The variable life insurance market represents a significant segment within the broader life insurance industry, offering policyholders a unique combination of life insurance coverage and investment opportunities. Variable life insurance policies allow policyholders to allocate their premiums into various investment options such as mutual funds, stocks, and bonds, providing the potential for cash value growth over time. This market segment has gained popularity among individuals seeking life insurance protection along with the flexibility to tailor their investment strategies to their financial goals and risk tolerance.

Meaning

Variable life insurance refers to a type of permanent life insurance policy that combines a death benefit with a savings component linked to investment options. Unlike traditional whole life insurance, where the cash value grows at a fixed rate, variable life insurance allows policyholders to invest in separate accounts, typically mutual funds, whose performance determines the cash value accumulation. This market segment appeals to individuals seeking both life insurance coverage and the potential for investment growth within a single policy.

Executive Summary

The variable life insurance market has experienced steady growth driven by increasing demand for flexible financial planning solutions and investment opportunities. These policies offer policyholders the ability to customize their investment portfolios, potentially maximizing returns while providing life insurance protection. However, market participants face challenges such as regulatory compliance, market volatility, and competition from alternative investment products. Navigating these challenges while capitalizing on market opportunities is essential for sustained growth and success in this segment.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Demand for Flexibility: Consumers increasingly seek financial products that offer flexibility and customization to meet their unique needs and preferences. Variable life insurance policies appeal to individuals looking for both life insurance protection and investment flexibility.

Investment Potential: Variable life insurance policies provide policyholders with the opportunity to invest in a range of investment options, allowing them to tailor their portfolios based on their risk tolerance, investment objectives, and market outlook.

Regulatory Compliance: The variable life insurance market is subject to regulatory oversight to ensure transparency, fairness, and consumer protection. Compliance with regulatory requirements is essential for market participants to maintain trust and credibility with regulators and policyholders.

Competition from Alternatives: Variable life insurance policies compete with alternative investment products such as mutual funds, exchange-traded funds (ETFs), and retirement accounts, which offer different features, benefits, and investment options.

Market Drivers

Investment Flexibility: The ability to allocate premiums into various investment options provides policyholders with flexibility and control over their investment portfolios, potentially maximizing returns based on market performance.

Tax Advantages: Variable life insurance policies offer tax-deferred growth of cash value and tax-free death benefits, providing policyholders with valuable tax advantages and estate planning benefits.

Wealth Transfer Strategies: Variable life insurance policies can serve as effective wealth transfer vehicles, allowing policyholders to pass on tax-free assets to beneficiaries while potentially leveraging cash value accumulation for supplemental income during retirement.

Financial Planning Solutions: Variable life insurance policies offer a comprehensive financial planning solution by combining life insurance coverage with investment opportunities, addressing multiple financial needs and goals within a single policy.

Market Restraints

Market Volatility: The performance of variable life insurance policies is subject to market fluctuations, which may result in fluctuations in cash value accumulation and investment returns, posing risks to policyholders’ financial objectives and expectations.

Regulatory Compliance: Compliance with regulatory requirements, including investment restrictions, disclosure obligations, and sales practices, can pose challenges for market participants, impacting product design, distribution, and marketing strategies.

Complexity and Transparency: Variable life insurance policies are complex financial products that require careful consideration of policy terms, investment options, fees, and risks. Ensuring transparency and clarity in product disclosures and communications is essential to building trust and confidence with consumers.

Cost Considerations: Variable life insurance policies often have higher premiums and fees compared to traditional life insurance products, which may limit affordability and accessibility for some consumers, particularly those with limited financial resources or risk tolerance.

Market Opportunities

Education and Awareness: Educating consumers about the benefits, features, and risks of variable life insurance policies can help increase market awareness and penetration, empowering individuals to make informed decisions about their financial planning needs.

Innovation in Product Design: Innovating product features such as investment options, fee structures, policy riders, and digital tools can enhance the attractiveness and competitiveness of variable life insurance policies in the market.

Targeted Marketing Strategies: Targeting specific demographic segments such as high-net-worth individuals, business owners, and pre-retirees can help tailor marketing efforts and messaging to address unique financial needs, preferences, and concerns.

Regulatory Compliance and Consumer Protection: Proactively addressing regulatory compliance requirements and consumer protection measures can build trust and credibility with regulators, investors, and policyholders, fostering long-term relationships and sustainable growth.

Market Dynamics

The variable life insurance market operates within a dynamic landscape shaped by factors such as consumer preferences, market conditions, regulatory developments, and competitive pressures. Market participants must navigate these dynamics effectively, adapting strategies and offerings to meet evolving customer needs and preferences while addressing regulatory requirements and market challenges.

Regional Analysis

The variable life insurance market exhibits regional variations influenced by factors such as socioeconomic conditions, cultural norms, regulatory environments, and consumer behaviors. Tailoring product offerings, marketing strategies, and distribution channels to specific regional characteristics and preferences can enhance market relevance and competitiveness.

Competitive Landscape

Leading Companies in the Variable Life Insurance Market:

Prudential Financial

MetLife

New York Life Insurance Company

Northwestern Mutual

AXA Equitable Life Insurance Company

Lincoln National Corporation

MassMutual (Massachusetts Mutual Life Insurance Company)

Transamerica

Guardian Life Insurance Company of America

Nationwide Mutual Insurance Company

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

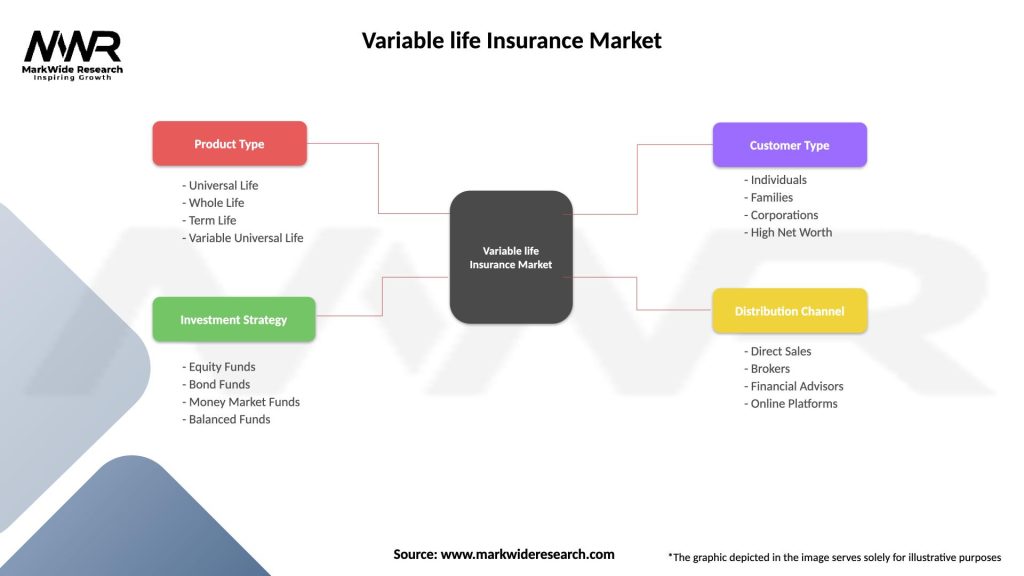

Segmentation

The variable life insurance market can be segmented based on factors such as policy features, investment options, premium structures, and target demographics. Segmentation allows market participants to tailor their offerings and marketing strategies to specific customer segments, addressing unique needs, preferences, and risk profiles.

Category-wise Insights

Investment Options: Variable life insurance policies offer a range of investment options, including equity funds, bond funds, money market funds, and balanced funds, allowing policyholders to diversify their investment portfolios based on their risk tolerance and investment objectives.

Policy Riders: Variable life insurance policies may offer optional policy riders such as accelerated death benefits, waiver of premium, and long-term care riders, providing additional benefits and flexibility to policyholders.

Fee Structures: Variable life insurance policies typically have fee structures that include mortality and expense charges, administrative fees, investment management fees, and surrender charges, which impact policy performance and cash value accumulation over time.

Premium Flexibility: Variable life insurance policies may offer premium flexibility options such as adjustable death benefits, flexible premium payments, and partial withdrawals, allowing policyholders to adapt their coverage and premiums to changing financial circumstances.

Key Benefits for Industry Participants and Stakeholders

Revenue Generation: Variable life insurance policies represent a significant source of revenue for life insurance companies, financial advisors, and distribution partners through premiums, fees, and investment management services.

Client Relationships: Variable life insurance policies enable financial advisors to deepen client relationships by offering comprehensive financial planning solutions that address both insurance and investment needs, fostering long-term loyalty and trust.

Competitive Advantage: Offering variable life insurance policies allows insurance companies and financial advisors to differentiate themselves in the market, attract affluent clients, and compete more effectively against alternative investment products.

Regulatory Compliance: Adhering to regulatory requirements and consumer protection measures helps insurance companies and financial advisors maintain compliance, avoid legal risks, and uphold their reputation and credibility in the marketplace.

SWOT Analysis

Strengths: Variable life insurance policies offer policyholders a unique combination of life insurance protection, investment opportunities, tax advantages, and flexibility, providing comprehensive financial planning solutions for diverse needs and objectives.

Weaknesses: Variable life insurance policies may face challenges such as market volatility, regulatory scrutiny, complexity, and cost considerations, limiting market penetration and adoption rates among certain consumer segments.

Opportunities: Educating consumers about the benefits and potential risks of variable life insurance policies, innovating product features, targeting specific demographic segments, and addressing regulatory concerns can unlock growth opportunities and expand market share.

Threats: Regulatory changes, economic downturns, market volatility, and competition from alternative investment products pose threats to the variable life insurance market, requiring market participants to adapt and innovate to maintain competitiveness.

Market Key Trends

Digital Transformation: Market participants are embracing digital technologies to enhance customer engagement, streamline operations, and facilitate remote transactions, catering to tech-savvy consumers’ preferences for digital interactions and services.

Regulatory Compliance: Proactive compliance measures, product disclosures, and consumer protection initiatives are essential for market participants to navigate regulatory complexities and maintain trust and credibility with regulators, investors, and customers.

Product Innovation: Innovations in product features such as investment options, fee structures, policy riders, and digital tools enhance the attractiveness and competitiveness of variable life insurance policies, addressing evolving customer needs and preferences.

Investment Strategies: Market participants are offering customizable investment strategies, risk management solutions, and portfolio diversification options within variable life insurance policies to meet policyholders’ unique investment objectives, risk tolerance, and market outlook.

Covid-19 Impact

The COVID-19 pandemic has influenced consumer behavior, market dynamics, and regulatory developments in the variable life insurance market. While the pandemic’s economic impact and market volatility may pose challenges in the short term, the long-term outlook remains positive as consumers prioritize financial protection, investment opportunities, and estate planning strategies amidst economic uncertainties and evolving market conditions.

Key Industry Developments

Digital Distribution Channels: The adoption of digital distribution channels such as online platforms, mobile apps, and virtual consultations enables insurance companies and financial advisors to reach and engage with consumers effectively, offering convenient and accessible financial planning solutions in a rapidly evolving digital landscape.

Regulatory Compliance: Proactive compliance measures, product disclosures, and consumer protection initiatives are essential for insurance companies and financial advisors to navigate regulatory complexities and maintain trust and credibility with regulators, investors, and policyholders, fostering long-term relationships and sustainable growth.

Product Innovation: Innovating product features such as investment options, fee structures, policy riders, and digital tools enhances the attractiveness and competitiveness of variable life insurance policies, addressing evolving customer needs and preferences in a dynamic marketplace.

Market Education Initiatives: Educating consumers about the benefits, features, and risks of variable life insurance policies through financial literacy programs, educational materials, and personalized consultations helps increase market awareness, confidence, and adoption rates among target demographics.

Analyst Suggestions

Educate Consumers: Market participants should invest in consumer education initiatives to raise awareness about the benefits, features, and potential risks of variable life insurance policies, empowering consumers to make informed decisions about their financial planning needs and objectives.

Innovate Products: Continuous innovation in product design, investment options, fee structures, policy riders, and digital tools enhances the attractiveness and competitiveness of variable life insurance policies, addressing evolving customer preferences and market dynamics.

Enhance Transparency: Transparency in product disclosures, pricing, performance metrics, and policy terms is critical to building trust and confidence with consumers, regulators, and investors, fostering long-term relationships and sustainable growth in the variable life insurance market.

Strengthen Regulatory Compliance: Proactively addressing regulatory compliance requirements and consumer protection measures helps insurance companies and financial advisors maintain trust and credibility with regulators, investors, and policyholders, ensuring compliance with legal and ethical standards in the marketplace.

Future Outlook

The variable life insurance market is poised for continued growth and innovation, driven by factors such as increasing consumer demand for financial protection and investment opportunities, regulatory developments, technological advancements, and market expansion initiatives. Market participants must adapt to changing dynamics, seize emerging opportunities, and address evolving challenges to capitalize on market potential and achieve long-term success in this dynamic and evolving segment.

Conclusion

In conclusion, the variable life insurance market offers policyholders a unique combination of life insurance coverage and investment opportunities, catering to diverse financial planning needs and objectives. Despite challenges such as market volatility, regulatory scrutiny, and competition from alternative investment products, the market presents significant growth potential driven by increasing consumer demand for flexible financial solutions and investment opportunities. By prioritizing consumer education, product innovation, regulatory compliance, and market expansion initiatives, insurance companies and financial advisors can navigate market dynamics effectively and position themselves for sustained growth and success in meeting the evolving needs of policyholders and investors alike.

What is Variable life Insurance?

Variable life insurance is a type of permanent life insurance that combines a death benefit with an investment component. Policyholders can allocate their premiums to various investment options, allowing the cash value to fluctuate based on market performance.

Who are the key players in the Variable life Insurance Market?

Key players in the variable life insurance market include MetLife, Prudential Financial, and AIG, among others. These companies offer a range of products that cater to different consumer needs and investment strategies.

What are the growth factors driving the Variable life Insurance Market?

The growth of the variable life insurance market is driven by increasing consumer awareness of investment options, the demand for flexible insurance products, and the rising need for long-term financial planning. Additionally, favorable regulatory changes are also contributing to market expansion.

What challenges does the Variable life Insurance Market face?

The variable life insurance market faces challenges such as market volatility, which can affect the cash value of policies, and regulatory scrutiny that may impose stricter compliance requirements. Additionally, consumer skepticism regarding investment risks can hinder market growth.

What opportunities exist in the Variable life Insurance Market?

Opportunities in the variable life insurance market include the development of innovative products that cater to younger consumers and the integration of technology for better customer engagement. There is also potential for growth in emerging markets where insurance penetration is low.

What trends are shaping the Variable life Insurance Market?

Trends in the variable life insurance market include a shift towards digital platforms for policy management and investment tracking, as well as an increasing focus on sustainable investment options. Additionally, personalized insurance solutions are becoming more popular among consumers.

Leading Companies in the Variable Life Insurance Market:

Prudential Financial

MetLife

New York Life Insurance Company

Northwestern Mutual

AXA Equitable Life Insurance Company

Lincoln National Corporation

MassMutual (Massachusetts Mutual Life Insurance Company)

Transamerica

Guardian Life Insurance Company of America

Nationwide Mutual Insurance Company

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.