444 Alaska Avenue

Suite #BAA205 Torrance, CA 90503 USA

+1 424 999 9627

24/7 Customer Support

sales@markwideresearch.com

Email us at

Market Overview

The Australia LNG bunkering market refers to the industry involved in the supply and distribution of liquefied natural gas (LNG) as a marine fuel in Australia. With the growing emphasis on cleaner energy sources and the need to reduce greenhouse gas emissions in the shipping industry, LNG bunkering has emerged as a viable alternative to traditional marine fuels. LNG is a cleaner-burning fuel compared to heavy fuel oil and diesel, offering environmental benefits such as reduced carbon dioxide, sulfur oxide, and nitrogen oxide emissions.

Meaning

LNG bunkering refers to the process of supplying LNG to ships for use as fuel. It involves the transfer of LNG from storage facilities to vessels either through ship-to-ship transfer or shore-to-ship transfer. LNG bunkering infrastructure typically includes storage tanks, transfer systems, and refueling equipment. The LNG bunkering market in Australia plays a crucial role in facilitating the adoption of LNG as a marine fuel, enabling ship operators to comply with stricter environmental regulations.

Executive Summary

The Australia LNG bunkering market has witnessed significant growth in recent years, driven by various factors such as increasing environmental concerns, stringent emissions regulations, and the need for cleaner fuel alternatives. The market offers immense potential for both domestic and international players involved in LNG production, distribution, and infrastructure development. However, it also faces challenges related to infrastructure availability, investment requirements, and regulatory frameworks.

Important Note: The companies listed in the image above are for reference only. The final study will cover 18–20 key players in this market, and the list can be adjusted based on our client’s requirements.

Key Market Insights

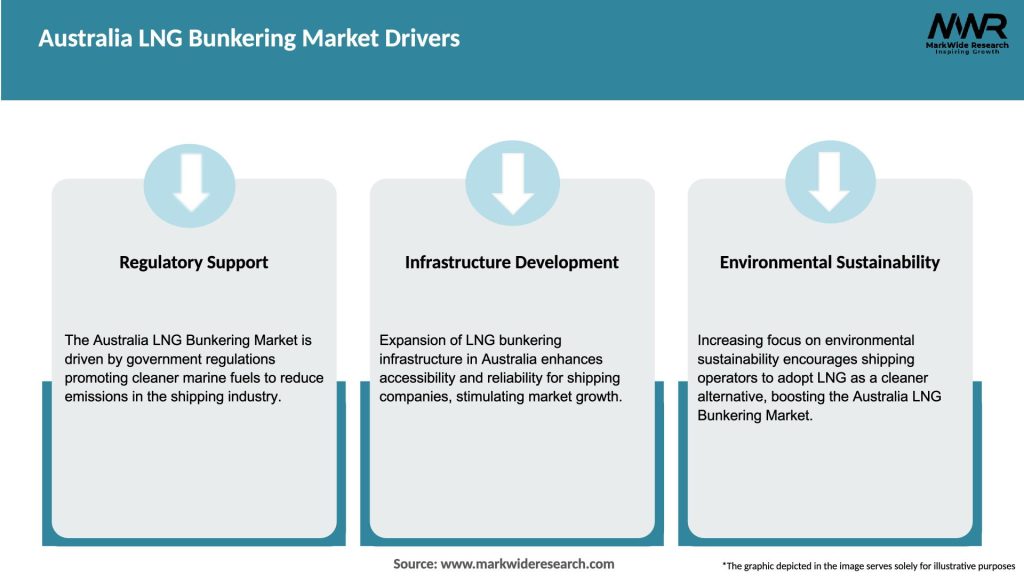

Market Drivers

Market Restraints

Market Opportunities

Market Dynamics

The Australia LNG bunkering market is influenced by various dynamics, including regulatory developments, technological advancements, market competition, and customer preferences. The market is characterized by a growing focus on environmental sustainability, increasing investments in infrastructure, and the emergence of new LNG bunkering players. The demand for LNG bunkering services is expected to increase as more shipowners and operators recognize the economic and environmental benefits of LNG as a marine fuel.

Regional Analysis

Australia’s vast coastline and strategic geographic location position it as a promising market for LNG bunkering. Major ports such as Sydney, Melbourne, Brisbane, and Perth offer significant opportunities for LNG bunkering infrastructure development. The country’s strong trade relationships with countries in the Asia-Pacific region further enhance the market’s potential. However, regional variations in regulatory frameworks and infrastructure availability may impact the pace of market growth across different states and territories.

Competitive Landscape

Leading Companies in the Australia LNG Bunkering Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.

Segmentation

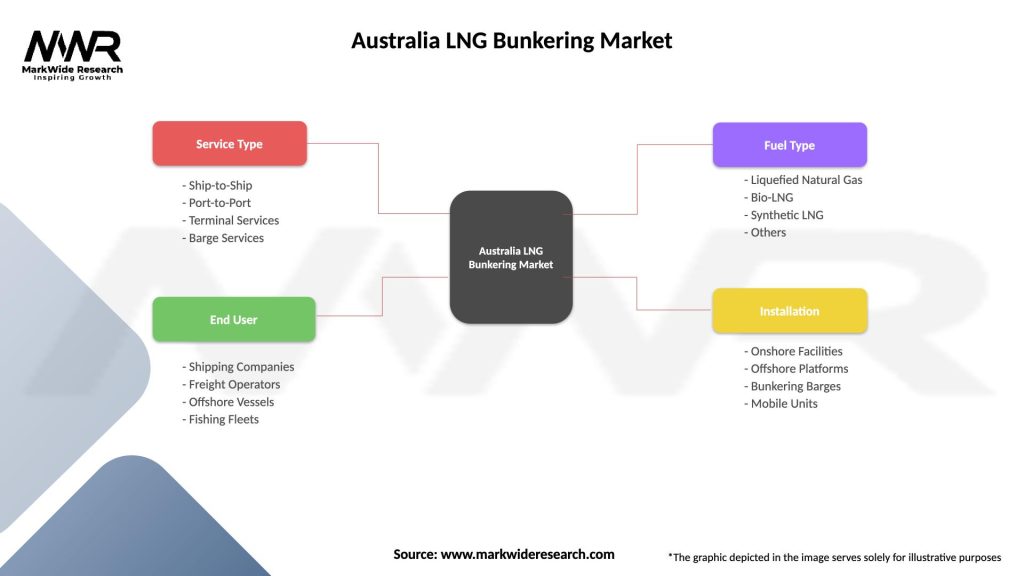

The Australia LNG bunkering market can be segmented based on various factors, including:

Category-wise Insights

Key Benefits for Industry Participants and Stakeholders

SWOT Analysis

Strengths:

Weaknesses:

Opportunities:

Threats:

Market Key Trends

Covid-19 Impact

The COVID-19 pandemic has had both short-term and long-term impacts on the Australia LNG bunkering market. In the short term, the pandemic disrupted global trade and shipping activities, leading to a decline in demand for LNG bunkering services. Travel restrictions, reduced vessel operations, and economic uncertainties resulted in a temporary slowdown in the market. However, the long-term impact of the pandemic has reinforced the importance of environmental sustainability and emissions reduction, driving the demand for cleaner marine fuels like LNG. As the industry recovers and adapts to the new normal, the Australia LNG bunkering market is expected to regain momentum.

Key Industry Developments

Analyst Suggestions

Future Outlook

The Australia LNG bunkering market is poised for significant growth in the coming years. With increasing environmental concerns and the need for cleaner marine fuels, LNG bunkering offers a viable solution to reduce emissions in the shipping industry. The expansion of LNG bunkering infrastructure, harmonization of regulatory frameworks, and collaboration among industry stakeholders will drive market development. Australia has the potential to become a regional LNG bunkering hub, serving both domestic vessels and international ships traversing the Asia-Pacific region.

Conclusion

The Australia LNG bunkering market presents substantial opportunities for the adoption of LNG as a marine fuel. As the shipping industry seeks cleaner and more sustainable alternatives to traditional fuels, LNG bunkering emerges as a viable solution. The market is driven by environmental concerns, stringent emissions regulations, and the availability of abundant natural gas reserves in Australia. However, challenges such as limited infrastructure availability, capital-intensive nature, and regulatory frameworks need to be addressed. Through collaborative partnerships, infrastructure investments, and regulatory advancements, the Australia LNG bunkering market can foster sustainable growth and contribute to a greener maritime industry.

What is LNG Bunkering?

LNG Bunkering refers to the process of supplying liquefied natural gas (LNG) as fuel to ships and vessels. This method is gaining traction due to its environmental benefits and compliance with international regulations on emissions.

What are the key players in the Australia LNG Bunkering Market?

Key players in the Australia LNG Bunkering Market include Woodside Petroleum, Shell Australia, and Santos, among others. These companies are involved in the development and supply of LNG for maritime applications.

What are the growth factors driving the Australia LNG Bunkering Market?

The Australia LNG Bunkering Market is driven by the increasing demand for cleaner marine fuels, stringent emission regulations, and the expansion of LNG infrastructure in ports. Additionally, the shift towards sustainable shipping practices is contributing to market growth.

What challenges does the Australia LNG Bunkering Market face?

Challenges in the Australia LNG Bunkering Market include the high initial investment for infrastructure development and the need for regulatory compliance. Additionally, competition from alternative fuels and technologies poses a challenge to market players.

What opportunities exist in the Australia LNG Bunkering Market?

Opportunities in the Australia LNG Bunkering Market include the potential for expanding LNG supply chains and the development of new bunkering facilities. Furthermore, partnerships between shipping companies and LNG suppliers can enhance market growth.

What trends are shaping the Australia LNG Bunkering Market?

Trends in the Australia LNG Bunkering Market include the adoption of digital technologies for efficient operations and the increasing focus on sustainability. Additionally, the growth of the offshore and shipping industries is influencing the demand for LNG as a marine fuel.

Australia LNG Bunkering Market

| Segmentation Details | Description |

|---|---|

| Service Type | Ship-to-Ship, Port-to-Port, Terminal Services, Barge Services |

| End User | Shipping Companies, Freight Operators, Offshore Vessels, Fishing Fleets |

| Fuel Type | Liquefied Natural Gas, Bio-LNG, Synthetic LNG, Others |

| Installation | Onshore Facilities, Offshore Platforms, Bunkering Barges, Mobile Units |

Please note: The segmentation can be entirely customized to align with our client’s needs.

Leading Companies in the Australia LNG Bunkering Market:

Please note: This is a preliminary list; the final study will feature 18–20 leading companies in this market. The selection of companies in the final report can be customized based on our client’s specific requirements.