cancer Generics market is characterized by dynamic trends driven by scientific advances, regulatory reforms, and market competition. Key players in the market are investing in research and development, manufacturing capabilities, and commercialization strategies to capitalize on emerging opportunities and address evolving challenges in generic oncology drug development. Moreover, strategic partnerships, licensing agreements, and acquisitions are reshaping the competitive landscape and driving consolidation in the generic drug industry.

Regional Analysis

North America dominates the global Cancer Generics market, owing to factors such as the high prevalence of cancer, well-established generic drug industry, and favorable regulatory environment for generic drug approval and market access. Europe and Asia-Pacific are also significant markets for cancer generics, driven by increasing demand for affordable cancer treatments, healthcare cost containment measures, and regulatory initiatives to promote generic drug utilization.

Competitive Landscape

Leading Companies in Cancer Generics Market:

Teva Pharmaceutical Industries Ltd.

Mylan N.V. (now Viatris Inc.)

Sandoz International GmbH (a subsidiary of Novartis AG)

Accord Healthcare Inc.

Hikma Pharmaceuticals PLC

Aspen Pharmacare Holdings Limited

Dr. Reddy’s Laboratories Ltd.

Cipla Ltd.

Sun Pharmaceutical Industries Ltd.

Fresenius Kabi AG

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

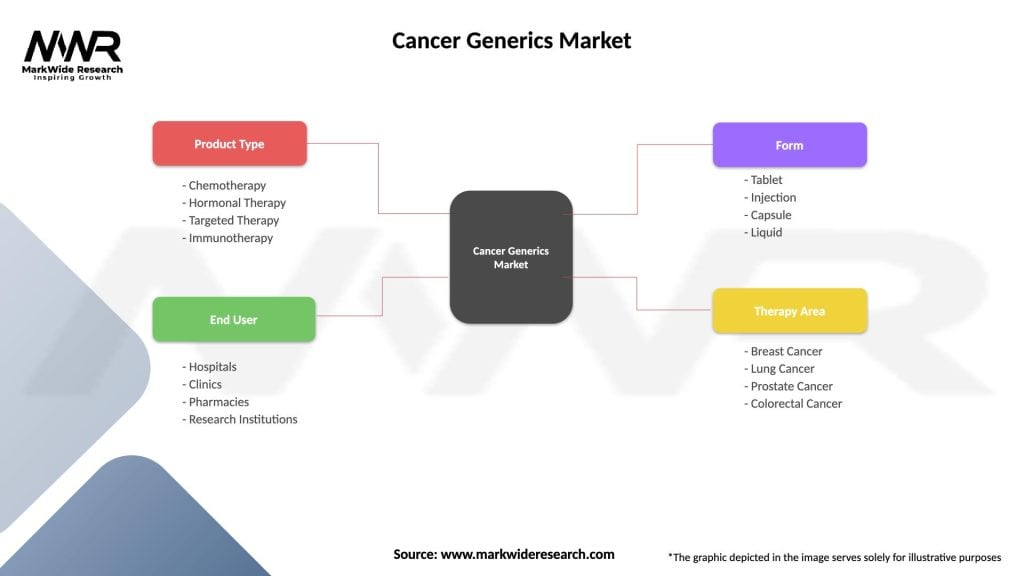

The Cancer Generics market can be segmented based on drug class, cancer type, dosage form, and distribution channel. Drug classes may include cytotoxic agents, hormonal therapies, targeted therapies, supportive care medications, and biosimilars. Cancer types may include breast cancer, lung cancer, colorectal cancer, prostate cancer, and hematological malignancies. Dosage forms may include oral tablets, injectable formulations, topical preparations, and oral solutions. Distribution channels may include retail pharmacies, hospital pharmacies, online pharmacies, and specialty clinics.

Category-wise Insights

Cytotoxic agents represent the largest segment of the Cancer Generics market, accounting for the majority of generic oncology drug sales and utilization in chemotherapy regimens.

Biosimilars are an emerging segment of the Cancer Generics market, offering lower-cost alternatives to biologic cancer drugs, such as monoclonal antibodies and growth factor inhibitors, with comparable efficacy and safety profiles.

Key Benefits for Industry Participants and Stakeholders

Expanded market opportunities and revenue potential in the growing oncology drug market, driven by the rising demand for affordable cancer treatments and cost containment measures.

Differentiation and competitive advantage through the development and commercialization of complex generic oncology drugs, such as biosimilars and cytotoxic agents, addressing unmet medical needs and therapeutic gaps in cancer care.

Improved patient access to essential cancer therapies and supportive care medications, leading to enhanced treatment outcomes, quality of life, and survival rates for cancer patients worldwide.

Enhanced cost-effectiveness and sustainability of healthcare systems, payers, and government agencies through the promotion of generic drug utilization, formulary management, and value-based reimbursement models in cancer care.

SWOT Analysis

Strengths: Lower costs, comparable efficacy, and safety to brand-name medications, expanded access to essential cancer therapies, regulatory support for generic drug approval.

Weaknesses: Regulatory hurdles, market barriers, and intellectual property challenges in generic drug development, pricing pressures and reimbursement constraints, quality and safety concerns.

Opportunities: Development of complex generics, such as biosimilars and targeted therapies, expansion into emerging markets, collaboration and partnerships to address scientific challenges.

Threats: Patent litigation and intellectual property disputes, regulatory uncertainties, supply chain disruptions, competition from branded medications and innovative therapies.

Market Key Trends

Rising adoption of biosimilars in oncology, driven by patent expirations for biologic cancer drugs, increasing healthcare costs, and regulatory initiatives to promote biosimilar utilization and competition.

Development of niche generic oncology drugs targeting rare cancers, pediatric malignancies, and underserved patient populations, offering new treatment options and therapeutic alternatives in cancer care.

Emphasis on patient-centered care, shared decision-making, and patient engagement in cancer treatment decisions, influencing prescribing patterns, medication adherence, and treatment outcomes.

Integration of digital technologies, data analytics, and real-world evidence in generic drug development, clinical trials, and post-marketing surveillance to optimize drug safety, efficacy, and patient outcomes.

Covid-19 Impact

The Covid-19 pandemic has had mixed effects on the Cancer Generics market, with disruptions to drug manufacturing, supply chains, and clinical trials offset by increased demand for affordable cancer treatments and healthcare cost containment measures. While the pandemic has underscored the importance of generic drugs in ensuring access to essential medications and improving healthcare affordability, it has also highlighted vulnerabilities in global drug supply chains and regulatory frameworks. Moving forward, the Cancer Generics market is expected to rebound as healthcare systems adapt to new challenges, regulatory agencies implement reforms, and industry stakeholders collaborate to address emerging needs and opportunities in cancer care.

Key Industry Developments

Teva Pharmaceutical Industries Ltd. launched several generic oncology drugs, including generic versions of imatinib, paclitaxel, and letrozole, expanding its portfolio of affordable cancer treatments for patients worldwide.

Mylan N.V. received regulatory approval for its biosimilar trastuzumab, a lower-cost alternative to branded Herceptin, for the treatment of HER2-positive breast cancer, demonstrating the potential of biosimilars in oncology.

Sandoz International GmbH partnered with oncology clinics and healthcare providers to offer patient assistance programs, co-pay assistance, and medication access initiatives to uninsured and underinsured cancer patients.

Analyst Suggestions

Industry stakeholders should invest in research and development, manufacturing capabilities, and regulatory compliance to enhance the quality, safety, and efficacy of generic oncology drugs and biosimilars.

Collaboration between generic drug manufacturers, regulatory agencies, and healthcare providers is essential to address scientific challenges, regulatory requirements, and market access barriers in generic oncology drug development and commercialization.

Patient education, physician outreach, and advocacy efforts can help raise awareness of cancer generics, improve medication adherence, and enhance patient access to affordable cancer treatments.

Policy reforms, pricing transparency initiatives, and reimbursement reforms are needed to promote generic drug utilization, foster competition, and improve healthcare affordability in cancer care.

Future Outlook

The Cancer Generics market is poised for sustained growth and innovation in the coming years, driven by factors such as demographic trends, regulatory reforms, and market dynamics shaping the global oncology drug market. With the increasing demand for affordable cancer treatments, rising prevalence of cancer worldwide, and expanding opportunities for generic drug development, cancer generics are expected to play a vital role in improving patient access to essential cancer therapies, reducing treatment costs, and advancing cancer care across diverse healthcare settings.

Conclusion

In conclusion, the Cancer Generics market presents significant opportunities for industry participants and stakeholders to address unmet medical needs, improve patient outcomes, and enhance healthcare affordability in cancer care. By providing cost-effective alternatives to branded cancer drugs, generic oncology drugs and biosimilars enable patients, healthcare providers, and payers to maximize treatment benefits, minimize financial burden, and allocate resources more efficiently in the fight against cancer. With ongoing advancements in drug development, regulatory reforms, and market access initiatives, cancer generics are poised to revolutionize the oncology landscape and contribute to the global effort to combat cancer and improve public health outcomes.

What is Cancer Generics?

Cancer Generics refer to pharmaceutical products that are chemically identical to brand-name drugs used in cancer treatment but are sold under their chemical names. These generics provide cost-effective alternatives for patients and healthcare systems while maintaining the same efficacy and safety standards as their branded counterparts.

What are the key players in the Cancer Generics Market?

Key players in the Cancer Generics Market include companies like Teva Pharmaceutical Industries, Mylan N.V., and Sandoz, which focus on developing and distributing generic oncology medications. These companies play a significant role in increasing access to cancer treatments for patients worldwide, among others.

What are the growth factors driving the Cancer Generics Market?

The Cancer Generics Market is driven by factors such as the rising prevalence of cancer, increasing healthcare costs, and the growing demand for affordable treatment options. Additionally, the expiration of patents for several blockbuster cancer drugs has opened the market for generics.

What challenges does the Cancer Generics Market face?

Challenges in the Cancer Generics Market include stringent regulatory requirements, the complexity of cancer treatments, and competition from branded drugs. These factors can hinder the entry of new generics and affect market growth.

What opportunities exist in the Cancer Generics Market?

The Cancer Generics Market presents opportunities such as the development of biosimilars and the expansion into emerging markets. Additionally, increasing collaborations between generic manufacturers and research institutions can lead to innovative treatment options.

What trends are shaping the Cancer Generics Market?

Trends in the Cancer Generics Market include the rise of personalized medicine, advancements in drug formulation technologies, and the increasing focus on sustainability in drug manufacturing. These trends are influencing how generics are developed and marketed.

Sandoz International GmbH (a subsidiary of Novartis AG)

Accord Healthcare Inc.

Hikma Pharmaceuticals PLC

Aspen Pharmacare Holdings Limited

Dr. Reddy’s Laboratories Ltd.

Cipla Ltd.

Sun Pharmaceutical Industries Ltd.

Fresenius Kabi AG

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.