The US surplus lines insurance market occupies a crucial niche within the broader insurance industry, providing coverage for risks that cannot be insured through standard admitted insurance carriers. Surplus lines insurance, also known as non-admitted insurance, offers specialized coverage for unique and high-risk exposures that fall outside the underwriting guidelines of traditional insurance companies. This market serves a diverse range of clients, including businesses, organizations, and individuals seeking customized insurance solutions tailored to their specific needs and risk profiles.

Meaning

Surplus lines insurance refers to the segment of the insurance market that provides coverage for risks deemed too complex, unusual, or high-risk to be underwritten by standard admitted insurance carriers. These risks may include emerging industries, specialized professions, unusual property types, and catastrophic events that traditional insurers are unwilling or unable to cover. Surplus lines insurers, also known as non-admitted carriers, operate with greater flexibility and underwriting discretion, allowing them to accommodate unique risk exposures and offer innovative insurance solutions.

Executive Summary

The US surplus lines insurance market plays a vital role in the insurance ecosystem, filling gaps in coverage and providing solutions for hard-to-place risks. With a focus on innovation, flexibility, and specialized expertise, surplus lines insurers cater to clients with unique insurance needs, offering coverage for emerging industries, non-standard risks, and challenging exposures. Despite regulatory complexities and market challenges, the surplus lines market continues to thrive, driven by factors such as increased demand for specialty coverage, evolving risk landscapes, and technological advancements shaping the future of insurance.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Specialized Coverage: The US surplus lines insurance market offers specialized coverage for a wide range of risks, including professional liability, cyber liability, directors and officers (D&O) liability, excess and umbrella liability, and property and casualty risks. These policies are tailored to the specific needs and risk profiles of clients who cannot obtain coverage through standard admitted carriers.

Risk Appetite: Surplus lines insurers have a higher risk appetite than traditional admitted carriers, allowing them to underwrite non-standard risks and unique exposures that may be deemed too risky or complex by standard insurers. This flexibility enables surplus lines insurers to fill coverage gaps and provide solutions for hard-to-place risks.

Market Dynamics: The US surplus lines insurance market operates in a dynamic environment influenced by factors such as regulatory changes, market conditions, emerging risks, and technological advancements. Understanding these dynamics is essential for surplus lines insurers to adapt to evolving market trends and meet the needs of their clients effectively.

Distribution Channels: Surplus lines insurance is typically distributed through specialized brokers and intermediaries known as surplus lines brokers. These brokers have expertise in placing non-standard risks and navigating the complexities of the surplus lines market, serving as intermediaries between clients and surplus lines insurers.

Market Drivers

Demand for Specialty Coverage: The increasing complexity of risks and the emergence of new industries drive demand for specialty insurance coverage not available through standard admitted carriers. Surplus lines insurers fill this demand by offering customized solutions tailored to the unique needs of clients.

Evolving Risk Landscapes: Rapid technological advancements, changing regulatory environments, and emerging risks such as cyber threats, climate change, and pandemics create new challenges and opportunities for the insurance industry. Surplus lines insurers are well-positioned to address these evolving risk landscapes and provide innovative solutions.

Market Capacity: Surplus lines insurers play a crucial role in providing additional capacity to the insurance market, particularly during periods of hardening market conditions or capacity constraints. Their ability to underwrite non-standard risks and absorb excess and surplus lines enables them to supplement the capacity of traditional insurers and support the needs of clients.

Technological Advancements: Technological innovations such as artificial intelligence (AI), data analytics, and digital platforms are reshaping the surplus lines insurance market, enhancing underwriting efficiency, improving risk assessment, and enabling faster policy issuance and claims processing.

Market Restraints

Regulatory Compliance: Surplus lines insurers operate under a complex regulatory framework governed by state insurance laws and regulations. Compliance with regulatory requirements, including licensing, surplus lines taxes, and reporting obligations, can pose challenges for surplus lines insurers operating in multiple jurisdictions.

Market Volatility: The surplus lines insurance market is subject to fluctuations in market conditions, including changes in insurance capacity, pricing trends, and underwriting guidelines. Market volatility can impact the availability and affordability of surplus lines coverage, posing challenges for clients and insurers alike.

Legal and Litigation Risks: Surplus lines insurers face legal and litigation risks associated with underwriting non-standard risks and complex insurance contracts. Disputes over policy interpretation, coverage disputes, and claims litigation can result in financial losses and reputational damage for insurers.

Competitive Pressures: Surplus lines insurers face competitive pressures from traditional admitted carriers, alternative risk transfer mechanisms, and emerging insurtech startups. Maintaining a competitive edge in the surplus lines market requires differentiation through product innovation, underwriting expertise, and client service excellence.

Market Opportunities

Innovation in Product Development: Surplus lines insurers have opportunities to innovate in product development by introducing new coverage solutions, enhancing existing products, and addressing emerging risks such as cyber liability, climate change, and supply chain disruptions.

Expansion into Niche Markets: Surplus lines insurers can expand into niche markets and underserved segments by developing specialized insurance programs tailored to the needs of specific industries, professions, or geographic regions.

Partnerships and Collaborations: Collaborating with insurtech startups, technology providers, and industry partners can enable surplus lines insurers to leverage technological advancements, enhance underwriting capabilities, and improve operational efficiency.

Risk Mitigation Services: Offering risk management and loss prevention services in addition to insurance coverage can add value for clients and differentiate surplus lines insurers in the market. Services such as risk assessments, safety training, and claims management can help clients reduce their exposure to risks and mitigate losses.

Market Dynamics

The US surplus lines insurance market operates in a dynamic and evolving landscape characterized by shifting market conditions, regulatory developments, emerging risks, and technological advancements. Key market dynamics shaping the surplus lines insurance market include:

Regulatory Environment: Surplus lines insurers must navigate a complex regulatory environment governed by state insurance laws and regulations. Compliance with licensing requirements, surplus lines taxes, and reporting obligations is essential for insurers operating in multiple jurisdictions.

Market Conditions: Market conditions in the surplus lines insurance market are influenced by factors such as insurance capacity, pricing trends, underwriting guidelines, and claims experience. Fluctuations in market conditions can impact the availability and affordability of surplus lines coverage for clients.

Emerging Risks: Emerging risks such as cyber threats, climate change, pandemics, and geopolitical uncertainties present new challenges and opportunities for surplus lines insurers. Developing innovative solutions to address these emerging risks is essential for insurers to remain competitive and meet the evolving needs of clients.

Technological Advancements: Technological innovations such as artificial intelligence, data analytics, and digital platforms are reshaping the surplus lines insurance market. Insurers are leveraging technology to enhance underwriting efficiency, improve risk assessment, and streamline policy administration processes.

Regional Analysis

The US surplus lines insurance market operates across all 50 states and the District of Columbia, with varying regulatory environments and market conditions in each jurisdiction. While surplus lines insurance is regulated at the state level, the National Association of Insurance Commissioners (NAIC) provides guidance and oversight to promote consistency and uniformity in surplus lines regulation nationwide. Key regional factors influencing the surplus lines market include:

State Insurance Laws: Each state has its own insurance laws and regulations governing surplus lines insurance, including licensing requirements, surplus lines taxes, eligibility criteria, and reporting obligations. Compliance with state regulations is essential for surplus lines insurers operating in multiple jurisdictions.

Market Conditions: Market conditions in the surplus lines insurance market vary by region, influenced by factors such as insurance capacity, pricing trends, underwriting appetites, and claims experience. Regional differences in market conditions can impact the availability and affordability of surplus lines coverage for clients.

Competitive Landscape: The competitive landscape of the surplus lines insurance market varies by region, with differences in market share, distribution channels, and competitive pressures. Understanding regional market dynamics and competitor strategies is essential for insurers to effectively compete and grow their market presence.

Industry Trends: Regional factors such as economic trends, industry composition, and regulatory developments influence demand for surplus lines insurance and market opportunities. Insurers must monitor regional industry trends and adapt their strategies to capitalize on emerging opportunities and mitigate risks.

Competitive Landscape

Leading Companies in US Surplus Lines Insurance Market:

Lloyd’s of London

American International Group (AIG)

Berkshire Hathaway Specialty Insurance (BHSI)

Zurich Insurance Group

Chubb Limited

Markel Corporation

AXIS Capital Holdings Limited

Hiscox Ltd

Beazley Group plc

Tokio Marine HCC

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

The US surplus lines insurance market can be segmented based on various factors, including:

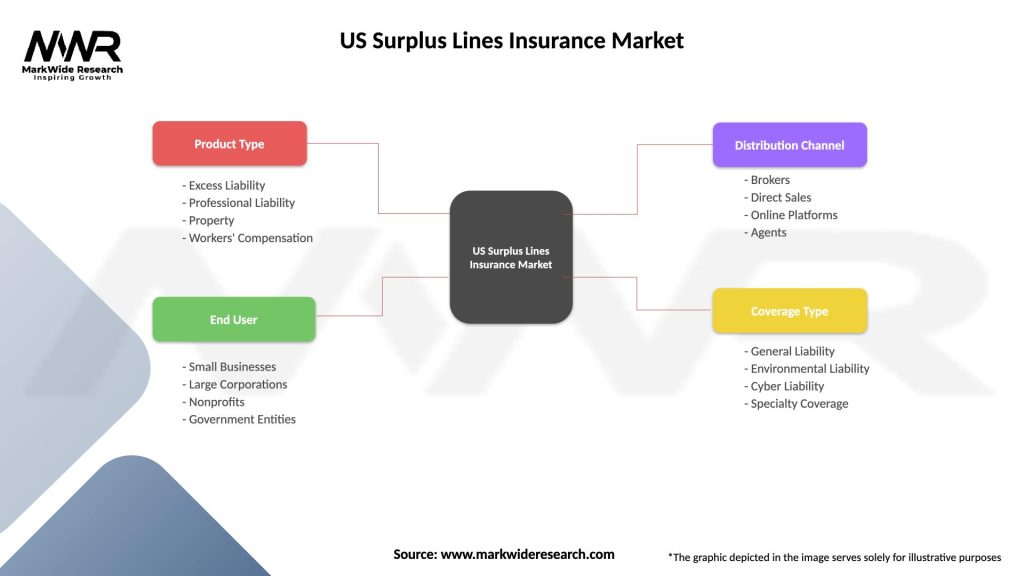

Product Type: Segmentation by product type includes property and casualty insurance, professional liability insurance, directors and officers (D&O) liability insurance, cyber liability insurance, and specialty lines coverage.

Industry Vertical: Segmentation by industry vertical includes sectors such as construction, real estate, healthcare, manufacturing, technology, and transportation.

Geography: Segmentation by geography includes regional markets, state markets, and metropolitan areas with varying market dynamics and demand for surplus lines coverage.

Distribution Channel: Segmentation by distribution channel includes surplus lines brokers, retail agents, managing general agents (MGAs), wholesale brokers, and online platforms facilitating insurance placement.

Category-wise Insights

Property and Casualty Insurance: Property and casualty insurance provide coverage for physical assets and liability exposures, including commercial property, general liability, workers’ compensation, and commercial auto risks.

Professional Liability Insurance: Professional liability insurance protects professionals against claims alleging negligence, errors, or omissions in the performance of professional services, including lawyers, doctors, architects, engineers, and consultants.

Directors and Officers (D&O) Liability Insurance: D&O liability insurance provides coverage for corporate directors and officers against claims alleging wrongful acts, mismanagement, or breaches of fiduciary duty in the performance of their duties.

Cyber Liability Insurance: Cyber liability insurance protects businesses against cyber risks and data breaches, including data theft, network security breaches, and privacy violations resulting in financial losses or legal liabilities.

Key Benefits for Industry Participants and Stakeholders

Specialized Coverage: Surplus lines insurance offers specialized coverage for unique and high-risk exposures that cannot be insured through standard admitted carriers, providing solutions for hard-to-place risks.

Risk Transfer: Surplus lines insurance enables businesses to transfer and mitigate their exposure to complex and emerging risks by accessing coverage solutions tailored to their specific needs and risk profiles.

Market Capacity: Surplus lines insurers supplement the capacity of the insurance market by underwriting non-standard risks and providing additional coverage options during periods of hardening market conditions or capacity constraints.

Flexibility and Innovation: Surplus lines insurers operate with greater flexibility and underwriting discretion, allowing them to innovate in product development, underwriting guidelines, and risk assessment methodologies to meet evolving market needs.

SWOT Analysis

Strengths:

Specialized expertise in underwriting complex and high-risk exposures

Flexibility in underwriting and risk assessment

Capacity to provide coverage for hard-to-place risks

Innovation in product development and risk management solutions

Weaknesses:

Regulatory compliance challenges and licensing requirements

Vulnerability to market volatility and pricing fluctuations

Legal and litigation risks associated with non-standard insurance contracts

Dependence on broker relationships and distribution channels

Opportunities:

Expansion into emerging markets and niche segments

Development of innovative coverage solutions for evolving risks

Collaboration with technology partners to enhance underwriting capabilities

Focus on risk mitigation services and loss prevention initiatives

Threats:

Regulatory changes impacting surplus lines eligibility and compliance

Competitive pressures from traditional admitted carriers and alternative risk transfer mechanisms

Market disruptions due to catastrophic events, economic downturns, or geopolitical uncertainties

Technological advancements reshaping the insurance industry and distribution channels

Market Key Trends

Digital Transformation: Surplus lines insurers are embracing digital transformation initiatives, including online platforms, electronic policy issuance, and data analytics, to enhance operational efficiency, streamline underwriting processes, and improve customer experiences.

Cyber Risk Management: The increasing frequency and severity of cyber threats are driving demand for cyber liability insurance and risk management solutions. Surplus lines insurers are developing innovative coverage options and risk mitigation services to address evolving cyber risks.

Alternative Capital: Surplus lines insurers are exploring alternative capital sources, including insurance-linked securities (ILS), catastrophe bonds, and collateralized reinsurance, to supplement traditional reinsurance capacity and manage catastrophe exposures more effectively.

Climate Resilience: Climate change and natural catastrophes pose significant challenges for the insurance industry. Surplus lines insurers are developing climate resilience strategies, including catastrophe modeling, risk assessment tools, and resilience planning, to mitigate climate-related risks and losses.

Covid-19 Impact

The Covid-19 pandemic has had a profound impact on the US surplus lines insurance market, disrupting business operations, shifting risk landscapes, and accelerating digital transformation initiatives. Some key impacts of Covid-19 on the surplus lines market include:

Business Interruption Claims: The pandemic has triggered a surge in business interruption claims, with businesses seeking coverage for revenue losses resulting from government-mandated shutdowns and operational disruptions.

Remote Workforce: The shift to remote work arrangements has increased cyber risks and data security vulnerabilities, driving demand for cyber liability insurance and risk management services to protect businesses from cyber threats.

Pandemic Exclusions: Surplus lines insurers have introduced pandemic exclusions and limitations in commercial insurance policies to mitigate exposure to Covid-19-related losses, including event cancellations, travel disruptions, and supply chain interruptions.

Claims Handling Challenges: The pandemic has posed challenges for claims handling and settlement processes, including delays in claims processing, remote inspections, and disputes over coverage interpretations, leading to increased litigation and claims costs.

Key Industry Developments

Regulatory Updates: Regulatory developments impacting surplus lines insurance include changes in surplus lines eligibility requirements, licensing standards, tax regulations, and reporting obligations. Insurers must stay abreast of regulatory changes and compliance requirements to ensure continued market access and operational compliance.

Market Consolidation: The surplus lines insurance market is experiencing consolidation through mergers, acquisitions, and strategic partnerships among insurers, brokers, and managing general agents (MGAs). Market consolidation can lead to economies of scale, enhanced distribution networks, and increased market share for industry participants.

Claims Innovation: Surplus lines insurers are investing in claims innovation initiatives to enhance claims handling processes, improve customer experiences, and expedite claims settlements. Technologies such as artificial intelligence, claims analytics, and digital platforms are being deployed to streamline claims workflows and reduce claims cycle times.

Diversity and Inclusion: The insurance industry is prioritizing diversity, equity, and inclusion initiatives to foster a more inclusive workplace culture and promote diversity among leadership teams, workforce, and distribution channels. Surplus lines insurers are implementing diversity programs, unconscious bias training, and recruitment strategies to attract and retain diverse talent and foster a culture of belonging.

Analyst Suggestions

Focus on Risk Assessment: Surplus lines insurers should prioritize risk assessment and underwriting discipline to maintain profitability and manage exposure to complex and emerging risks effectively. Investing in data analytics, risk modeling, and predictive analytics can enhance underwriting accuracy and decision-making processes.

Enhance Digital Capabilities: Digital transformation is essential for surplus lines insurers to improve operational efficiency, enhance customer experiences, and stay competitive in the digital age. Insurers should invest in digital platforms, electronic policy issuance, and customer portals to streamline processes and facilitate remote interactions with clients and distribution partners.

Collaborate with Insurtech Startups: Collaboration with insurtech startups and technology partners can enable surplus lines insurers to leverage innovative technologies, accelerate digital transformation initiatives, and address emerging market needs. Partnerships in areas such as data analytics, artificial intelligence, and blockchain can enhance underwriting capabilities, streamline operations, and drive business growth.

Diversify Product Portfolio: Surplus lines insurers should diversify their product portfolio to address evolving market needs and emerging risks. Developing innovative coverage solutions for niche markets, specialty risks, and emerging industries can differentiate insurers in the market and unlock new growth opportunities.

Future Outlook

The future outlook for the US surplus lines insurance market remains positive, with continued growth expected driven by factors such as increasing demand for specialty coverage, evolving risk landscapes, technological advancements, and regulatory developments. Surplus lines insurers that adapt to changing market dynamics, innovate in product development, embrace digital transformation, and prioritize risk management will be well-positioned to capitalize on emerging opportunities and maintain a competitive edge in the dynamic and rapidly evolving insurance landscape.

Conclusion

The US surplus lines insurance market plays a vital role in the insurance ecosystem, providing coverage for unique and high-risk exposures that fall outside the underwriting guidelines of standard admitted carriers. With a focus on innovation, flexibility, and specialized expertise, surplus lines insurers cater to clients with diverse insurance needs, offering customized solutions for emerging industries, non-standard risks, and challenging exposures. Despite regulatory complexities and market challenges, the surplus lines market continues to thrive, driven by increasing demand for specialty coverage, evolving risk landscapes, and technological advancements shaping the future of insurance. By understanding market trends, embracing digital transformation, and prioritizing risk management, surplus lines insurers can navigate challenges, capitalize on growth prospects, and contribute to the resilience and sustainability of the US insurance market.

What is Surplus Lines Insurance?

Surplus Lines Insurance refers to coverage that is not available in the standard insurance market. It is often used for high-risk or unique situations, such as specialized industries or unusual property types.

What are the key players in the US Surplus Lines Insurance Market?

Key players in the US Surplus Lines Insurance Market include companies like Lloyd’s of London, Berkshire Hathaway, and Markel Corporation, among others.

What are the growth factors driving the US Surplus Lines Insurance Market?

The growth of the US Surplus Lines Insurance Market is driven by increasing demand for specialized coverage, the rise of new industries, and the need for flexible insurance solutions for unique risks.

What challenges does the US Surplus Lines Insurance Market face?

Challenges in the US Surplus Lines Insurance Market include regulatory complexities, competition from standard insurers, and the need for continuous innovation to meet evolving customer needs.

What opportunities exist in the US Surplus Lines Insurance Market?

Opportunities in the US Surplus Lines Insurance Market include expanding into emerging sectors, leveraging technology for better risk assessment, and developing tailored products for niche markets.

What trends are shaping the US Surplus Lines Insurance Market?

Trends in the US Surplus Lines Insurance Market include the increasing use of data analytics for underwriting, a focus on sustainability in insurance practices, and the growth of cyber insurance as a critical coverage area.

Leading Companies in US Surplus Lines Insurance Market:

Lloyd’s of London

American International Group (AIG)

Berkshire Hathaway Specialty Insurance (BHSI)

Zurich Insurance Group

Chubb Limited

Markel Corporation

AXIS Capital Holdings Limited

Hiscox Ltd

Beazley Group plc

Tokio Marine HCC

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.