The aerospace and defense brake market serves a critical function in ensuring the safety and performance of aircraft and defense systems. Brakes in aerospace and defense applications must meet stringent requirements for reliability, durability, and performance under extreme conditions. These brakes are essential for controlling the speed, maneuverability, and stopping distance of aircraft, helicopters, unmanned aerial vehicles (UAVs), and military vehicles.

Meaning

Aerospace and defense brakes are specialized braking systems designed to provide precise control and stopping power in aircraft, rotorcraft, and defense vehicles. These brakes must withstand high temperatures, heavy loads, and harsh operating environments while ensuring the safety and efficiency of aerospace and defense operations. They are integral components of landing gear systems, providing critical support during takeoff, landing, and taxiing.

Executive Summary

The aerospace and defense brake market is driven by the increasing demand for commercial air travel, military modernization programs, and the growing use of UAVs for defense and surveillance applications. Key market players are focusing on developing lightweight, high-performance brake systems using advanced materials and technologies to meet evolving industry requirements. However, challenges such as regulatory compliance, supply chain disruptions, and competitive pressures pose constraints on market growth.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Commercial Aviation Growth: The expansion of global air travel, fueled by rising passenger demand and fleet modernization initiatives, drives the demand for aerospace brakes. Commercial aircraft manufacturers are investing in lightweight, high-performance brake systems to improve fuel efficiency and reduce operating costs.

Military Modernization Programs: Military modernization efforts, particularly in regions like North America, Europe, and Asia-Pacific, fuel the demand for advanced aerospace and defense brakes. Military aircraft, rotorcraft, and tactical vehicles require robust braking systems to support mission-critical operations in diverse environments.

Rise of UAVs: The proliferation of UAVs for defense, reconnaissance, and surveillance applications creates opportunities for aerospace brake manufacturers. UAVs require lightweight, reliable braking systems to ensure safe takeoff, landing, and operation in both military and civilian settings.

Technological Advancements: Advances in materials science, friction technology, and brake design enable the development of next-generation aerospace and defense brakes. Carbon composite materials, ceramic brakes, and electromechanical braking systems offer superior performance, weight savings, and durability compared to traditional brake technologies.

Market Drivers

Safety and Reliability: Safety is paramount in aerospace and defense applications, driving the demand for reliable braking systems that can operate under extreme conditions without compromising performance. Aerospace and defense brakes must meet stringent certification standards and regulatory requirements to ensure airworthiness and mission success.

Performance Optimization: Aircraft and defense vehicles require precise control and maneuverability during takeoff, landing, and ground operations. Aerospace brakes play a crucial role in optimizing performance, reducing stopping distances, and enhancing overall operational efficiency.

Weight Reduction: Lightweighting is a key trend in aerospace and defense manufacturing, aimed at improving fuel efficiency and performance. Lightweight brake systems, such as carbon composite brakes, offer significant weight savings without compromising braking performance, making them attractive for aircraft and defense applications.

Environmental Sustainability: Environmental concerns and regulatory pressure drive the adoption of eco-friendly brake technologies in aerospace and defense applications. Carbon ceramic brakes, for example, offer reduced carbon emissions, longer service life, and lower maintenance requirements compared to traditional steel brakes.

Market Restraints

Cost Constraints: The high cost of aerospace and defense brake systems, coupled with budgetary constraints in the defense sector, poses a challenge to market growth. Manufacturers must balance performance requirements with cost considerations to remain competitive in the market.

Supply Chain Disruptions: Disruptions in the aerospace supply chain, such as raw material shortages, logistics bottlenecks, and geopolitical tensions, impact the availability and cost of brake components and subsystems. These disruptions can lead to delays in production and delivery, affecting customer satisfaction and profitability.

Regulatory Compliance: Compliance with stringent aerospace regulations and certification standards adds complexity and cost to brake system development and certification. Manufacturers must invest in extensive testing, validation, and documentation to ensure regulatory compliance and airworthiness certification.

Intense Competition: The aerospace and defense brake market is highly competitive, with numerous players competing for market share. Manufacturers face pressure to innovate, differentiate, and offer value-added solutions to maintain a competitive edge in the market.

Market Opportunities

Emerging Markets: The expansion of aerospace and defense industries in emerging markets, particularly in Asia-Pacific and the Middle East, presents growth opportunities for brake manufacturers. Rising defense spending, infrastructure development, and fleet expansion drive demand for advanced brake systems in these regions.

Technological Innovation: Investments in research and development enable manufacturers to innovate and differentiate their brake products. Technologies such as regenerative braking, smart brake monitoring systems, and predictive maintenance solutions offer opportunities for market differentiation and value creation.

Aftermarket Services: The aftermarket segment presents opportunities for revenue generation through maintenance, repair, and overhaul (MRO) services for aerospace and defense brake systems. Manufacturers can offer comprehensive aftermarket support, including spare parts, upgrades, and technical services, to enhance customer satisfaction and loyalty.

Partnerships and Collaborations: Collaborations between aerospace OEMs, brake manufacturers, and technology suppliers facilitate innovation, knowledge sharing, and market expansion. Strategic partnerships enable access to new markets, technologies, and capabilities, driving growth and competitiveness in the aerospace and defense brake market.

Market Dynamics

The aerospace and defense brake market operates in a dynamic environment shaped by technological advancements, regulatory changes, geopolitical developments, and market trends. Manufacturers must anticipate and respond to these dynamics to capitalize on opportunities, mitigate risks, and maintain competitiveness in the market.

Regional Analysis

The aerospace and defense brake market exhibits regional variations driven by factors such as defense spending, aerospace manufacturing capabilities, and market demand. Key regions include:

North America: The largest market for aerospace and defense brakes, driven by robust defense spending, technological innovation, and a strong aerospace manufacturing base. The United States dominates the market, supported by major aerospace OEMs and defense contractors.

Europe: A significant market for aerospace brakes, characterized by leading aerospace OEMs, defense contractors, and advanced manufacturing capabilities. Countries like France, Germany, and the United Kingdom are key contributors to the market, driven by defense modernization programs and commercial aerospace demand.

Asia-Pacific: A rapidly growing market for aerospace and defense brakes, fueled by rising defense budgets, expanding commercial aviation markets, and increasing aerospace manufacturing activities. Countries like China, India, and Japan are investing in indigenous aerospace capabilities, driving demand for brake systems in the region.

Middle East and Africa: A growing market for aerospace and defense brakes, driven by defense procurement, infrastructure development, and commercial aviation growth. The Middle East, in particular, is a key market for military and commercial aerospace applications, supported by investments in defense modernization and aviation infrastructure.

Competitive Landscape

Leading Companies in the Aerospace and Defense Brake Market:

Honeywell International Inc.

Safran S.A.

Raytheon Technologies Corporation

Meggitt PLC

Crane Aerospace & Electronics

Parker Hannifin Corporation

Beringer Aero

Matco Manufacturing Inc.

Cleveland Wheels & Brakes

Grove Aircraft Landing Gear Systems Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

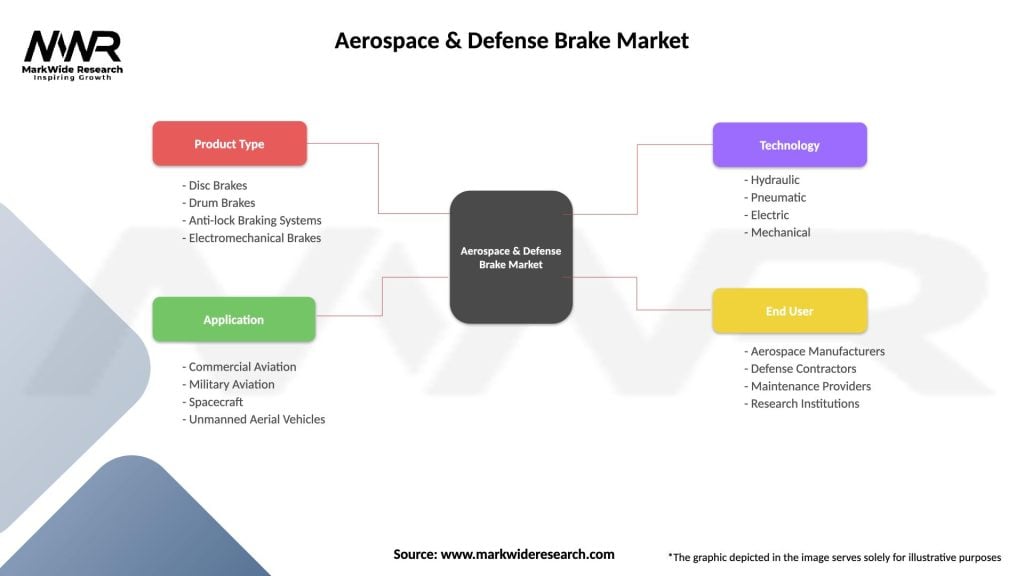

Segmentation

The aerospace and defense brake market can be segmented based on various factors, including:

Brake Type: Segmentation by brake type includes carbon brakes, steel brakes, and electromechanical braking systems, each offering unique performance characteristics and applications.

Aircraft Type: Segmentation by aircraft type includes commercial aircraft, military aircraft, rotorcraft, UAVs, and defense vehicles, each requiring specialized braking solutions tailored to their operational requirements.

End User: Segmentation by end-user includes aerospace OEMs, defense contractors, airlines, MRO service providers, and government agencies, each with distinct needs and procurement processes.

Geography: The market can be segmented into regions, countries, and key aerospace hubs based on market size, growth potential, and regulatory frameworks.

Segmentation enables a more targeted approach to market analysis, product development, and customer engagement, allowing brake manufacturers to better address customer needs and market opportunities.

Category-wise Insights

Carbon Brakes: Carbon brakes offer lightweight, high-performance braking solutions for commercial and military aircraft, providing superior stopping power, thermal management, and durability under demanding operating conditions.

Steel Brakes: Steel brakes are commonly used in military aircraft, rotorcraft, and defense vehicles, offering robust braking performance, reliability, and cost-effectiveness for tactical and heavy-duty applications.

Electromechanical Brakes: Electromechanical braking systems utilize electric actuators and control systems to provide precise, responsive braking performance with reduced weight and complexity compared to traditional hydraulic systems.

Integrated Brake Control Systems: Integrated brake control systems combine braking functions with other aircraft systems, such as anti-skid, autobrake, and brake-by-wire systems, to optimize braking performance and enhance safety in commercial and military aircraft.

Key Benefits for Industry Participants and Stakeholders

Enhanced Safety: Aerospace and defense brakes play a critical role in ensuring the safety and reliability of aircraft and defense vehicles, protecting passengers, crew, and valuable assets during takeoff, landing, and ground operations.

Improved Performance: Advanced brake technologies, such as carbon brakes and electromechanical systems, offer superior performance, precision, and control, enhancing aircraft maneuverability, stopping distance, and operational efficiency.

Reduced Maintenance: Modern brake systems incorporate advanced materials and design features to minimize wear, extend service intervals, and reduce maintenance costs, resulting in lower lifecycle costs for aircraft operators and defense organizations.

Regulatory Compliance: Aerospace and defense brakes are designed and certified to meet stringent regulatory requirements and industry standards, ensuring airworthiness, compliance, and operational safety in accordance with aviation authorities and military agencies.

Market Differentiation: Brake manufacturers that invest in innovation, quality, and customer support can differentiate their products and services in the market, attracting customers, gaining market share, and fostering long-term relationships with aerospace OEMs, defense contractors, and operators.

SWOT Analysis

A SWOT analysis provides insights into the strengths, weaknesses, opportunities, and threats facing the aerospace and defense brake market:

Strengths:

High-performance braking solutions

Strong regulatory compliance

Technological innovation

Established customer relationships

Weaknesses:

High manufacturing costs

Supply chain vulnerabilities

Dependence on aerospace and defense cycles

Regulatory complexity

Opportunities:

Emerging markets

Technological advancements

Aftermarket services

Strategic partnerships

Threats:

Intense competition

Supply chain disruptions

Budgetary constraints

Geopolitical tensions

Understanding these factors through a SWOT analysis helps brake manufacturers identify strategic priorities, address vulnerabilities, and capitalize on growth opportunities in the aerospace and defense market.

Market Key Trends

Lightweighting: Lightweight brake materials and designs, such as carbon composites and ceramic matrix composites, enable weight reduction, fuel savings, and performance improvements in aerospace and defense applications.

Electrification: The adoption of electromechanical braking systems and brake-by-wire technology offers benefits such as reduced weight, improved efficiency, and enhanced control in electric and hybrid aircraft platforms.

Digitalization: Digital technologies, such as sensors, data analytics, and predictive maintenance, enable condition monitoring, performance optimization, and predictive maintenance of aerospace and defense brake systems.

Autonomous Systems: The integration of braking systems with autonomous flight control systems and unmanned aerial vehicles (UAVs) enables autonomous takeoff, landing, and ground operations in military and commercial applications.

Covid-19 Impact

The Covid-19 pandemic has had a significant impact on the aerospace and defense brake market, leading to disruptions in air travel, defense procurement, and manufacturing operations. Some key impacts include:

Reduced Demand: The sharp decline in air travel and passenger demand during the pandemic resulted in lower aircraft production rates, reduced aftermarket demand, and supply chain disruptions for aerospace brake manufacturers.

Defense Budget Pressures: Budgetary constraints and shifting defense priorities in response to the pandemic impacted defense spending and procurement programs, affecting demand for military aircraft and defense braking systems.

Supply Chain Disruptions: Disruptions in the aerospace supply chain, including factory closures, transportation restrictions, and component shortages, affected the availability and delivery of brake components and subsystems, leading to production delays and cost overruns.

Focus on Resilience: The pandemic highlighted the importance of supply chain resilience, operational agility, and risk management in aerospace and defense manufacturing, prompting industry stakeholders to reevaluate their strategies and business continuity plans.

Key Industry Developments

Advanced Materials: Continued research and development efforts focus on developing advanced brake materials, such as carbon composites, ceramic matrix composites, and metal alloys, to enhance performance, durability, and sustainability in aerospace and defense applications.

Smart Braking systems: The integration of sensors, actuators, and control systems enables the development of smart braking systems capable of real-time monitoring, adaptive control, and predictive maintenance, enhancing safety and operational efficiency.

Electric Aircraft: The emergence of electric and hybrid-electric aircraft platforms drives demand for lightweight, efficient braking systems optimized for electric propulsion systems, regenerative braking, and energy recovery in aerospace applications.

Autonomous Technologies: Advances in autonomous flight control systems and unmanned aerial vehicles (UAVs) create opportunities for brake manufacturers to develop autonomous braking solutions tailored to autonomous aircraft operations and unmanned systems.

Analyst Suggestions

Innovate for Sustainability: Brake manufacturers should prioritize research and development efforts aimed at developing sustainable brake materials, energy-efficient braking systems, and environmentally friendly manufacturing processes to meet regulatory requirements and customer preferences.

Strengthen Supply Chain Resilience: Given the vulnerabilities exposed by the Covid-19 pandemic, brake manufacturers should enhance supply chain visibility, diversify sourcing strategies, and invest in digital technologies to improve supply chain resilience and risk management.

Focus on Aftermarket Services: Aftermarket services, including maintenance, repair, and overhaul (MRO), present opportunities for revenue generation and customer engagement. Brake manufacturers should invest in aftermarket support capabilities, such as spare parts logistics, technical services, and predictive maintenance solutions, to enhance customer satisfaction and loyalty.

Collaborate for Innovation: Strategic partnerships and collaborations with aerospace OEMs, technology suppliers, and academic institutions enable brake manufacturers to access complementary capabilities, share risks and rewards, and accelerate innovation in materials, technologies, and product development.

Future Outlook

The aerospace and defense brake market is expected to rebound from the Covid-19 pandemic and witness steady growth in the coming years, driven by factors such as increasing air travel demand, defense modernization programs, and technological advancements. Key trends such as lightweighting, electrification, digitalization, and autonomy will shape the future of aerospace and defense braking systems, offering opportunities for innovation, differentiation, and growth in the global market.

Conclusion

The aerospace and defense brake market plays a critical role in ensuring the safety, performance, and reliability of aircraft and defense systems worldwide. Despite challenges such as regulatory compliance, supply chain disruptions, and market competition, brake manufacturers continue to innovate, collaborate, and adapt to evolving industry trends and customer requirements. By investing in sustainable technologies, strengthening supply chain resilience, focusing on aftermarket services, and fostering innovation through collaboration, brake manufacturers can navigate market dynamics, capitalize on growth opportunities, and contribute to the advancement of aerospace and defense capabilities in the future.

What is Aerospace & Defense Brake?

Aerospace & Defense Brake refers to the braking systems used in aircraft and defense vehicles, designed to ensure safety and performance during operations. These brakes are critical for various applications, including commercial aviation, military aircraft, and ground defense systems.

What are the key players in the Aerospace & Defense Brake Market?

Key players in the Aerospace & Defense Brake Market include Honeywell International Inc., Safran S.A., and Parker Hannifin Corporation, among others. These companies are known for their innovative braking solutions and extensive experience in the aerospace and defense sectors.

What are the main drivers of growth in the Aerospace & Defense Brake Market?

The main drivers of growth in the Aerospace & Defense Brake Market include the increasing demand for advanced braking systems in new aircraft designs, the rise in defense spending, and the need for enhanced safety features in aviation. Additionally, technological advancements are contributing to the development of more efficient braking solutions.

What challenges does the Aerospace & Defense Brake Market face?

The Aerospace & Defense Brake Market faces challenges such as stringent regulatory requirements, high manufacturing costs, and the need for continuous innovation to meet evolving safety standards. These factors can impact the speed of product development and market entry.

What opportunities exist in the Aerospace & Defense Brake Market?

Opportunities in the Aerospace & Defense Brake Market include the growing trend towards electric and hybrid aircraft, which require specialized braking systems. Additionally, the expansion of unmanned aerial vehicles (UAVs) presents new avenues for brake technology development.

What trends are shaping the Aerospace & Defense Brake Market?

Trends shaping the Aerospace & Defense Brake Market include the integration of smart technologies for predictive maintenance, the use of lightweight materials to improve fuel efficiency, and the increasing focus on sustainability in manufacturing processes. These trends are driving innovation and enhancing the performance of braking systems.

Leading Companies in the Aerospace and Defense Brake Market:

Honeywell International Inc.

Safran S.A.

Raytheon Technologies Corporation

Meggitt PLC

Crane Aerospace & Electronics

Parker Hannifin Corporation

Beringer Aero

Matco Manufacturing Inc.

Cleveland Wheels & Brakes

Grove Aircraft Landing Gear Systems Inc.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.