M2M (Machine-to-Machine) satellite communication is a revolutionary technology that enables devices to communicate with each other via satellite networks, eliminating the need for human intervention. This technology has gained significant traction in recent years, revolutionizing various industries such as transportation, agriculture, healthcare, and energy. In this comprehensive market analysis, we will delve into the meaning of M2M satellite communication, provide an executive summary, highlight key market insights, discuss market drivers, restraints, and opportunities, explore the market dynamics, analyze the regional landscape, evaluate the competitive landscape, present segmentation details, offer category-wise insights, outline the key benefits for industry participants and stakeholders, conduct a SWOT analysis, examine the market key trends, assess the impact of Covid-19, present key industry developments, provide analyst suggestions, offer a future outlook, and conclude with a summary of the findings.

M2M satellite communication refers to the seamless exchange of data and information between machines or devices via satellite networks. It enables devices to communicate with each other without the need for human intervention, leading to enhanced efficiency, improved decision-making, and increased automation. This technology has become a critical enabler for various applications, including remote monitoring, asset tracking, smart grid management, fleet management, and disaster management.

Executive Summary

The M2M satellite communication market has witnessed significant growth in recent years due to advancements in satellite technology and the increasing demand for connected solutions. This market analysis provides a comprehensive overview of key market insights, drivers, restraints, opportunities, and dynamics that shape the M2M satellite communication landscape. Additionally, it includes regional analysis, competitive landscape assessment, segmentation, SWOT analysis, and a future outlook.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Coverage Expansion: LEO deployments by SpaceX Starlink, OneWeb, and Amazon Kuiper are reducing latency from 600 ms (GEO) to under 50 ms, enabling near-real-time M2M applications.

Cost Reduction: Miniaturized, flat-panel M2M terminals under 10 cm and <$300 hardware cost accelerate large-scale sensor rollouts in agriculture and environment monitoring.

Platform Convergence: Unified IoT platforms integrate satellite M2M with LTE-M and NB-IoT, providing seamless failover and centralized device management.

Data Monetization: Subscription plans are evolving—moving from per-kilobyte billing to tiered, predictable data packages tailored to telemetry vs. high-bandwidth needs.

Service Ecosystem: Managed connectivity services bundle hardware, airtime, and analytics, simplifying deployments for enterprises without in-house satellite expertise.

Market Drivers

Remote Asset Visibility: Demand for real-time monitoring of pipelines, offshore platforms, and mining equipment drives satellite M2M adoption where cellular is absent.

Regulatory Compliance: Mandates for global tracking (e.g., IMO’s GMDSS, aviation ELT requirements) necessitate satellite connectivity for safety and reporting.

Smart Agriculture: Precision farming—soil moisture sensors, livestock trackers—leverages satellite M2M to optimize yields in rural areas.

Logistics & Fleet Management: Global shipment tracking and cold-chain monitoring require ubiquitous, tamper-proof data links.

Energy Transition: Distributed renewable assets (wind turbines, solar farms) in remote locales employ satellite M2M for condition monitoring and predictive maintenance.

Market Restraints

Power Constraints: Battery-powered M2M devices face energy challenges transmitting via high-power satellite links, limiting reporting frequency.

Spectrum Congestion: Allocation of S-band and L-band spectrum for mega-constellations may create interference risks for legacy services.

Regulatory Complexity: Cross-border licensing and customs clearance for satellite terminals complicate global rollouts.

Latency Sensitivity: Some time-critical M2M control loops still prefer terrestrial low-latency networks over GEO links.

Total Cost of Ownership: Higher airtime fees compared to cellular can deter adoption for non-mission-critical, high-volume data transmissions.

Market Opportunities

Hybrid Networking: Dynamic routing between terrestrial and satellite networks optimizes cost and performance for diverse M2M profiles.

LEO IoT Constellations: Purpose-built, narrowband LEO networks (e.g., Swarm Technologies, Hiber) offering ultra-low-cost connectivity for billions of sensors.

5G Integration: Satellite backhaul for private 5G campus networks in remote industrial sites, supporting both M2M and human communications.

Edge Analytics: Embedding AI at M2M terminals to preprocess data, reducing airtime usage and enabling autonomous edge decisions.

Subscription Models: Usage-based and outcome-based service contracts align costs with business value, accelerating adoption in logistics and utilities.

Market Dynamics

Vertical Specialization: Providers offer tailored end-to-end solutions (hardware, airtime, platform) for industries like maritime, mining, and agritech.

Partnership Ecosystems: Collaborations among satellite operators, IoT platform vendors, and system integrators streamline solution delivery.

Regulatory Alignment: Standardized global type approvals and harmonized customs processes reduce deployment friction.

Technological Convergence: Advances in flat-panel antennas, SDR modulation, and network virtualization enhance terminal performance and reduce costs.

Sustainability Focus: Solar-powered M2M terminals and longer device lifecycles align with corporate ESG targets and reduce field service demands.

Regional Analysis

North America: Largest market led by oil & gas, utilities, and logistics, with early LEO adoption and hybrid network experiments.

Europe: Strong maritime and rail M2M applications; regulatory support for Galileo E6C authentication boosts GNSS-satellite integration.

Asia Pacific: Rapid growth in agriculture, disaster monitoring, and supply-chain tracking; growing domestic satellite programs in India and China.

Latin America: Expanding mining and remote infrastructure projects drive GEO and LEO M2M usage; local VSAT networks evolving into IoT hubs.

Middle East & Africa: Infrastructure and telecom expansions leverage satellite M2M for power grid monitoring and rural connectivity initiatives.

Competitive Landscape

Leading Companies in the M2M Satellite Communication Market:

Inmarsat plc

Iridium Communications Inc.

Orbcomm Inc.

Globalstar, Inc.

Thuraya Telecommunications Company

Viasat, Inc.

ORBCOMM

Ligado Networks

Kymeta Corporation

SES S.A.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

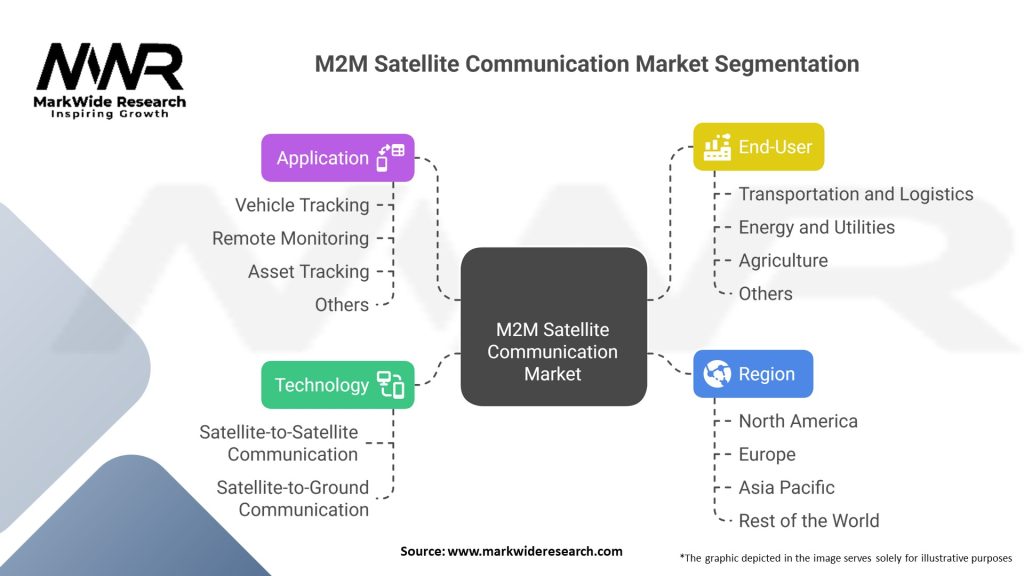

Segmentation

By Orbit: GEO, MEO, LEO, Hybrid.

By Service Type: Two-Way Data, Simplex Messaging, Tracking & Telemetry, Voice-Enabled M2M.

By Vertical: Oil & Gas, Maritime, Transportation & Logistics, Agriculture, Utilities, Mining, Public Safety.

By Subscription Model: Prepaid Airtime, Postpaid Plans, Data Packages (Metered, Unlimited), Outcome-Based SLAs.

Category-wise Insights

GEO M2M Services: Provide mature long-standing networks with 99.9% uptime; ideal for high-data-rate and voice-capable needs.

LEO M2M Services: Lower latency (<100 ms) and growing capacity; perfect for time-sensitive tracking, remote control, and burst data.

Simplex M2M Messaging: Extremely low-cost, low-power devices suited for basic telemetry and cold-chain alerts.

Two-Way Data: Supports command-and-control use cases—e.g., remote actuator commands in oil & gas and power utilities.

Voice-Enabled M2M: Embedded voice channels in terminals for hybrid human-machine workflows in emergency response.

Key Benefits for Industry Participants and Stakeholders

True Global Reach: Eliminate coverage gaps in remote or offshore operations, ensuring continuous asset monitoring.

Resilience & Redundancy: Complement terrestrial networks to maintain connectivity during disasters or network outages.

Scalability: Modular terminal and subscription offerings enable rapid deployment of thousands of endpoints.

Dynamic Billing: AI-optimized data-plan recommendations based on usage patterns and predictive forecasting.

Standardized APIs: Adoption of OneM2M and OMA LwM2M for seamless application integration and device interoperability.

LEO/GEO Roaming: Automatic switching between orbits for cost and performance balance in global deployments.

Covid-19 Impact The pandemic underscored the need for remote, unmanned operations, particularly in critical infrastructure and supply-chain contexts. Many enterprises accelerated satellite M2M deployments to monitor remote assets when on-site access was restricted. Ongoing hybrid work models and digital transformation initiatives continue to prioritize resilient, automated connectivity solutions.

Key Industry Developments

Iridium partnered with Thales (2023) to integrate Certus M2M into land-mobile radios for mission-critical services.

OneWeb launched its Enterprise IoT plan (2024) targeting low-power sensors with global node-to-cloud coverage.

Swarm Technologies unveiled its Nano M2M terminal (2022), priced under $150, for ultra-wide sensor fleets.

SES introduced multi-orbit managed IoT services (2023) leveraging O3b mPOWER LEO capacity for low-latency enterprise solutions.

Analyst Suggestions

Adopt Hybrid Strategies: Combine GEO and LEO services dynamically to optimize cost, latency, and coverage for each use case.

Enhance Edge Intelligence: Deploy AI at the device edge to preprocess data, reducing airtime usage and speeding decision loops.

Standardize Device Certifications: Champion global type-approval frameworks to simplify cross-border deployments and logistics.

Offer Outcome-Based Plans: Structure subscriptions around business KPIs—uptime, data latency, throughput—rather than raw airtime volumes.

Expand Ecosystem Partnerships: Collaborate with cloud-IoT platforms, sensor manufacturers, and system integrators to deliver turnkey solutions.

Future Outlook The M2M Satellite Communication market is forecast to grow at a high-single to low-double digit CAGR through 2030, fueled by the rollout of hundreds of LEO satellites, continued expansion of IoT use cases, and declining terminal costs. As satellite ubiquity becomes a baseline expectation for mission-critical and remote operations, M2M services will integrate seamlessly with terrestrial networks, enabling universal connectivity. Edge computing, AI-driven data management, and flexible subscription models will further expand the market, underpinning the next wave of industrial digitalization.

Conclusion M2M Satellite Communication has emerged as an essential pillar of global IoT infrastructure, bridging coverage gaps and delivering automated, resilient connectivity for remote assets. Stakeholders who invest in hybrid network architectures, edge intelligence, and outcome-oriented services will unlock new operational efficiencies and revenue streams. As satellite constellations proliferate and technology converges with terrestrial IoT, M2M SATCOM will underpin the transformation of industries—from agriculture and utilities to logistics and public safety—into fully connected, data-driven enterprises.

What is M2M satellite communication?

M2M satellite communication refers to machine-to-machine communication that utilizes satellite technology to enable devices to communicate with each other without human intervention. This technology is crucial for applications in remote monitoring, asset tracking, and IoT connectivity in areas lacking terrestrial infrastructure.

Who are the key players in the M2M satellite communication market?

Key players in the M2M satellite communication market include Iridium Communications, Inmarsat, Globalstar, and SES S.A., among others. These companies provide various satellite communication services and solutions tailored for M2M applications.

What are the main drivers of growth in the M2M satellite communication market?

The main drivers of growth in the M2M satellite communication market include the increasing demand for remote monitoring solutions, the expansion of IoT applications, and the need for reliable communication in remote areas. These factors are pushing industries like agriculture, transportation, and energy to adopt satellite communication technologies.

What challenges does the M2M satellite communication market face?

The M2M satellite communication market faces challenges such as high operational costs, limited bandwidth, and regulatory hurdles. These issues can hinder the deployment of satellite communication solutions, particularly in competitive sectors.

What opportunities exist in the M2M satellite communication market?

Opportunities in the M2M satellite communication market include the growing demand for smart city solutions, advancements in satellite technology, and the increasing adoption of connected devices. These trends are likely to create new applications and enhance service offerings.

What trends are shaping the M2M satellite communication market?

Trends shaping the M2M satellite communication market include the integration of AI and machine learning for data analysis, the rise of low Earth orbit (LEO) satellite constellations, and the increasing focus on cybersecurity measures. These trends are expected to enhance the efficiency and security of M2M communications.

Leading Companies in the M2M Satellite Communication Market:

Inmarsat plc

Iridium Communications Inc.

Orbcomm Inc.

Globalstar, Inc.

Thuraya Telecommunications Company

Viasat, Inc.

ORBCOMM

Ligado Networks

Kymeta Corporation

SES S.A.

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA

What This Study Covers

✔ Which are the key companies currently operating in the market?

✔ Which company currently holds the largest share of the market?

✔ What are the major factors driving market growth?

✔ What challenges and restraints are limiting the market?

✔ What opportunities are available for existing players and new entrants?

✔ What are the latest trends and innovations shaping the market?

✔ What is the current market size and what are the projected growth rates?

✔ How is the market segmented, and what are the growth prospects of each segment?

✔ Which regions are leading the market, and which are expected to grow fastest?

✔ What is the forecast outlook of the market over the next few years?

✔ How is customer demand evolving within the market?

✔ What role do technological advancements and product innovations play in this industry?

✔ What strategic initiatives are key players adopting to stay competitive?

✔ How has the competitive landscape evolved in recent years?

✔ What are the critical success factors for companies to sustain in this market?

Why Choose MWR ?

Trusted by Global Leaders Fortune 500 companies, SMEs, and top institutions rely on MWR’s insights to make informed decisions and drive growth.

ISO & IAF Certified Our certifications reflect a commitment to accuracy, reliability, and high-quality market intelligence trusted worldwide.

Customized Insights Every report is tailored to your business, offering actionable recommendations to boost growth and competitiveness.

Multi-Language Support Final reports are delivered in English and major global languages including French, German, Spanish, Italian, Portuguese, Chinese, Japanese, Korean, Arabic, Russian, and more.

Unlimited User Access Corporate License offers unrestricted access for your entire organization at no extra cost.

Free Company Inclusion We add 3–4 extra companies of your choice for more relevant competitive analysis — free of charge.

Post-Sale Assistance Dedicated account managers provide unlimited support, handling queries and customization even after delivery.

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.

"MarkWide Research has been a valuable partner for us in obtaining the market insights we need to

make informed business decisions. Their research reports are comprehensive, accurate, and

delivered in a timely manner. We appreciate their professionalism and attention to detail, and would

highly recommend their services to other companies."

"We have been working with MarkWide Research for several years now, and they have consistently

provided us with high-quality market research reports that have helped us stay ahead of the

competition. Their team is responsive, knowledgeable, and easy to work with. We look forward to

continuing our partnership with them in the years to come."

"MarkWide Research is an excellent market research provider that delivers valuable insights to help

us understand the market and industry trends. Their reports are always well researched,

comprehensive, and insightful. We have been very pleased with their services and would highly

recommend them to other organizations."

"We have been working with MarkWide Research for a number of years now, and we have found

their market research reports to be invaluable in helping us make strategic decisions for our

business. Their team is knowledgeable, responsive, and always delivers high-quality work. We highly

recommend their services to anyone looking for reliable market research."

"MarkWide Research is a trusted partner that provides us with the market insights we need to make

informed decisions. Their reports are thorough, accurate, and delivered on time. We appreciate

their professionalism and expertise, and would highly recommend their services to other companies

looking for reliable market research."

GET A FREE SAMPLE REPORT

This free sample study provides a complete overview of the report, including executive summary, market segments, competitive analysis, country level analysis and more.