Market Overview The osteotomy fixator market plays a vital role in orthopedic surgery, providing stabilization and support for bone realignment procedures. Osteotomy fixators are essential devices used to correct bone deformities, fractures, and alignment issues, allowing for proper healing and restoration of skeletal function. This market is characterized by a range of fixator types, including external, internal, and hybrid systems, each offering unique benefits for specific surgical applications.

Meaning Osteotomy fixators are medical devices designed to stabilize and support bones during osteotomy procedures, which involve cutting and realigning bone segments to correct deformities, fractures, or misalignments. These fixators provide mechanical stability, facilitate bone healing, and enable surgeons to achieve precise alignment and positioning of bone fragments. Osteotomy fixators may be classified as external, internal, or hybrid devices, depending on their design and mode of application.

Executive Summary The osteotomy fixator market is witnessing steady growth driven by the increasing prevalence of orthopedic conditions, rising demand for minimally invasive surgical techniques, and advancements in fixation technologies. Key market players are focusing on product innovation, strategic partnerships, and geographic expansion to gain a competitive edge and capitalize on emerging opportunities in the global orthopedic surgery market.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Rising Orthopedic Disorders: The growing incidence of orthopedic disorders, such as osteoarthritis, traumatic injuries, and congenital deformities, is fueling demand for osteotomy procedures and fixator devices worldwide.

Minimally Invasive Techniques: Surgeons are increasingly adopting minimally invasive techniques for osteotomy procedures to minimize tissue trauma, reduce postoperative pain, and accelerate recovery, driving demand for less invasive fixator solutions.

Technological Advancements: Advances in fixation technologies, including computer-assisted navigation, patient-specific implants, and biocompatible materials, are enhancing the precision, stability, and safety of osteotomy procedures, stimulating market growth.

Aging Population: The aging population demographic, particularly in developed regions, is contributing to the increasing demand for orthopedic interventions, including osteotomy surgeries, as older adults seek to maintain mobility and quality of life.

Market Drivers

Increasing Prevalence of Orthopedic Conditions: The rising incidence of orthopedic disorders, such as osteoarthritis, rheumatoid arthritis, and fractures, is driving demand for osteotomy fixators to address bone deformities and alignment issues.

Advancements in Fixation Technologies: Technological innovations, including improved implant materials, biomechanical designs, and surgical techniques, are driving the development of more effective and patient-friendly osteotomy fixators.

Growing Preference for Minimally Invasive Surgery: Surgeons and patients increasingly prefer minimally invasive surgical approaches for osteotomy procedures due to shorter recovery times, reduced complications, and improved cosmetic outcomes, boosting the adoption of fixator devices.

Expanding Geriatric Population: The aging population demographic, characterized by a higher prevalence of orthopedic conditions and osteoporosis-related fractures, is driving demand for osteotomy fixators to address age-related bone deformities and instability.

Market Restraints

High Cost of Fixator Devices: The high cost associated with osteotomy fixator devices, including implant costs, surgical instrumentation, and postoperative care, may limit market adoption, particularly in regions with limited healthcare budgets or reimbursement challenges.

Complications and Risks: Despite technological advancements, osteotomy procedures and fixator applications carry inherent risks of complications, such as infection, implant failure, nonunion, and malunion, which may deter patients and surgeons from opting for these interventions.

Regulatory Hurdles and Compliance: Stringent regulatory requirements, including premarket approval, clinical validation, and post-market surveillance, pose challenges for fixator manufacturers in terms of time-to-market, product development costs, and compliance with global standards and regulations.

Limited Access to Healthcare Services: Inadequate access to specialized orthopedic care, particularly in rural or underserved areas, may restrict market growth for osteotomy fixator devices, as patients may face barriers to timely diagnosis, treatment, and follow-up care.

Market Opportunities

Emerging Markets: Rapid urbanization, expanding healthcare infrastructure, and increasing disposable incomes in emerging markets present lucrative opportunities for osteotomy fixator manufacturers to expand their presence and address unmet orthopedic needs.

Technological Innovations: Continued investments in research and development (R&D) to develop next-generation fixator technologies, such as patient-specific implants, 3D-printed constructs, and smart implants with integrated sensors, offer opportunities for differentiation and market penetration.

Strategic Partnerships and Collaborations: Collaboration with healthcare providers, research institutions, and regulatory agencies to conduct clinical trials, validate new technologies, and navigate regulatory pathways can facilitate market entry and adoption of innovative fixator solutions.

Patient-Centric Solutions: Designing patient-centric fixator devices with improved comfort, usability, and cosmetic outcomes can enhance patient satisfaction, compliance, and outcomes, driving market demand and differentiation in a competitive landscape.

Market Dynamics The osteotomy fixator market operates within a dynamic environment shaped by various internal and external factors, including technological advancements, regulatory changes, competitive pressures, and shifting healthcare trends. Understanding these dynamics is essential for market participants to identify opportunities, mitigate risks, and formulate effective strategies for sustainable growth and competitive advantage.

Regional Analysis The osteotomy fixator market exhibits regional variations in market size, growth potential, and regulatory landscape:

North America: The largest market for osteotomy fixators, driven by a robust healthcare infrastructure, high prevalence of orthopedic conditions, and significant R&D investments in fixation technologies.

Europe: A mature market for osteotomy fixators, characterized by stringent regulatory requirements, sophisticated healthcare systems, and strong demand for minimally invasive surgical techniques.

Asia Pacific: Emerging as a key growth region for osteotomy fixators, fueled by expanding healthcare access, rising orthopedic surgical volumes, and increasing adoption of advanced fixation technologies in countries such as China, India, and Japan.

Latin America, Middle East, and Africa: Growing demand for orthopedic interventions, improving healthcare infrastructure, and increasing medical tourism contribute to market expansion opportunities in these regions, albeit with varying degrees of regulatory complexity and economic development.

Competitive Landscape

Leading Companies in the Osteotomy Fixator Market:

Johnson & Johnson

Stryker Corporation

Zimmer Biomet Holdings, Inc.

Smith & Nephew plc

B. Braun Melsungen AG

Orthofix Medical Inc.

DePuy Synthes (Johnson & Johnson)

Acumed, LLC

Wright Medical Group N.V.

Integra LifeSciences Corporation

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

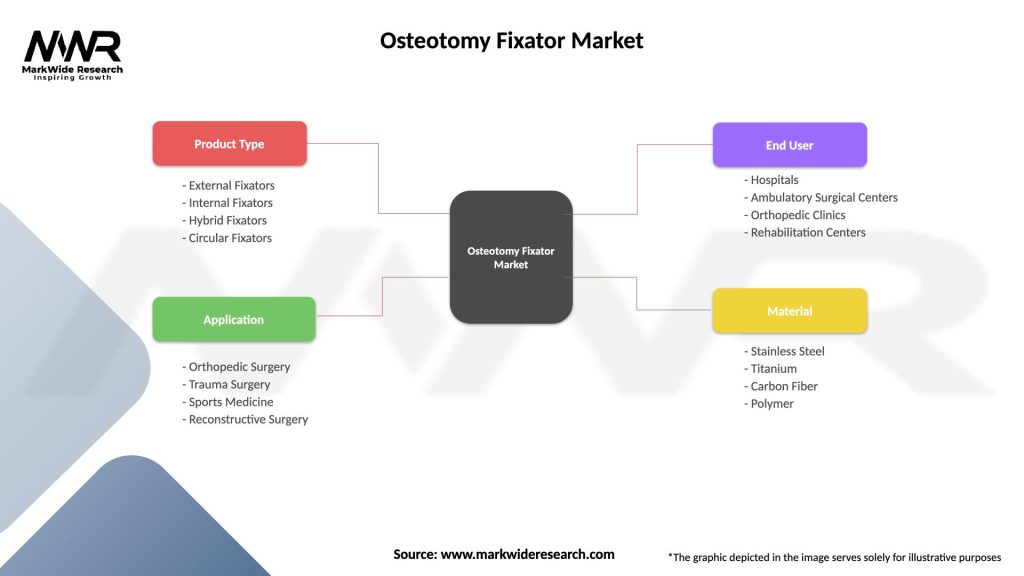

Segmentation The osteotomy fixator market can be segmented based on various factors, including:

Type of Fixator: External fixators, internal fixators, hybrid fixators, circular fixators, and patient-specific fixators.

End User: Hospitals, ambulatory surgical centers (ASCs), orthopedic clinics, and specialty clinics.

Segmentation enables a more granular understanding of market dynamics, customer preferences, and growth opportunities, allowing companies to tailor their product offerings, marketing strategies, and distribution channels accordingly.

Category-wise Insights

External Fixators: Used for temporary stabilization of bone segments, external fixators are versatile devices suitable for a wide range of orthopedic procedures, including trauma, deformity correction, and limb lengthening.

Internal Fixators: Internal fixators provide rigid internal fixation of bone segments, promoting bone healing and stability, while minimizing soft tissue disruption and external hardware complications.

Hybrid Fixators: Hybrid fixators combine elements of external and internal fixation techniques, offering a balance of stability, flexibility, and tissue preservation for complex osteotomy procedures.

Patient-Specific Fixators: Patient-specific fixators are custom-designed implants based on preoperative imaging and computer-assisted planning, enabling precise osteotomy execution and optimal bone alignment for individual patients.

Understanding the unique characteristics and clinical applications of each fixator category is essential for surgeons, healthcare providers, and medical device manufacturers to optimize treatment outcomes and patient satisfaction.

Key Benefits for Industry Participants and Stakeholders The osteotomy fixator market offers several benefits for industry participants and stakeholders:

Improved Surgical Outcomes: Osteotomy fixators facilitate accurate bone alignment, stable fixation, and optimal healing, resulting in improved clinical outcomes and patient satisfaction.

Enhanced Surgeon Efficiency: Advanced fixation technologies, ergonomic designs, and intuitive instrumentation streamline surgical workflows, reduce operative time, and enhance surgeon productivity.

Patient Comfort and Recovery: Minimally invasive techniques, patient-specific implants, and biocompatible materials minimize tissue trauma, pain, and discomfort, promoting faster recovery and rehabilitation.

Customized Treatment Solutions: Patient-specific fixators, modular implant systems, and customizable instrumentation enable personalized treatment approaches tailored to individual patient anatomy and clinical needs.

Clinical and Economic Value: Osteotomy fixators offer cost-effective solutions for orthopedic interventions, reducing hospitalization costs, complication rates, and long-term healthcare expenditures.

SWOT Analysis

A SWOT analysis provides insights into the strengths, weaknesses, opportunities, and threats facing the osteotomy fixator market:

Strengths:

Established clinical efficacy and safety of osteotomy procedures and fixator devices.

Technological advancements in fixation technologies, materials, and surgical techniques.

Diverse product offerings and application versatility across orthopedic specialties.

Weaknesses:

High upfront costs and reimbursement challenges for fixator devices and procedures.

Inherent risks of surgical complications, infections, and hardware failures.

Regulatory complexities and compliance requirements for product development and market entry.

Opportunities:

Emerging markets with unmet orthopedic needs and growing healthcare infrastructure.

Technological innovations in patient-specific implants, 3D printing, and smart fixator systems.

Strategic partnerships, collaborations, and acquisitions to expand market reach and product portfolios.

Threats:

Intense competition from established orthopedic implant manufacturers and emerging startups.

Regulatory uncertainties, market access barriers, and reimbursement restrictions.

Economic downturns, healthcare budget constraints, and shifts in healthcare policies and regulations.

Understanding these factors enables stakeholders to leverage strengths, address weaknesses, capitalize on opportunities, and mitigate threats to achieve sustainable growth and competitive advantage in the osteotomy fixator market.

Market Key Trends

Personalized Medicine: The trend towards personalized medicine and precision orthopedics is driving demand for patient-specific fixators, customized implants, and tailored treatment approaches based on individual patient anatomy and pathology.

Digital Health Integration: Integration of digital health technologies, such as imaging modalities, surgical navigation systems, and remote monitoring platforms, enhances preoperative planning, intraoperative guidance, and postoperative care in osteotomy procedures.

Regenerative Therapies: The emergence of regenerative therapies, including bone graft substitutes, growth factors, and tissue engineering approaches, complements osteotomy fixation by promoting bone healing, tissue regeneration, and implant integration.

Value-Based Healthcare: The shift towards value-based healthcare models emphasizes patient outcomes, cost-effectiveness, and quality of care, prompting providers and payers to prioritize evidence-based practices, clinical pathways, and value-based reimbursement for orthopedic interventions.

Covid-19 Impact The COVID-19 pandemic has had significant implications for the osteotomy fixator market:

Disruption of Elective Surgeries: The suspension of elective surgeries during the pandemic led to a temporary decline in osteotomy procedures and fixator utilization, affecting market demand and revenue for orthopedic implant manufacturers and healthcare providers.

Adoption of Telehealth and Virtual Care: The pandemic accelerated the adoption of telehealth, virtual consultations, and remote monitoring solutions for orthopedic patients, facilitating preoperative assessments, postoperative follow-up, and rehabilitation support without physical clinic visits.

Supply Chain Disruptions: Global supply chain disruptions, logistics challenges, and manufacturing delays due to lockdowns, travel restrictions, and workforce shortages impacted the availability and delivery of fixator devices and surgical implants.

Focus on Patient Safety and Infection Control: Enhanced infection control measures, screening protocols, and personal protective equipment (PPE) requirements in healthcare settings aimed to minimize the risk of COVID-19 transmission during orthopedic surgeries and hospital stays.

Key Industry Developments

Advanced Fixation Technologies: Continued investments in advanced fixation technologies, including bioabsorbable materials, shape memory alloys, and locking screw systems, enhance stability, biocompatibility, and osseointegration of osteotomy fixators.

3D Printing and Customization: The adoption of 3D printing technologies enables rapid prototyping, customization, and patient-specific design of fixator devices, optimizing fit, function, and implant-host interface in orthopedic surgeries.

Smart Fixator Systems: The integration of smart sensors, wireless connectivity, and digital feedback mechanisms into fixator devices enables real-time monitoring, data analytics, and remote patient management, enhancing safety, compliance, and clinical outcomes.

Regulatory Harmonization Efforts: Collaborative initiatives among regulatory agencies, industry consortia, and standards organizations aim to harmonize regulatory requirements, streamline approval processes, and promote global interoperability of osteotomy fixator devices.

Analyst Suggestions

Invest in R&D and Innovation: Continued investments in research and development (R&D) to develop next-generation fixation technologies, patient-specific implants, and smart fixator systems are essential for maintaining competitiveness and meeting evolving clinical needs.

Address Regulatory Challenges: Proactively engage with regulatory agencies, navigate compliance requirements, and streamline regulatory submissions to expedite market approval and ensure timely access to new fixator devices and technologies.

Focus on Value-Based Solutions: Emphasize value-based healthcare delivery, patient outcomes, and cost-effectiveness in product development, clinical studies, and market access strategies to align with evolving healthcare trends and payer preferences.

Collaborate Across the Ecosystem: Foster collaboration with surgeons, healthcare providers, payers, and patient advocacy groups to co-create innovative solutions, validate clinical evidence, and drive market adoption of osteotomy fixator devices and procedures.

Future Outlook The osteotomy fixator market is poised for significant growth and innovation in the coming years:

Technological Advancements: Continued advancements in fixation technologies, materials science, and digital health integration will drive the development of smarter, safer, and more effective fixator solutions for orthopedic surgery.

Personalized Medicine: The integration of personalized medicine, digital imaging, and artificial intelligence (AI) will enable more precise, patient-specific osteotomy procedures tailored to individual anatomy, pathology, and treatment goals.

Value-Based Healthcare: The shift towards value-based healthcare models and bundled payment arrangements will incentivize providers and payers to prioritize evidence-based practices, outcomes measurement, and cost-effective solutions in orthopedic care.

Global Market Expansion: Emerging markets in Asia Pacific, Latin America, and Africa will offer significant growth opportunities for osteotomy fixator manufacturers, driven by rising healthcare investments, expanding patient populations, and increasing demand for orthopedic interventions.

Conclusion The osteotomy fixator market plays a critical role in orthopedic surgery, providing essential stabilization and support for bone realignment procedures. With increasing prevalence of orthopedic conditions, advancements in fixation technologies, and growing adoption of minimally invasive techniques, the market offers significant opportunities for industry participants and stakeholders. Despite challenges such as regulatory hurdles, cost constraints, and pandemic-related disruptions, continued investments in R&D, innovation, and collaboration will drive market growth, improve patient outcomes, and shape the future of orthopedic surgery worldwide.

What is Osteotomy Fixator?

An osteotomy fixator is a medical device used to stabilize and support bone segments during the healing process after an osteotomy procedure, which involves cutting and repositioning bones. These fixators are crucial in orthopedic surgeries to ensure proper alignment and healing of bones.

What are the key players in the Osteotomy Fixator Market?

Key players in the Osteotomy Fixator Market include companies such as Stryker Corporation, DePuy Synthes, Zimmer Biomet, and Smith & Nephew, among others. These companies are known for their innovative products and technologies in orthopedic fixation devices.

What are the growth factors driving the Osteotomy Fixator Market?

The growth of the Osteotomy Fixator Market is driven by factors such as the increasing prevalence of orthopedic disorders, advancements in surgical techniques, and a growing aging population that requires orthopedic interventions. Additionally, the rise in sports-related injuries contributes to market expansion.

What challenges does the Osteotomy Fixator Market face?

The Osteotomy Fixator Market faces challenges such as the high cost of advanced fixation devices and the risk of complications associated with surgical procedures. Furthermore, the availability of alternative treatment options can also hinder market growth.

What opportunities exist in the Osteotomy Fixator Market?

Opportunities in the Osteotomy Fixator Market include the development of innovative and minimally invasive fixation devices, as well as the potential for growth in emerging markets. Additionally, increasing investments in orthopedic research and development present further opportunities.

What trends are shaping the Osteotomy Fixator Market?

Trends shaping the Osteotomy Fixator Market include the integration of smart technology in fixation devices, the rise of personalized medicine, and a focus on patient-centric approaches in orthopedic care. These trends aim to enhance surgical outcomes and improve patient recovery times.

Leading Companies in the Osteotomy Fixator Market:

Johnson & Johnson

Stryker Corporation

Zimmer Biomet Holdings, Inc.

Smith & Nephew plc

B. Braun Melsungen AG

Orthofix Medical Inc.

DePuy Synthes (Johnson & Johnson)

Acumed, LLC

Wright Medical Group N.V.

Integra LifeSciences Corporation

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.