The Europe Mortgage Lending Market is a crucial component of the region’s financial sector, facilitating access to housing finance for individuals and families across diverse economic and social backgrounds. Mortgage lending involves the provision of loans secured by real estate properties, enabling borrowers to purchase homes, invest in real estate, or access capital for various purposes. With its role in promoting homeownership, driving economic growth, and supporting financial stability, the Europe Mortgage Lending Market plays a vital role in the region’s housing market and broader economy.

Meaning

Mortgage lending refers to the process of extending loans to borrowers for the purpose of purchasing or refinancing real estate properties. These loans are secured by the underlying property, which serves as collateral for the loan. Mortgage lenders, such as banks, financial institutions, and mortgage brokers, assess the creditworthiness of borrowers, evaluate the value of the property, and determine the terms and conditions of the loan. Mortgage lending enables individuals and families to achieve homeownership, invest in real estate, and access financing for personal or business purposes, contributing to economic growth and wealth accumulation.

Executive Summary

The Europe Mortgage Lending Market has experienced significant growth and evolution in recent years, driven by factors such as low interest rates, demographic trends, government policies, and technological advancements. Mortgage lending plays a central role in the housing market, providing financing solutions for homebuyers, real estate investors, and property developers. With increasing demand for housing and favorable economic conditions in Europe, the mortgage lending market presents opportunities for lenders, borrowers, and other stakeholders to participate in the homeownership journey and contribute to sustainable housing finance solutions.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Low Interest Rates: Historically low interest rates in Europe have stimulated demand for mortgage loans, making homeownership more affordable and accessible to a wider range of borrowers. Low borrowing costs incentivize homebuyers to enter the housing market and refinance existing mortgages, driving demand for mortgage lending products.

Demographic Trends: Changing demographics, including population growth, urbanization, and household formation, influence demand for housing and mortgage lending in Europe. Millennial homebuyers, aging populations, and migration trends shape housing preferences, affordability considerations, and mortgage product innovation in response to evolving consumer needs.

Government Policies: Government interventions, regulatory reforms, and housing policies impact the mortgage lending market in Europe. Measures such as first-time homebuyer programs, mortgage interest deductions, and affordability initiatives aim to promote homeownership, address housing affordability challenges, and mitigate systemic risks in the mortgage market.

Technological Advancements: Technological innovations in mortgage lending, including digital platforms, online mortgage applications, and automated underwriting systems, enhance operational efficiency, customer experience, and risk management for lenders and borrowers. Digitalization trends accelerate the digitization of mortgage processes, streamline loan origination, and improve access to mortgage credit for underserved populations.

Market Drivers

Housing Demand: Strong demand for housing, driven by population growth, urbanization, and lifestyle preferences, fuels demand for mortgage lending in Europe. Housing shortages, demographic shifts, and lifestyle changes contribute to increased homeownership aspirations and housing affordability challenges, stimulating mortgage market growth.

Low Interest Rates: Persistently low interest rates stimulate mortgage lending activity by reducing borrowing costs, lowering mortgage payments, and incentivizing homebuyers to enter the housing market. Low interest rate environments encourage mortgage refinancing, debt consolidation, and home equity extraction, driving demand for mortgage products and refinancing services.

Government Support: Government interventions, housing subsidies, and policy initiatives support mortgage lending and homeownership in Europe. First-time homebuyer programs, down payment assistance, and mortgage guarantee schemes enable access to mortgage credit for creditworthy borrowers, promote housing affordability, and mitigate risks in the mortgage market.

Economic Recovery: Economic growth, employment stability, and income growth support mortgage lending activity by enhancing borrower creditworthiness, reducing loan defaults, and stimulating housing demand. Improving economic conditions, consumer confidence, and housing market sentiment create favorable conditions for mortgage lending expansion and market growth in Europe.

Market Restraints

Regulatory Compliance: Stringent regulatory requirements, capital adequacy standards, and prudential regulations impose compliance burdens on mortgage lenders in Europe. Regulatory compliance costs, risk management obligations, and capital constraints limit mortgage lending capacity, constrain credit availability, and increase operational expenses for financial institutions operating in the mortgage market.

Credit Risk: Credit risk exposure, loan delinquencies, and default risks pose challenges for mortgage lenders in Europe. Economic uncertainties, borrower creditworthiness, and property market volatility influence credit risk assessment, loan underwriting standards, and risk management practices, affecting mortgage lending profitability and asset quality in the mortgage portfolio.

Interest Rate Risks: Interest rate fluctuations, yield curve dynamics, and monetary policy changes expose mortgage lenders to interest rate risks in Europe. Rising interest rates increase borrowing costs, reduce affordability, and dampen housing demand, impacting mortgage origination volumes, refinancing activity, and profitability for lenders with interest rate-sensitive mortgage portfolios.

Market Competition: Intense competition among mortgage lenders, banks, financial institutions, and non-bank lenders in Europe compresses profit margins, increases pricing pressures, and drives innovation in mortgage products and services. Market saturation, product commoditization, and customer churn challenge mortgage lenders to differentiate offerings, enhance customer value propositions, and retain market share in a competitive landscape.

Market Opportunities

Digital Transformation: Digitalization trends, online mortgage platforms, and fintech innovations create opportunities for mortgage lenders to streamline processes, enhance customer experience, and expand market reach in Europe. Digital mortgage origination, automated underwriting, and electronic document management improve efficiency, reduce costs, and accelerate loan processing for borrowers and lenders.

Inclusive Finance: Inclusive finance initiatives, affordable housing programs, and social impact investing promote access to mortgage credit for underserved populations, low-income households, and first-time homebuyers in Europe. Targeted lending programs, community development initiatives, and government partnerships address housing affordability challenges, reduce financial exclusion, and foster inclusive homeownership opportunities.

Green Mortgages: Sustainable finance, green lending, and energy-efficient mortgages support environmental sustainability and climate resilience in the housing sector. Green mortgage products, energy retrofit financing, and eco-friendly home improvements incentivize energy efficiency upgrades, renewable energy installations, and sustainable building practices, aligning mortgage lending with sustainability goals and ESG principles.

Partnerships and Collaborations: Strategic partnerships, cross-sector collaborations, and ecosystem alliances enable mortgage lenders to leverage synergies, expand distribution channels, and enhance value propositions in Europe. Partnerships with real estate agents, property developers, and housing associations facilitate customer referrals, market insights, and integrated solutions that meet evolving customer needs and market demands.

Market Dynamics

The European mortgage lending market is shaped by various dynamics, including economic conditions, regulatory changes, technological advancements, and housing market trends. Key dynamics influencing the market include:

Economic Indicators: Economic factors such as GDP growth, employment rates, and inflation impact mortgage demand and lending conditions.

Regulatory Landscape: National and EU-wide regulations affecting lending practices, consumer protection, and financial stability play a significant role in shaping the market.

Technological Advancement: Innovations in fintech and digital platforms are transforming the mortgage lending process, improving efficiency, and expanding access to mortgage products.

Regional Analysis

The European mortgage lending market exhibits varying trends and conditions across different regions:

Western Europe: Countries such as Germany, France, and the UK have well-developed mortgage markets with a high degree of regulation and a wide range of mortgage products. Low interest rates and strong housing demand drive market activity.

Northern Europe: Nordic countries like Sweden and Denmark have stable mortgage markets, supported by low interest rates and high levels of homeownership. Digital mortgage solutions are increasingly popular in this region.

Southern Europe: Southern European countries, including Spain and Italy, are experiencing a recovery in mortgage lending following the financial crisis. Rising property prices and economic recovery are influencing market dynamics.

Eastern Europe: Emerging markets in Eastern Europe, such as Poland and Hungary, are seeing growth in mortgage lending as economic conditions improve and homeownership rates rise.

Competitive Landscape

Leading Companies in the Europe Mortgage Lending Market:

HSBC Holdings plc

Barclays PLC

Lloyds Banking Group plc

Royal Bank of Scotland Group plc

Santander Group

Nationwide Building Society

BNP Paribas SA

ING Group N.V.

Credit Agricole Group

Deutsche Bank AG

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

The European mortgage lending market can be segmented based on various factors, including:

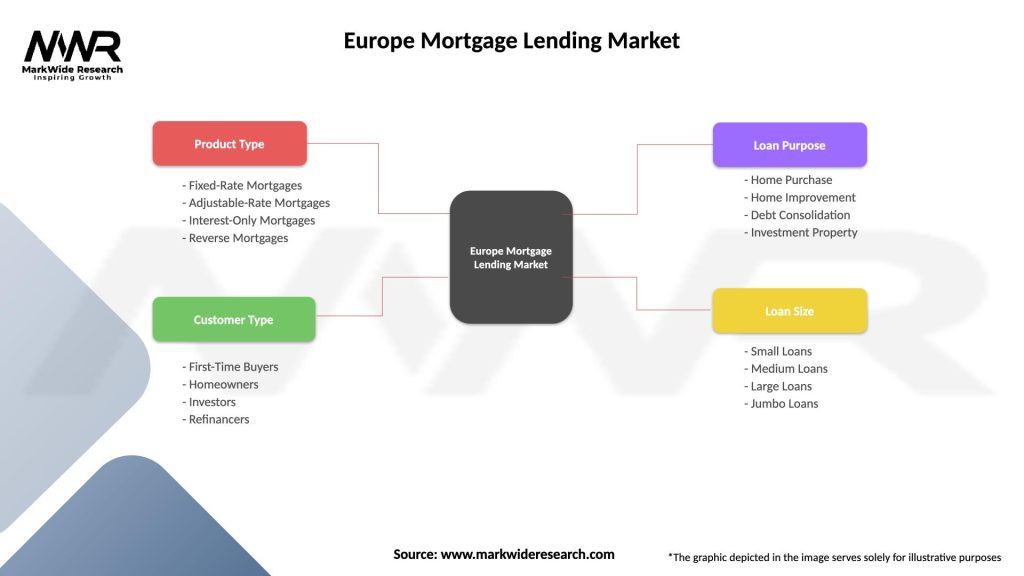

By Lender Type: Banks, Credit Institutions, Mortgage Brokers, Online Lenders

By Customer Type: Residential, Commercial, Buy-to-let

By Region: Western Europe, Northern Europe, Southern Europe, Eastern Europe

Category-wise Insights

Each category within the European mortgage lending market offers unique features and benefits:

Fixed-rate Mortgages: Provide stable monthly payments with a fixed interest rate for the duration of the loan, offering predictability and security for borrowers.

Adjustable-rate Mortgages: Feature interest rates that adjust periodically based on market conditions, potentially offering lower initial rates but with varying payments over time.

Interest-only Mortgages: Allow borrowers to pay only the interest for a specified period, which can result in lower initial payments but may increase the overall loan balance.

Reverse Mortgages: Designed for older borrowers, allowing them to convert home equity into cash while continuing to live in the property.

Key Benefits for Industry Participants and Stakeholders

The European mortgage lending market offers several benefits for lenders, borrowers, and stakeholders:

Revenue Growth: Lenders can capitalize on growing demand for mortgages and refinancing, driving revenue through interest income and fees.

Market Expansion: Opportunities for growth in emerging markets and underserved regions can expand lender reach and increase market share.

Customer Satisfaction: Offering a range of mortgage products and innovative solutions enhances customer satisfaction and loyalty.

Technological Advancements: Embracing digital transformation and fintech innovations can improve operational efficiency and streamline the mortgage application process.

SWOT Analysis

Strengths:

Low interest rates supporting mortgage affordability and demand.

Diverse range of mortgage products catering to different borrower needs.

Strong regulatory framework enhancing market stability and consumer protection.

Weaknesses:

Economic uncertainties impacting mortgage lending conditions and borrower confidence.

High competition among lenders affecting profit margins and pricing strategies.

Complex regulatory requirements posing challenges for compliance and operations.

Opportunities:

Growth in digital mortgage solutions and online platforms enhancing customer experience.

Development of innovative mortgage products addressing emerging trends and consumer preferences.

Expansion into emerging markets and underserved regions driving market growth.

Threats:

Economic downturns and financial instability affecting mortgage demand and credit risk.

Regulatory changes impacting lending practices and market dynamics.

Rising property prices leading to affordability issues and potential declines in mortgage volumes.

Market Key Trends

Key trends shaping the European mortgage lending market include:

Digital Transformation: Increasing adoption of digital platforms and technologies for mortgage applications, processing, and management.

Product Innovation: Development of new mortgage products and features to meet evolving consumer needs and preferences.

Regulatory Changes: Ongoing updates to regulations and standards affecting mortgage lending practices and compliance.

Economic Factors: Influences of economic conditions, such as interest rates and inflation, on mortgage demand and lending behavior.

Covid-19 Impact

The Covid-19 pandemic has had a notable impact on the European mortgage lending market:

Increased Mortgage Demand: The pandemic has led to a surge in mortgage refinancing and new mortgage applications due to historically low interest rates.

Economic Uncertainty: Economic challenges and uncertainties during the pandemic have affected housing market conditions and borrower confidence.

Acceleration of Digitalization: The pandemic has accelerated the adoption of digital mortgage solutions and remote application processes.

Key Industry Developments

Technological Innovations: Advances in fintech and digital platforms are transforming the mortgage lending process, improving efficiency and customer experience.

Product Enhancements: Introduction of new mortgage products and features to address changing consumer needs and market conditions.

Regulatory Adaptations: Evolving regulatory frameworks and standards shaping mortgage lending practices and market dynamics.

Analyst Suggestions

Based on market trends and developments, analysts suggest the following strategies for industry participants:

Embrace Digital Transformation: Invest in digital technologies and platforms to enhance the mortgage application process and improve customer experience.

Innovate Mortgage Products: Develop new and flexible mortgage products to meet diverse borrower needs and adapt to changing market conditions.

Monitor Regulatory Changes: Stay informed about regulatory developments and ensure compliance with evolving standards and requirements.

Explore Market Expansion: Identify growth opportunities in emerging markets and underserved regions to drive market expansion and increase reach.

Future Outlook

The future of the European mortgage lending market is optimistic, with continued growth and innovation expected. As economic conditions stabilize and consumer confidence rebounds, the demand for mortgage financing is anticipated to rise. Embracing digital transformation, adapting to regulatory changes, and focusing on product innovation will be key to capturing growth opportunities and achieving success in the evolving market.

Conclusion

In conclusion, the European mortgage lending market offers significant opportunities for lenders, borrowers, and stakeholders. Despite challenges such as economic uncertainties and regulatory complexities, the market is poised for growth driven by favorable interest rates, digital innovation, and evolving consumer preferences. By focusing on technological advancements, product innovation, and market expansion, industry participants can differentiate themselves, capture market share, and drive success in the European mortgage lending market.

What is Mortgage Lending?

Mortgage lending refers to the process of providing loans to individuals or businesses to purchase real estate, where the property itself serves as collateral. This process involves various financial institutions and can include different types of loans, such as fixed-rate and adjustable-rate mortgages.

What are the key players in the Europe Mortgage Lending Market?

Key players in the Europe Mortgage Lending Market include major banks and financial institutions such as Deutsche Bank, BNP Paribas, and Santander. These companies offer a range of mortgage products and services to consumers and businesses across Europe, among others.

What are the main drivers of the Europe Mortgage Lending Market?

The main drivers of the Europe Mortgage Lending Market include low interest rates, increasing property prices, and a growing demand for housing. Additionally, favorable government policies and economic recovery in various regions contribute to the market’s growth.

What challenges does the Europe Mortgage Lending Market face?

The Europe Mortgage Lending Market faces challenges such as regulatory changes, economic uncertainty, and rising property prices that may limit affordability for borrowers. Additionally, competition among lenders can lead to tighter margins and increased risk.

What opportunities exist in the Europe Mortgage Lending Market?

Opportunities in the Europe Mortgage Lending Market include the potential for digital transformation in lending processes, the rise of alternative lending platforms, and increasing demand for green mortgages. These trends can enhance customer experience and expand market reach.

What trends are shaping the Europe Mortgage Lending Market?

Trends shaping the Europe Mortgage Lending Market include the adoption of technology in loan processing, a shift towards sustainable lending practices, and the growing popularity of flexible mortgage products. These trends reflect changing consumer preferences and advancements in financial technology.

Leading Companies in the Europe Mortgage Lending Market:

HSBC Holdings plc

Barclays PLC

Lloyds Banking Group plc

Royal Bank of Scotland Group plc

Santander Group

Nationwide Building Society

BNP Paribas SA

ING Group N.V.

Credit Agricole Group

Deutsche Bank AG

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.