444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The 3D IC and 2.5D IC packaging market has witnessed significant growth in recent years due to the rising demand for compact and high-performance electronic devices. These advanced packaging technologies have revolutionized the semiconductor industry by enhancing device functionality, reducing form factor, and improving overall performance. As technology continues to evolve, the demand for 3D IC and 2.5D IC packaging is expected to surge further, driving innovations and propelling the market to new heights.

Meaning

3D IC and 2.5D IC packaging refer to advanced packaging techniques used in the semiconductor industry to vertically stack multiple integrated circuits (ICs) or dies within a single package. Unlike traditional 2D IC packaging, which places ICs side by side on a single plane, 3D IC and 2.5D IC packaging enable the integration of multiple ICs, memory, and other components on top of each other, resulting in enhanced performance and reduced footprint.

Executive Summary

The 3D IC and 2.5D IC packaging market have experienced robust growth over the past few years, driven by the increasing demand for compact and powerful electronic devices in various industries. The market’s growth can be attributed to the numerous benefits offered by 3D and 2.5D packaging, including improved performance, reduced power consumption, and smaller form factors. This report aims to provide valuable insights into the market dynamics, key trends, regional analysis, and competitive landscape of the 3D IC and 2.5D IC packaging market.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The 3D IC and 2.5D IC packaging market are influenced by several dynamic factors, including technological advancements, market collaborations, and the evolving demands of end-user industries. The market is expected to witness continued growth as industry players focus on R&D and form strategic alliances to address the challenges associated with 3D IC and 2.5D IC packaging.

Regional Analysis

Competitive Landscape

Leading Companies in the 3D IC and 2.5D IC Packaging Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

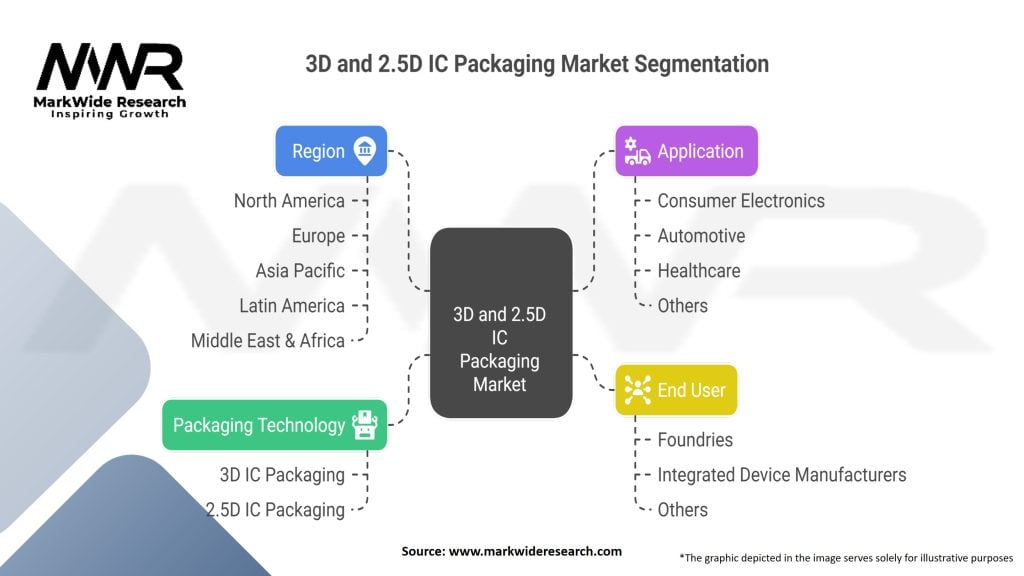

Segmentation

The 3D IC and 2.5D IC packaging market can be segmented based on the following factors:

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Strengths:

Weaknesses:

Opportunities:

Threats:

Market Key Trends

Covid-19 Impact

The COVID-19 pandemic has had a mixed impact on the 3D IC and 2.5D IC packaging market. While the initial outbreak disrupted supply chains and manufacturing operations, the growing demand for electronic devices during lockdowns and remote working spurred the market growth. The pandemic accelerated the adoption of IoT, AI, and cloud technologies, driving the demand for high-performance semiconductors and advanced packaging solutions.

Key Industry Developments

Analyst Suggestions

Future Outlook

The future of the 3D IC and 2.5D IC packaging market looks promising, with the increasing demand for miniaturized, energy-efficient electronic devices. As semiconductor technology advances and new applications emerge, the adoption of 3D IC and 2.5D IC packaging is expected to grow significantly. Companies that focus on innovation, collaboration, and cost-effective solutions will be well-positioned to capitalize on the market opportunities.

Conclusion

The 3D IC and 2.5D IC packaging market is on a growth trajectory, driven by the demand for compact, powerful, and energy-efficient electronic devices across various industries. The continuous advancements in semiconductor fabrication technologies, along with increasing applications of AI, IoT, and 5G, present lucrative opportunities for market participants. However, challenges related to design complexity, thermal management, and IP protection should be addressed through strategic collaborations and investments in research and development. As the market evolves, industry players must remain agile and innovative to stay competitive and meet the changing demands of the semiconductor industry.

What are 3D IC and 2.5D IC packaging?

3D IC and 2.5D IC packaging refer to advanced semiconductor packaging technologies that allow multiple integrated circuits to be stacked vertically or placed side by side on a single substrate. These methods enhance performance, reduce power consumption, and save space in electronic devices.

What companies are leading the 3D IC and 2.5D IC packaging market?

Leading companies in the 3D IC and 2.5D IC packaging market include TSMC, Intel, and ASE Group, which are known for their innovative packaging solutions and significant investments in research and development, among others.

What are the growth factors driving the 3D IC and 2.5D IC packaging market?

The growth of the 3D IC and 2.5D IC packaging market is driven by the increasing demand for high-performance computing, the rise of artificial intelligence applications, and the need for miniaturization in consumer electronics.

What challenges does the 3D IC and 2.5D IC packaging market face?

Challenges in the 3D IC and 2.5D IC packaging market include the high manufacturing costs associated with advanced packaging technologies, thermal management issues, and the complexity of integration with existing semiconductor processes.

What future opportunities exist in the 3D IC and 2.5D IC packaging market?

Future opportunities in the 3D IC and 2.5D IC packaging market include the expansion of applications in the Internet of Things (IoT), automotive electronics, and enhanced mobile devices, which require more efficient and compact packaging solutions.

What trends are shaping the 3D IC and 2.5D IC packaging market?

Trends in the 3D IC and 2.5D IC packaging market include the increasing adoption of heterogeneous integration, advancements in materials for better thermal performance, and the growing focus on sustainability in semiconductor manufacturing.

3D IC and 2.5D IC Packaging Market

| Segmentation | Details |

|---|---|

| Packaging Technology | 3D IC Packaging, 2.5D IC Packaging |

| Application | Consumer Electronics, Automotive, Healthcare, Others |

| End User | Foundries, Integrated Device Manufacturers, Others |

| Region | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the 3D IC and 2.5D IC Packaging Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

North America

o US

o Canada

o Mexico

Europe

o Germany

o Italy

o France

o UK

o Spain

o Denmark

o Sweden

o Austria

o Belgium

o Finland

o Turkey

o Poland

o Russia

o Greece

o Switzerland

o Netherlands

o Norway

o Portugal

o Rest of Europe

Asia Pacific

o China

o Japan

o India

o South Korea

o Indonesia

o Malaysia

o Kazakhstan

o Taiwan

o Vietnam

o Thailand

o Philippines

o Singapore

o Australia

o New Zealand

o Rest of Asia Pacific

South America

o Brazil

o Argentina

o Colombia

o Chile

o Peru

o Rest of South America

The Middle East & Africa

o Saudi Arabia

o UAE

o Qatar

o South Africa

o Israel

o Kuwait

o Oman

o North Africa

o West Africa

o Rest of MEA